AI in Medical Devices Market Outlook:

AI In Medical Devices Market size was valued at USD 13.2 billion in 2025 and is projected to reach USD 123.4 billion by the end of 2035, rising at a CAGR of 28.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of AI in medical devices is assessed at USD 16.9 billion.

The global AI in medical devices market is all set to witness tremendous growth in the upcoming years, owing to the shift toward the integration of intelligent algorithms into routine clinical practice, transforming devices from passive monitoring tools into active decision-support systems. In this context, the article published by the Journal of Medical Internet Research in March 2026 revealed that AI-enabled medical devices are advancing personalized healthcare, whereas the AI healthcare industry is projected to exceed USD 187.9 billion by the conclusion of 2030, rising at a CAGR of 37% from 2022. The study was based on over 100 publications from seven years, reports diagnostic accuracies of up to 98.88% for disease classification and 95% for insulin injection site recognition, whereas more than 70% of clinical decisions rely on diagnostic tests. AI-driven automation is shown to reduce diagnostic delays by up to 50%, improving care efficiency and outcomes, thus denoting a huge growth opportunity for the artificial intelligence (AI) in medical devices market.

Furthermore, the visible trends elevating the growth potential of AI in medical devices market are the rapid proliferation of machine learning and computer vision across medical imaging, radiology, and cardiology, which are aiming for faster, more accurate, and standardized diagnostic results. As of the March 2025 data from the U.S. Food & Drug Administration (FDA), artificial intelligence and machine learning are remarkably influencing software as a medical device by enabling systems to learn from real-world use and improve diagnostic and treatment support. Besides, the FDA is proactively developing regulatory frameworks with a main goal to address the adaptive nature of AI and ML, including guidance on lifecycle management, transparency, and predetermined change control plans. Also, these consistent efforts from the governing body aim to balance innovation with patient safety, ensuring that AI-enabled devices are effective and trustworthy. Moreover, with the presence of initiatives such as the AI/ML SaMD Action Plan and recent draft guidances, the FDA is working to provide clarity while fostering innovation in this rapidly evolving field.

Recent FDA-Approved AI-Enabled Medical Devices (December 2025) with Companies, Panels, and Product Codes

|

Date of Final Decision |

Device |

Company |

Panel (Lead) |

Primary Product Code |

|

12/30/2025 |

TruSPECT Processing Station |

Spectrum Dynamics Medical, Ltd. |

Radiology |

QIH |

|

12/23/2025 |

AIR Recon DL |

GE Medical Systems, LLC |

Radiology |

LNH |

|

12/23/2025 |

ART-Plan+ (v3.1.0) |

Therapanacea Sas |

Radiology |

MUJ |

|

12/22/2025 |

PeekMed web |

Peek Health, S.A. |

Radiology |

QIH |

|

12/22/2025 |

SKOUT system |

Iterative Health |

Gastroenterology-Urology |

QNP |

|

12/22/2025 |

BioticsAI |

Bioticsai, Inc. |

Radiology |

IYN |

|

12/22/2025 |

Lumify Diagnostic Ultrasound System |

Philips Ultrasound, LLC |

Radiology |

IYN |

|

12/19/2025 |

Alzevita |

TOPIA MEDTECH LIMITED |

Radiology |

QIH |

|

12/19/2025 |

eMurmur Heart AI |

CSD Labs |

Cardiovascular |

DQD |

Source: U.S. FDA

Key AI in Medical Devices Market Insights Summary:

Regional Highlights:

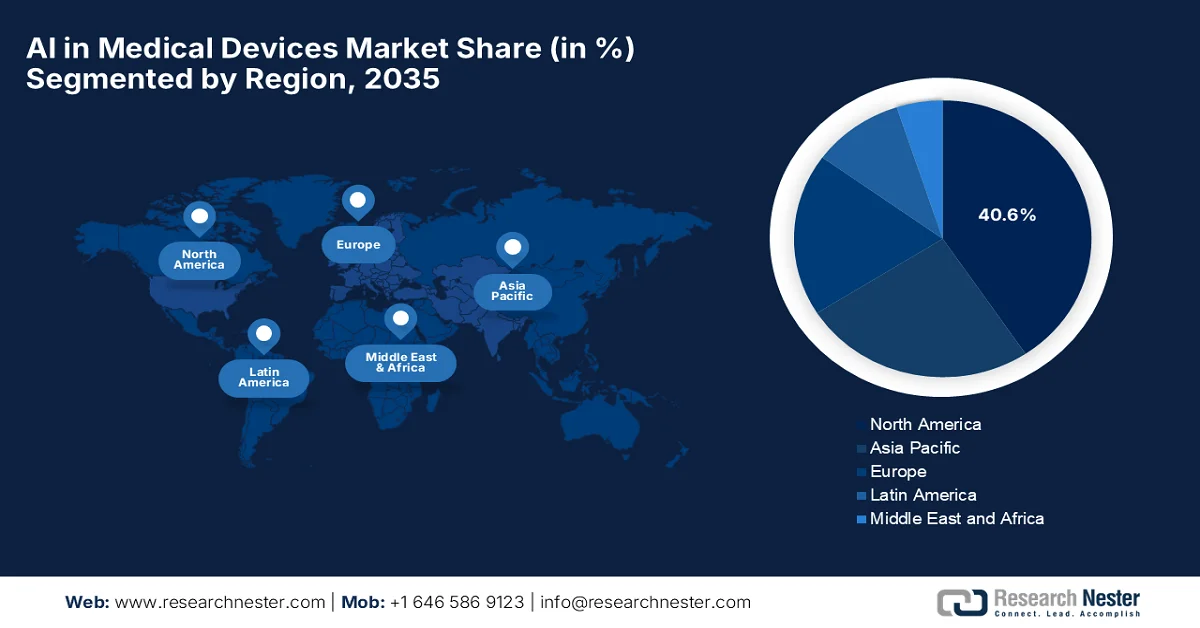

- North America is projected to dominate the ai in medical devices market with a 40.6% share by 2035, bolstered by strong regulatory support, early adoption of AI-enabled diagnostics, and advanced healthcare infrastructure.

- Asia Pacific is set to witness the fastest expansion in the forecast period 2026-2035, fueled by rapid healthcare infrastructure modernization and a growing aging population.

Segment Insights:

- In the ai in medical devices market, the software segment is expected to account for a 55.4% revenue share by 2035, propelled by continuous advancements delivered through software-as-a-medical-device platforms and regulatory-backed innovations.

- AI diagnostic imaging systems are likely to secure a considerable share by 2035, supported by the rising volume of imaging procedures alongside enhanced detection accuracy and reduced clinician workload.

Key Growth Trends:

- Personalized & precision medicine

- Expansion of remote monitoring & wearables

Major Challenges:

- Data quality, availability, and interoperability challenges

- Regulatory and compliance uncertainty

Key Players: Medtronic (U.S.), GE HealthCare (U.S.), Siemens Healthineers (Germany), Philips Healthcare (Netherlands), Johnson & Johnson MedTech (U.S.), Abbott Laboratories (U.S.), Boston Scientific (U.S.), Stryker Corporation (U.S.), Canon Medical Systems (Japan), Zimmer Biomet (U.S.), Aidoc (Israel), Digital Diagnostics Inc. (U.S.), TEMPUS (U.S.), Nvidia (U.S.), iRhythm Technologies (U.S.), Intuitive Surgical (U.S.), Qure.ai (India), Samsung Medison (South Korea), Sonio SAS (France), Samsung Medison (South Korea), Medow Health AI (Australia), Lords Mark Industries Ltd. (India), Healthcare AI group (Malaysia).

Global AI in Medical Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 13.2 billion

- 2026 Market Size: USD 16.9 billion

- Projected Market Size: USD 123.4 billion by 2035

- Growth Forecasts: 28.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 9 April, 2026

AI in Medical Devices Market - Growth Drivers and Challenges

Growth Drivers

- Personalized & precision medicine: AI enables suitable treatment planning and patient-specific treatment procedures by analyzing complex datasets, i.e., imaging, genomics, and EHRs. These align with the structural shift towards precision, which effectively fuels the demand for AI in the artificial intelligence in medical devices market. In December 2024, PGxAI announced the launch of Sirius, which is an advanced AI-powered pharmacogenetics model especially designed to personalize drug selection, dosage, and interaction management based on individual genomes. This particular Sirius covers 730 drugs and 40 genes, offering unprecedented precision in treatment guidance. Therefore, such instances denote that AI is enabling highly personalized and data-driven medical interventions, thereby driving the adoption of AI in medical devices by demonstrating tangible improvements in treatment efficacy.

- Expansion of remote monitoring & wearables: The growth of wearable sensors and connected health devices sometimes consists of AI capabilities that support patient monitoring, chronic care management outside hospitals, and telehealth expansion. This particular trend boosts the overall AI in medical devices market uptake, especially in terms of home and outpatient care settings. In this context, Invest India in April 2025 reported that remote monitoring in the country has showcased tremendous expansion due to the presence of telehealth platforms such as eSanjeevani, with almost 2,30,742 providers onboarded and over 340 million patients served since 2021. In addition, it also mentioned that leveraging AI-driven virtual healthcare, wearable devices, and connected sensors, remote patient monitoring enables health tracking and virtual consultations, thereby improving care for all age groups. Furthermore, the global RPM market is projected to reach a substantial value of USD 56.9 billion by the end of 2030 at a CAGR of 12.7%, highlighting strong investment potential.

- Healthcare digitalization & data availability: The continuous digitalization of health records, imaging systems, and clinical workflows generates huge amounts of datasets that AI can leverage, which enhances its analytical capabilities and demonstrates clearer clinical value. In November 2025, the Organization for Economic Co-operation and Development (OECD) disclosed that remote monitoring and digital health have readily advanced across OECD countries, mainly propelled by attributes such as telemedicine, EHRs, AI, and digital therapeutics. It also mentioned that by 2024, 82% of citizens had access to online digital health services, which is up from 79% in 2023, though full EHR functionality is only available in Belgium and Estonia. Teleconsultations doubled during the COVID-19 pandemic, stabilizing at 1.0 per patient in 2023, wherein Israel led this at 2.8 per patient, thus suitable for bolstering the overall AI in medical devices market’s growth.

Challenges

- Data quality, availability, and interoperability challenges: The absence of standardized healthcare data is a major obstacle that is hindering the upliftment of artificial intelligence in medical devices market. These AI-based systems are heavily dependent on large datasets for training and validation, but healthcare data is still fragmented across hospitals, stored in incompatible formats, and plagued by inconsistencies. Therefore, this data silos problem causes limitations in the scalability of AI-based devices, as inaccurate data in turn leads to flawed outputs and reduced clinical trust. Moreover, semantic inconsistencies across electronic health records again hinder AI’s ability to interpret information correctly. Influenced by the absence of proper data governance frameworks and standards, the full potential of AI-enabled medical devices will be constrained across healthcare ecosystems.

- Regulatory and compliance uncertainty: The regulatory ecosystem of AI in medical devices market is considered to be complex and evolving, which is creating uncertainty for manufacturers and healthcare providers. Besides, regulatory frameworks that were designed for static medical devices find it difficult to accommodate continuously learning AI systems. At the same time, issues such as algorithm updates, post-market surveillance, and re-certification requirements complicate compliance processes. The fragmented global regulations and continuously emerging policies, such as AI-specific legislation, cause ambiguity regarding approval pathways and liability. Therefore, companies need to navigate stringent requirements that are related to transparency, safety validation, and human oversight, making regulatory strategy a major obstacle to innovation and widespread adoption.

AI in Medical Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

28.2% |

|

Base Year Market Size (2025) |

USD 13.2 billion |

|

Forecast Year Market Size (2035) |

USD 123.4 billion |

|

Regional Scope |

|

AI in Medical Devices Market Segmentation:

Component Segment Analysis

In the component segment, software is anticipated to capture the largest revenue share of 55.4% in the artificial intelligence in medical devices market by the conclusion of the forecast period. The dominance of the segment is largely attributable to the use of advancements in medical devices, which are primarily delivered through software-as-a-medical-device platforms. In March 2026, Philips received the U.S. FDA clearance for DeviceGuide, which is an AI-powered solution integrated with EchoNavigator R5.0 to assist physicians during complex minimally invasive mitral valve repair procedures. It was developed in collaboration with Edwards Lifesciences, and the software combines live ultrasound and X-ray imaging to automatically track and visualize repair devices in real time, improving navigation and precision. Therefore, such continued innovations coupled with regulatory support are expected to bolster the segment’s growth and expansion.

Device Type Segment Analysis

By the end of 2035, the AI diagnostic imaging systems are expected to capture a considerable revenue share in the AI in medical devices market. The segment’s progression is largely attributable to the exponential growth in imaging procedures and strong regulatory support. At the same time, AI significantly improves detection accuracy and reduces clinician workload, driving widespread hospital adoption. In July 2025, GE HealthCare topped the U.S. FDA’s list with 100 authorizations, marking the fourth consecutive year of dominance. Its AI-based solutions, including AIR Recon DL for MRI image clarity, AI-based Auto Positioning for CT/PET scans, and LOGIQ Series ultrasound systems, enhance diagnostic precision, workflow efficiency, and patient outcomes. Hence, such instances indicate that the integration of AI in diagnostic imaging is becoming a major driver of efficiency and accuracy in healthcare. This trend is evidence for strong artificial intelligence (AI) in medical devices market growth potential and solidifies the strategic importance of regulatory alignment, technology adoption, and clinical validation for stakeholders in this sector.

Application Segment Analysis

The radiology which is under application is predicted to grow at a significant rate in the artificial intelligence in medical devices market during the stipulated timeframe. The segment’s growth is highly propelled by high data availability and clinical demand for faster diagnosis. AI efficiently enhances radiology workflows by enabling automated image interpretation, triage, and prioritization of critical cases, thus improving efficiency and patient outcomes. In this regard, a2z Radiology AI in November 2025 received the U.S. FDA clearance for a2z‑Unified‑Triage, which is the first multi‑condition triage system for abdomen‑pelvis CT scans. This particular solution can simultaneously flag seven urgent conditions, including small bowel obstruction, acute cholecystitis, and abdominal aortic aneurysm, helping radiologists prioritize critical cases faster. More than 20 million abdomen‑pelvis CT exams are performed annually in the U.S., whereas this innovation positions the segment at the forefront of revenue generation in this category.

Our in-depth analysis of the global artificial intelligence (AI) in medical devices market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Device Type |

|

|

Application |

|

|

Technology |

|

|

End user |

|

|

Functionality |

|

|

Deployment Mode |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

AI in Medical Devices Market - Regional Analysis

North America Market Insights

The North America AI in medical devices market is anticipated to garner the largest share of 40.6% by the end of the forecast period. The region’s dominance is highly propelled by strong regulatory support, early adoption of AI-enabled diagnostics, and advanced healthcare infrastructure. The region leads through continued innovations, a strong ecosystem of established medical technology giants and agile startups, which are focused on diagnostic accuracy and operational efficiency. In June 2025, IQVIA introduced new AI agents for life sciences and healthcare, which were developed in collaboration with NVIDIA to enhance workflows and accelerate insights. These agents leverage NVIDIA’s NIM Agent Blueprints, NeMo Customizer, and NeMo Guardrails to support tasks such as target identification, clinical data review, literature analysis, and HCP engagement, thus denoting a positive artificial intelligence (AI) in medical devices market outlook.

A sophisticated medical ecosystem and a large aging population that requires advanced diagnostic and monitoring tools are the main factors that are responsible for uplifting artificial intelligence in medical devices market in the U.S. The landscape is moving toward integrated ecosystems where software defines hardware, shifting traditional sales models into recurring value subscriptions that combine devices with paid analytics. In this context, the Congress Government in December 2024 reported that the adoption of AI in health care has remarkably accelerated, positively impacted by the increased availability of clinical data and advancements in machine learning, deep learning, and neural networks, enabling a very accurate analysis of medical records, imaging, and patient histories. It also mentioned that federal oversight has evolved along with these technologies, wherein the agencies are establishing standards for algorithm transparency and interoperability, hence suitable for standard market growth.

A strong emphasis on digital health integration within a publicly funded healthcare system is responsibly boosting the overall AI in medical devices market in Canada. The landscape is effectively reshaped by Health Canada’s modernization of regulatory frameworks, which allow for iterative algorithm updates without repeated license amendments. In April 2026, the IRPP Organization revealed that AI scribes are utilized in the country’s healthcare to reduce physicians’ documentation time by up to 90%, but they raise serious concerns around privacy, accuracy, and equity. Besides the trials of tools such as DAX Copilot show promise in efficiency, yet risks such as transcription errors, bias, and patient data misuse are unresolved. Therefore, there is an urgent need for stronger governance, explicit consent, and safeguards to ensure these technologies enhance care without any compromise on patient trust or safety.

APAC Market Insights

The Asia Pacific artificial intelligence in medical devices market is expected to grow at the quickest rate from 2026 to 2035. The region’s progress in this field is largely propelled by rapid healthcare infrastructure modernization and a massive, aging patient population. The landscape is transitioning from experimental pilots to integrated clinical ecosystems wherein the multimodal AI combines imaging, genomics, and real-time data from AI-powered wearables to enable predictive, preventive care. In February 2026, an NIH article revealed that a study in Japan analyzed healthcare providers’ perspectives on AI, whereas the focus group interviews with 37 doctors, nurses, and allied professionals examined applications in lung cancer detection, clinical note generation, and wearable monitoring devices. In this context, participants acknowledged AI’s complete potential to support clinical decision-making and reduce workload, but there were concerns about algorithmic accuracy, bias, over-reliance, and shifts in professional roles. In addition, the study highlights that human-centered design and adaptive governance are highly essential for an effective integration of AI in healthcare systems.

The China AI in medical devices market is solidifying its position in the region based on a unique combination of centralized health data, state-led strategic support, and an opportunistic domestic ecosystem. The sector is highly focused on lifecycle governance, cross-border data compliance, and the integration of AI into smart hospitals, with a main goal to bridge the specialist gap between urban centers and rural townships. In this context, NIH in March 2026 stated that its study on AI-based medical device approvals in China from 2020 to mid-2025 identified 154 devices, with annual approvals rising from 9 in 2020 to 45 in 2024, reflecting a 49.53% CAGR. It mentioned that most devices 79.9% were high-risk class III, which were using deep learning algorithms, and focused on radiology with CT-based applications for pulmonary and cardiovascular assessment. Clinical trials were the main evaluation pathway, particularly for class III devices, whereas the artificial intelligence (AI) in medical devices market was concentrated among a few manufacturers in major innovation hubs such as Beijing, Shanghai, Shenzhen, and Hangzhou.

Fueled by an urgent need to bridge healthcare accessibility gaps and the rising prevalence of chronic diseases, the artificial intelligence in medical devices market in India is expected to witness tremendous progress over the forecasted years. The sector is moving from a heavy reliance on imports toward becoming a global innovation hub, supported by government initiatives such as the Make in India campaign and production-linked incentive schemes that encourage local manufacturing. In March 2026, the Press Information Bureau (PIB) revealed that the country’s Ministry of Health and Family Welfare has launched the Secure AI in Health initiative and the Benchmarking Open Data Platform for Health AI, with a main goal to strengthen safe and evidence-based AI adoption in healthcare. SAHI provides national guidance for ethical and inclusive AI use, whereas BODH, developed with IIT Kanpur, enables structured testing and validation of AI tools before large-scale deployment. Furthermore, under the Medical Devices Rules, AI-enabled devices need to meet strict documentation, safety, and performance requirements for licensing as well as commercialization, thus denoting a positive artificial intelligence (AI) in medical devices market outlook.

Europe Market Insights

Europe AI in medical devices market is expected to witness noteworthy growth, which is facilitated by a strong emphasis on integrating high-tech solutions. The region has registered itself as a predominant leader in AI-driven diagnostics, particularly in oncology and cardiology, where machine learning algorithms enhance the precision of medical imaging and pathology. In this context, NIH in September 2024 revealed that the EU AI Act, which was approved in March 2024, formed a regulatory framework for AI systems, including AI and ML-enabled medical devices, classifying them as risky attributes and leading them to strict compliance requirements. This particular act applies extraterritorially to providers whose AI outputs are used in the region, thereby intersecting with existing regulations. In this context, providers need to implement an AI quality management system, maintain detailed technical documentation, and conduct post-market monitoring, with the option to integrate AI documentation into the medical device technical file, thus allowing safe and effective products to the market.

The Germany AI in medical devices market has registered itself as a powerhouse characterized by its integration within a mature, research-heavy industrial landscape and a robust public healthcare system. Technological advancements are particularly prominent in AI-enabled diagnostic imaging, robotic-assisted surgery, and the rapidly expanding field of DiGAs, i.e., reimbursable digital health applications. As of the November 2025 data from the Federal Ministry of Health, it emphasizes that advancing digitalisation is highly essential for modernising Germany’s healthcare system, improving care quality, and enabling patient-centred treatment. Besides, the key initiatives include the expansion of secure telematics infrastructure, implementation of electronic patient records, e-prescriptions, digital health applications, and telemedicine services. At the same time, legislative frameworks such as the Digital Act and Health Data Use Act deliberately support data-driven innovation and research, whereas the Health Data Lab and interoperability platforms strengthen the infrastructure for AI and digital medical solutions.

The government and health system bodies that are actively shaping both regulation and adoption of AI‑enabled medical technologies are reorganizing the growth dynamics of AI in medical devices market in the UK. The country’s regulatory landscape is evolving towards a light-touch approach by prioritizing ethical, secure, and robust AI solutions. Based on the government data published in February 2025, the MHRA’s Software Group looks into the regulation of software and AI as medical devices (SaMD and AIaMD) in the UK, ensuring safety, clinical effectiveness, and public access at the same time, guiding classification, qualification, and vigilance. Their change programme addresses pre- and post-market requirements, adaptive AI regulation, transparency, and international alignment with the FDA as well as Health Canada standards. Furthermore, the group also supports digital mental health technologies, collaborates with academic and healthcare partners, promotes good machine learning practices, and regulatory innovation, thus suitable for standard AI in medical devices market growth.

Key AI in Medical Devices Market Players:

- Medtronic (U.S.)

- GE HealthCare (U.S.)

- Siemens Healthineers (Germany)

- Philips Healthcare (Netherlands)

- Johnson & Johnson MedTech (U.S.)

- Abbott Laboratories (U.S.)

- Boston Scientific (U.S.)

- Stryker Corporation (U.S.)

- Canon Medical Systems (Japan)

- Zimmer Biomet (U.S.)

- Aidoc (Israel)

- Digital Diagnostics Inc. (U.S.)

- TEMPUS (U.S.)

- Nvidia (U.S.)

- iRhythm Technologies (U.S.)

- Intuitive Surgical (U.S.)

- Qure.ai (India)

- Samsung Medison (South Korea)

- Sonio SAS (France)

- Samsung Medison (South Korea)

- Medow Health AI (Australia)

- Lords Mark Industries Ltd. (India)

- Healthcare AI group (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Medtronic is one of the world’s leading medical technology companies, which is driving AI integration across its broad device portfolio, including surgical robotics, cardiac rhythm management, and diabetes care. The company also embeds AI‑based analytics into its monitoring and decision‑support systems with a main goal to improve clinical accuracy and patient outcomes.

- GE HealthCare is highly focused on embedding advanced AI into diagnostic imaging and clinical workflows through its Edison digital platform, which supports machine learning for image enhancement and decision‑support tools. Besides, the firm’s solutions span MRI, CT, ultrasound, and X‑ray systems, which allow it to maintain a strong position in this field.

- Siemens Healthineers holds a leadership position in AI‑enabled imaging and diagnostics, which is combining deep learning and predictive analytics into its scanner hardware and digital platforms such as AI‑Rad Companion. In addition, the company’s investments in molecular diagnostics and digital twins strengthen its ability to offer AI‑augmented clinical workflows.

- Philips Healthcare is yet another prominent player in this sector, and it applies AI to imaging systems, patient monitoring, and digital pathology with a main goal to deliver smarter diagnostics and more efficient care pathways. The company emphasizes adaptive intelligence that augments clinicians' decision-making with pattern recognition as well as predictive analytics.

- Johnson & Johnson MedTech maintains a strong position in this field, and it leverages AI with the main goal of enhancing surgical robotics, digital surgery analytics, and advanced visualization systems. The company adopts a strategic approach to collaborations with technology partners such as NVIDIA, aiming to scale AI deployment in the operating room, thus improving surgical precision and decision support.

Below is the list of some prominent players operating in the global artificial intelligence (AI) in medical devices market:

The global AI in medical devices market is identified as a moderately fragmented landscape, which is being dominated by legacy MedTech giants such as Medtronic, GE HealthCare, Siemens Healthineers, and Philips Healthcare. These pioneers readily combine advanced machine learning into imaging, diagnostics, and robotic systems to enhance clinical accuracy and workflow efficiency. Partnerships, strategic acquisitions, and regulatory clearances bolster product portfolios, whereas specialized innovators such as Aidoc, Digital Diagnostics Inc., and Qure.ai are focused on driving niche AI diagnostics and workflow automation. In May 2024, Samsung Medison announced the acquisition of Sonio SAS, which is a France-based fetal ultrasound AI software company, to strengthen its position in advanced medical devices. This particular partnership aims to deliver AI-enhanced workflows, improve maternal health outcomes, and expand access to advanced diagnostic technology across the globe.

Corporate Landscape of the AI in Medical Devices Market:

Recent Developments

- In November 2025, Philips introduced the DeviceGuide, which is an AI-powered solution designed to assist doctors during minimally invasive heart valve repair. It was built on the EchoNavigator platform, and it uses AI to track and visualize repair devices inside the beating heart, offering real-time 3D navigation support.

- In May 2025, NVIDIA and GE HealthCare entered into a partnership to develop autonomous diagnostic imaging systems using the new Isaac for Healthcare simulation platform. This particular technology leverages physics-based digital twins and pretrained AI models to train and validate robotic imaging capabilities in virtual environments before real-world deployment.

- Report ID: 2944

- Published Date: Apr 09, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.