Sports Apparel Market Outlook:

Sports Apparel Market size was valued at USD 280.4 billion in 2025 and is projected to reach USD 572.5 billion by the end of 2035, rising at a CAGR of 7.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of sports apparel is estimated at USD 301.1 billion.

The sports apparel market is being shaped by the rising participation in physical activity, supported by the public health initiatives and measurable increases in consumer expenditure. According to the FRED March 2026 data, the personal consumption expenditures on clothing and footwear in the U.S. reached USD 586.479 billion in 2024, reflecting the sustained discretionary spending on apparel categories that include sportswear. Government-backed health promotion programs are also expanding the active consumer base. Moreover, the participation trends are reinforced by public investments; for example, the UK government committed a million to grassroots sports facilities and community activity programs, strengthening long-term consumption patterns for sports apparel across demographics.

Additionally, the trade flows and the manufacturing indicators highlight the global scale and the supply-side dynamics of the sector. According to the USITC September data, the U.S. imports of apparel totaled over 79.3 billion, with a significant share attributed to the activewear and the synthetic fiber garments, underscoring the reliance on the international supply chains. Moreover, the global textile and apparel manufacturing drives the demand for recovery and increased capacity utilization in Asia. Additionally, sustainability compliance and material innovation are gaining importance due to regulatory oversight. The EPA's October 2025 data depicts that the textile waste in the U.S. reached 17 million tons annually, prompting policy attention on recycling and circular production models. These regulatory and trade-linked factors are influencing sourcing strategies, cost structures, and procurement decisions across the sports apparel value chain.

Key Sports Apparel Market Insights Summary:

Regional Highlights:

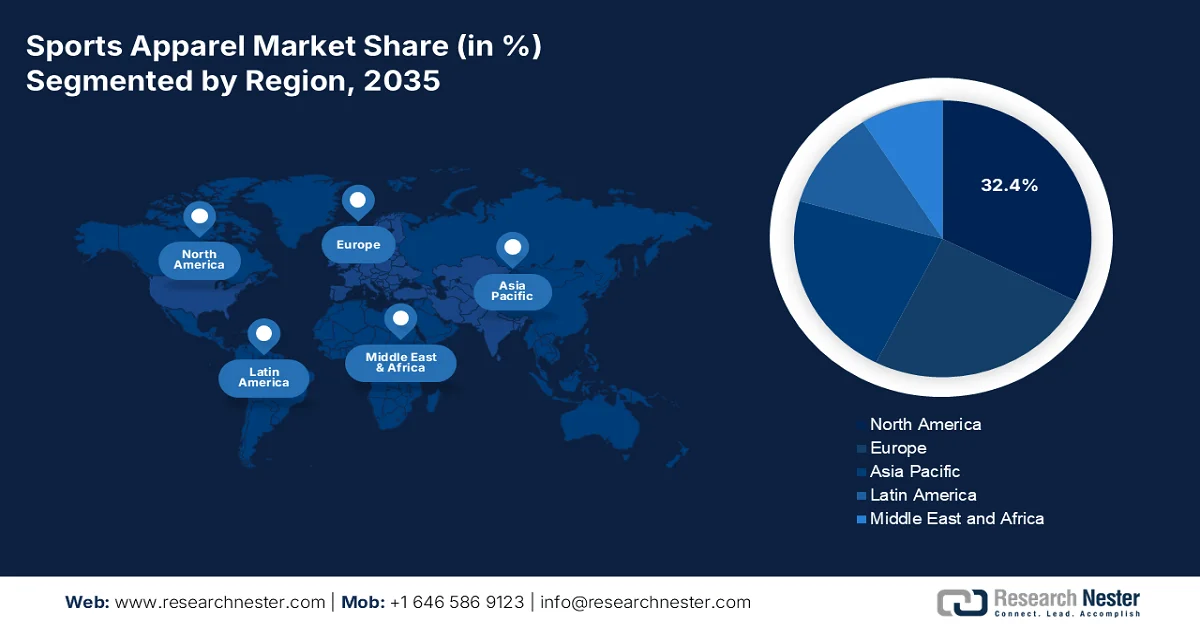

- North America sports apparel market is anticipated to command a 32.4% share by 2035, underpinned by strong integration of sports culture and advanced retail infrastructure

- Asia Pacific is forecasted to witness a CAGR of 7.1% during 2026–2035, fueled by rising disposable incomes and increasing government investment in sports infrastructure

Segment Insights:

- Sports apparel market mid-range price point segment is projected to capture a 45.4% share by 2035, propelled by growing consumer preference for balancing quality, performance, and affordability

- Online distribution channel segment is expected to lead over the forecast period, driven by the expanding convenience of mobile commerce and availability of exclusive digital inventories

Key Growth Trends:

- Public investment in sports infrastructure

- National health and physical activity programs

Major Challenges:

- Tariff volatility and supply chain costs

- Sustainability and eco-friendly compliance

Key Players: Nike, Inc. (U.S.), Adidas AG (Germany), Puma SE (Germany), Under Armour, Inc. (U.S.), Lululemon Athletica (Canada), Anta Sports Products Limited (China), Li-Ning Company Limited (China), Asics Corporation (Japan), Mizuno Corporation (Japan), Fila Holdings Corp. (South Korea), Amer Sports, Inc. (Finland), Columbia Sportswear Company (U.S.), New Balance Athletics, Inc. (U.S.), V.F. Corporation (U.S.), Gap Inc. (U.S.), DICK'S Sporting Goods (U.S.), Authentic Brands Group (U.S.), Skechers USA, Inc. (U.S.), Bata Corporation (Canada), Li & Fung Limited (Hong Kong/Malaysia).

Global Sports Apparel Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 280.4 billion

- 2026 Market Size: USD 301.1 billion

- Projected Market Size: USD 572.5 billion by 2035

- Growth Forecasts: 7.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (32.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, Brazil, South Korea, Indonesia, Vietnam

Last updated on : 25 March, 2026

Sports Apparel Market - Growth Drivers and Challenges

Growth Drivers

- Public investment in sports infrastructure: Government expenditure on sports infrastructure is a primary demand driver in the sports apparel market, expanding access to organized and recreational physical activity. The capital allocation towards the stadiums, community gyms, and school-level facilities directly increases the participation rates, translating into higher apparel consumption. For example, the government of the UK, January 2026 data depicted that USD 436 million is allocated to upgrade grassroots sports infrastructure, targeting multi-sport participation and community fitness access. These investments create sustained demand for athletes procuring performance apparel in bulk. As governments prioritize sports as part of social development and youth engagement policies, infrastructure expansion continues to drive consistent, volume-based demand across regional markets.

- National health and physical activity programs: Rising government spending on preventive healthcare is increasing participation in physical activity, directly influencing the sports apparel market demand. The public health agencies are promoting structured exercise to reduce the chronic disease burden, expanding the consumer base for activewear. The CDC August 2022 data reports that only 24.2% of the U.S. adults met recommended physical activity levels in 2022, promoting continued federal and the state level funding for fitness initiatives. These initiatives create recurring demand for affordable and mid-range sports apparel suited for daily exercise. For B2B stakeholders, this translates into a stable institutional demand from the fitness programs, schools, and healthcare-linked wellness initiatives.

- School athletic program funding: Public education spending on athletics remains a consistent demand driver in the sports apparel market. The public secondary schools spent a certain billion on athletic programs, with the uniform and equipment purchases representing a significant portion. This continues to drive the funding parity, expanding the apparel demand for the women’s team. The government accountability office noted that schools receiving federal assistance must provide equitable athletic opportunities, creating a consistent replacement cycle for team uniforms. Manufacturers offering bundled procurement solutions to school districts and athletic departments can secure multi-year supply contracts. The cyclical nature of school budgeting, typically finalized in spring for the fall sports, allows suppliers to align sales efforts with public sector fiscal calendars.

Challenges

- Tariff volatility and supply chain costs: Trade policy instability has become a major barrier in the sports apparel market. The growth is occurring despite significant government pricing constraints from tariffs. The uncertainty surrounding the potential tariffs caused paralysis across the industry. New players face the daunting task of navigating these fluctuating costs while the top players absorb the impacts better. The industry has adjusted by passing only one third of tariff costs to consumers, with the remainder absorbed by the manufacturers and brands.

- Sustainability and eco-friendly compliance: The shift toward sustainable materials presents both an opportunity and a formidable challenge in the sports apparel market. The sustainable athleisure market is growing from the previous year. However, the tariffs on recycled yarns and bio-based fibers are increasing the production costs for sustainable apparel manufacturers. New players face sustainability challenges, and consumers demand eco-friendly products but remain price sensitive, while the sustainable materials cost more, mainly when the tariffs apply.

Sports Apparel Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.4% |

|

Base Year Market Size (2025) |

USD 280.4 billion |

|

Forecast Year Market Size (2035) |

USD 572.5 billion |

|

Regional Scope |

|

Sports Apparel Market Segmentation:

Price Point Segment Analysis

Under the price point segment, the mid-range is leading the segment and is poised to hold the largest share value of 45.4% by the end of 2035. The segment is driven due to the consumer demand to balance between the quality, performance features, and affordability. Unlike the other sub-segments that cater to elite athletes or economy lines that compete strictly on cost, mid-range apparel offers the sweet sport of durable fabrics and brand recognition without extreme pricing. According to the FRED December 2025 data, the expenditure on apparel and services reached USD 1,461, with a significant portion directed towards the mid-tier activewear brands that offer versatility for both workouts and casual wear. Rising athleisure trends further boost the demand for mid-range apparel among urban consumers seeking style and comfort.

Distribution Channel Segment Analysis

Within the distribution channel segment, the online sub-segment is leading in the sports apparel market. The segment is driven by the convenience of mobile commerce and the exclusive digital inventories offered by brands to bypass traditional retail markups. According to the U.S. Census Bureau's March 2026 report, the e-commerce sales in Q4 of 2025 reached USD 1,900.5 billion, with apparel and accessories remaining the largest online category. Specifically, the report noted that the sporting goods, hobby, and book stores saw a rise in online penetration. This data confirms that consumers now prefer the seamless browsing and home try-on options that digital platforms provide over traditional brick-and-mortar visits.

Fabric Type Segment Analysis

Polyester is leading in the fabric type segment in the sports apparel market, valued for its durability, moisture-wicking properties, and cost-effectiveness in manufacturing. As the industry pushes toward sustainability, recycled polyester derived from plastic bottles is becoming the standard for major brands such as Nike and Adidas. According to the OEC 2024 data, the staple fibers of polyester imports by the U.S. in 2024 reached USD 561 million. This data highlights the manufacturing world’s heavy reliance on synthetics to meet the global demand for high-performance sportswear. Further, the report noted that cotton remains relevant for lifestyle wear, and the functional requirements of modern athletics continue to favor synthetic blends for compression, stretch, and rapid drying.

Leading Exporters of Staple Fabric Polyester, 2024

|

Country |

Value |

|

China |

USD 1.36 billion |

|

South Korea |

USD 699 million |

|

Thailand |

USD 449 million |

Source: OEC

Our in-depth analysis of the sports apparel market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

End user |

|

|

Distribution Channel |

|

|

Price Point |

|

|

Fabric Type |

|

|

Application |

|

|

Age Group |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Sports Apparel Market - Regional Analysis

North America Market Insights

North America is dominating and is poised to hold the regional share of 32.4% by the end of 2035 in the sports apparel market. The region is defined by the deep cultural integration of sports and fitness into daily life. The market is defined by the well-established retail infrastructure, high consumer disposable income, and a pronounced preference for branded performance wear that transitions seamlessly into casual athleisure attire. A key structural driver is the institutional procurement pipeline encompassing everything from the federal defense contracts for physical training gear to municipal investments in public recreational facilities. Manufacturers in this region benefit from an advanced logistics network that supports rapid fulfillment, but they must navigate a complex regulatory environment marked by stringent trade documentation requirements and an evolving supply chain with significant pricing power.

The strong consumer spending patterns and its position as a major global importer of sports goods are driving the sports apparel market in the U.S. According to the WTO July 2024 data, sports goods imports reached nearly USD 64 billion in 2022, with the U.S. identified as one of the primary importing regions, indicating a high reliance on international supply chains to meet domestic demand. Moreover, the sustained apparel expenditure at the household level in 2023 U.S. households spent an average of USD 655 on women’s apparel and USD 406 on men’s apparel, with additional spending on children’s clothing and footwear based on U.S. BLS February 2025 data. The higher spending on apparel also signals stronger growth potential in sportswear segments, therefore driving the market demand.

Annual Expenditure for Apparel, 2025

|

Metric (Age-wise) |

Expenditure (USD) |

|

Women 16 and above |

655 |

|

Girls 2 to 15 |

87 |

|

Women Footwear |

208 |

|

Men 16 and above |

406 |

|

Boys 2 to 15 |

96 |

|

Men Footwear |

147 |

Source: BLS February

The broad-based participation in physical activities is driving the sports apparel market in Canada and is supporting a consistent demand for performance and recreational clothing. According to Statistics Canada's November 2023 data, 55% of Canada aged 15 years and older engaged in sports activities over a 12-month period, with higher participation among men is 62% compared to women is 49%. This wide participation base creates steady demand across multiple apparel categories, including running wear, swimwear, and training apparel. Activity-specific trends further shape product demand; swimming 35%, cycling 33%, and running, 27% rank as the most common sports, indicating strong consumption of specialized apparel. These participation patterns support both seasonal and year-round demand cycles. These data are positioning Canada as a stable, participation-driven market.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region during the assessed period, 2026 to 2035, and is expected to grow at a CAGR of 7.1%. The region is driven by the rising disposable incomes, increasing government investment in sports infrastructure, and deep manufacturing capabilities. The region benefits from concentrated textile production capacity as the top three suppliers of man-made fiber apparel are demonstrating the region’s manufacturing dominance. Government initiatives across the region are surging the demand for increasing regular physical activity participation, while Japan’s Ministry of Education, Culture, and Sports Science and Technology funds school sports programs that require regular uniform replacement cycles. Furthermore, the infrastructure spending creates a sustained demand for the team's apparel and equipment.

The rapid demand expansion, strong domestic consumption, and the increasing influence of the local brands are shaping the sports apparel market in China. According to the ITA January 2022 data, the market is projected to grow at an annual rate of around 11%, reaching USD 82.8 billion by 2024. This economic shift is driving higher spending on athletic apparel, footwear, and accessories across the urban populations. On the other hand, the competitive landscape is evolving with the rise of domestic brands under the guochao trend, where younger consumers prefer locally designed products incorporating Chinese cultural elements. The People’s Republic of China March 2022 data depicts that companies such as ANTA Sports have strengthened their market position, achieving revenues of USD 6.9 billion in 2021 and surpassing several international competitors in market share. These data show China as a high-growth and strategically important market.

The strong manufacturing base, growing domestic demand, and increasing export contribution are fueling the sports apparel market in India. As per the IBEF December 2025 data, the country’s sports goods market was valued at approximately USD 4.5 billion, indicating a steady expansion driven by the rising participation in sports and fitness activities. India also plays a critical role in global supply chains, with around 60% of its sporting goods production exported and total exports reaching about USD 400.1 million in 2025. Additionally, the sector employs around 500,000 people, highlighting its economic significance. Increasing consumer spending, government support for sports initiatives, and a growing fitness culture are further strengthening domestic demand for sports apparel, positioning India as both a production hub and an emerging consumption market.

Europe Market Insights

The sports apparel market in Europe is expanding rapidly and is defined by the strong cross-border trade integration and increasing institutional support for physical activity. The region promotes grassroots sports participation across the member states, directly stimulating the demand for team apparel and equipment. The market benefits from the sustained demand for sports clothing among participant populations. The market benefits from the EU’s harmonized regulatory frameworks, which simplify distribution across the member states because manufacturers must comply with strict chemical regulations governing production. Moreover, the retail concentration varies significantly with the e-commerce penetration, and traditional specialty retail dominates the market.

The strong institutional support and widespread participation in organized sports are shaping the sports apparel market in Germany. According to EPAS March 2023 data, the government expenditure on sports reached over USD 450 million, with more than half allocated to sports facilities and national infrastructure, reinforcing access to training environments and increasing demand for sports-related products, including apparel. Moroever the Sports in Germany March 2023 data depicts that the country ranked third in the all-time Olympic medal table with over 1,800 medals, reflecting a deeply embedded high-performance sports ecosystem. Further, 27 million people are members of around 90,000 sports clubs, creating a large and consistent consumer base for team uniforms, training gear, and recreational sportswear. These data show an active growth market.

The sports apparel market in UK is supported by physical activity participation and sustained government investment. According to Sport England's April 2025 data, nearly 63.7% of adults met the recommended 150 minutes of physical activity per week in 2023, reflecting a broad and active consumer base that drives demand for sportswear across various sports categories. This participation is reinforced by public funding; the UK government has committed over GBP 300 million toward grassroots sports facilities and school-level infrastructure, based on the UK government's January 2026 report. The combination of widespread participation, institutional procurement via clubs and schools, and stable discretionary spending supports consistent demand across both the performance and athleisure categories, positioning the UK as a mature and steadily growing market.

Key Sports Apparel Market Players:

- Nike, Inc. (U.S.)

- Adidas AG (Germany)

- Puma SE (Germany)

- Under Armour, Inc. (U.S.)

- Lululemon Athletica (Canada)

- Anta Sports Products Limited (China)

- Li-Ning Company Limited (China)

- Asics Corporation (Japan)

- Mizuno Corporation (Japan)

- Fila Holdings Corp. (South Korea)

- Amer Sports, Inc. (Finland)

- Columbia Sportswear Company (U.S.)

- New Balance Athletics, Inc. (U.S.)

- V.F. Corporation (U.S.)

- Gap Inc. (U.S.)

- DICK'S Sporting Goods (U.S.)

- Authentic Brands Group (U.S.)

- Skechers USA, Inc. (U.S.)

- Bata Corporation (Canada)

- Li & Fung Limited (Hong Kong/Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Nike Inc is a dominant player in the sports apparel market and maintains its leadership via relentless innovation and deep consumer connections. The company uses its extensive Nike Direct strategy to bypass traditional retail and engage customers via its apps and membership programs. The company is offering professional performance gear to retro lifestyle sneakers. In 2024, the company made a revenue of USD 51.4 billion.

- Adidas AG remains a powerhouse in the sports apparel market by blending athletic performance with the streetwear culture. The company has strategically pivoted to rehabilitate its brand after the breakup with Kanye West, focusing on its heritage in soccer and running. The company is focusing on sustainability via products made from recycled materials. According to the 2024 annual report, nearly 32% of the total sales was in Europe.

- Puma SE has successfully repositioned itself as a fast-growing challenger in the sports apparel market by merging sport and fashion. The company has revitalized its brand via high-profile collaborations with celebrities. In the modern market, the company heavily focuses on performance categories such as training and running, capitalizing on the retro sneaker trend.

- Under Armour Inc has carved out a specific niche in the sports apparel market centered on performance and athletic toughness. Unlike the lifestyle-focused competitors, the company concentrates heavily on the engineering of fabrics to improve the athlete's performance, such as UA Rush and HOVR technologies.

- Lululemon Athletica revolutionized the sports apparel market by essentially creating the athleisure category. Starting with the yoga pants, the company has successfully expanded its running training and even self-care products. In the premium segment, the company differentiates itself via high-quality fabrics and a strong community-based retail model.

Here is a list of key players operating in the global sports apparel market:

The global sports apparel market is intensely competitive and is dominated by a large number of multinational giants, most notably Nike and Adidas, which together hold a significant share of the market. The competitive landscape is defined by rapid product innovation, aggressive marketing via athlete endorsements, and a strong pivot towards digital sales channels. For example, in 2024, Adidas made 18% of its total sales in digital sales. The key strategic initiatives among the top players include a major focus on sustainability, with the companies leading in recycled materials. Further, there is a distinct shift from pure performance wear to sportswear to casual fashion. To capture the market share in the developing economies, these manufacturers are increasingly localizing the supply chains and product designs to cater to regional sports preferences such as cricket in India and badminton in Asia.

Corporate Landscape of the Sports Apparel Market:

Recent Developments

- In June 2025, Anta Sports completes the acquisition of Jack Wolfskin. The acquisition aligns with the Group’s single-focus, multi-brand, globalization strategy and presents opportunities to further strengthen and to grow the Group’s outdoor sports segment.

- In May 2025, DICK'S Sporting Goods, Inc. announced that they have entered into a definitive merger agreement under which DICK'S acquired Foot Locker. This transaction implies an equity value of approximately USD 2.4 billion and an enterprise value of approximately USD 2.5 billion.

- In September 2024, Authentic Brands Group announced that it has finalized the acquisition of athleticwear icon Champion. As the second-largest brand acquisition in Authentic’s history, Champion generates nearly USD 3 billion in global retail sales annually.

- Report ID: 8474

- Published Date: Mar 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.