OUR GEOGRAPHIC COVERAGE

Research Nester offers detailed reports on markets, products and services in the Middle East and Africa regions. These reports assist clients in making business decisions by providing valuable insights such, as enhancing brand visibility conducting competitive analyses understanding customer requirements identifying fresh opportunities and gaining a deeper understanding of their product/service offerings.

Middle East and Africa (Israel, GCC, North Africa, South Africa, Rest of Middle East and Africa)

The Middle East and Africa continue to emerge as a dynamic hub of global economic growth, driven by their strengths in geographic locations, natural resources, and rapid infrastructure development. Gulf countries such as Saudi Arabia and the UAE are expanding at a rapid pace other than oil through investments in renewable energy, digital infrastructure, and technology, whereas Africa sees steady growth in agriculture, construction, and services. Infrastructure development, such as transport, energy, and telecommunications, is also a major driving factor, complemented by a booming e-commerce market, expanding tourism and aviation sectors, and increasing regional integration through trade and investment partnerships.

Israel

Israel boasts a highly developed and innovation-driven industrial economy that is recognized for its technological expertise and entrepreneurial culture. Over recent decades, the country has experienced steady economic growth, and it ranked 25th in the world by nominal GDP at USD 610 billion in 2025, with a GDP per capita of USD 60,100. The country’s revenue is further accelerated through its advanced infrastructure, efficient transportation systems, and open trade policies, making it a leading hub for innovation, startups, and global business partnerships.

Technology & Innovation

- This is the backbone of Israel’s economy, with world-leading R&D, a dense startup ecosystem, and major international tech R&D centers. The country’s high-tech sector contributed to around IS 317 billion (17% of GDP) in 2024, maintaining a steady share of national output. It employed 403,000 people, which is 11.5% of the workforce, though R&D roles declined 6.5% year-over-year.

- In addition, high-tech exports reached USD 78 billion in 2024, accounting for 57% of all exports in H1 2025. Israel ranks as the 5th-largest global startup hub, with strong investment in cybersecurity, enterprise software, and software services, underscoring its worldwide innovation footprint.

- The country’s leadership is further represented through deep-tech & investment, wherein approximately 1,500 deep-tech companies operate in Israel, raising USD 28.6 billion since the last five years, i.e., 35% of all high-tech capital. The sector also produced 39 unicorns, with leading domains in AI, medical devices, semiconductors, cybersecurity, and agrifood.

Cybersecurity & ICT

- Israel is solidifying its position in terms of cybersecurity solutions, telecommunications, and software development. It has drawn around 20% of international cyber investments, the highest share outside the U.S., and has produced numerous unicorns and centaur companies in this field. In 2025, three out of every five dollars raised by startups were directed towards cybersecurity or enterprise software, highlighting concentrated strength and wide recognition for Israel-based technology innovation.

- The country’s software development and telecommunications, high-tech sector accounted for 57% of total exports in the first half of 2025, of which 72% were derived from software services. This demonstrates Israel’s dominant role in global ICT, software, and enterprise solutions. In addition, the country maintains a startup ecosystem, producing around 500 new ventures annually and fostering continued innovation in software-intensive fields, solidifying its reputation as a prominent hub for technological development and global digital infrastructure.

Biotech & Pharmaceuticals

- Strong expertise in medical research, biotechnology innovation, and generic drug production is propelling revenue in the country. Israel benefits from investment and fundraising, wherein in 2024, Israel’s life sciences sector attracted approximately USD 2.7 billion in investments by marking a 25% increase when compared to the previous year. Private investments totaled more than USD 2 billion, primarily from foreign investors, i.e., 58%, whereas the domestic investor contributions grew 62%. Venture capital remained the dominant, accounting for 84% of private funding.

- In recent years, Israel has witnessed substantial exports in medical and & biotech. In this context, the Israel Innovation Authority allocated around 500 million NIS (USD 140 million) to health-tech, supporting medical device, pharmaceutical, and digital health companies. The country’s life sciences exports also included USD 1.8 billion in pharmaceuticals and USD 3.4 billion in medical devices, with medical device exports at a five-year high. Technological advancements accelerated post-war, focusing on rehabilitation, battlefield treatment, prosthetics, and emergency care.

North Africa

North Africa generally encompasses Morocco, Algeria, Tunisia, Libya, and Egypt, with Western Sahara sometimes included. It is widely recognized for its natural resources, such as oil and gas. The region is mostly characterized by the vast Sahara Desert, which is the world’s largest hot desert, dominating much of the region’s landscape. The region’s economies are mostly diverse, with significant contributions from oil and gas, agriculture, mining, and increasingly tourism. The region also serves as a strategic crossroads between Africa, Europe, and the Middle East, influencing trade, migration, as well as geopolitics. In 2026, North Africa’s economy is projected to reach a GDP of USD 990.21 billion, with a per capita GDP of approximately USD 4,560, reflecting modest growth.

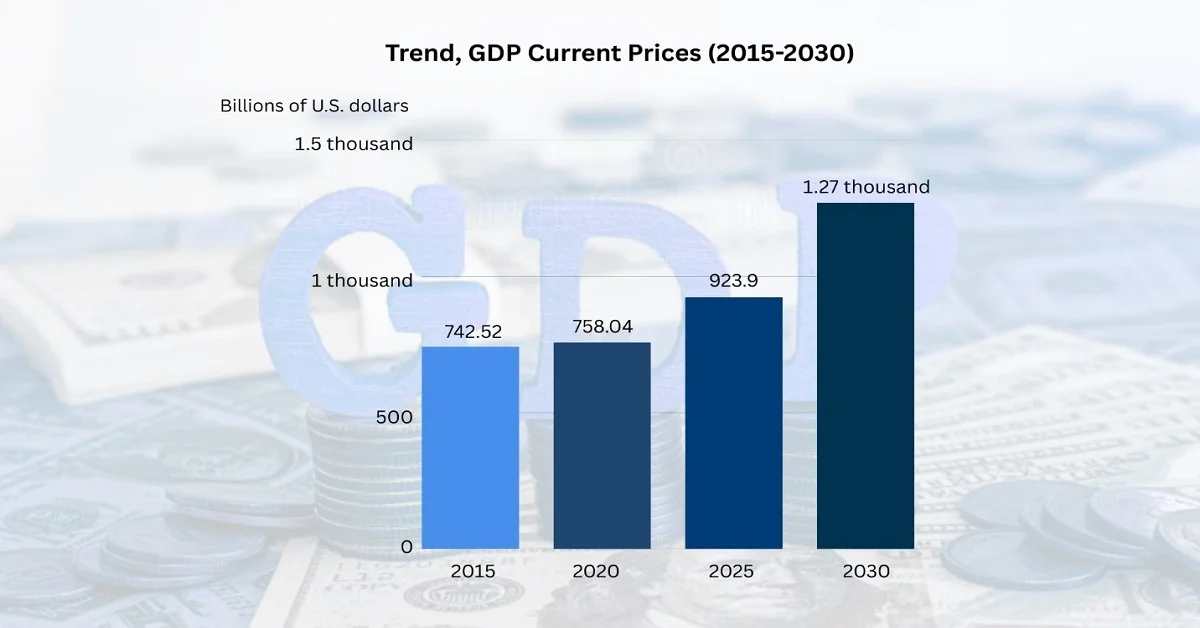

North Africa Economic Growth

Source: International Monetary Fund

Energy and Natural Resources

- North Africa is undergoing significant transformations in terms of oil and gas production, i.e., Algeria, Libya, Egypt, as well as emerging renewable energy projects, particularly solar and wind in Morocco and Egypt. Morocco is mainly focused on the expansion of its renewable energy capacity to reduce reliance on fuel imports, which currently cover 90% of its energy needs. As of 2023, total renewable capacity reached 11.42 GW, with solar at 831 MW, wind at 1,650 MW, and hydropower at 1,800 MW.

- The government of Morocco plans to increase the share of renewables in total installed capacity to 56% by the conclusion of 2030, backed strongly by MASEN’s institutional framework, updated regulatory laws, and IPP participation. Morocco also leads in terms of regional initiatives in green hydrogen production, targeting 14.6 GW of extra renewable capacity by the end of 2030 and potential exports to Europe.

- Morocco continues to import the majority of its fossil fuels but is actively diversifying its energy mix through domestic gas projects. The Gas Roadmap of 2024 includes the construction of LNG terminals at Nador West Med and Dakhla, new gas pipelines, and the expansion of combined-cycle gas turbines that totalled 836 MW. In addition, partnerships with Shell for LNG supply and ONHYM-led exploration aim to enhance energy security by efficiently phasing in renewables and green hydrogen and reduce long-term reliance on imported coal, oil, and gas.

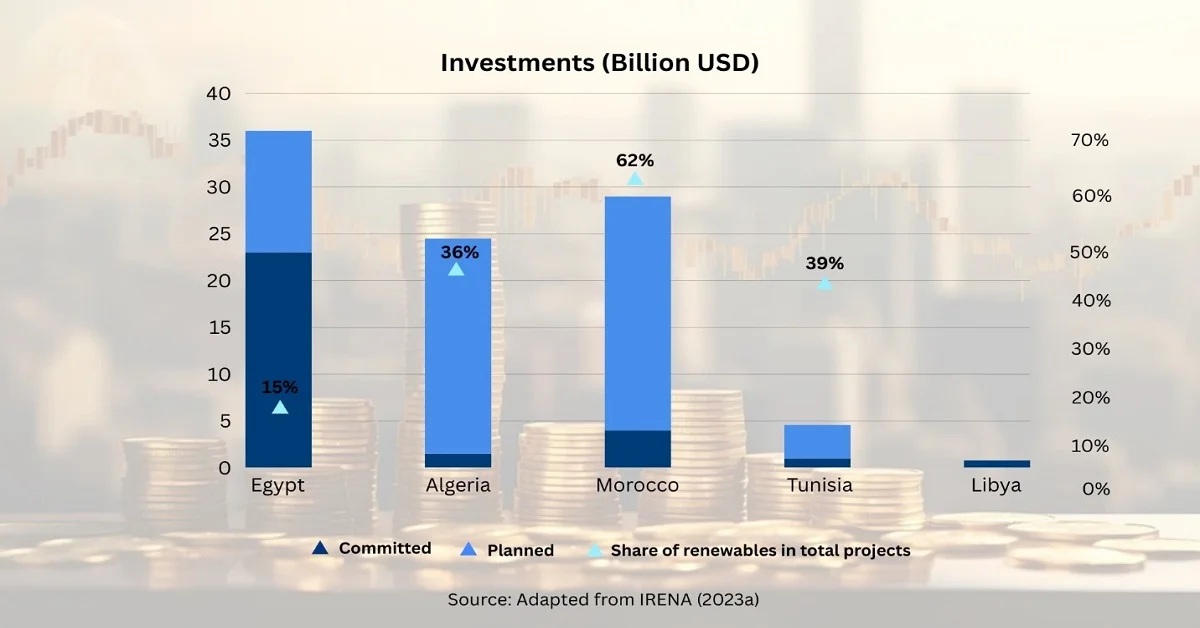

Committed vs. Planned Power Investments in North Africa (2021-2025)

Mining and Minerals

- Phosphate production in Morocco is identified as the world leader, and other minerals across the region. Approximately 97 % of Africa’s reported phosphate reserves are concentrated in Morocco, Egypt, Tunisia, and Algeria. Morocco’s Khouribga project alone holds around 26.8 billion tons, representing 45 % of the country’s phosphate reserves and maintaining its position as the world’s largest active phosphate deposit, whereas current production is heavily concentrated in North Africa and other regions.

- Despite Africa holding the largest phosphate reserves amongst all nations, the continued investments in both production and downstream processing are concentrated in North Africa. It also needs to focus on addressing infrastructure gaps, regulatory uncertainty, and limited access to finance, whereas the aspect of new exploration projects in Namibia, the Republic of Congo, and South Africa indicates significant potential for expanding production and diversifying supply across the continent.

Tourism

- Morocco has witnessed record visitor growth and foreign tourism strength by welcoming 17.4 million tourists in 2024, which is a 20% increase when compared to 2023 and 35% above previous five-year levels. Foreign tourists reached 8.8 million, which is an increase of 23%, while Moroccan citizens residing abroad accounted for 8.6 million arrivals +17%, underscoring its strong international appeal and the sector’s significant role in generating foreign exchange.

- Government-led strategy and economic importance also play an important role in strengthening North Africa’s economic position, targeted public investment, and the national tourism roadmap, originally set for 2026 but achieved ahead of schedule. The balanced share between foreign visitors 51% and expatriate Moroccans, 49% highlights tourism’s resilience and importance. The government recognizes tourism as a vital pillar of the national economy, reinforcing Morocco’s position as a key source of foreign cash inflows.

South Africa

South Africa, the second largest economy in Africa it hosts an economy that is reliant on agriculture, mining, manufacturing, and services. Nigeria and Egypt are leading in terms of highest GDPs, whereas the region enormously benefits from natural resources that include the largest as well as historical diamond and platinum mines. South Africa is also facing challenges in terms of increasing unemployment and limited infrastructural capital allocations. In contrast, progress is being driven by suitable policies and reforms, which are focused on facilitating revenue growth and enhancing citizens' quality of life. South Africa’s economy generated USD 401.1 billion in GDP in 2024, with GDP per capita of about USD 6,267, reflecting modest growth of 0.5%.

Natural Resources

- South Africa is a global leader in mining, holding the world’s largest reserves of platinum-group metals and ranking among the top producers of gold, manganese, and chromium. As of 2024, this region holds mineral ore reserves that were valued at over USD 2.5 trillion, with 16 commodities ranked among the global top 10. The country possesses the largest known global reserves of platinum group metals, being 88%, manganese 80%, chromite at 72%, and gold 13%, underscoring its prominent position in worldwide mining supply chains.

- In addition, South Africa ranks second globally in reserves of titanium minerals 10%, zirconium 25%, vanadium 32%, vermiculite 40%, and fluorspar 17%, while also holding 2% of the world’s antimony reserves. Hence, the presence of this diverse geological endowment positions South Africa as a cornerstone supplier of industrial and critical minerals that are highly essential for manufacturing, energy, and advanced technologies.

Agriculture and Food Processing

- The region boasts a well-developed commercial agriculture sector, which leads the entire continent in the production and export of fruits, wine, and processed foods, supported by agro-processing as well as cold-chain infrastructure. Agricultural exports in the region reached USD 3.36 billion in the first quarter of 2025, which marks a 10% year-over-year rise. Growth was efficiently driven by higher export volumes of grapes, maize, apples, and wine, supported by improved global prices and reinforcing the country’s position as a leading exporter of fruits, wine, and processed agricultural products.

- In addition, employment and sector resilience have also been contributing to the economic growth, showcasing primary agriculture employment rising by 1% quarter-on-quarter to 930,000 jobs during the same time, with gains in field crops, game, and hunting. On the other hand, annual employment remains slightly lower year-on-year, the recovery highlighting its continued momentum across the agricultural value chain, supported by government interventions that are focused on skills development, youth participation, agro-processing, and long-term food security.

Manufacturing

- South Africa hosts the continent’s rising manufacturing base, with strengths lying in automotive production, metals fabrication, chemicals, and machinery, thereby serving both national and international markets. In 2023, South Africa’s automotive industry successfully captured substantial production and exports, with 633,332 vehicles produced and 399,594 exported, generating around R270.8 billion (USD 15.5 billion) in revenue, which is a 19.1% increase from 2022. Similarly, in the aspect of exports to African markets reached 25,381 vehicles were reached, highlighting encouraging opportunities under the AfCFTA. The sector employs over 116,000 people and accounts for 3.2% of GDP, with the retail value chain contributing an additional 2.1%.

- Meanwhile, the strategic investments by OEMs and component manufacturers, supported by DTIC initiatives, include R60 billion (USD 3.4 billion) for plant upgrades and new models, Stellantis’s new factory, BMW’s R4.5 billion (USD 255 million) X3 Plug-in Hybrid production, and Volkswagen’s R4 billion (USD 227 million) SUV project, collectively supporting over 10,000 jobs. These consistent efforts position South Africa as Africa’s largest vehicle producer, the 22nd largest globally, and contribute to regional trade, industrial development, as well as sustainable employment.

GCC Countries

The Gulf Cooperation Council (GCC) represents a group of six countries in the Middle East, i.e., Saudi Arabia, Kuwait, the United Arab Emirates, Qatar, Bahrain, and Oman. These countries are home to some of the largest oil reserves across the globe. The non-oil sectors also contribute to the growth across member states, boosted by tourism, financial services, logistics, advanced infrastructure, and digital transformation initiatives. Hydrocarbons continue to play a central role; the GCC economies are actively accelerating economic diversification. Saudi Arabia’s Vision 2030 reforms have increased the share of non-oil GDP substantially, whereas the UAE has seen growth in non-oil trade, reflecting integration into international markets and trade agreements. Economic growth in the GCC is expected to surge from 3.2% in 2025 to 4.5% in 2026, fueled by the rollback of OPEC and oil production cuts and the strong expansion of non-oil sectors such as tourism, finance, logistics, and digital services. Collectively, these trends reflect constant efforts to reduce dependency on oil and gas, build resilience to price volatility, and expand sectors across the GCC.

Economic Diversification and Digital Transformation

- Economies in the Gulf Cooperation Council are demonstrating resilience with projected GDP growth in 2025: UAE 4.8%, Saudi Arabia 3.8%, Bahrain 3.5%, Oman 3.1%, Qatar 2.8%, and Kuwait 2.7%. This progress is effectively propelled by structural reforms, ongoing economic diversification, and the expansion of non-oil sectors. In addition, official data denotes that hydrocarbons are dominating the financial positions, but strategic investments in infrastructure, SMEs, and non-oil exports are reducing reliance on oil revenues, thereby aligning with national vision strategies.

- The region is accelerating digital transformation and AI adoption, wherein 5G coverage exceeds 90%, high-speed connectivity, and continued investments in data centers and high-performance computing. Saudi Arabia and the UAE are emerging as worldwide AI leaders, supported by startup ecosystems, venture funding, and government AI initiatives. Women’s participation in STEM fields surpasses global averages, whereas the regional collaboration on AI centers, reskilling programs, and innovation ecosystems is highly essential to sustain economic diversification and long-term progress across the MENAAP region.

Water Security

- Gulf Cooperation Council nations have been facing the challenge of water scarcity owing to the arid climates and limited natural freshwater resources. Decades of major investment in advanced desalination technologies, combined with efficient utility management and modern infrastructure, have positioned the region in a prominent position in water security solutions. These efforts not only ensure a reliable water supply for households, agriculture, and industry but also strengthen the GCC’s resilience to climate change. By integrating innovation, sustainable practices, and regional cooperation, the countries are turning water scarcity into a pillar of advantage, extending the supporting economic growth and environmental sustainability.

Logistics & Transport

- The GCC countries are well known for the presence of ports, airports, and logistics hubs that are expanding on account of their strategic location for trade between Asia, Europe, and Africa. 10 Gulf container ports were ranked amongst the 70 most efficient ports across the globe in 2024, out of 405 total ports across the world. Saudi Arabia, UAE, Oman, and Qatar are also among the 35 countries that consist of the largest maritime fleets, with Gulf commercial ships representing 54.2% of the total Arab fleet. GCC countries have crossed the Arab average for maritime connectivity, i.e., 100.5 in 2023, with more than 25 major seaports, demonstrating strong investment in infrastructure.

- In terms of container throughput, two Gulf ports are classified as high throughput, over 4 million containers on a yearly basis, whereas eight others are reported to be medium throughput, 0.5 to 4 million containers. The increasing emphasis on the role of maritime navigation and port infrastructure as strategic assets for global shipping, logistics operations, and regional security, strengthened through initiatives such as the Unified Maritime Operations Centre.

Rest of Middle East and Africa

The Rest of the Middle East and Africa region encompasses diverse economies, which include Egypt, Oman, Qatar, Saudi Arabia, the UAE, and others. The region has shown considerable economic growth in recent years, driven by a combination of strategic investments, resource endowments, and policy reforms aimed at enhancing competitiveness and resilience in global markets.

- Geographic location that connects Asia, Europe, and Africa, constantly supporting trade, logistics, as well as international supply chains.

- The region boasts most of the natural resources, particularly oil and gas, which continue to allow revenue inflow by supporting energy exports.

- Economic diversification initiatives, in which the governments are expanding sectors of tourism, manufacturing, fintech, and renewable energy to reduce dependency on hydrocarbons.

Egypt and Oman

- Egypt and Oman are among the densely populated and rapidly developing nations in the rest of Middle East and Africa region, which have demonstrated strong economic resilience despite the presence of various challenges.

- Egypt’s growth is mainly fueled by economic diversification, structural reforms, expansion of non-oil sectors such as manufacturing and tourism, and rising private investment.

- Oman continues to strengthen its economy since it leverages diversification efforts, infrastructure development, and policies that attract investment by also promoting sustainable and long-term growth.

Qatar and Saudi Arabia

- Qatar’s economy is well established in its oil and gas sector, whereas the ongoing efforts under the Qatar National Vision 2030 are aiming to achieve long-term knowledge-based socio-economic prosperity through four pillars being human, social, economic, and environmental development.

- The nation has implemented three successive national development strategies, each building on the previous one with medium-term objectives to advance the goals of QNV 2030. With the third national development strategy 2024-2030, the government, private sector, and civil society are constantly putting efforts into creating a modern, sustainable, and prosperous society.

- Saudi Arabia is reliant on oil revenues, but the country’s efforts drive reforms to diversify the economy, fostering burgeoning growth in tourism, renewable energy, entertainment, and non-oil industries.

- Both nations are making continued investments in infrastructure, digital innovation, and human capital to support sustainable, long-term economic transformation in the upcoming years.

United Arab Emirates and Others

- The UAE continues to strengthen its economy, in which the sectors such as tourism, finance, logistics, and renewable energy are driving consistent revenue upstream. Strategic investments in terms of transportation, smart cities, and digital infrastructure have enhanced the business environment, attracted global investors, and supported innovation-led development.

- Other countries in the region, Bahrain, Kuwait, and Lebanon, are deliberately leveraging infrastructure modernization, financial sector reforms, and SME support programs to expand economic activity. Regional efforts are focused mainly on trade facilitation and technology adoption to reduce reliance on hydrocarbons and boost resilience.