Solar PV Backsheet Market Outlook:

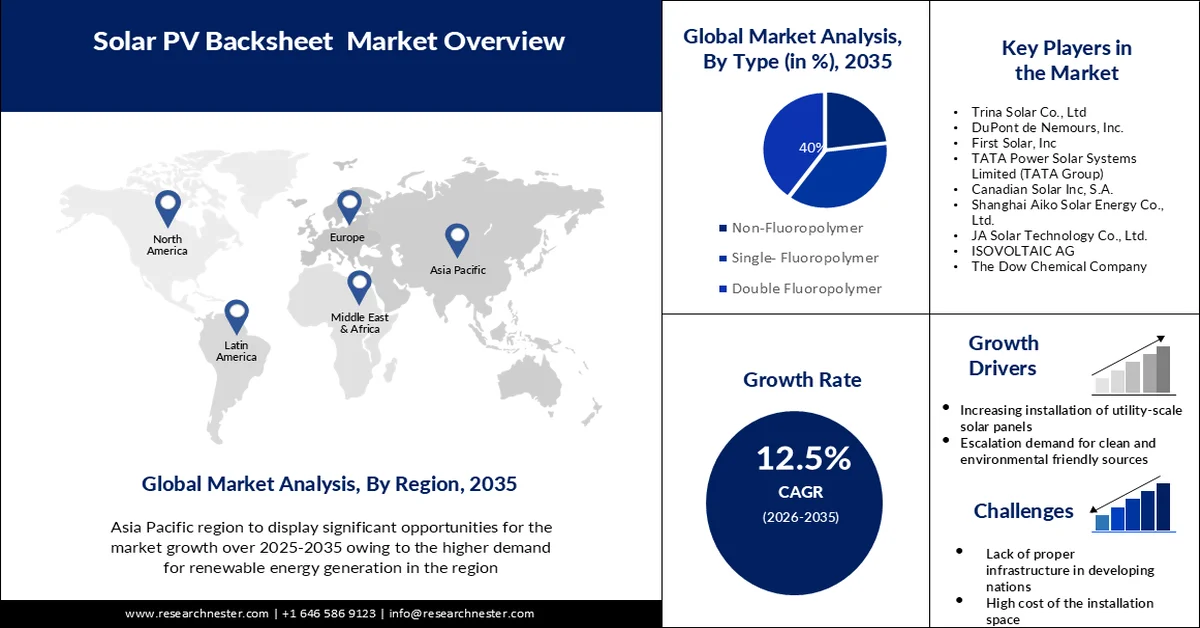

Solar PV Backsheet Market size was valued at USD 3 billion in 2025 and is likely to cross USD 9.74 billion by 2035, expanding at more than 12.5% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of solar PV backsheet is estimated at USD 3.34 billion.

Rising worldwide solar PV installation, as well as the growing demand and necessity to reduce carbon emissions, are likely to drive the global solar backsheet market. In the previous nine years, installed solar energy capacity has expanded by 24.4 times, and it now stands at 66.7 GW as of May 2023 in India.

Promising expansion and development in the renewable energy industry are also projected to positively benefit the target market's growth. Another driver expected to drive solar backsheet revenue is technical improvement in solar back sheets, which will result in new product innovations. According to SolarPower Europe, solar power developed quickly over the last decade, from 30 GW in 2011 to 138 GW in 2020, mostly due to utility-scale projects and the fluoropolymer solar back sheet business.

Key Solar PV Backsheet Market Insights Summary:

Regional Insights:

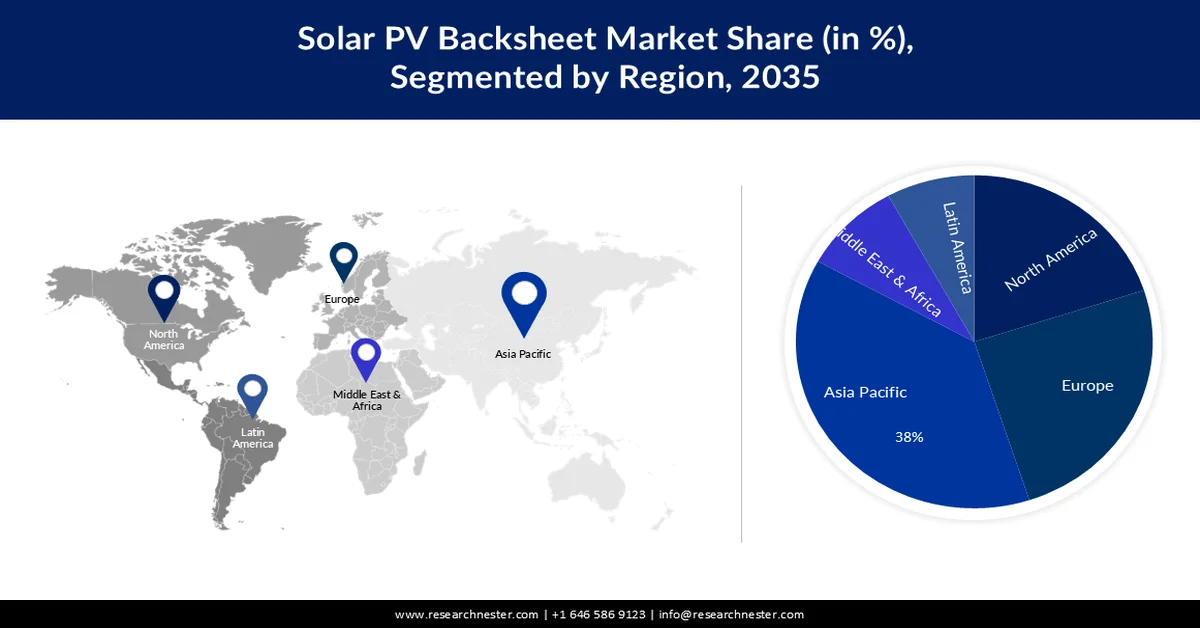

- Asia Pacific is projected to command a 38% revenue share by 2035 in the solar pv backsheet market, propelled by expanding renewable energy initiatives and rising infrastructure investments.

- Europe is estimated to capture a 25% revenue share by 2035, fueled by stringent environmental regulations and accelerating adoption of renewable energy.

Segment Insights:

- The double fluoropolymer segment in the solar pv backsheet market is anticipated to hold a 40% share by 2035, driven by higher efficiency, improved manufacturing productivity, and enhanced insulating qualities.

- The floating segment is forecast to account for 35% share by 2035, supported by the higher electricity generation potential enabled by the cooling effect of water and mitigation of land constraints.

Key Growth Trends:

- Increased Investment in Solar Energy Farm and Station Construction and Infrastructure

- Increased Demand for Clean and Environment-Friendly Energy Sources

Major Challenges:

- High Cost of Installation Space Required

- Lack of Proper Infrastructure in Developing Countries.

Key Players: Komatsu Ltd, Mine Master, Boart Longyear, MacLean Engineering & Marketing Co., J.H. Fletcher & Co., Inc., Sandvik AB, Caterpillar Inc., EPIROC AB, Hager Equipment Company, Normet Group.

Global Solar PV Backsheet Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3 billion

- 2026 Market Size: USD 3.34 billion

- Projected Market Size: USD 9.74 billion by 2035

- Growth Forecasts: 12.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (38% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: China, United States, Germany, Japan, South Korea

- Emerging Countries: China, India, Japan, South Korea, United States

Last updated on : 25 February, 2026

Solar PV Backsheet Market - Growth Drivers and Challenges

Growth Drivers

- Increased Investment in Solar Energy Farm and Station Construction and Infrastructure- Solar power generation technologies is assisting in the battle against catastrophic climate change. Solar panel power generation, for example, is a low-polluting power generation segment with lower carbon emissions than conventional energy sources such as petroleum, oil, and coal. The initialization of governments throughout the world to deliver 100% electric energy using renewable energy, including solar power sources, anticipates worldwide solar PV backsheet market growth. Solar accounted for 54% of all new electric capacity added to the grid this quarter. Solar's growing competitiveness against other technologies has enabled it to rapidly raise its proportion of total US electrical output, from 0.1% in 2010 to roughly 5% now.

- Increased Demand for Clean and Environment-Friendly Energy Sources- The worldwide solar backsheet industry is expanding as demand for sustainable energy grows globally. Many countries are increasingly turning to renewable energy sources through different ways such as renewable energy transformer. Solar energy is the most widely used among the various sources due to the availability of government incentives and tax breaks for the installation of solar panels.

- Advancement in the Photovoltaic industry- The technological innovation and continued expansion of the photovoltaic industry are forecasted to boost the growth of the market in the near future.

Challenges

- High Cost of Installation Space Required- The high cost of solar panel installation is a major restraint for the solar backsheet business. Along with the high expenses, a specific quantity of land must be provided for the installation of the panels; the needed amount of area grows in proportion to the amount of energy required. The space cannot be used for any other purpose after the panels have been installed, which limits the expansion of the solar backsheet business.

- Lack of Proper Infrastructure in Developing Countries.

- Lack Of Awareness Amongst the People.

Solar PV Backsheet Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.5% |

|

Base Year Market Size (2025) |

USD 3 billion |

|

Forecast Year Market Size (2035) |

USD 9.74 billion |

|

Regional Scope |

|

Solar PV Backsheet Market Segmentation:

Type Segment Analysis

The double fluoropolymer segment led the worldwide solar PV backsheet market with a share of 40 % and will continue to do so during the projected period. Higher efficiency, increased acceptability, improved manufacturing productivity, and enhanced insulating qualities are the primary reasons attributed to market growth. Fluoropolymer has a lengthy track record of outstanding performance.

Installation Segment Analysis

Solar PV backsheet market from the floating segment is expected to have the largest share of 35 % and rise at a rapid CAGR. The ability of these plants to create more electricity due to the cooling nature of water might be attributed to the market expansion. Floating power plants also shed light on land limits, which are a major impediment to ground-mounted solar arrays.

Our in-depth analysis of the global solar PV backsheet market includes the following segments:

|

Type |

|

|

Installation |

|

|

End-User |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Solar PV Backsheet Market - Regional Analysis

APAC Market Insights

The Asia Pacific industry is predicted to account for largest revenue share of 38% by 2035. East Asia is expected to play a significant role in the global solar backsheet industry and is likely to have a large share throughout the projection period. Various government programmes aimed at increasing the use of renewable energy in this region have contributed to the market's rapid expansion. Investment in infrastructure development boosts solar panel usage, leading to proportionate growth of the solar panel backsheet industry. Market integration with China and other East Asian nations is growing as manufacturing and distribution networks become more complicated, thanks to Chinese investments. Cost reductions in solar PV from the East Asian area have facilitated the deployment of solar backsheet. The introduction of solar energy has had a significant influence on GDP and jobs in this region, encouraging product sales. Solar energy capacity in Asia is expected to reach 486 thousand megawatts by 2021. This was a considerable gain from 2012, when Asia's solar energy capacity was estimated to be at 16.2 thousand megawatts.

European Market Insights

The European solar PV backsheet market is anticipated to growth at significant CAGR with 25% revenue share. Environmental laws from the European area are expected to result in a significant increase in product sales. The shifting trend in the European area towards the predominant usage of renewable energy is likely to enhance the industry. Competitive incentive programmes, renewable energy objectives set by European nations showing a bright picture for solar backsheet use. The fast expansion of non-residential and residential solar has fuelled national debates over rate reform. New product offerings by local and worldwide businesses in the European area are projected to boost the potential of the European solar PV backsheet market. Countries in southern and north western Europe are projected to be in the forefront of regional market expansion. Solar power costs have dropped by 82% between 2010 and 2020, making it the most cost-effective source of electricity in many regions of the EU.

Solar PV Backsheet Market Players:

- Cybrid Technologies Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Trina Solar Co., Ltd

- DuPont de Nemours, Inc.

- First Solar, Inc

- TATA Power Solar Systems Limited (TATA Group)

- Canadian Solar Inc, S.A.

- Shanghai Aiko Solar Energy Co., Ltd.

- JA Solar Technology Co., Ltd.

- ISOVOLTAIC AG

- The Dow Chemical Company

- Royal DSM

Recent Developments

- Trina Solar Co. LLtd., announced the launch of nTrina Tracker Vanguard 600+ series which aims to increase solar panel efficiency by 2%-8%.

- Royal DSM, a global science-based company in health, nutrition, and sustainable living, agreed to sell its Advanced Solar business involved in backsheet products to the Worthen Industries Inc.

- Report ID: 3347

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Solar PV Backsheet Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.