Children’s Apparel Market Outlook:

Children’s Apparel Market size was valued at USD 264.1 billion in 2025 and is projected to reach USD 451.1 billion by the end of 2035, rising at a CAGR of 5.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of children’s apparel is evaluated at USD 278.5 billion.

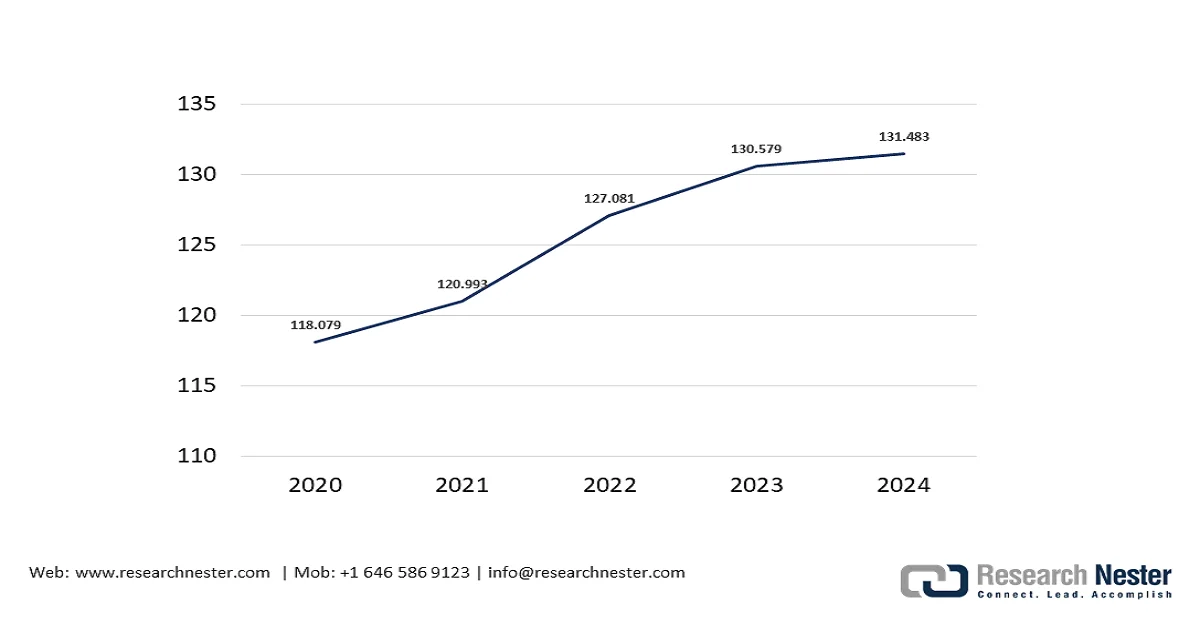

The worldwide children’s apparel market is supported by the stable demographic demand and consistent household spending patterns across major economies. According to the article published by NLM in December 2024, individuals under 18 years accounted for 22% of the total population, representing over 73 million children, sustaining recurring demand for the age-segmented clothing categories. Besides, the consumer price index data on apparel in 2024 reached 131.483 index (1982-84=100), based on U.S. BLS data February 2025, in allocating a defined share toward children’s garments mainly in back-to-school and seasonal purchase cycles. Moreover, the OEC 2024 data shows that the export growth of textiles was nearly 0.88%. These structural indicators support a steady replenishment demand, driven by growth cycles, school calendars, and climate-based replacement patterns.

Consumer Price Index for Apparel

Source: U.S. BLS February 2025

Besides, the demographic concentration in emerging economies continues to shape the sourcing and volume dynamics. According to the World Bank data in 2026, children aged 0 to 14 represent about 25% of the global population in 2024, with significantly higher shares in South Asia and Sub-Saharan Africa. This demographic distribution supports a sustained baseline for essential and seasonal children’s garments across both the organized and informal retail channels. It is also influenced by the global procurement planning as buyers align production volumes with high-growth population clusters. Moreover, the trade policy, logistics infrastructure, and compliance standards in these regions play a material role in shaping long-term sourcing strategies for manufacturers and international retailers.

Key Children’s Apparel Market Insights Summary:

Regional Highlights:

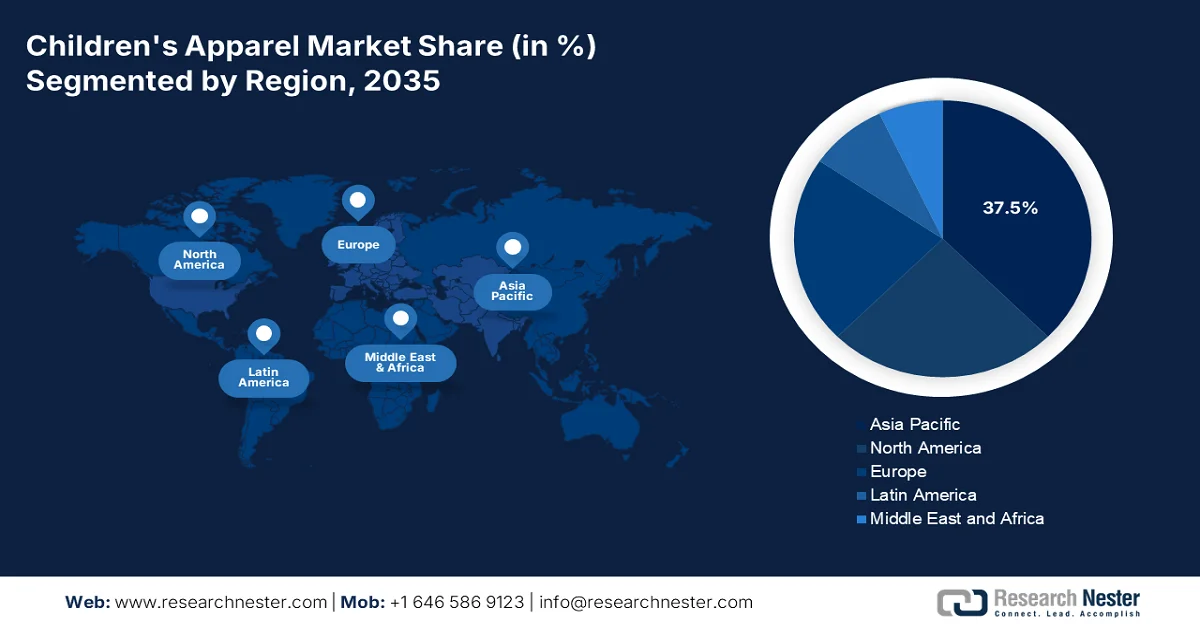

- Asia Pacific is projected to secure a 37.5% revenue share by 2035 in the children’s apparel market, propelled by the region’s vast child population and expanding middle-class households.

- North America is anticipated to witness a CAGR of 5.6% during 2026–2035, stimulated by premiumization trends and rising e-commerce penetration.

Segment Insights:

- In the children’s apparel market, the cotton segment is forecast to command a 55.5% share by 2035, attributed to its breathability, hypoallergenic qualities, and increasing demand for organic and sustainably sourced fabrics.

- The economy/mass market segment is expected to retain the largest share of the market by 2035, fueled by frequent low-cost purchasing patterns driven by rapid clothing replacement needs among growing children.

Key Growth Trends:

- Household consumption and income support programs

- Trade policy and import dependence

Major Challenges:

- Tariff and trade policy volatility

- Rapid growth cycles and inventory risk

Key Players: The Children's Place (U.S.), Carter's, Inc. (U.S.), Gap Inc. (U.S.), Nike, Inc. (U.S.), Adidas AG (Germany), Inditex (Zara) (Spain), H&M (Hennes & Mauritz AB) (Sweden), Fast Retailing Co. (Uniqlo) (Japan), Shimamura Co. (Japan), Next plc (UK), Monnalisa S.p.A. (Italy) Jacadi (France), Pomme d'Api (France), Seed Heritage (Australia), Punpune (South Korea), Reliance Retail (India), Ms. Rachel (New York), Apparel Group India (India), Centric Brands LLC (New York), LT Apparel Group (South Korea).

Global Children’s Apparel Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 264.1 billion

- 2026 Market Size: USD 278.5 billion

- Projected Market Size: USD 451.1 billion by 2035

- Growth Forecasts: 5.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (37.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, India, Japan, Germany

- Emerging Countries: Brazil, Indonesia, Vietnam, Mexico, South Korea

Last updated on : 3 March, 2026

Children’s Apparel Market - Growth Drivers and Challenges

Growth Drivers

- Household consumption and income support programs: The government-backed income support programs strengthen the household purchasing capacity for essential goods, including children’s clothing. The U.S. Bureau of Labor Statistics February 2025 data reported that average annual household spending on women's apparel reached USD 655 in 2023. Additionally, increased disposable income for families with dependents confirms expanded child tax credit disbursements. Income transfer programs in OECD economies support baseline spending stability even during economic slowdowns. Further, the apparel suppliers benefit from reduced demand contraction risk in markets with structured social protection systems. Retailers operating in regions with robust child-related tax credits and subsidies experience stronger seasonal sales resilience, particularly during the back-to-school and winter seasons.

- Trade policy and import dependence: The global sourcing dynamics are shaped by tariff structures and textile import flows, driving the children's apparel market. According to the OEC 2024 data, China is the leading exporter of textiles and exported over USD 268 billion, reflecting a sustained cross-border supply integration. Moreover, the trade facilitation agreements and duty structures influence suppliers' selection and production geography. The preferential trade agreements with the developing economies cost-efficient children's apparel imports into North America and Europe. Further, the government customs statistics provide procurement teams with transparency on sourcing concentration and compliance exposure. Trade data also highlights reliance on Asia-Pacific manufacturing hubs, reinforcing the importance of geopolitical risk monitoring and regulatory compliance planning in children’s garment supply chains.

- Seasonal aid programs: Government-supported relief and seasonal distribution programs influence the children’s apparel market volumes mainly in colder regions. Agencies are administering assistance program that support low-income families, reinforcing the winter clothing demand. In disaster-prone regions, the public emergency management agencies coordinate clothing distribution during climate events, generating institutional demand. Moreover, the participation in the public tenders for relief apparel provides stable volume contracts independent of retail cycles. Additionally, climate variability increases multi-season stocking requirements. Publicly funded social welfare frameworks reduce volatility in basic garment demand and create procurement pipelines aligned with state-supported assistance schemes.

Challenges

- Tariff and trade policy volatility: The tariff volatility has emerged as the most significant financial roadblock for children's apparel market manufacturers. Unlike many industries, children’s clothing manufacturers operate on thin margins while facing complex, frequently changing import duties. The challenge is intensified dramatically in 2025 when new tariff structures imposed import duties on major countries including Bangladesh, India and Vietnam.

- Rapid growth cycles and inventory risk: The inventory management risk is uniquely challenging in children’s apparel due to the children’s rapid physical development. Moreover the adult clothing, which may remain wearable for years, children typically outgrow clothing within months, creating a compressed lifecycle that complicates the demand forecasting in the children’s apparel market. further the manufacturers face the constant dilemma of either overproducing or underproducing.

Children’s Apparel Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.5% |

|

Base Year Market Size (2025) |

USD 264.1 billion |

|

Forecast Year Market Size (2035) |

USD 451.1 billion |

|

Regional Scope |

|

Children’s Apparel Market Segmentation:

Material Segment Analysis

Under the material segment, cotton remains the leading segment in the children’s apparel market, poised to hold the share value in 55.5% by the end of 2035. This dominance is driven by the natural breathability, hypoallergenic properties, and superior softness, which are essential for the delicate skin of infants and toddlers. Further, the surge in demand for organic and sustainably sourced cotton has added a premium layer to this segment, appealing to eco-conscious consumers. The fiber’s versatility across seasons and its durability via repeated washing a necessity in children’s clothing, solidifies its long market leadership. According to the PIB January 2026 data, nearly 17% of the cotton textiles are exported to the EU, driven largely by the enduring preference for natural fibers in essential clothing categories, including children's wear.

Price Point Segment Analysis

Within the price point segment, the economy/mass market segment is projected to maintain the largest share of the children’s apparel market. This persistent dominance is rooted in the fundamental economics of parenting children, who outgrow clothing rapidly, making the high frequency, low cost purchasing a necessity for the majority of households. Moreover, the mass market retailers and discount chains offer affordable basics and fashion-forward pieces that allow parents to manage wardrobe budgets effectively without sacrificing variety. Further, the fast fashion model has further entrenched this segment by offering the trend-driven styles at extremely accessible price points, promoting more frequent purchases. Furthermore, the consumer expenditure survey highlights this trend, revealing that families with children purchase at mass merchants and discount department stores, underscoring the value-driven nature of the market.

Distribution Channel Segment Analysis

Online retail is forecasted to become the largest distribution channel in the children’s apparel market. The channel’s ascendance is driven by the unparalleled convenience for time-pressed parents who can browse extensive catalogs, compare prices, and complete purchases without the logistical challenge of shopping with young children in physical stores. The production of mobile commerce, coupled with features such as AI-powered size recommendation, flexible return policies, and subscription boxes, has effectively overcome the traditional hesitation to buy clothing online without trying it on. According to the International Trade Administration data in 2024, India ranks first among 20 countries worldwide in retail e-commerce, with a CAGR of 14.1% from 2023 to 2027.

Our in-depth analysis of the children’s apparel market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Age Group |

|

|

Price Point |

|

|

Distribution Channel |

|

|

Material |

|

|

Season |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Children’s Apparel Market - Regional Analysis

APAC Market Insights

The Asia Pacific is the dominant player and is expected to hold the regional revenue share of 37.5% by the end of 2035. The market is driven by the world’s largest child population and rapidly expanding middle-class households. The market is defined by the stark contrasts between mature economies such as Japan and South Korea, where the premiumization and low birth rates define the demand, and emerging giants such as India and China, where the volume growth and formal retail expansion drive the market dynamics. Moreover, the government policies across the region actively shape the market via family support programs, trade agreements, and infrastructure development. Sustainability concerns are gaining traction, particularly in the mature markets, while value remains paramount in price-sensitive segments. Supply chain integration via regional trade agreements such as the RCEP facilitates cross-border manufacturing and distribution efficiencies.

High volume domestic consumption market and a globally integrated production hub is driving the children’s apparel market in India. According to the PIB January 2025 data, in 2023 to 2024, textiles and apparel accounted for 8.21% of India’s total exports underscoring the sector’s macroeconomic importance. Besides India holds 3.9% share of the global textile and apparel trade and ranks as the 6th largest exporter worldwide reinforcing its role in the international supply chains. The U.S. and the EU account for around 47% of India’s total T&A exports indicating strong alignment with the major children’s apparel consumption markets. This export depth, combined with large-scale domestic demand, positions India as a strategic sourcing base and growth market for children’s apparel manufacturers.

Export of Textile & Apparel

|

Commodity |

Oct-23 |

Oct-24 |

% Change |

Apr-Oct 2023 |

Apr-Oct 2024 |

% Change |

|

Readymade Garment |

909 |

1227 |

35% |

7,825 |

8,733 |

12% |

|

Cotton Textiles |

1005 |

1049 |

4% |

7,014 |

7,082 |

1% |

|

Man-made textiles |

414 |

474 |

14% |

2,958 |

3,105 |

5% |

|

Wool & Woolen textiles |

16 |

14 |

-11% |

117 |

95 |

-19% |

|

Silk Products |

13 |

14 |

5% |

70 |

98 |

40% |

|

Handloom Products |

12 |

13 |

4% |

89 |

84 |

-6% |

Source: PIB January 2025

The children’s apparel market in China operates within a large and consumption-driven retail environment supported by an extensive manufacturing infrastructure. According to the FDI November 2025 data in 2024, the total retail sales of consumer goods reached USD 60.75 trillion, increasing by 3.0% YoY, indicating a stable recovery in the domestic demand and sustained household purchasing activity. This retail expansion supports spending across the essential categories, including children’s clothing, which benefits from recurring replacement cycles. Besides, the OEC 2024 data shows that China is the leading exporter of textiles in 2024, reinforcing its position as a leading global textile producer and a core sourcing destination for international apparel brands. Further, the structured retail growth and the supply chain scale continue to support the market stability and international trade relevance.

North America Market Insights

The children’s apparel market in North America is the fastest-growing and is expected to register a CAGR of 5.6% between 2026 and 2035. The U.S. and Canada dominate the regional revenue. The trends for the market growth are premiumization of toddler wear, demand for organic cotton, and e-commerce penetration. Consumer preferences in the region are heavily influenced by brand loyalty, with parents shifting toward trusted names that signify quality and safety. A significant trend is the ongoing shift toward omnichannel retailing, where the physical stores and digital platforms offer a seamless shopping experience. The market is also adapting to shifting demographic patterns and the influence of social media on young parents' purchasing decisions.

Measurable household expenditure and structured trade flows are driving the children’s apparel market in U.S. According to the U.S. Bureau of Labor Statistics, February 2025 data, the average annual spending on boys' apparel was USD 96 and girls' apparel USD 87 per consumer unit, reflecting a consistent category allocation within household apparel budgets. Besides, the OEC 2024 data shows that the U.S. has imported USD 118 billion worth of textiles and apparel, underscoring strong reliance on global sourcing networks to meet domestic consumption needs. Further, the NLM February 2024 study shows that digital commerce is further reshaping purchasing behavior, representing a 15% to 30% increase in consumers purchasing online; therefore, these data indicate a growing demand in the U.S. market.

Average Annual Expenditure on Apparel

|

Factor |

Expenditure (USD) |

|

Apparel for women 16 and over |

655 |

|

Apparel for girls 2-16 |

87 |

|

Apparel for men 16 and over |

406 |

|

Apparel for boys 2-16 |

96 |

Source: U.S. Bureau of Labor Statistics, February 2025

Structured household spending patterns and a high reliance on textile imports are propelling the children’s apparel market in Canada. According to Statistics Canada data in November 2023, the estimated cost of raising a child from birth to age 17 is USD 293,000 (about USD 17,235 annually). Moreover, the clothing accounts for 10% of total child-related expenditures, underscoring consistent allocation toward the apparel purchases across income groups. Besides, the OEC 2024 data shows that Canada imported USD 15.6 billion worth of textiles, reflecting a strong dependence on the international manufacturing hubs to meet the domestic retail demand. This import intensity highlights opportunities for global suppliers and private-label manufacturers serving Canadian retailers. These data place Canada as a huge market growth opportunity for the market.

Europe Market Insights

Advanced and value driven landscape shaped by the robust regulatory standards and diverse consumer preferences are propelling the children’s apparel market in Europe. The trends are defined by the high penetration of premium and luxury children’s wear, mainly in Western Europe, where the disposable income levels support aspirational purchasing. Moreover, the sustainability mandates from the European Union have fundamentally altered the manufacturing and sourcing strategies, and reporting textile circularity initiatives are influencing the purchasing decisions across the member states. The market demonstrates resilience via consistent replacement cycles driven by the children’s growth patterns. The harmonization of the safety standards under the European Committee for Standardization ensures consistent quality expectations, though enforcement variations create distinct national market characteristics.

Germany represents one of the most structured and opportunity-driven children’s apparel markets in Europe. As the most populous country in the EU, Germany recorded the highest number of births in 2022 and has experienced 0.99% child population growth (2017–2022), partly supported by the migration and refugee inflows, based on the CBI February 2024 data. The children’s apparel market in Germany generated an estimated USD 9.28 billion in revenue in 2023, with projected annual growth of 1.7% during 2023 to 2027 and an estimated per capita consumption of 14.9 pieces in 2023. Further, Germany also operates under strict EU REACH compliance standards requiring suppliers to meet rigorous chemical and safety benchmarks. These data show a positive impact on the market growth.

German Childrenswear Market

|

Child population growth, 2017-2022 |

Estimated market revenue (euro), 2023 |

Estimated annual growth, 2023-2027 |

Estimated per capita volume (pieces), 2023 |

Inflation–wage increase differential, 2022 |

Average per capita purchasing power, 2022 |

|

0.99% |

7.87 bn |

1.7% |

14.9 |

4.3 |

24,807 |

Source: CBI February 2024

France is the largest child population base in the EU and EFTA region, with 11.8 million children in 2022, accounting for 17.7% of the total population, as per the CBI February 2024 data. The children’s apparel market in France generated an estimated USD 6.54 billion in revenue in 2023, with the projected annual growth of 0.89% from 2023 to 2027 and relatively high per capita consumption of 16.4 pieces. Purchasing power remains strong at USD 25,869 per capita, while the wage inflation differential stood at 2.2%, significantly below the EU average of 4.8%, supporting the spending stability. Moreover, France sources 48.6% of its apparel imports from developing countries, with imports from these markets growing at an average annual rate of 3.2%, indicating sustained opportunities for compliant international suppliers targeting mid-range and design-focused children's wear segments.

Key Children’s Apparel Market Players:

- The Children's Place (U.S.)

- Carter's, Inc. (U.S.)

- Gap Inc. (U.S.)

- Nike, Inc. (U.S.)

- Adidas AG (Germany)

- Inditex (Zara) (Spain)

- H&M (Hennes & Mauritz AB) (Sweden)

- Fast Retailing Co. (Uniqlo) (Japan)

- Shimamura Co. (Japan)

- Next plc (UK)

- Monnalisa S.p.A. (Italy)

- Jacadi (France)

- Pomme d'Api (France)

- Seed Heritage (Australia)

- Punpune (South Korea)

- Reliance Retail (India)

- Ms. Rachel (New York)

- Apparel Group India (India)

- Centric Brands LLC (New York)

- LT Apparel Group (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- The Children’s Place is a market-leading pureplay retailer in the children’s apparel market, primarily operating in North America. As a dominant player in the value segment, the company has strategically consolidated its position by focusing exclusively on kids' clothing from birth to adolescence. According to the 2024 annual report, the company has made a total revenue of USD 1,386.3 million.

- Carter’s Inc. is the largest branded marketer in the North American children’s apparel market, mainly dominating the newborn to toddlers segment. Housing renowned brands such as Carter's, OshKosh B’gosh, and Little Planet, the company holds a massive share in the essential basics and layette category. In 2024, the company made a net sales of USD 2,844 million.

- Gap Inc., via its flagship brand Gap and its subsidiary Old Navy, is a significant influencer in the casual and accessible style segment of the global children’s apparel market. GapKids has long been recognized for iconic quintessentially American basics, while Old Navy serves as the family value segment with the trend driven low cost options.

- Nike, Inc. operates at the premium performance end of the children’s apparel market, leveraging its powerful brand equity to dominate the kids' activewear and footwear sector. Unlike the traditional apparel markers Nike sells a lifestyle of aspiration and athletic achievement, commanding higher price points for products ranging from onesies to basketball jerseys.

- Adidas AG serves as the top player in the global children’s apparel market, blending high-performance sportswear with streetwear aesthetics, making their children's collections popular for both playground athletics and casual wear. The company’s strategic initiatives in the kids space focus on sustainability.

Here is a list of key players operating in the global market:

The global children’s apparel market is highly competitive and fragmented, defined by the presence of multinational players, specialty retailers, and luxury fashion houses. The key players are increasingly focusing on digital expansion, sustainability, and brand diversification to capture market share. Strategic initiatives include direct-to-consumer models leveraging social media influencers and incorporating eco-friendly materials to appeal to modern, environmentally conscious parents. The market is driven by the need for frequent wardrobe updates due to children’s rapid growth, leading to the strong demand for both affordable basics and premium designer wear. Further, the Western brands maintain a stronghold, Asia manufacturers are expanding their global footprint via innovation and aggressive marketing. For example, in Merch 2025, Ms. Rachel has officially joined the Blues Group family, joining our diverse and expanding roster of premium licenses.

Corporate Landscape of the Children’s Apparel Market:

Recent Developments

- In January 2026, Apparel Group India has expanded its partnership with the iconic global denim brand, Levi’s, by launching Levi's Kids in the Indian market. Recognising India as a key Asian market, this move introduces the celebrated brand's children's clothing line to the country for the first time.

- In December 2025, Centric Brands LLC, a leading global lifestyle brand collective, today announced the acquisition of the Vingino Group, an international children’s fashion lifestyle brand known for its innovative product and design.

- In April 2025, LT Apparel Group, a manufacturer of children’s apparel, announces the acquisition of Elder Manufacturing Company, a company that has manufactured and provided school uniforms for over 100 years. Elder includes brands Elderwear, K12 Gear, and Elderado.

- Report ID: 8407

- Published Date: Mar 03, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.