Polyurethanes Market Outlook:

Polyurethanes Market size was over USD 85.4 billion in 2025 and is anticipated to exceed USD 310.8 billion by the end of 2035, growing at over 13.8% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of polyurethanes is evaluated at USD 97.1 billion.

The global polyurethanes market is growing significantly on account of its expanding applications in construction, automotive, furniture, appliances, and packaging industries, where there is a heightened demand for lightweight and energy-efficient materials. Growth is being supported by the shift toward sustainable building practices, the expansion of the cold chain, and insulation requirements. According to the article published by the National Institute of Health (NIH) in August 2025, polyurethanes function through dynamic covalent bonds or reversible non-covalent interactions, and they help restore mechanical properties and extend the lifespan of flexible materials, especially in coatings and electronics. In addition, the study highlights strong application potential in flexible electronic devices due to improved damage tolerance and thus elevates the uptake of polyurethanes.

Furthermore, the technological advancements, which include bio-based polyols, low-emission formulations, and improved recycling and circular economy initiatives, are reshaping product development and encouraging innovation across the value chain. This prompts a profitable business environment for pioneers in the market. As per an article published by World Integrated Trade Solution in 2024, global trade of polyurethanes in primary forms was led by major exporting regions including Europe, Germany, China, the U.S. and Italy, which reflects the dominance of established chemical manufacturing hubs. Besides, export values and quantities change across countries, wherein both high-value and high-volume exporters contribute to international supply chains. Hence, the data indicates a geographically diversified but highly concentrated market structure, in which Europe, East Asia, and North America are registered as the primary centers of polyurethane production and export.

Global Polyurethane Export Rankings 2024: Top Countries by Shipment Value and Volume

|

Country/Region |

Export Value (USD ‘000) |

Quantity (Kg) |

|

Europe |

1,664,660.13 |

399,727,000 |

|

Germany |

1,489,022.09 |

320,307,000 |

|

China |

962,420.64 |

411,327,000 |

|

U.S. |

852,051.84 |

152,676,000 |

|

Italy |

580,826.08 |

156,855,000 |

|

Other Asia, nes |

381,549.35 |

96,689,100 |

|

Korea, Rep. |

312,595.13 |

72,560,600 |

|

Belgium |

310,349.46 |

66,249,400 |

|

Netherlands |

306,296.64 |

76,016,700 |

|

Spain |

301,274.14 |

71,079,400 |

|

Japan |

238,210.31 |

34,102,700 |

Source: WITS

Global Polyurethane Imports 2023: Top Countries by Trade Value and Volume

|

Country/Region |

Import Value (USD ‘000) |

Quantity (Kg) |

|

China |

715,502.36 |

143,094,000 |

|

Germany |

463,629.35 |

98,877,800 |

|

Vietnam |

455,564.26 |

96,062,700 |

|

U.S. |

452,255.64 |

84,136,700 |

|

European Union |

375,180.84 |

75,619,600 |

|

Italy |

367,823.77 |

75,799,700 |

|

India |

348,795.70 |

132,233,000 |

|

Mexico |

280,839.20 |

59,611,100 |

|

France |

240,868.13 |

- |

|

Canada |

232,874.18 |

38,382,300 |

|

Spain |

191,548.40 |

48,706,200 |

Source: WITS

Key Polyurethanes Market Insights Summary:

Regional Highlights:

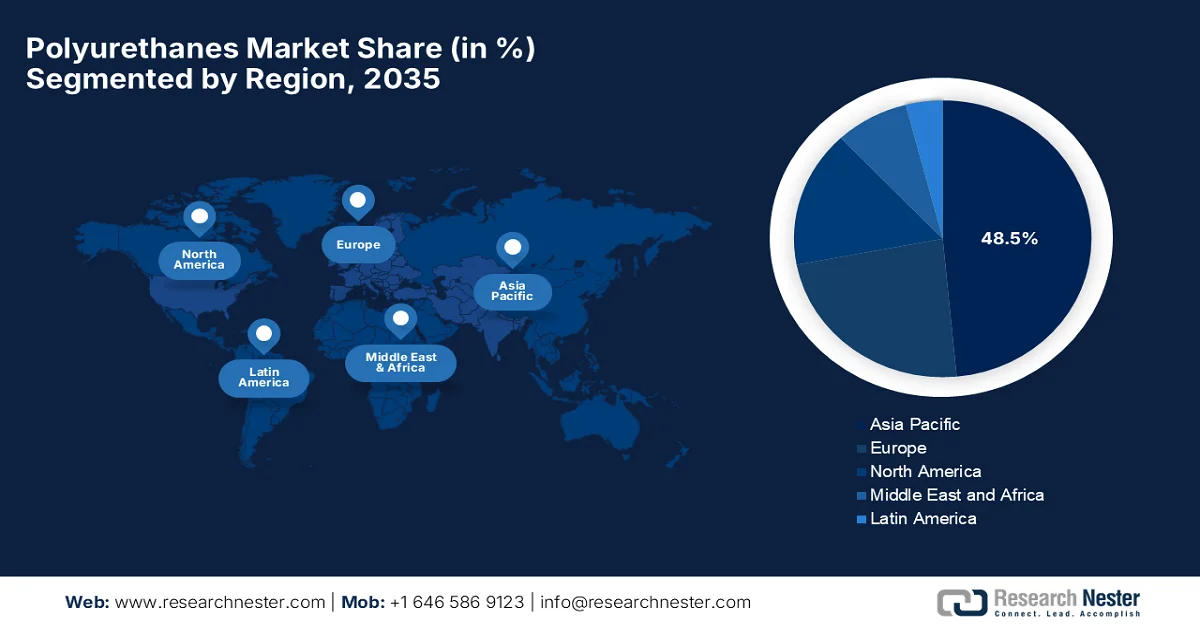

- Asia Pacific polyurethanes market is projected to capture 48.5% of the market share by 2035, reinforcing its leadership position amid rapid industrialization, accelerating urbanization, and massive infrastructure developments across key economies such as China, India, and Southeast Asia

- North America is expected to register considerable growth during 2026-2035, supported by stringent building codes and energy-efficiency mandates driving the adoption of rigid spray foam insulation in residential and commercial buildings

Segment Insights:

- In the polyurethanes market, methylene diphenyl di-isocyanate (MDI) is anticipated to account for 35.4% of the share by 2035, underpinned by its extensive use in rigid polyurethane foams for construction insulation panels, refrigeration, and cold-chain logistics infrastructure

- The construction application segment is set to expand significantly by 2035, fueled by the increasing adoption of pre-engineered and modular building systems requiring high-performance insulation and bonding materials

Key Growth Trends:

- Footwear and apparel comfort

- Cold chain logistics expansion

Major Challenges:

- Feedstock volatility and escalating production costs

- End-of-life waste management and circularity failures

Key Players: BASF SE (Germany), Covestro AG (Germany), Dow Inc. (U.S.), Huntsman Corporation (U.S.), Tosoh Corporation (Japan), Mitsui Chemicals, Inc. (Japan), Lubrizol Corporation (U.S.), INOAC Corporation (Japan), RAMPF Holding GmbH & Co. KG (Germany), Carpenter Co. (U.S.), Milliken & Company (U.S.), Azelis (Belgium), Woodbridge (Canada).

Global Polyurethanes Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 85.4 billion

- 2026 Market Size: USD 97.1 billion

- Projected Market Size: USD 310.8 billion by 2035

- Growth Forecasts: 13.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (48.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Germany, Japan, India

- Emerging Countries: India, Vietnam, Indonesia, Mexico, Thailand

Last updated on : 7 July, 2026

Polyurethanes Market - Growth Drivers and Challenges

Growth Drivers

- Footwear and apparel comfort: The booming global athleisure industry fuels an intense demand for polyurethane elastomers and flexible foams. Footwear brands across different nations have been utilizing these polymers to manufacture lightweight, shock-absorbing midsoles that enhance athletic performance thus boosting demand in the polyurethanes market. In November 2025, Huntsman, in collaboration with Steitz Secura, announced that it had developed a breakthrough DALTOPED® polyurethane midsole system that enables safety footwear to incorporate recycled PU without changing existing production processes. This innovation helps close the loop on manufacturing waste by reusing scrap polyurethane from production, thus contributing to the market’s expansion.

- Cold chain logistics expansion: The expansion of worldwide pharmaceutical and perishable food supply chains positively contributes to the expansion of the market. The rigid foam panels are used in refrigerated trucks, shipping containers, and commercial cold storage facilities to maintain precise temperatures. For instance, in May 2023, DHL Global Forwarding announced that it inaugurated a new pharma-focused logistics hub at Indianapolis International Airport to strengthen its life sciences and healthcare supply chain network in the U.S. It is a USD 1.5 million, 30,000 sq. ft. facility and is designed for temperature-controlled air cargo handling, especially for pharmaceuticals, whereas it provides end-to-end cold chain services, thus heightening the demand for polyurethanes.

Challenges

- Feedstock volatility and escalating production costs: The global polyurethanes market faces severe pressure from fluctuating raw material prices due to its dependence on petroleum-derived feedstocks. Therefore, the essential components such as methylene diphenyl diisocyanate, toluene diisocyanate, and polyols suffer frequent price swings due to geopolitical conflicts, crude oil fluctuations, and sudden supply chain issues. Meanwhile, in China, the capacity surpluses have led to reductions in MDI and TDI prices, thereby forcing integrated global producers to curb production rates. At the same time, unexpected supply constraints hit smaller downstream converters hard, wherein feedstock price swings account for a maximum of their total cost of goods, thus causing hindrance to the market’s expansion and exposure.

- End-of-life waste management and circularity failures: The commercial circularity goals are also a major barrier for the global market due to low recycling efficiency, with very low amounts being recycled. The chemical stability of crosslinked urethane networks resists standard thermal depolymerization, which in turn forces industries to dump huge quantities of flexible foams and insulation panels into landfills or incinerators. Apart from this, mechanical recycling methods that grind foam into powder require excessive synthetic binders and intense heat energy, which causes output to be basic, low-margin products such as underlay sheets. In this context, managing the logistics of transporting bulky but lightweight foam waste across long distances makes commercial recycling economically unviable.

Polyurethanes Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

13.8% |

|

Base Year Market Size (2025) |

USD 85.4 billion |

|

Forecast Year Market Size (2035) |

USD 310.8 billion |

|

Regional Scope |

|

Polyurethanes Market Segmentation:

Raw Material Segment Analysis

The methylene diphenyl di-isocyanate (MDI), which is under the raw material segment, is anticipated to garner the highest share of 35.4% in the polyurethanes market during the forecast period. The segment’s dominance is largely propelled by its extensive use in rigid polyurethane foams, which are applied in construction insulation panels, refrigeration, and cold-chain logistics infrastructure. Its strong demand is also supported by growing automotive lightweighting requirements and energy-efficient building standards. In January 2024, BASF and Carlisle Construction Materials entered into a partnership to explore the use of Lupranate® ZERO, which is the world’s first zero-carbon-footprint MDI, in producing polyisocyanurate insulation boards and rigid polyurethane foam. This initiative is highly focused on reducing emissions in construction materials while maintaining high product performance, thus supporting the segment’s dominant position.

Application Segment Analysis

In terms of application, the construction segment is forecasted to grow considerably in the market by the conclusion of 2035. The increasing adoption of pre-engineered and modular building systems, which require high-performance insulation and bonding materials, is the main factor driving the segment’s leadership. Rising investments in retrofit and renovation activities of aging infrastructure in developed economies are also boosting demand for polyurethane-based solutions. For instance, in August 2023, Covestro completed a new polyurethane dispersions production facility in Shanghai, which is designed to meet rising demand for environmentally compatible coatings and adhesives across Asia Pacific. The plant will serve industries such as automotive, construction, footwear, packaging, and furniture, thus positively benefiting the segment’s expansion.

Product Segment Analysis

On the basis of product, rigid foam is expected to attain a noteworthy share in the market during the discussed timeframe. The high structural strength and load-bearing capability make it suitable for demanding applications other than basic insulation. It is also widely adopted in sandwich panels and prefabricated construction systems, which are increasingly used in modular building and industrial infrastructure projects. In addition, the sub segment’s low water absorption and long-term dimensional stability enhance performance in harsh environments, supporting its use in roofing, wall insulation, and industrial enclosures. Apart from this, the segment benefits from its excellent fire-retardant formulations, improving safety compliance in building applications. Furthermore, the heightened demand for renewable energy infrastructure, such as insulation in wind turbine components and related enclosures, is also supporting its adoption.

Our in-depth analysis of the polyurethanes includes the following segments:

|

Segment |

Subsegments |

|

Raw Material |

|

|

Application |

|

|

Product |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Polyurethanes Market - Regional Analysis

APAC Market Insights

Asia Pacific polyurethanes market is anticipated to be the dominating capturing around 48.5% of the share during the forecast period. The region’s dominance is effectively propelled by rapid industrialization, accelerating urbanization, and massive infrastructure developments across key economies such as China, India, and Southeast Asia. Asia Pacific also benefits from domestic manufacturing bases in the automotive, construction, and electronics sectors, along with a booming furniture and bedding market driven by a growing middle-class population. In March 2023, Covestro began constructing new extrusion lines at its Map Ta Phut Industrial Park in Thailand to expand global capacity for polycarbonate specialty films. The investment will support growing demand across the region and hence denote a positive opportunity for polyurethanes.

The fully integrated domestic supply chains and immense chemical production capacities are positioning China polyurethanes market as a primary manufacturing and consumption hub. The country’s market is effectively propelled by its massive automotive sector, where advanced polyurethanes are heavily deployed for cabin comfort and lightweighting electric vehicles. Based on government data published in January 2025, China’s auto industry reached surging numbers in 2024, with production at 31.28 million vehicles and sales at 31.44 million units, marking steady year-on-year growth. A major driver of this expansion was new energy vehicles, which crossed 10 million units in both production and sales for the first time, thereby accounting for over 40% of total vehicle sales, thus reflecting a sustained demand for polyurethanes.

In India, the market is poised for explosive growth, which is facilitated by the country's massive infrastructure push, urbanization, and a surging middle-class consumer base. Market expansion is also being driven by the booming construction and real estate sectors, which adopt rigid polyurethane insulation panels for energy-efficient commercial buildings and modern cold storage networks. In this context, Covestro India in July 2025 signed an MoU with CSIR-National Chemical Laboratory to develop advanced polyurethane upcycling solutions as part of a CSR initiative focused on improving material circularity. This collaboration combines NCL’s scientific knowledge with Covestro’s industry experience to address key limitations in current polyurethane recycling methods, thus elevating the growth potential of the market.

North America Market Insights

In North America market is expected to witness considerable growth from 2026 to 2035. The region benefits from a robust construction sector, where stringent building codes and energy-efficiency mandates drive the adoption of rigid spray foam insulation in residential and commercial buildings. In addition, the well-established aerospace, consumer bedding, and medical device manufacturing hubs maintain a stable demand for polyurethane elastomers and flexible foams. In July 2026, the article published by the U.S. Census Bureau disclosed that the U.S. construction spending in May 2026 edged up 0.1% from April to a seasonally adjusted annual rate of USD 2.21 trillion. It also outlines that private construction spending was USD 1.67 trillion, with residential construction rising 0.3%, whereas public construction increased 0.5% to USD 541.2 billion, thus elevating the demand for polyurethanes in the country.

Advanced technological innovation, strict regulatory compliance, and a strong shift toward circularity are the visible trends reshaping the growth dynamics of the U.S. polyurethanes market. In addition, a highly developed consumer retail sector propels a constant demand for premium flexible foams, which are used in high-end bedding, furniture, and medical devices. In June 2024, the article published by the U.S. Department of Energy stated that its funded startup, Algenesis Corporation, developed a bio-based polyurethane made from algae-derived oil that naturally biodegrades and offers a reliable solution to the growing microplastic pollution problem. The material is designed so microorganisms can completely break it down, leaving no persistent microplastics behind. Also, this innovation has already attracted industry partners, including Trelleborg and RhinoShield, to develop biodegradable coated fabrics and smartphone cases, thus making it suitable for standard market growth.

In Canada market is extensively supported by a strong focus on extreme-weather thermal performance, sustainable infrastructure, and advanced manufacturing. The country’s market also benefits from robust aerospace and high-end furniture sectors, which maintain a steady demand for specialized elastomers and flexible foams. For instance, Elastochem in September 2024 achieved a 45-minute (Canada) and 1-hour (Canada and U.S.) fire rating for its Insulthane® Extreme spray polyurethane foam insulation in a new metal wall construction system, thus expanding its use in warehouses, industrial, agricultural, and commercial buildings. This insulation provides an air and moisture barrier, industry-leading thermal performance, GREENGUARD GOLD certification, and a global warming potential of one.

Europe Market Insights

The Europe market is gaining enhanced traction mainly due to strict environmental regulations and a shift toward a circular economy. Regional demand is facilitated by premier automotive manufacturing hubs that rely extensively on specialized polyurethane composites for acoustic management and battery insulation in electric vehicles. Europe’s chemical manufacturers lead the global industry in scaling up chemical recycling infrastructure, implementing mass-balance supply chains. As per an article published by Europur in March 2025, Europe’s polyurethane industry contributes remarkably to the region’s economic welfare, generating around USD 161 billion annually, supporting 700,000 direct jobs, and involving nearly 80,000 companies across Europe. The report also found that more than 1.7 million companies use polyurethane products, generating around USD 91 billion in additional economic activity, whereas flexible foams contribute about USD 60 billion in value.

In Germany polyurethanes market is growing significantly on account of highly automated manufacturing, premium material standards, and a rapid transition toward industrial circularity. Simultaneously, stringent national energy efficiency laws drive massive demand for rigid polyurethane insulation foams across the residential and commercial construction renovation sectors. In February 2025, researchers at the Fraunhofer Institute for Applied Polymer Research developed FOIM, which is an innovative shape-memory polyurethane foil that expands into foam when heated to 60°C, enabling isocyanate-free foam production, thus improving workplace safety by eliminating exposure to hazardous isocyanates. This material expands 16 times in thickness which is from 2.5 mm to 40 mm, and offers significant storage and transportation advantages while allowing customizable properties for different applications.

The evolving building regulations, net-zero commitments, and localized manufacturing strengths are positively influencing the growth of polyurethanes market in the UK. In addition, the country’s strong mattress, furniture, and subsea oil and gas pipeline industries maintain a steady baseline demand for flexible foams and durable marine-grade protective elastomers. The country’s market benefits from increasing investment in energy-efficient building insulation, which is accelerating the adoption of high-performance polyurethane systems across residential and commercial construction. Apart from this sustainability-driven innovation, including bio-based polyols and recycling initiatives, is reshaping product development across the UK polyurethane value chain and thus encouraging more players to establish their footprint in the country.

Key Polyurethanes Market Players:

- BASF SE (Germany)

- Covestro AG (Germany)

- Dow Inc. (U.S.)

- Huntsman Corporation (U.S.)

- Tosoh Corporation (Japan)

- Mitsui Chemicals, Inc. (Japan)

- Lubrizol Corporation (U.S.)

- INOAC Corporation (Japan)

- RAMPF Holding GmbH & Co. KG (Germany)

- Carpenter Co. (U.S.)

- Milliken & Company (U.S.)

- Azelis (Belgium)

- Woodbridge (Canada)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BASF SE is one of the world's largest polyurethane manufacturers, which is offering polyurethane systems, thermoplastic polyurethanes, polyurethane elastomers, and specialty solutions. The company has established strong capabilities in R&D, vertically integrated operations, and a focus on sustainable polyurethane technologies.

- Covestro AG is a predominant leader in terms of polyurethane materials, manufacturing methylene diphenyl diisocyanate, polyether polyols, and thermoplastic polyurethanes. The company's polyurethane products are being utilized extensively in insulation, automotive interiors, furniture, electronics, refrigeration, and footwear applications.

- Dow Inc. is yet another prominent producer of polyurethane materials which is supplying polyols, isocyanates, polyurethane systems, and specialty formulations. Besides, the firm benefits from an extensive global manufacturing footprint that enables reliable supply across growing regional markets.

- Huntsman Corporation is one of the world's leading manufacturers of MDI-based polyurethane products. The company primarily serves construction, automotive, aerospace, furniture, footwear, and industrial markets worldwide.

- Tosoh Corporation specializes in polymeric MDI, modified MDI, and polyurethane raw materials, which are to be used in rigid foams, flexible foams, elastomers, coatings, adhesives, and sealants. The company has established a strong presence across Asia, thereby expanding its global customer base through advanced manufacturing technologies.

Here is a list of key players operating in the global market:

The global polyurethanes market hosts a small group of multinational manufacturers that account for a significant share of global production, whereas a large number of regional producers have been working with niche applications and domestic markets. Market leaders compete in terms of integrated manufacturing capabilities, polyurethane portfolios, global production footprints, and sustainability initiatives such as bio-based and low-emission polyurethane solutions. Meanwhile, China has become a major manufacturing hub due to capacity expansion, whereas Europe- and North America-based manufacturers maintain strong positions through advanced technologies and specialty polyurethane systems. For instance, BASF in March 2025 introduced its Loop portfolio at CHINAPLAS 2025, which consists of polyurethane solutions made with recycled content for the footwear, automotive, and synthetic leather industries in China. BASF converts end-of-life polyurethane waste into high-quality recycled raw materials for new PU products, thus supporting a circular economy.

Corporate Landscape of the Market:

Recent Developments

- In February 2026, Lubrizol introduced Tolerathane™ thermoplastic polyurethane, which is a new medical-grade material specifically engineered for implantable medical devices. This material is designed to provide improved durability in the body while maintaining softness and mechanical strength.

- In February 2026, Milliken & Company and Azelis entered into a distribution partnership in India to expand the availability of Reactint® polyurethane colorant solutions. This particular collaboration aims to strengthen Milliken's presence in India's market.

- Report ID: 8660

- Published Date: Jul 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.