Smart Kitchen Market Outlook:

Smart Kitchen Market size was valued at USD 22.1 billion in 2025 and is projected to reach USD 64.4 billion by the end of 2035, rising at a CAGR of 11.3% during the forecast period, i.e., 2026-2035. In 2026, the industry size of smart kitchen is assessed at USD 24.6 billion.

The smart kitchen market is expanding in response to policy-driven energy efficiency targets, rising urban electrification, and increasing integration of connected home ecosystems. According to the UNEP December 2023 data, the cooling equipment represents 20% of the electricity consumption, representing a significant share of household electricity demand. The Ministry of Power July 2023 data depicts that the domestic electricity generated grew by 8.87% during 2021 to 2022, driven by appliance adoption and urban housing expansion. This rise in consumption is prompting the regulatory emphasis on energy-efficient appliances, including smart refrigerators, induction cooktops, and connected dishwashers. These developments are encouraging manufacturers to align product portfolios with compliance standards, grid efficiency requirements, and consumer energy cost considerations.

Total Electricity Generation Growth

|

Year |

Total Generation (Including Renewable Sources) (BU) |

% of growth |

|

2020-21 |

1,381.855 |

-0.52 |

|

2021-22 |

1,491.859 |

7.96 |

|

2022-23 |

1,624.158 |

8.87 |

|

2023-24 |

286.176 |

-0.72 |

Source: The Ministry of Power July 2023

Additionally, the expansion of the digital infrastructure and smart home penetration is surging the adoption across the developed and emerging economies. According to the International Telecommunication Union, October 2023 data, the global internet penetration reached 67% in 2023, enabling seamless integration of IoT-enabled kitchen systems into residential environments. On the other hand, the public investments in the smart infrastructure and sustainability initiatives are further strengthening the ecosystem. In the Asia Pacific, the government-led smart city programs and electrification initiatives are expanding the addressable market, particularly in high-density urban regions. These structural drivers, energy regulation, digital connectivity, and public infrastructure investment, are shaping procurement strategies, supply chain alignment, and long-term demand visibility within the market.

Key Smart Kitchen Market Insights Summary:

Regional Highlights:

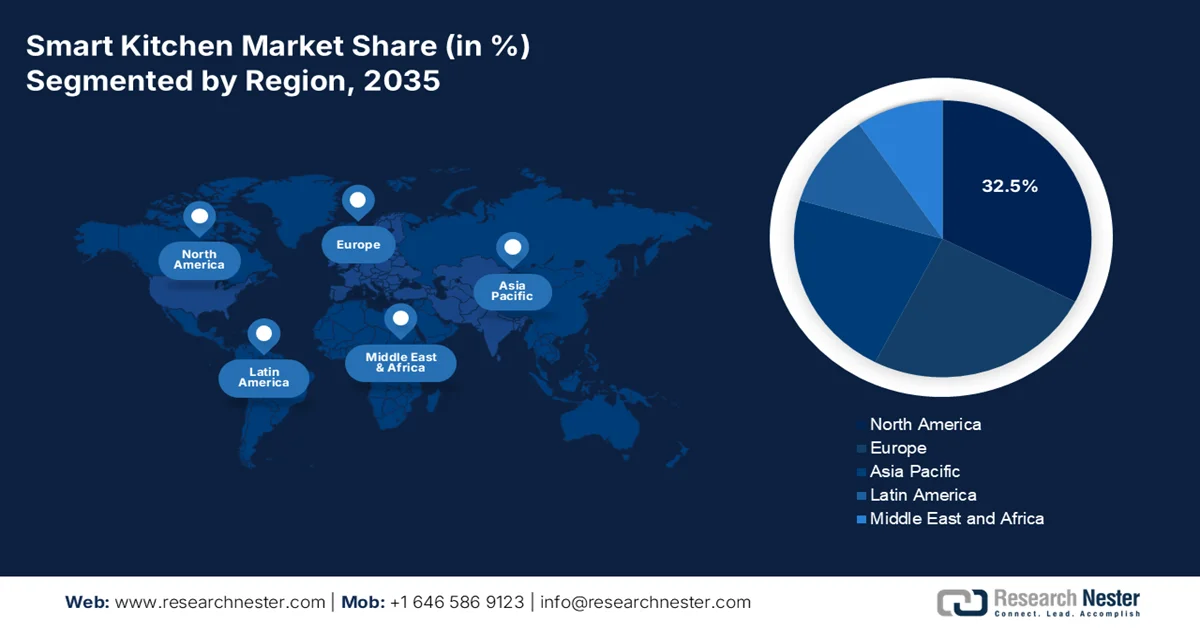

- North America is projected to lead the smart kitchen market with a 32.5% share by 2035, propelled by high broadband penetration, rising disposable incomes, and strong energy efficiency mandates

- Asia Pacific is expected to witness the fastest growth in the market during 2026–2035 with a CAGR of 11.8%, impelled by rapid urbanization and increasing investments in smart city infrastructure

Segment Insights:

- The residential segment in the smart kitchen market is anticipated to account for a 78.4% share by 2035, driven by growing demand for convenience, energy efficiency, and connected home ecosystems

- The Wi-Fi segment is expected to dominate over the forecast period 2026–2035, owing to widespread internet penetration and the need for seamless high-bandwidth connectivity in smart appliances

Key Growth Trends:

- Government-led energy efficiency program

- Expansion of smart city investments

Major Challenges:

- High product costs and price sensitivity

- Technical integration and interoperability issues

Key Players: Whirlpool Corporation (U.S.), LG Electronics (South Korea), Samsung Electronics (South Korea), BSH Hausgeräte GmbH (Germany), Electrolux AB (Sweden), Haier Group (China), Panasonic Corporation (Japan), Sony Group Corporation (Japan), Midea Group (China), Robert Bosch GmbH (Germany), Koninklijke Philips N.V. (Netherlands), De'Longhi S.p.A. (Italy), Breville Group Limited (Australia), iRobot Corporation (U.S.), Groupe SEB (France), Instant Brands Inc. (U.S.), TTK Prestige Limited (India).

Global Smart Kitchen Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 22.1 billion

- 2026 Market Size: USD 24.6 billion

- Projected Market Size: USD 64.4 billion by 2035

- Growth Forecasts: 11.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (32.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Indonesia, Vietnam, Mexico

Last updated on : 27 March, 2026

Smart Kitchen Market - Growth Drivers and Challenges

Growth Drivers

- Government-led energy efficiency program: Public investment in energy efficiency is a primary demand driver in the smart kitchen market. According to the U.S. Department of Energy, December 2023 data, the federal energy efficiency programs, including the appliance standards and labeling, have delivered over USD 1 trillion in consumer energy savings. These policies directly influence the procurement patterns by incentivizing the manufacturers to deploy smart sensor-enabled kitchen systems that comply with the efficiency benchmarks. Further, these programs are pushing demand for connected refrigerators, smart ovens, and induction systems capable of optimizing electricity use. The demand growth in the market is being reinforced by regulatory compliance requirements tied to national carbon reduction targets, particularly across North America and Europe.

- Expansion of smart city investments: The large-scale public investments in smart city infrastructure are surging the adoption of the connected home ecosystem, including smart kitchens. According to the Invest India Grid October 2025 data, nearly USD 10.67 billion is allocated for the smart city mission in India to support the infrastructure and digital integration. These investments include a residential automation framework and IoT-enabled housing, which directly increases the deployment of smart kitchen appliances. Moreover, the resulting infrastructure readiness, high-speed connectivity, smart grids, and IoT frameworks create a favorable environment for manufacturers and solution providers to scale deployments in both new and retrofit housing projects.

- Aging population and public health data: The demographic shifts are creating a demand for kitchen technologies in the smart kitchen market. According to the U.S. Census Bureau, June 2025 data, the U.S. population aged above 65 rose by 3.1%. Moreover, the health issues among the senior living facilities are also considered as one of the key drivers for the market expansion. The rehabilitation centers and public housing authorities are seeking smart kitchen solutions with medication reminders, automated shut-off features, and remote monitoring capabilities. B2B suppliers serving healthcare and senior housing markets can leverage these demographic projections to justify product development investments in accessibility-focused smart kitchen technologies.

Challenges

- High product costs and price sensitivity: The premium pricing of smart kitchen appliances remains a significant barrier to smart kitchen market entry and mass adoption. The manufacturers must embed the expensive sensors, connectivity modules, and AI capabilities, which drive up the production costs and final retail prices. This cost challenge is mainly acute in price-sensitive developing regions where the consumer hesitates to pay a premium over conventional appliances. Mid-range households remain deterred by maintenance costs and software update expenses, forcing manufacturers to either absorb margin pressure or risk limited market penetration.

- Technical integration and interoperability issues: Manufacturers face the complex challenge on the device work in diverse home ecosystems. The smart kitchen market lacks unified standards, pushing companies to invest heavily in ensuring compatibility with multiple voice assistants, smart home platforms, and connectivity protocols. Moreover, the companies are addressing this by introducing the connectivity standards. However, the fragmentation remains costly as the integrated operating system is designed to unify smart kitchen devices, offering features such as device integration, voice control, and AI-driven assistance across multiple platforms.

Smart Kitchen Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.3% |

|

Base Year Market Size (2025) |

USD 22.1 billion |

|

Forecast Year Market Size (2035) |

USD 64.4 billion |

|

Regional Scope |

|

Smart Kitchen Market Segmentation:

End user Segment Analysis

Under the end user segment, the residential sub-segment is projected to hold the largest share value of 78.4% by the end of 2035 in the smart kitchen market. The segment is driven by the increasing consumer demand for convenience, energy efficiency, and connected living experiences. Houseowners are rapidly adopting the smart appliances that offer remote monitoring capabilities and integration with the broader home automation ecosystems. The expansion of dual-income households and the growing awareness of food waste reduction have stimulated this trend as smart refrigerators and ovens provide tangible solutions for busy families. According to the OEC 2024 data, the domestic electric housewares imports in the Netherlands reached USD 784 million, providing the essential infrastructure for residential smart device adoption. This widespread connectivity, combined with the falling prices of smart technology, ensures that residential users remain the primary revenue contributors in the market.

Connectivity Technology Segment Analysis

Within the connectivity technology, Wi-Fi is anticipated to dominate the segment in the smart kitchen market, serving as the foundational communication backbone for the entire smart kitchen market. Unlike shorter-range protocols, the Wi Fi enables seamless high-bandwidth connectivity that allows appliances to connect directly to the cloud, facilitating remote user access, over-the-air firmware updates, and integration with voice assistants. This technology supports the data-intensive requirements of modern smart kitchens, including the video streaming from the in refrigerators cameras to real-time recipe synchronization. According to the Census Bureau, June 2024 data, nearly 90% of the households used the internet, with the Wi Fi being the primary connection method. This near-global penetration of Wi Fi networks in homes globally ensures that the manufacturers prioritize these connectivity standards.

Distribution Channel Segment Analysis

Offline is leading the distribution channel segment in the smart kitchen market due to the high-touch nature of smart appliance purchases. The consumer investing in premium, technologically advanced kitchen equipment often prefers physical interaction before committing to a purchase. The stores offer experiential showrooms where the consumer can see, touch, and operate the smart refrigerators or ovens, receive expert consultations, and understand the integration capabilities firsthand. This experience is vital for building consumer confidence in complex products. The U.S. Census Bureau indicates that the electronics and appliances store accounted for billions in annual sales, showing a persistent consumer preference for in-person research and purchase of high-value technological goods. This trust in specialized retail expertise ensures that offline channels remain the dominant revenue generator even as e-commerce grows.

Our in-depth analysis of the smart kitchen market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Connectivity Technology |

|

|

Application |

|

|

End user |

|

|

Distribution Channel |

|

|

Technology |

|

|

Price Point |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Smart Kitchen Market - Regional Analysis

North America Market Insights

North America is projected to maintain its leadership position in the global smart kitchen market and is expected to hold the regional revenue share of 32.5% by the end of 2035. The region is driven by the high broadband penetration, consumer disposable income, and aggressive energy efficiency mandates. The region benefits from a mature retail infrastructure and early adoption of connected home technologies. The key drivers include energy regulations and the integration of smart appliances into the federal procurement programs. The trend towards the aging in place and remote monitoring via kitchen devices further accelerates the demand. Moreover, the convergence of grid interactive technologies and cybersecurity standardization solidifies North America’s revenue dominance, with the U.S. contributing the majority share due to its scale and innovation ecosystem.

The strong federal support for the energy efficiency digital infrastructure and residential electrification is shaping the smart kitchen market in the U.S. According to the IEEMA 2022 data, the residential electricity consumption reached 1,509 billion kWh, reflecting sustained growth in appliance usage and the connected home systems. On the other hand, the connectivity is another key enabler, with the NITA November 2024 data confirming that the USD 65 billion has been allocated under the Infrastructure Investment and Jobs Act for broadband expansion, accelerating IoT adoption across households. These policy-backed investments are supporting the integration of connected appliances such as smart refrigerators, ovens, and dishwashers into residential and multi-unit housing. As a result, these trends are positioning the market for steady growth.

U.S. Energy Demand and Power Generation

|

Category |

2022 |

2023 |

2024 |

2025 |

|

Total Power Demand (billion kWh) |

— |

4,000 |

4,099 |

4,128 |

|

Residential Electricity Sales (billion kWh) |

1,509 |

— |

1,511 |

— |

|

Commercial Electricity Sales (billion kWh) |

1,391 |

— |

1,396 |

— |

|

Industrial Electricity Sales (billion kWh) |

— |

— |

1,042 |

— |

|

Natural Gas Share of Power Generation (%) |

— |

42% |

42% |

41% |

|

Coal Share of Power Generation (%) |

— |

17% |

15% |

14% |

|

Renewables Share of Power Generation (%) |

— |

21% |

24% |

25% |

|

Nuclear Share of Power Generation (%) |

— |

19% |

19% |

19% |

|

Residential Gas Consumption (bcfd) |

— |

— |

12.41 |

— |

|

Commercial Gas Consumption (bcfd) |

— |

— |

9.17 |

— |

|

Industrial Gas Consumption (bcfd) |

— |

— |

23.19 |

— |

|

Gas for Power Generation (bcfd) |

— |

35.43 |

35.98 |

— |

Source: IEEMA 2022

The strong energy efficiency mandates and the measurable household consumption trends are fueling the smart kitchen market in Canada. According to the Government of Canada, March 2025 data, the household appliances account for 14.1% of total residential energy use across more than 16.4 million homes, along with over 500,000 commercial and institutional buildings, underscoring a substantial installed base for efficiency upgrades. On the other hand, the Canada’s early adoption of ENERGY STAR standards requiring a minimum 95% annual fuel utilization efficiency (AFUE), nearly a decade ahead of the U.S. compliance timeline, as per the Efficiency of Canada March 2024 report demonstrates a proactive regulatory environment that is accelerating replacement cycles. These factors are influencing procurement strategies across residential and commercial segments, thus fueling the market growth.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region during the assessed period, 2026 to 2035, and is poised to grow at a CAGR of 11.8%. The region is driven by rapid urbanization, expanding middle-class populations, and aggressive government investment in smart city infrastructure. Unlike the mature market, where the replacement drives the demand, the APAC growth is fueled by the new household formation and first-time adoption of connected appliances. Additionally, the regional population growth is creating a demand for modern housing and embedded kitchen technologies. A dominant trend is the integration of smart appliances into national digital transformation agendas, with China, Japan, and South Korea prioritizing the IoT infrastructure development. The government-led smart city projects and rising disposable incomes position APAC as the growth engine for the smart kitchen industry through the forecast period.

The scale driven food infrastructure and rising smart appliance penetration are fueling the smart kitchen market in India. As per the Akshaya Patra Foundation, July 2023 data, the large centralized kitchen models, such as those capable of producing up to 100,000 meals per day, highlight the increasing demand for the semi-automated and efficient cooking systems, particularly in public food programs and contract catering. On the other hand, the IBEF November 2025 data depicts that the smart home adoption is accelerating, with the penetration reaching 8% to 10% in 2023, up from below 4% pre-pandemic, and the market is valued at USD 10.3 billion, projected to reach USD 16 billion by 2028. India’s household kitchen appliances market stood at USD 15.2 billion in 2024, driven by the strong demand for refrigerators and rapid dishwasher adoption. These trends indicate an optimistic growth in the nation.

Strong electrification, digital infrastructure, and government-backed smart home initiatives are propelling the growth of the smart kitchen market in China. According to the People’s Republic of China, total electricity consumption exceeded 10.4 trillion kWh in 2025, reflecting sustained growth in residential and appliance usage. The country’s high digital penetration further strengthens adoption, with the March 2024 data reporting over 1.09 billion internet users in 2023, enabling large-scale integration of connected home and kitchen appliances. Additionally, urbanization continues to expand the addressable market with the urban population exceeding 66% of the total population in 2023, supporting higher appliance ownership and the modernization of kitchen environments. These factors, government-led digitalization, rising electricity demand, and a large-scale urban consumer base, are positioning China as a high-growth market for smart kitchen solutions across both new housing and replacement demand cycles.

Europe Market Insights

The smart kitchen market is Europe is showing active growth and is reshaped by the region’s aggressive circular economy action plan. Unlike the other regions where the convenience is the primary driver, the European demand is heavily influenced by the energy labeling regulations and waste reduction directives from the European Commission. Moreover, the household energy consumption reports show that cooking and refrigeration represent a significant portion, making them primary targets for efficiency mandates. A dominant trend is the integration of smart appliances, which aims to double annual energy renovation rates across member states. The convergence of mandated energy efficiency carbon reduction targets and an aging population's desire for independent living creates sustained institutional and consumer demand across the region's diverse markets.

The smart kitchen market in UK is influenced by rising household energy consumption, regulatory efficiency targets, and digital infrastructure expansion. According to the Adam Smith Institute, January 2024 data, the total electricity consumption reached 312 TWh in 2023, with the residential sector accounting for a significant share, driven by appliance usage. Additionally, the digital readiness is strengthening adoption, with the Government of the UK's December 2025 data reporting in 2024 that 96% of UK households had internet access, enabling seamless integration of connected kitchen appliances. These factors are driving procurement toward energy-efficient and IoT-enabled kitchen systems across residential and multi-unit housing. As a result, manufacturers are aligning with compliance standards and connectivity requirements, positioning the UK as a steady-growth market.

The strong export performance and industrial manufacturing capacity of domestic electric appliances are fueling the smart kitchen market in Germany. According to the OEC 2024 data, Germany exported USD 1.27 billion worth of domestic electric housewares, showing a robust production base and international demand for the electrically powered kitchen equipment. This export strength is complemented by policy-driven energy efficiency initiatives, which emphasize reduced household energy consumption and electrification of appliances. Moreover, the broader digital and sustainability strategy aligned with the EU directives continues to promote the adoption of energy-efficient and connected home systems. These factors position the nation as a key contributor to both regional demand and global supply within the smart kitchen ecosystem.

Key Smart Kitchen Market Players:

- Whirlpool Corporation (U.S.)

- LG Electronics (South Korea)

- Samsung Electronics (South Korea)

- BSH Hausgeräte GmbH (Germany)

- Electrolux AB (Sweden)

- Haier Group (China)

- Panasonic Corporation (Japan)

- Sony Group Corporation (Japan)

- Midea Group (China)

- Robert Bosch GmbH (Germany)

- Koninklijke Philips N.V. (Netherlands)

- De'Longhi S.p.A. (Italy)

- Breville Group Limited (Australia)

- iRobot Corporation (U.S.)

- Groupe SEB (France)

- Instant Brands Inc. (U.S.)

- TTK Prestige Limited (India)

- Xiaomi Corporation (China)

- Miele & Cie. KG (Germany)

- Hafele (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Whirlpool Corporation is a dominant player in the smart kitchen market, leveraging its deep heritage in home appliances to drive connectivity and convenience. The company has significantly advanced the market by integrating its latest technology, which utilizes sensors and machine learning to automate the cooking processes and optimize the appliance performance. By embedding smart functionality, the company ensures that consumers can monitor and control the kitchen environment.

- LG Electronics has redefined innovation in the smart kitchen market by advancing the concept of the fully integrated intelligent home. Through its AI platform, LG enables its kitchen appliances to learn the user's habits and communicate seamlessly with each other. The company has significantly advanced the market by integrating features based on ingredients. In 2024, the company made sales of 87,728,182.

- Samsung Electronics has made significant advancements in the smart kitchen market by focusing on ecosystem integration and visual intelligence. The strategy connects the home appliances, such as refrigerators, with other smart devices in the home. The Family Hub represents a major leap forward, utilizing internal cameras to allow users to view fridge contents remotely. In 2024, the company made a revenue of USD 220,726,499.

- BSH Hausgerate GmbH has advanced the smart kitchen market via its commitment to precision engineering and the Home Connect ecosystem. The company focuses on delivering smart appliances that enhance efficiency and sustainability without compromising on design. Their advancements in the market include ovens with sensors that automatically regulate the temperature.

- Electrolux AB has made strategic advancements in the smart kitchen market by focusing on well-being and sustainable eating habits via intuitive technology. The manufacturer integrates smart features across its premium brands, aiming to simplify complex cooking techniques for the home user. The key advancements are their work with precision cooking, which combines precision and technology.

Here is a list of key players operating in the global smart kitchen market:

The competitive landscape of the smart kitchen market is defined by a strong battle between established home appliance giants and agile consumer electronics innovators. The key players are actively pursuing ecosystem integration, ensuring their smart ovens, refrigerators, and cooking appliances can communicate seamlessly within a connected home network. For example, in September 2025, Hafele expands its North India presence with the new appliances studio in Noida. Further, there is a significant push toward sustainability and energy efficiency with manufacturers developing appliances that minimize food waste and reduce energy consumption. Companies are also forming strategic partnerships with food delivery services and recipe platforms to offer a holistic cooking experience, moving beyond the appliance itself to become a central part of the consumer’s daily food journey.

Corporate Landscape of the Smart Kitchen Market:

Recent Developments

- In June 2025, BSH Home Appliances Pvt. Ltd. announced the launch of its first Siemens Brand Store in Coimbatore, Tamil Nadu. Built to Siemens’ global Retail Excellence standards, the new store marks a strategic expansion in response to growing demand in South India.

- In June 2025, Samsung introduced its 2025 Bespoke AI appliance lineup, built on four distinct consumer benefits such as Easy, Care, Save and Secure to enrich and simplify your lives with AI. A new compact display debuts on Bespoke refrigerators, while the 7-inch AI Home is integrated into the Bespoke AI Laundry Combo for smarter, personalized laundry care

- In January 2024, Panasonic announced an expanded partnership with Fresco, the leading smart kitchen platform for the world’s top appliance brands. The companies will collaborate to deliver a revolutionary cooking assistant for Panasonic kitchen appliances, starting with the Panasonic HomeCHEF 4-in-1 multi-oven.

- Report ID: 8478

- Published Date: Mar 27, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Smart Kitchen Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.