Medical Suction Devices Market Outlook:

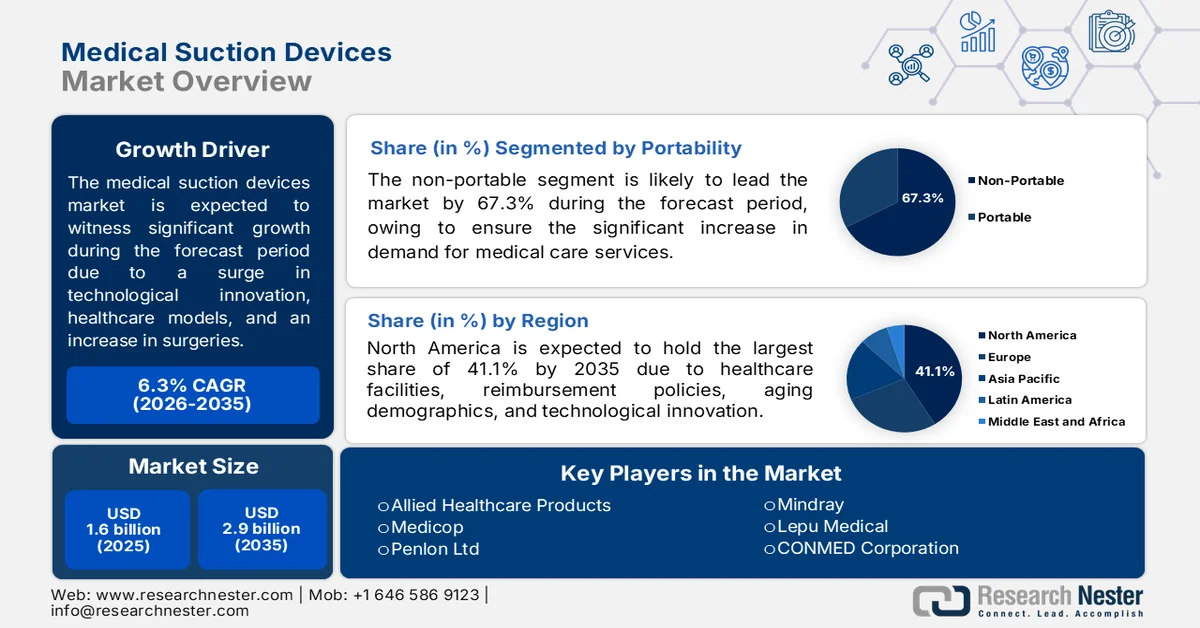

Medical Suction Devices Market size was valued at USD 1.6 billion in 2025 and is predicted to cross USD 2.9 billion by the end of 2035, expanding at more than 6.3% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of medical suction devices is estimated at USD 1.7 billion.

The worldwide medical suction devices market is readily undergoing a transformative evolution, owing to healthcare delivery model reforms, demographic shifts, technological convergence, an expansion in health and medical services, an increase in surgeries, product development priorities, and competitive dynamics. According to official statistics published by NLM in October 2024, a clinical study conducted by the University of Michigan found that the sudden switch from paper to electronic health records led to a 3% reduction in outpatient care expenses, equating to monthly savings of USD 5.1 per patient. This effectively indicates a significant amount across large-scale hospital networks. Moreover, limitation in doctors is projected to range between 37,800 and 124,000 in the upcoming decade. Therefore, to overcome this, significant innovations in technology are readily accessible for supporting doctors, thus proliferating the medical suction devices market growth and demand globally.

Furthermore, the integration of real-time monitoring and smart sensors, the adoption of pre-assembled and single-use suction kits, convergence with negative pressure wound therapy systems, ergonomic and aesthetic design for home utilization, along with blockchain-enabled device tracking and maintenance logging, are a few trends that are enhancing the medical suction devices market globally. As stated in a data report published by the World Integrated Trade Solution (WITS) in 2023, the U.S. is considered the top importer of medical appliances and instruments with a trade valuation of USD 19,524,852.4 and shipments of 2,377,630,000 units as of 2023. Likewise, China amounts to USD 5,451,937.0 of the supply with 764,181,000 units of devices that readily support the adoption of advanced devices. Meanwhile, the supply dynamic of medical instruments also play a huge role in enhancing the utilization of devices and bolstering the market exposure.

2024 Medical Instruments Global Export and Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

U.S. |

35.8 billion |

41.3 billion |

|

Mexico |

19.3 billion |

- |

|

Germany |

18.4 billion |

12.7 billion |

|

Netherlands |

- |

15.6 billion |

|

Global Trade Valuation |

176.0 billion |

|

|

Global Trade Share |

0.7% |

|

|

Product Complexity |

0.8 |

|

|

Export Growth |

3.2% |

|

Source: OEC

Key Medical Suction Devices Market Insights Summary:

Regional Highlights:

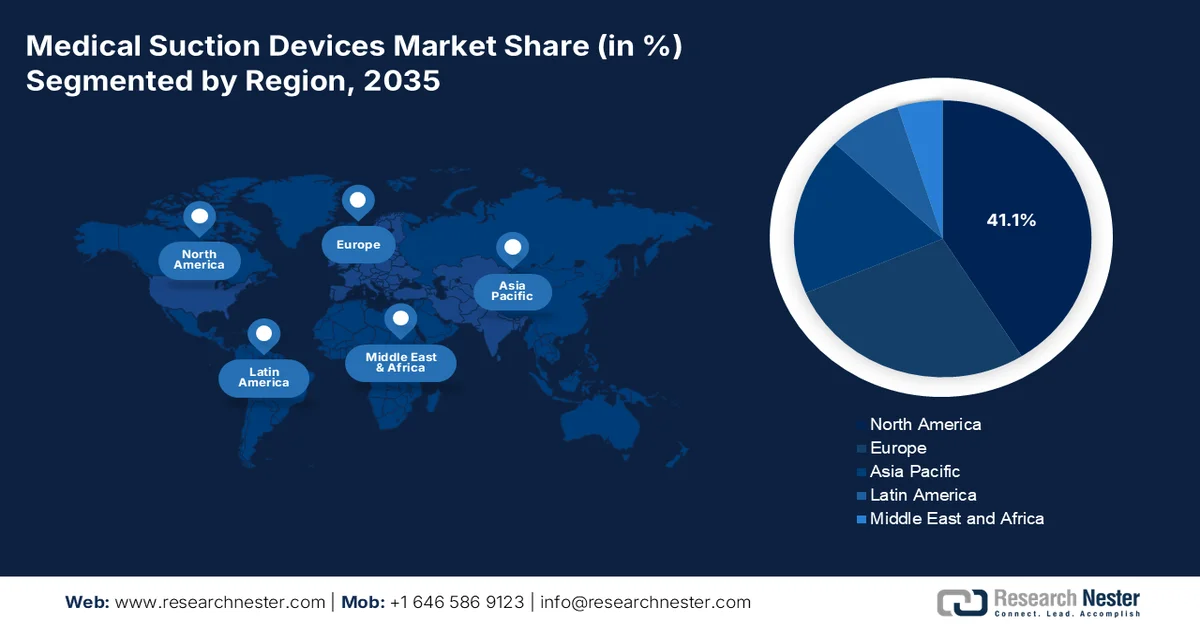

- North America is anticipated to dominate the medical suction devices market with a 41.1% share by 2035, reinforced by expanding surgical volumes, advanced healthcare infrastructure, supportive reimbursement policies, and rising adoption of portable suction technologies

- Asia Pacific is projected to emerge as the fastest-growing region throughout 2026-2035, spurred by healthcare modernization initiatives, increasing respiratory disease prevalence, growing surgical procedures, and accelerating transition toward portable devices

Segment Insights:

- The non-portable segment is forecast to capture 67.3% of the medical suction devices market by 2035, propelled by the growing requirement for uninterrupted high-volume vacuum power across intensive care units, operating rooms, and emergency departments

- The airway clearing sub-segment is expected to secure the second-largest share in the market during the forecast period, impelled by rising demand for effective airway obstruction management and anti-choking medical devices

Key Growth Trends:

- Rise in hospital-acquired pneumonia

- Expansion in dental surgeries

Major Challenges:

- Supply chain vulnerabilities for critical components

- Limited clinical awareness and training in low-resource settings

Key Players: Medela AG (Switzerland), ZOLL Medical Corporation (U.S.), Drive DeVilbiss Healthcare (U.S.), Olympus Corporation (Japan), Precision Medical, Inc. (U.S.), Laerdal Medical (Norway), Atmos Medizintechnik GmbH & Co. KG (Germany), Integra Biosciences (Switzerland), Ohio Medical (U.S.), SSCOR, Inc. (U.S.), Allied Healthcare Products (U.S.), Medicop (Switzerland), Penlon Ltd (UK), Mindray (China), Lepu Medical (China), CONMED Corporation (U.S.), BPL Medical Technologies (India), Mermaid Medical (Denmark), Besco Medical (Germany), Nouvag AG (Switzerland), Cook Medical (U.S.), Air Techniques, Inc. (U.S.), Karl Storz (Germany), LifeVac LLC (U.S.).

Global Medical Suction Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.6 billion

- 2026 Market Size: USD 1.7 billion

- Projected Market Size: USD 2.9 billion by 2035

- Growth Forecasts: 6.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (41.1% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: U.S., Germany, China, Japan, India

- Emerging Countries: India, China, South Korea, Brazil, Saudi Arabia

Last updated on : 29 May, 2026

Medical Suction Devices Market - Growth Drivers and Challenges

Growth Drivers

- Rise in hospital-acquired pneumonia: This type of infection, especially ventilator-based pneumonia, is considered a patient safety priority, which is enhancing the medical suction devices market demand globally. According to official statistics published by NLM in January 2024, hospital-acquired pneumonia (HAP) is recognized as an infection of the pulmonary parenchyma, appearing after almost 48 hours of hospital admission. Apart from this, ventilator-associated pneumonia (VAP) also occurs among patients, with its incidence rate ranging from 1 to 2.5 cases per 1,000 ventilator days in North America. Likewise, VAP accounts for 18 cases per 1,000 ventilator days across hospital facilities in Europe, thereby denoting an optimistic outlook for the market’s growth across different regions.

- Expansion in dental surgeries: There is a rise in dental implant surgery, highly propelled by the demand for cosmetic dentistry, aging population, and implant expenses, creating a specialized need for the medical suction devices market. As per an article published by NLM in July 2025, caries of deciduous teeth and permanent teeth impact an estimated 2.8 billion people globally. Besides, the Institute for Health Metrics and Evaluation (IHME) at the University of Washington recorded 371 such disease types as well as dental injuries from 204 territories and countries. However, in-depth research is ongoing to unveil targeted and suitable prevention approaches, which significantly caters to the medical suction devices market development in the upcoming years.

Challenges

- Supply chain vulnerabilities for critical components: Manufacturers in the medical suction devices market depend on a globalized supply chain for critical components, including miniature vacuum pumps, batteries, pressure sensors, and medical-grade plastics. The concentration of battery cell manufacturing in China, semiconductor fabrication in Taiwan and South Korea, and specialized pump components in Germany creates single points of failure. Disruptions, whether from geopolitical tensions, natural disasters, or pandemics, can halt production indefinitely. During the pandemic, manufacturers faced simultaneous shortages of electronic components and logistics bottlenecks for finished device shipping.

- Limited clinical awareness and training in low-resource settings: Healthcare workers across many low- and middle-income countries receive inadequate training on proper suction device selection, operation, and maintenance. Simple errors, such as using incorrect catheter sizes, failing to monitor vacuum pressure, or neglecting filter changes, compromise patient outcomes and damage equipment prematurely. The absence of standardized clinical protocols for suction use in specific procedures leads to inappropriate device application. Furthermore, biomedical engineering support for device maintenance is often unavailable outside major urban centers, resulting in non-functional equipment accumulating in storage rooms, which in turn, is negatively impacting the medical suction devices market.

Medical Suction Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.3% |

|

Base Year Market Size (2025) |

USD 1.6 billion |

|

Forecast Year Market Size (2035) |

USD 2.9 billion |

|

Regional Scope |

|

Medical Suction Devices Market Segmentation:

Portability Segment Analysis

Based on portability, the non-portable segment is anticipated to record the highest share of 67.3% in the medical suction devices market by the end of 2035. The segment’s upliftment is primarily attributed to its crucial role as the gold standard for high-acuity medical care services. This particular segment comprises wall-mounted and central station-based suction systems, that remains the clinical backbone of acute care infrastructure. These devices are permanently integrated into hospital gas supply networks or mounted directly onto patient headwalls in intensive care units, operating rooms, and emergency departments. Their sustained dominance is driven by the critical care requirement for uninterrupted, high-volume vacuum power. Unlike portable units, non-portable systems draw directly from central building utilities, eliminating battery life concerns during prolonged surgical procedures or multi-day ICU stays.

Application Segment Analysis

During the forecast period, the airway clearing sub-segment, part of the application segment, is projected to grab the second-highest share in the medical suction devices market. The sub-segment’s growth is effectively fueled by its importance as medical tools for removing blood, vomit, mucus, or foreign objects from a patient’s respiratory tract. According to official statistics published by the International Emergency Nursing in March 2025, in terms of airway obstruction, more than 5,000 choking-based deaths have been reported every year, particularly in the U.S., while almost 400 deaths have occurred in Wales and England. Therefore, to combat these incidents, there is a huge demand for anti-choking devices. In this regard, the success rate of these devices usually ranges from 71% to 99%, thereby denoting an optimistic outlook for the sub-segment’s growth.

End use Segment Analysis

The hospitals sub-segment, which is part of the end use segment, is expected to account for the third-highest share in the medical suction devices market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by the aspect of representing the most mature and high-volume end-use segment for medical suction devices, encompassing intensive care units, general surgical suites, emergency rooms, post-anesthesia care units, and specialized departments such as neurosurgery and ear, nose, and throat. The concentration of critically ill patients requiring invasive airway management, including those on mechanical ventilation, creates a baseline demand that exceeds all other care settings combined. Moreover, hospitals prioritize device interoperability with existing central gas systems, regulatory compliance with stringent local and international safety standards, and bulk procurement contracts that standardize equipment across different beds.

Our in-depth analysis of the medical suction devices market includes the following segments:

|

Segment |

Subsegments |

|

Portability |

|

|

Application |

|

|

End use |

|

|

Type |

|

|

Technology/Suction System |

|

|

Component/Suction Parts |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Medical Suction Devices Market - Regional Analysis

North America Market Insights

North America in the medical suction devices market is anticipated to account for the largest share of 41.1% by the end of 2035. The market’s upliftment in the region is primarily attributed to the existence of medical and health infrastructure, an increase in surgical volumes, suitable reimbursement policies, the aging population, technological shifts toward battery-powdered and portable devices, and regulatory support from the government. According to official statistics published by the MedPAC Government in March 2025, the volume of ambulatory surgical center (ASC)-based surgical procedures per fee-for-service (FFS) beneficiary surged by 5.7% as of 2023, in comparison to a yearly average rate of 0.6% from 2022. In addition, almost 6,300 ASCs aided 3.4 million FFS Medicare beneficiaries, and this program spending on these surgical services amounted to nearly USD 6.8 billion, thus proliferating the market’s growth in the region.

Average Yearly Change in Regional ASCs, 2018-2023

|

Year |

Total Number of ASCs |

New |

Closed/Merged |

|

2018 |

5,650 |

226 |

136 |

|

2022 |

6,153 |

221 |

93 |

|

2023 |

6,308 |

250 |

95 |

|

2018-2022 (% Change) |

2.2 |

- |

- |

Source: MedPAC Government

The medical suction devices market is growing significantly in the U.S., owing to the presence of stringent Medicare coverage criteria, along with compliance burden impacting device suppliers, the differentiation between NPWT and suction pumps, and the provision of healing benefits. As stated in an article published by the Centers for Medicare and Medicaid Services in November 2025, the Medicare Part A inpatient-based hospital deductible amounts to USD 1,736 as of 2026, demonstrating a surge of USD 60 from USD 1,676 in 2025. Additionally, this particular deductible covers beneficiaries’ share of expenses for the first 60 days of Medicare-specific inpatient hospital care. Moreover, beneficiaries are required to pay USD 484 per day as a coinsurance amount for the 61st and 90th day of hospitalization, indicating an increase from USD 419 in 2025, thus enhancing the medical suction devices market upliftment in the country.

The existence of provincial health systems, generous investments by the government for increasing the spending on suction-based treatments, a rise in chronic respiratory diseases, an upsurge in the aging population, the presence of a unified national coding framework, and growth in home healthcare services are certain factors that are bolstering the medical suction devices market in Canada. As per a data report published by the House of Commons in July 2024, the estimated yearly payer’s pricing of aiding chronic obstructive pulmonary disease (COPD) on the domestic healthcare system is projected to rise to USD 9.4 billion by the end of 2030. Based on this, asthma is considered the leading cause of emergency hospital visits for the population. In addition, the direct expenses of this disease to the country’s economy, including indirect and direct healthcare expenses, are expected to surge to USD 4.2 billion every year by the same year, thereby enhancing the medical suction devices market growth.

APAC Market Insights

The Asia Pacific in the medical suction devices market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by an expansion in healthcare advancements, a rise in surgeries, an increase in the prevalence of rare respiratory conditions, government-based health modernization strategies, especially in India and China, and the shift to portable devices. According to official statistics published by the IHME Organization in January 2026, the age -standardized prevalence of chronic disease was highest in South Asia, accounting for 3,044.1 per 100,000 population, and meanwhile, the asthma prevalence was highest across high-income locations, constituting 4,870.2 per 100,000 population. In addition, Southeast Asia catered to a higher age-standardized DALY rate of 508.6 per 100,000, in comparison to the overall region with a 204.4 rate per 100,000 population, thus ensuring an increase in the market demand.

The medical suction devices market is gaining increased traction in China, owing to massive investments in the health industry, the existence of the largest patient population, the availability of advanced suction devices, the Healthy China 2030 plan, and contributions initiated by domestic manufacturers. As stated in an article published by NLM in December 2025, the country’s population aged more than 60 years effectively reached 280 million as of 2023, which represented over 19% of the total population. Simultaneously, there has been a rise in chronic disease prevalence, accounting for over 80% of the domestic disease burden. Based on this, the floating population surpassed 240 million, experiencing severe health risks, while an estimated 85 million of the population with disabilities demanded enhanced health and medical services, thereby denoting a huge growth opportunity for the medical suction devices market in the country.

The aspects of quality standards, an increase in the adoption of automated surgical systems, strict regulatory oversight, generous funding for medical device advancement, research adjustment investments, aging demographics, and the availability of fluid management systems are a few trends that are responsible for fueling the medical suction devices market in Japan. As per an article published by the ITA in November 2025, the country’s Ministry of Health, Labour and Welfare (MHLW) demonstrated that the economy for the medical device industry as of 2024 was worth USD 32 billion. In addition, the industry is predicted to exhibit a yearly growth rate of 4.4% by the end of 2029. Moreover, the shipment facility of different medical instruments and appliances from the country to other regions are highly responsible for boosting the market.

2024 Medical Instruments and Appliances Export from Japan

|

Countries |

Trade Value (USD 1,000) |

Quantity |

|

Global |

1,452,054.1 |

1,404,840,000 |

|

U.S. |

495,828.0 |

89,515,800 |

|

China |

258,081.1 |

95,530,000 |

|

Germany |

173,450.5 |

115,696,000 |

|

Belgium |

50,974.0 |

380,862,000 |

|

Korea Republic |

49,652.6 |

6,388,180 |

|

Vietnam |

37,551.4 |

162,806,000 |

|

India |

32,942.6 |

14,751,300 |

|

Other Asia |

32,879.3 |

3,101,570 |

|

Thailand |

23,175.4 |

45,284,200 |

Source: World Integrated Trade Solution

Europe Market Insights

Europe in the medical suction devices market is projected to witness a considerable share by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by regulatory oversight under the regional Medical Device Regulation (MDR), followed by a transition to minimally invasive surgical techniques, centralized healthcare planning, and an increase in infection control protocolization. According to official statistics published by NLM in October 2024, the in-vitro diagnostic medical device (IVD) industry in the region readily employs almost 75,000 and generates approximately USD 12.8 billion in yearly revenue. Moreover, there are an estimated 40,000 IVDs in the regional economy, which effectively contribute to diminished yearly healthcare expenses by ensuring precise and efficient medical treatments to patients after diagnosis, thus enhancing the market expansion in the overall region.

The medical suction devices market is gaining increased exposure in Germany, owing to modernization in healthcare facilities, regulatory efficiency, surgical volume leadership, the Digital OP 2030 strategy, and rapid approvals for advanced suction consoles. As stated in an article published by the ITA in August 2025, the healthcare industry in the country significantly generates USD 838 billion or approximately 12.8% of the gross domestic product (GDP). Besides, with USD 172 billion readily generated through international sales, the industry contributed 8.1% of the country’s overall exports as of 2023, while imports amounted to USD 188.5 million. Moreover, 50% of physicians are aged more than 50 years, with a continuous rise in the need for nursing professionals. Based on this, predictions indicate that an estimated 1.9 million nurses are poised to be required by the end of 2040, which is positively driving the market exposure.

The presence of centralized healthcare governance, the transition to home-based care, infection control prioritization, upgradation in digitalized operating rooms, the adoption of minimally invasive technology, and the escalated shift from reutilized to single-patient-use disposable devices are a few factors that are enhancing the medical suction devices market in France. As per an article published by NLM in February 2026, an overall 58,232 robotic-assisted procedures were recognized in a clinical study, which increased from 27,011 as of 2021 to 31,221 in 2022, demonstrating a 15.6% of minimally invasive procedures. In this regard, urology predominated 61% of procedures, which is followed by 17% in digestive, 15% in gynecologic, and 7% in thoracic surgery. Besides, the robotic penetration in the country successfully reached 54.9% in urology, thereby making it suitable for bolstering the market exposure.

Key Medical Suction Devices Market Players:

- Medela AG (Switzerland)

- ZOLL Medical Corporation (U.S.)

- Drive DeVilbiss Healthcare (U.S.)

- Olympus Corporation (Japan)

- Precision Medical, Inc. (U.S.)

- Laerdal Medical (Norway)

- Atmos Medizintechnik GmbH & Co. KG (Germany)

- Integra Biosciences (Switzerland)

- Ohio Medical (U.S.)

- SSCOR, Inc. (U.S.)

- Allied Healthcare Products (U.S.)

- Medicop (Switzerland)

- Penlon Ltd (UK)

- Mindray (China)

- Lepu Medical (China)

- CONMED Corporation (U.S.)

- BPL Medical Technologies (India)

- Mermaid Medical (Denmark)

- Besco Medical (Germany)

- Nouvag AG (Switzerland)

- Cook Medical (U.S.)

- Air Techniques, Inc. (U.S.)

- Karl Storz (Germany)

- LifeVac LLC (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Medela AG leveraged its deep expertise in aspiration and negative pressure technology to maintain a strong foothold in hospital surgical suction and post-operative care. The company continues to focus on quiet, efficient pump systems that align with modern patient-centric operating room environments.

- ZOLL Medical Corporation differentiates its suction portfolio by integrating compact, battery-powered devices specifically engineered for emergency medical services and in-hospital transport. Its strategic emphasis lies on rugged, reliable units that perform seamlessly alongside its defibrillator and ventilation systems.

- Drive DeVilbiss Healthcare concentrates heavily on the home healthcare channel, offering portable and user-friendly suction machines for chronic respiratory conditions. The company prioritizes durable, low-maintenance designs that cater to both patients and non-specialist caregivers.

- Olympus Corporation integrates suction functionality directly into its endoscopy and surgical visualization platforms, creating a seamless fluid management experience for minimally invasive procedures. This embedded approach reinforces customer loyalty by reducing setup complexity in the operating room.

- Precision Medical, Inc. focuses on developing compact, AC or DC-powered vacuum systems for acute care, transport, and emergency settings. The company’s strategy emphasizes modular designs that allow healthcare providers to easily swap batteries or power sources without interrupting patient care.

Here is a list of key players operating in the global medical suction devices market:

The global medical suction devices market is highly competitive, with top players focusing on product innovation, strategic expansions, and digital integration. Besides, Medela AG led the market with a suitable share in 2025, while the top five players collectively held the majority of the share. Key strategic initiatives include launching battery-powered portable devices for home healthcare, integrating IoT for remote monitoring, and expanding distribution networks in the emerging Asia Pacific economy. Moreover, in March 2026, Cook Medical commercially launched two products from its very own urology segment, including the Syfonix® Suction Ureteral Access Sheath and the 7.5 Fr Ascend™ Single-Use Flexible Ureteroscope. Both these products are readily available in the U.S. and Canada, thereby making it suitable for ensuring the medical suction devices industry expansion globally.

Corporate Landscape of the Medical Suction Devices Market:

Recent Developments

- In March 2026, Air Techniques, Inc. introduced its newest outstanding product, the SepaStar Amalgam Separator, at the Art and Science of Dentistry in Anaheim, which has successfully set a standard in amalgam separation technology.

- In March 2026, Karl Storz received the FDA approval for the FIVE S 6.5 sterile single-use bronchoscope, which has made it suitable for the device to provide a valuable new option for severe care intensivists, physicians, ICU-based proceduralists, and RTs.

- In March 2026, LifeVac LLC proclaimed that the FDA has effectively granted the De Novo classification for LifeVac under 21 CFR 874.5400, which formally established the device type suction anti-choking device as a second-line treatment.

- Report ID: 8590

- Published Date: May 29, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.