Submarine Cables Market Outlook:

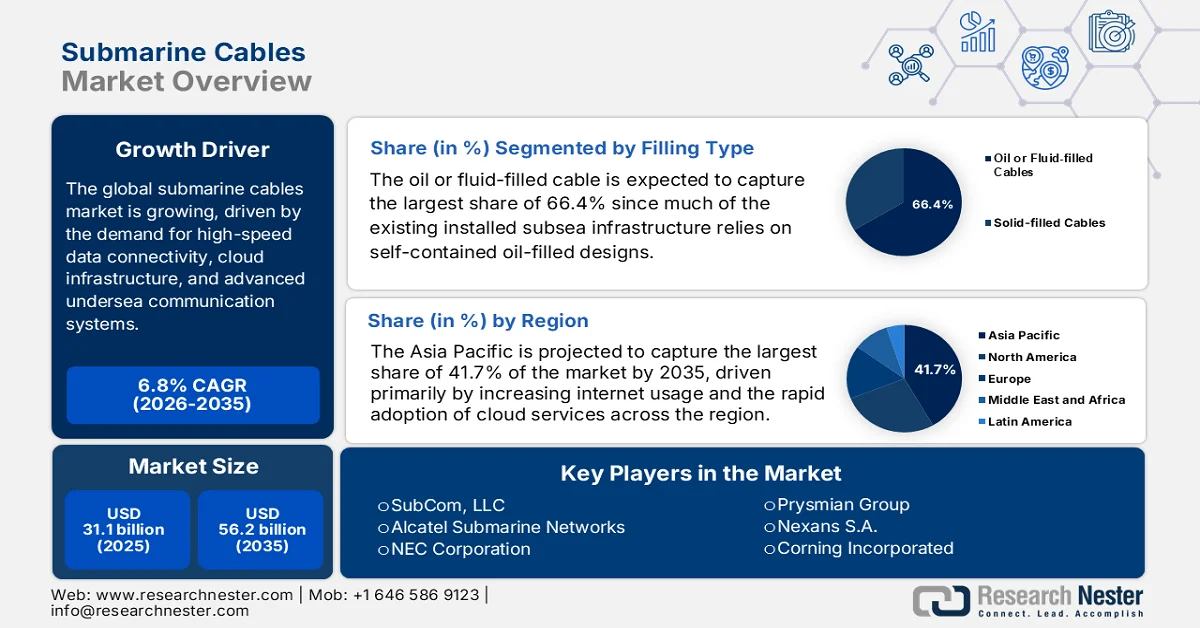

Submarine Cables Market size was valued at USD 31.1 billion in 2025 and is anticipated to be USD 56.2 billion by the end of 2035, rising at a CAGR of 6.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of submarine cables is assessed at USD 33.3 billion.

The global submarine cables market is growing based on factors such as heightened demand for high-speed data connectivity, cloud infrastructure, and advanced undersea communication systems worldwide. In January 2026, the U.S. Trade and Development Agency (USTDA) reported that it is supporting the SCNX3 submarine cable project by connecting India with Singapore and other data hubs in Southeast Asia by funding a feasibility study, which was led by Florida-based APTelecom LLC. Besides, this initiative aims to deploy secure U.S.-made cable technology, enhancing network resilience, protecting sensitive data, and expanding capacity for AI and cloud services across a population of 1.85 billion. The project will create encouraging opportunities for hardware, software, and service providers by improving digital access and route diversity in the region, hence positively impacting market growth.

Furthermore, the rapid expansion of global internet infrastructure and the growing demand for high-speed data transmission are also stimulating consistent progress in the market. In June 2023 Telecom Regulatory Authority of India reported that submarine communication cables are the backbone of the global digital economy, which are carrying nearly 99% of international internet traffic and serving as critical infrastructure for nations. It also mentioned that globally, there are more than 486 cable systems spanning 1.3 million kilometers, and heavy investments are being made in new builds to meet surging demand driven by cloud services, mobile technology, and 5G. Tech giants such as Google, Meta, Amazon, and Microsoft are now major cable owners who are pushing innovations in fiber capacity and route diversity, hence positively impacting the market’s growth and exposure over the years ahead.

Key Submarine Cable System Market Insights Summary:

Regional Highlights:

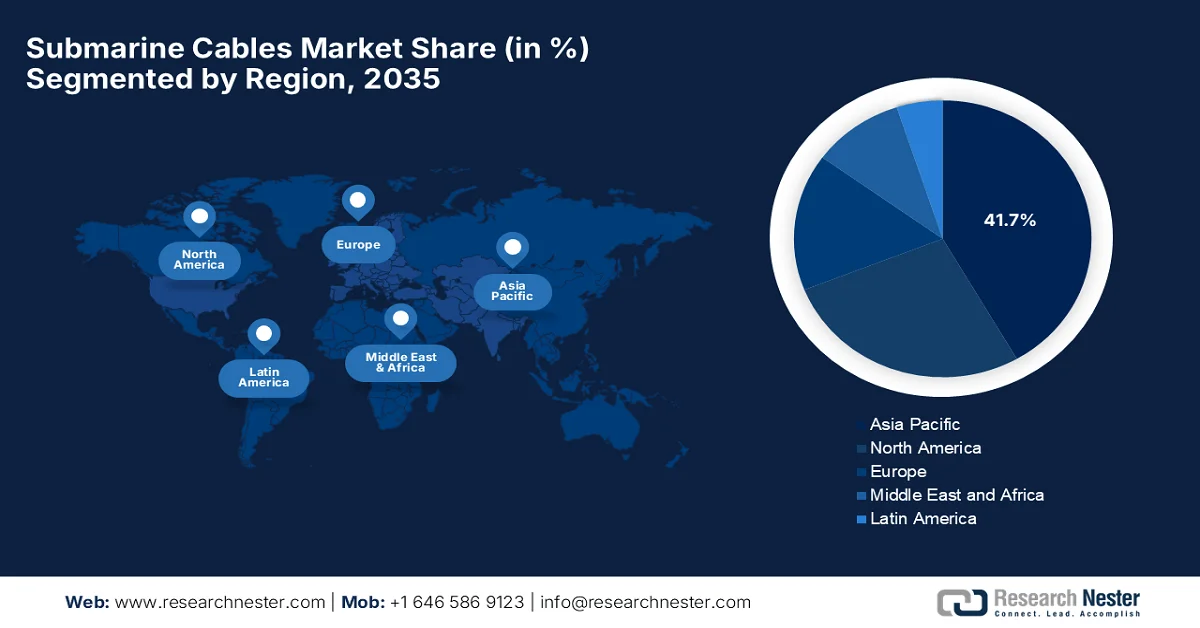

- Asia Pacific submarine cables market is projected to command a 41.7% share by 2035, attributed to rising internet demand supported by rapid digitalization and expanding cloud adoption across regional economies.

- North America is anticipated to secure a notable share in the market by 2035, stimulated by expanding high-capacity fiber routes and investments in resilient undersea communication infrastructure.

Segment Insights:

- The oil or fluid-filled cable segment in the submarine cables market is forecast to capture a 66.4% share by 2035, propelled by continued reliance on existing subsea infrastructure utilizing self-contained oil-filled cable designs.

- Dry plant products within the component segment are expected to obtain a considerable share during 2026–2035, supported by the growing need for advanced network monitoring, reliability, and long-haul subsea signal management systems.

Key Growth Trends:

- Expansion of offshore renewable energy projects

- Connectivity demand

Major Challenges:

- High capital expenditure and project complexity

- Geopolitical and security concerns

Key Players: SubCom, LLC (U.S.), Alcatel Submarine Networks (France), NEC Corporation (Japan), Prysmian Group (Italy), Nexans S.A. (France), Corning Incorporated (U.S.), Hengtong Marine Cable Systems (China), LS Cable & System Ltd. (South Korea), Fujitsu Limited (Japan), Sumitomo Electric Industries, Ltd. (Japan), Huawei Marine Networks Co., Ltd. (China), KEI Industries Ltd. (India), Hawaiki Cable Limited (Australia), Telekom Malaysia Berhad (Malaysia), Global Marine Systems Limited (UK), SUBCO Pty Ltd (Australia), NTT DATA Corporation (Japan), Sumitomo Corporation (Japan), JA Mitsui Leasing, Ltd. (Japan), Intra-Asia Marine Networks Co., Ltd. (Japan), OMS Group (Malaysia).

Global Submarine Cable System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 31.1 billion

- 2026 Market Size: USD 33.3 billion

- Projected Market Size: USD 56.2 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.7% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, Singapore, South Korea, Australia, United Arab Emirates

Last updated on : 11 March, 2026

Submarine Cables Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of offshore renewable energy projects: Increasing investments in terms of offshore wind farms globally, especially in Europe, Asia Pacific, and North America, require these submarine power cables to transmit electricity to shore. Transition to renewable energy targets efficiently boosts demand for power-grade undersea cables for transformer stations, HVDC links, and grid connections. In March 2025, EnBW announced that it had begun laying the first of 64 submarine cables for the 960 MW He Dreiht offshore wind farm in the North Sea, with approximately 100 kilometers of 66-kV inner-array cables being installed to connect all turbines. Besides, the project’s internal grid will link to an offshore converter platform operated by TenneT, where electricity will be converted to DC and transmitted to shore through two high-voltage DC export cables hence suitable for driving the overall submarine cables market.

- Connectivity demand: Almost all of the internet traffic travels through the undersea fiber optic cables; therefore, the rising cloud services increase the demand for more and higher-capacity submarine communication links. Also, the growth in 5G networks, IoT, and large data centers, which require high-bandwidth, low-latency routes, drives the growth of the market. The article, which was published by 5G Americas in April 2025, revealed that based on the industry-validated analysis, 5G has reached a global inflection point with over 2.25 billion connections, maturing from early hype into a foundational infrastructure driving economic and digital transformation. It also notes that the consumer adoption of 5G has been rapid, and the evolution toward 5G-advanced will unlock more advanced capabilities, hence denoting a positive market outlook.

- Oil & gas sector demand: The aspect of electrification of offshore oil and gas platforms is emerging as a significant driver, uplifting the submarine cables market. Traditionally powered by onboard gas turbines or diesel generators, most of the offshore installations are now being connected to onshore electricity grids through high-voltage submarine cables to reduce emissions and improve energy efficiency. In August 2023, Equinor reported that it had inaugurated the Hywind Tampen floating offshore wind farm, which now supplies renewable power to the Gullfaks and Snorre oil and gas platforms in the North Sea. It has a capacity of 88 MW from 11 floating turbines; the project meets around 35% of the electricity demand of five offshore platforms, using subsea power connections to replace gas turbine generation, denoting a positive outlook for market growth.

Global Submarine Cable Projects 2024-2026: Capacity Expansion & Strategic Connectivity Analysis

|

Year |

Company / Project |

Region |

Submarine Cable System |

Market Opportunity |

|

2026 |

Trans Pacific Networks (TPN) + Ciena |

U.S. - Southeast Asia |

Echo & Tabua |

High-speed, low-latency connectivity; supports AI workloads and cloud services; strategic transpacific expansion |

|

2026 |

NTT DATA, Sumitomo, JA Mitsui (I-AM NW) |

Japan - Malaysia - Singapore + Korea, Philippines, Taiwan |

Intra-Asia Marine (I-AM) Cable |

Flexible WSS and SDM tech; 320 Tbps; strengthens Asia-Pacific digital infrastructure. |

|

2026 |

NEC & Nokia / Eletronet |

Brazil |

Eletronet Optical Fiber Network |

8,000 km fiber expansion; high-speed backbone modernization; supports low-latency & AI traffic |

|

2024 |

Nexans + Equinor |

Northern Europe |

Power / Subsea cables (3,000 km) |

Contingency & repair contract; ensures resilience of energy and data submarine cables |

Source: Company Official Press Releases

Challenges

- High capital expenditure and project complexity: The projects in submarine cables mostly show higher capital expenditure for long-haul systems. The design, manufacturing, and installation of undersea cables require specialized vessels, optical technologies, and experienced engineering teams, which adds burgeoning costs on manufacturers. Also, most of the projects necessitate careful route planning to avoid any type of geological hazards, environmentally sensitive areas, and busy shipping lanes. In this context, the aspect of unexpected delays in permitting, weather, or technical issues can also increase the costs. Moreover, the long project timelines, sometimes spanning years from design to ready for service, can cause regulatory and technological risks negatively impacting the growth of the market.

- Geopolitical and security concerns: The submarine cables are considered to be one of the most critical national infrastructures that carry the global data traffic. This makes them targets for geopolitical tensions, espionage, and sabotage. Also, any type of disputes over territorial waters, regulatory control, or international consortium participation can delay projects or restrict access. Governments across different nations impose security requirements and ownership restrictions, especially for strategic or cross-border routes. On the other hand, physical threats, such as deliberate cable cuts, cyberattacks on network management systems, and interference from foreign actors, can disrupt global communications. Therefore, operators in the market need to invest in monitoring, cybersecurity, and resilient routing strategies.

Submarine Cables Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 31.1 billion |

|

Forecast Year Market Size (2035) |

USD 56.2 billion |

|

Regional Scope |

|

Submarine Cables Market Segmentation:

Filling Type Segment Analysis

The oil or fluid-filled cable segment is expected to maintain a leading position, capturing the largest share of 66.4% in the submarine cables market by 2035. The dominance of the subtype is highly propelled by the fact that much of the existing installed subsea infrastructure still relies on self-contained oil-filled designs. Energy Networks Association reported that the Fluid-Filled Cable (FFC) Care Phase 3 project in Great Britain, which ran from March 2023 to September 2024, tackles the technical and environmental challenge of oil loss from FFCs, which totals around 375,000 L on a yearly basis. The initiative introduces Anagen, which is a self-healing dielectric fluid that functions as normal insulation oil but solidifies to seal breaches. It reduces the need for costly repairs or replacements, where a single leak can cost around USD 55,000, and replacing EHV FFC circuits can reach USD 610,000 per km, and it aims to make self-healing fluids standard practice in GB’s FFC networks.

Component Segment Analysis

Dry plant products, which are a part of the component segment is forecasted to hold a significant share in the market during the discussed timeframe. The aspects of network reliability, management, and monitoring capabilities become more critical as overall capacity scales. These systems support signal processing and long-haul integration across vast underwater links. In November 2025, Alcatel Submarine Networks and Elwave announced that they had entered into a partnership to deploy electric-field sensors for enhanced monitoring and inspection of subsea telecommunication cables. The technology enables autonomous tracking of laid and buried cables, measures burial depth, and integrates with subsea drones to support maintenance across telecom, offshore wind, and pipeline applications, hence denoting a positive market outlook.

End use Segment Analysis

By the conclusion of the forecast period, the telecommunication is expected to grow with a considerable share in the market. The long-haul subsea construction is the main factor behind the sub-segment’s leadership. On the other hand, the booming internet traffic, coupled with the heightened demand for high-speed connectivity between continents, also positions the subtype at the forefront of revenue generation in this sector. Expansion of data centers and cloud services is fueling the need for additional long-haul subsea links. Meanwhile, the improvements in fiber-optic technology, including higher-capacity and low-latency cables, are also supporting this trend. Furthermore, geopolitical initiatives and national broadband strategies are encouraging investments in secure and resilient submarine communication networks, hence denoting a wider segment scope.

Our in-depth analysis of the submarine cables market includes the following segments:

|

Segment |

Subsegments |

|

Filling Type |

|

|

Component |

|

|

End use |

|

|

Application |

|

|

Type |

|

|

Offering |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Submarine Cables Market - Regional Analysis

APAC Market Insights

The Asia Pacific submarine cables market is expected to capture the largest share of 41.7% over the forecasted years. The region’s leadership is highly driven by rising internet demand, fueled by rapid digitalization and cloud adoption across the central countries. Also, the nations are actively participating in expanding and upgrading undersea network infrastructure to support cloud, internet, and cross-continent data flows. According to the data which was kept forward by the Organization for Economic Co-operation and Development (OECD) in December 2023, the mobile broadband subscriptions surged to more than 769 million in 2022, which is a tenfold increase when compared to a decade ago. Besides, Singapore leads with high fixed broadband penetration and submarine cable capacity. Furthermore, the report recommends strengthening independent regulators, streamlining infrastructure deployment, and fostering private sector participation to ensure inclusive digital transformation across the region.

Asia Pacific Submarine Cable Projects (2023-2026): Officially-Reported Data on Completed and Planned Undersea Networks

|

Year |

Cable Name |

Length (km) |

Details |

|

2025 |

Echo |

17,184 |

Connecting Agat & Piti (Guam), Tanjung Pakis (Indonesia), Ngeremlengui (Palau), Changi North (Singapore), Eureka (U.S.) |

|

2026 |

TAMTAM Cable |

375 |

Connecting Wé (New Caledonia) to Port Vila (Vanuatu) |

|

2026 |

South Pacific Connect Interlink |

- |

Connecting Fiji to French Polynesia, ports TBD |

|

2026 |

Honomoana |

- |

Connecting Australia (Sydney & Melbourne), France-Polynesia (TBD), New Zealand (Auckland), USA (TBD) |

|

2026 |

Tabua |

- |

Connecting Fiji (TBD), Australia (Sydney), U.S. (TBD) |

|

2026 |

Bulikula |

- |

Connecting Fiji (TBD), Tuvalu (Funafuti), Papua New Guinea (TBD), Guam (TBD) |

|

2025 |

East Micronesia Cable System |

2,250 |

Connecting Bairiki (Kiribati), Yaren (Nauru), Tofol (Federated States of Micronesia) to HANTRU1 Cable System (Alupang, Guam) |

|

2024 |

Timor-Leste South Submarine Cable |

600 |

Connecting Dili (Timor-Leste) to the North-West Cable System in the Timor Sea |

|

2023 |

Natitua Sud |

820 |

Connecting Tubuai and Rurutu to Hitia’a (France-Polynesia) |

|

2023 |

Tokelau Submarine Cable |

250 |

Connecting Atafu to Fakaofo (Tokelau) |

Source: UNCTAD

The sizable investments in undersea infrastructure support the expanding digital economy, and international data transmission corridors are identified as the major fueling factors for the market in China. Cable systems linking China to neighboring networks and long-distance hubs reflect the country’s focus on high-capacity connectivity and integration into broader global networks. Based on the government data, which was published in March 2025, China has become a major force in the global submarine cable industry, wherein the enterprises invested in 17 active international systems by the end of 2024 and are participating in several new projects. Companies such as HMN Tech have delivered more than 100,000 kilometers of submarine cable systems across 70 countries, positioning themselves among the top global contractors, hence suitable for bolstering the overall market growth in the country.

The focus on strengthening landing points for international data routes, rising digital service demand are responsible for uplifting the submarine cables market in India. The country’s geographic position offers strategic value for links connecting Asia, Africa, and Europe, and engaging in partnerships that enhance subsea network presence in the Indian Ocean Region, also propel growth of the country’s market. Press Information Bureau (PIB) in December 2024 reported that the International Advisory Body for Submarine Cable Resilience, which was launched by ITU to strengthen the resilience of global submarine telecom cables, carries nearly all internet traffic. It comprises 40 members worldwide, and the body will meet twice a year to guide policies, infrastructure, and best practices for reducing risks and ensuring rapid repairs. In addition, the country hosts 17 international subsea cables and multiple landing stations, contributing to wider market expansion.

North America Market Insights

The North America submarine cables market has acquired a prominent position, which is supported by extensive infrastructure linking coastal hubs across the U.S. and Canada with international networks. The region's significance as a digital traffic gateway has encouraged operators to make investments in high-capacity fiber routes and complementary systems for telecom and energy transmission. Based on the government data, which was published in September 2024, at the 79th UN General Assembly, Canada, along with 17 partner nations, issued a joint statement emphasizing the significant role of undersea cables in global communications and economic growth. The declaration also underscored the need for secure, resilient, and redundant infrastructure, considering the issues from high-risk suppliers, physical damage, and data compromise, thereby positively impacting the market’s growth and exposure.

The heightened demand for connectivity to major cloud providers and content platforms, along with expanding transoceanic cable routes, are the major factors that are efficiently boosting the U.S. submarine cables market. Policy and technological adoption trends influence the positioning of U.S. landing stations and capacity expansions. H.R.9766, which is the Undersea Cable Security and Protection Act, was introduced in the U.S. House of Representatives in September, 2024. In this context, the bill directs the Department of Homeland Security to establish an interagency working group with a prime goal to assess threats to commercial undersea telecommunications cables and landing stations, which also includes risks from foreign adversaries, natural causes, and accidental damage. It also requires reporting on private sector operators in securing and protecting these critical infrastructures, thus driving growth of the U.S. market.

The rapid expansion of digital infrastructure, supportive regulatory frameworks, and a growing reliance on cloud-based services are driving the market in Canada. The country is readily emerging as a central pillar for both national and international connectivity. Investments in subsea power cables for offshore renewable energy integration and communication links also support the Canada market’s growth. In June 2025, the country’s Ministry of Innovation, Science, and Economic Development approved a sub-delegation of authority policy to streamline international submarine cable licensing. It also notes that this reform allows senior executives who are below the ministerial level to approve routine or low-risk licensing decisions, such as name changes or renewals, thereby reducing delays and administrative burden. Therefore, stakeholders are expected to benefit from faster approvals, with timelines reduced by several weeks, hence denoting a positive outlook for the market’s expansion.

Europe Market Insights

Europe submarine cables market is primarily shaped by multiple networks of international connections that serve digital traffic flows between continents and intra-regional destinations. The region’s market is also propelled by the expansion of offshore wind farms, particularly in the North Sea and Baltic Sea, which necessitates advanced high-voltage subsea power links to transmit renewable energy to mainland grids. The article by the European Commission, which was published in February 2026, revealed that the submarine cable security report presents a Cable Security Toolbox and identifies Cable Projects of Europe’s Interest to strengthen the resilience of data and power submarine cables. It builds on the 2025 EU Action Plan and 2024/779 recommendation to provide risk assessments, mitigation measures, and guidance for prevention, detection, response, and recovery. In addition, the initiative has priority towards investments and public funding to safeguard critical intercontinental connectivity across Europe.

With the shifts toward a greener power grid, the demand for high-voltage direct current interconnectors has surged to facilitate the transmission of renewable energy from maritime wind farms to industrial hubs, thereby fostering a profitable business environment for the submarine cables market in Germany. This growth is also complemented by the country’s role as a regional data hub, which in turn necessitates robust subsea communication links to support its dense network of data centres. Federal Ministry of Transport in October 2024 revealed that Germany endorsed the New York Joint Statement on submarine cables at the UN General Assembly, joining the Europe and G7 partners in supporting nine guiding principles for secure and resilient undersea infrastructure. The statement emphasizes designing and maintaining cables with cybersecurity best practices, encouraging lower-risk operator choices, and strengthening cooperation between governments and industry.

The UK submarine cables market is growing based on its geographic position between North America and mainland Europe. The country’s market is also being fueled by the expansion of offshore wind energy, which necessitates a complex network of subsea export cables and interarray systems to connect renewable generation to the national grid. In this context, the UK government in December 2025 established the undersea infrastructure security oversight board, which is chaired by the Cabinet Office, to coordinate policy on subsea cables following recommendations from the Joint Committee on the National Security Strategy. The move responds to concerns about resilience and crisis preparedness, including risks of coordinated sabotage against transatlantic and regional connections. The government also announced its Atlantic Bastion programme, which will combine autonomous vessels, AI, warships, and patrol aircraft to protect North Atlantic cables.

Key Submarine Cables Market Players:

- SubCom, LLC (U.S.)

- Alcatel Submarine Networks (France)

- NEC Corporation (Japan)

- Prysmian Group (Italy)

- Nexans S.A. (France)

- Corning Incorporated (U.S.)

- Hengtong Marine Cable Systems (China)

- LS Cable & System Ltd. (South Korea)

- Fujitsu Limited (Japan)

- Sumitomo Electric Industries, Ltd. (Japan)

- Huawei Marine Networks Co., Ltd. (China)

- KEI Industries Ltd. (India)

- Hawaiki Cable Limited (Australia)

- Telekom Malaysia Berhad (Malaysia)

- Global Marine Systems Limited (UK)

- SUBCO Pty Ltd (Australia)

- NTT DATA Corporation (Japan)

- Sumitomo Corporation (Japan)

- JA Mitsui Leasing, Ltd. (Japan)

- Intra-Asia Marine Networks Co., Ltd. (Japan)

- OMS Group (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- SubCom is a leading U.S.-based submarine cable systems provider which is specializing in the design, manufacture, deployment, and maintenance of undersea fiber-optic networks. The company serves global carriers, hyperscalers, and government clients by offering turnkey solutions from planning to repair.

- Alcatel Submarine Networks is a predominant leader in terms of undersea cable solutions, which is delivering high-capacity, global submarine networks. The firm offers end-to-end services from network design and cable manufacturing to marine installation and maintenance.

- NEC Corporation is a Japan-based company that has a stronger presence in submarine cable systems, providing design, manufacturing, and deployment of high-capacity optical networks. Besides, the company makes investments in R&D for high-speed, low-latency systems, and it also collaborates with telecom operators to strengthen regional connectivity.

- Prysmian Group is yet another prominent player in this field that mainly focuses on energy and telecom cable solutions, including submarine systems. The firm makes investments in optical innovations, high-capacity fiber systems, and renewable energy grid connections by providing resilient deepwater solutions.

- Nexans S.A. is a leading pioneer which is specializing in power and communication cables, including submarine systems. The company is focused mainly on technological innovation, deploying advanced optical fibers, SDM technology, and deepwater installation methods.

Below is the list of some prominent players operating in the global market:

The submarine cables market is dominated by a combination of established telecommunications equipment manufacturers, specialized cable system providers, and offshore infrastructure firms. The pioneers from the U.S., Europe, and Japan benefit from extensive global deployments and turnkey system capabilities. Meanwhile, the players from the Asia Pacific are focused on regional expansions with cost-competitive offerings. Technological innovation in high-capacity fiber, SDM systems, expanded laying fleets, and joint ventures or consortium engagements are a few strategies opted for by these players to strengthen their market positions. In December 2025, Sumitomo Electric Industries, Ltd. announced that it will supply and install a 525 kV HVDC submarine cable for the Sea Link project by connecting Kent and Suffolk in the UK. The cable will be manufactured at Sumitomo Electric’s Port of Nigg facility in Scotland by supporting local jobs, the UK supply chain, and Net Zero 2050 clean energy goals.

Corporate Landscape of the Submarine Cables Market:

Recent Developments

- In January 2026, SUBCO announced its APX East submarine cable, which is an express 16‑fibre pair system connecting Australia and the U.S., and the cable offers the lowest latency, full deepwater routing without intermediate regeneration, and single‑end power feeding.

- In January 2026, NTT DATA, Sumitomo Corporation, and JA Mitsui Leasing announced the formation of Intra-Asia Marine Networks Co., Ltd. (I-AM NW) to construct and operate the Intra-Asia Marine Cable (I-AM Cable) connecting Japan, Malaysia, Singapore, and with future links to Korea, the Philippines, and Taiwan.

- In January 2026, Alcatel Submarine Networks and OMS Group reported that they were selected by Intra-Asia Marine Networks Co., Ltd. to build the I-AM Cable System that incorporates Wavelength Selective Switch (WSS) and Spatial Division Multiplexing (SDM) technologies, supporting up to 16 fiber pairs and an initial capacity of around 320 Tbps.

- Report ID: 3523

- Published Date: Mar 11, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Submarine Cable System Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.