Connected Medical Devices Market Outlook:

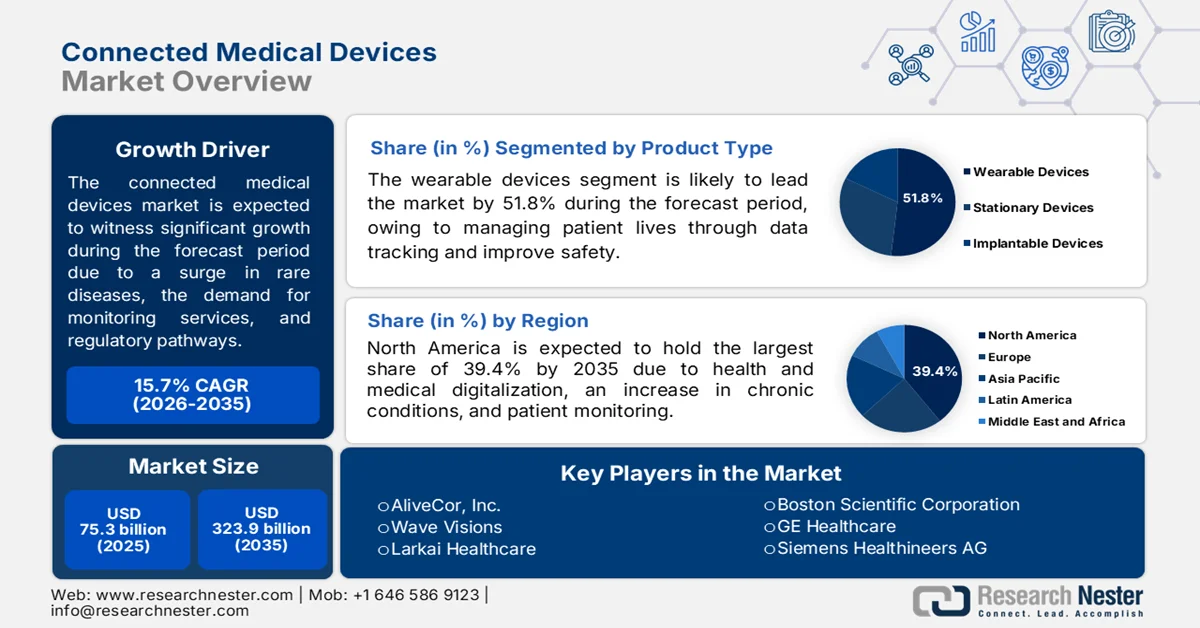

Connected Medical Devices Market size was valued at USD 75.3 billion in 2025 and is anticipated to reach USD 323.9 billion by the end of 2035, expanding at around 15.7% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of connected medical devices is estimated at USD 87.2 billion.

The worldwide connected medical devices market is undergoing a fundamental transformation, along with denoting an increase in non-communicable diseases, the sustained demand for continuous monitoring solutions, the availability of wireless modules and sensors, and suitable regulatory pathways. According to an article published by NLM in December 2025, non-communicable diseases significantly accounted for 12.4 billion incidences, which is equivalent to 156,680.6 per 100,000 population, along with 43.8 million deaths, and 1.7 billion disability-adjusted life years. In this regard, cardiovascular diseases accounted for 19.4 million deaths, which is followed by 9.9 million deaths due to neoplasms, 4.4 million deaths due to chronic respiratory diseases, and 1.7 million deaths due to diabetes mellitus, thus bolstering the market’s growth and demand globally.

Furthermore, the shift to value-added services and device-as-a-service models, along with the human-in-the-loop regulatory imperative, and the decoupling of intelligence and hardware through software as a medical device, are certain trends that are responsible for enhancing the connected medical devices market globally. As stated in the October 2025 Food and Drug Administration (FDA) Government article, the yearly establishment registration fee for medical devices amounts to USD 11,423. In addition, the FDA is effectively responsible for granting a waiver of this annual registration fee to certain small-scale businesses. These businesses are readily qualified through the Small Business Determination (SBD) Program, demonstrating the aspect of paying fees to overcome financial risks, thus making it suitable for making medical devices easily available.

Medical Devices Annual Registration Fee for Global Establishments, 2026

|

Application Type |

Standard Fee Structure (USD) |

Small-Scale Business Fee Structure (USD) |

|

510(k)‡ |

26,067 |

6,517 |

|

513(g) |

7,820 |

3,910 |

|

PMA, PDP, PMR, BLA |

579,272 |

144,818 |

|

De Novo Classification Request |

173,782 |

43,446 |

|

Panel-track Supplement |

463,418 |

115,855 |

|

180-Day Supplement |

86,891 |

21,723 |

|

Real-Time Supplement |

40,549 |

10,137 |

|

BLA Efficacy Supplement |

579,272 |

144,818 |

|

30-Day Notice |

9,268 |

4,634 |

|

Annual Fee for Periodic Reporting on a Class III device (PMAs, PDPs, and PMRs) |

20,275 |

5,069 |

Source: FDA Government

Key Connected Medical Devices Market Insights Summary:

Regional Highlights:

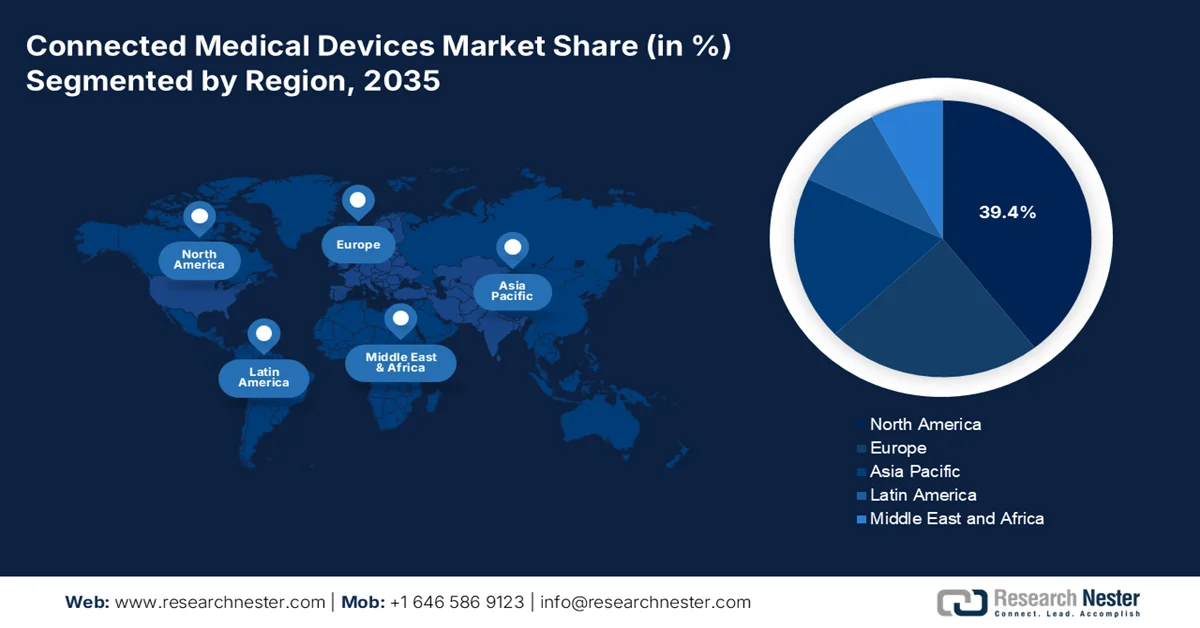

- Connected medical devices market North America is anticipated to account for 39.4% market share by 2035, bolstered by robust investments in healthcare digitalization, expanding telemedicine integration, advanced healthcare infrastructure, rising chronic disease prevalence, and growing demand for patient monitoring

- Asia Pacific is poised to be the fastest-growing regional market throughout 2026-2035, propelled by rapid digital health adoption, government-backed healthcare infrastructure initiatives, increasing chronic disease burden, expansion of wireless healthcare, and rising penetration of wearable technologies

Segment Insights:

- Connected medical devices market the wearable devices segment is projected to capture 51.8% market share by 2035, supported by increasing adoption of personalized health monitoring solutions for continuous data tracking, improved patient safety, and enhanced productivity

- The Hospitals and Clinics sub-segment is expected to hold 48.1% market share by 2035, benefiting from its central role in deploying connected medical devices for real-time patient monitoring, streamlined diagnostics, enhanced surgical precision, and continuous clinical data collection

Key Growth Trends:

- Rise in the telemedicine adoption

- AI-powered platforms for predictive analytics

Major Challenges:

- Interoperability and integration issues

- Regulatory and compliance barriers

Key Players: Medtronic PLC (Ireland/U.S.), Abbott Laboratories, Inc. (U.S.), Boston Scientific Corporation (U.S.), GE Healthcare (U.S.), Siemens Healthineers AG (Germany), Koninklijke Philips NV (Netherlands), AliveCor, Inc. (U.S.), Wave Visions (India), Larkai Healthcare (India), Jamnaa Healthtech (India), ResMed (U.S.), Baxter International Inc. (U.S.), Aptar Digital Health (U.S.).

Global Connected Medical Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 75.3 billion

- 2026 Market Size: USD 87.2 billion

- Projected Market Size: USD 323.9 billion by 2035

- Growth Forecasts: 15.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (39.4% share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Brazil, Saudi Arabia

Last updated on : 1 July, 2026

Connected Medical Devices Market - Growth Drivers and Challenges

Growth Drivers

- Rise in the telemedicine adoption: An increase in telemedicine services has successfully created a network effect, which is driving the demand for the connected medical devices market globally. According to an article published by NLM in February 2025, the teleconsultation pilot program, especially in South Korea, comprised 1,232 patients. Based on suitable analysis, this program led to lower payers’ pricing consultation for chronic diseases, amounting to USD 7.9, followed by USD 27.3 for dementia care, and USD 9.6 for rehabilitation. Therefore, these particular savings were eventually attributed to a decrease in productivity loss and transportation costs. In addition, this analysis recognized a transition in financial burden from caregivers and patients to public and government expenditures, thus enhancing the market exposure.

- AI-powered platforms for predictive analytics: The majority of worldwide organizations are continuously developing innovative AI-based platforms for adapting individual preferences and behaviors. As per the June 2026 IBEF Organization article, the medical technology sector is expected to reach shipment exports of almost USD 20 billion by the end of 2030, with the largest footprint in the UK’s USD 18.1 million medtech sector. Based on this, in February 2024, UK-based company, Feedback PLC, expanded in India by granting the import license for Bleepa as a registered medical device. In addition, USD 369,960 (£300k) was allocated by the NHS England central fund for Bleepa pilots for delivering different clinical pathways to consumers, thereby denoting a positive outlook for the market’s upliftment.

Challenges

- Interoperability and integration issues: The market suffers from a fragmented landscape where products from different manufacturers often operate on proprietary platforms and communication protocols. This lack of standardization hinders seamless data exchange between devices, electronic health records, and hospital information systems. Clinicians are frequently forced to manually reconcile data from multiple sources, negating the efficiency gains that connectivity promises. Integration challenges are particularly pronounced in large hospital networks that deploy devices from dozens of vendors, each with its own data format, interface, and update schedule.

- Regulatory and compliance barriers: The market operates at the intersection of healthcare, technology, and telecommunications, subjecting them to a complex web of regulatory requirements that vary significantly across geographies. Manufacturers must navigate rigorous approval processes from authorities such as the FDA in the U.S. and the EMA in Europe, often requiring extensive clinical trials and documentation before market entry. The software-driven nature of these devices further complicates matters, as frequent updates and patches intended to enhance functionality or address security vulnerabilities often trigger re-evaluation or re-certification under existing regulations. Moreover, the convergence of medical device regulations with data protection laws and telecommunications standards creates overlapping compliance burdens that are both time-consuming and resource-intensive.

Connected Medical Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

15.7% |

|

Base Year Market Size (2025) |

USD 75.3 billion |

|

Forecast Year Market Size (2035) |

USD 323.9 billion |

|

Regional Scope |

|

Connected Medical Devices Market Segmentation:

Product Type Segment Analysis

Based on the product type, the wearable devices segment is anticipated to capture the largest share of 51.8% in the connected medical devices market by the end of 2035. The segment’s upliftment is primarily attributed to crucial tools for transforming patients’ lives by offering personalized and rapid data to ensure data tracking, safety improvement, and bolster regular productivity. According to an article published by NLM in February 2025, a clinical study was conducted on 5,591 U.S. adults to examine and evaluate wearable device utilization and their willingness to share data with healthcare professionals. The study denoted a surge in the wearable device adoption by 36.3% as of 2022, indicating an increase from 28% to 30% in the past years. Besides, 78.4% of adults utilizing such devices were willing to share data with medical providers, thus positively impacting the segment’s growth.

End user Segment Analysis

During the forecast period, the hospitals and clinics sub-segment under the end user segment is projected to grab the second-largest share of 48.1% in the market. The sub-segment’s growth is effectively driven by its role as the cornerstone of the connected medical devices ecosystem, serving as the primary end-users where these technologies are deployed at scale. Within this particular clinical environment, connected devices are seamlessly integrated into daily workflows, enabling real-time patient monitoring, streamlining diagnostic processes, and enhancing surgical precision. Besides, from intensive care units to outpatient departments, these devices facilitate continuous data capture, permitting healthcare providers to make rapid and informed clinical decisions while reducing manual documentation burdens.

Application Segment Analysis

The remote patient monitoring sub-segment, which is part of the application segment, is expected to account for the third-largest share of 46.9% in the market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by the utilization of digital devices for sending patient health data, such as heart rate and blood pressure, directly to doctors. According to an article published by JMIR Publications in May 2024, the U.S. Centers for Disease Control reported that 51.8% of adults in the U.S. are affected by almost 1 chronic condition, while 27.2% are impacted by different chronic conditions, such as cardiovascular disease, diabetes, and obesity. Therefore, it is essential to collect an optimal combination of metrics for patients, based on which there is a huge growth and demand for remote patient monitoring.

Our in-depth analysis of the connected medical devices includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

End user |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Connected Medical Devices Market - Regional Analysis

North America Market Insights

The North America connected medical devices market is anticipated to garner the largest share of 39.4% by the end of 2035. The market’s upliftment in the region is primarily driven by robust investments for digitalization in health and medical, an increase in the integration of telemedicine services, innovative healthcare infrastructure, a surge in chronic conditions, and the demand for patient monitoring. According to an article published by the Rural Health Information Hub in April 2026, 22% of small rural areas and 19.8% of the large-scale rural area population are aged more than 65 years, in comparison to 17.2% of the total national population. Besides, health risks experienced by this age category of people in these areas include diabetes, Alzheimer’s disease, chronic cases, and associated dementia. Moreover, preventable premature deaths due to certain conditions are also enhancing the market demand in the overall region.

Preventable Premature Deaths Analysis in North America Rural Areas, 2022

|

Rural Area Types |

Heart Disease |

Cancer |

Chronic Lower Respiratory Disease |

Stroke |

|

Noncore |

49.4% |

18.1% |

54.8% |

40.9% |

|

Micro-politan |

45.8% |

14.0% |

50.7% |

42.0% |

|

Small Metro |

39.5% |

6.4% |

42.1% |

36.3% |

|

Medium Metro |

33.7% |

2.8% |

29.9% |

35.7% |

|

Large Fringe Metro |

22.0% |

- |

6.5% |

26.1% |

|

Large Central Metro |

30.1% |

- |

- |

32.8% |

Source: Rural Health Information Hub

The U.S. connected medical devices market is growing significantly, owing to government funding, Medicaid allocation, Medicare expenditure, the demand for Internet of Things IoT devices, a focus on health interoperability, and a rise in the need for remote patient monitoring. As per a report published by the Medicaid in March 2026, a total of 74,294,361 people were significantly enrolled in the Medicaid and CHIP enrollment program across 50 states in the country. Additionally, of the total enrollment, 67,080,865 were enrolled in Medicaid, along with 7,213,496 in CHIP. Besides, an overall 35,572,626 people were readily part of the CHIP, demonstrating 47.9% of the total program enrollment. Therefore, with the presence of such insurance programs, the total population of the country has access to standard health and medical solutions, thus fueling the market’s upliftment.

State-Wise Medicaid and CHIP Enrollment in the U.S., 2026

|

State |

Medicaid |

CHIP |

|

Washington |

1,720,278 |

66,336 |

|

Oregon |

1,101,912 |

182,349 |

|

California |

10,715,787 |

1,245,606 |

|

Nevada |

678,484 |

46,879 |

|

Idaho |

295,300 |

19,785 |

|

Montana |

187,610 |

20,037 |

|

Wyoming |

55,909 |

6,152 |

|

Utah |

291,584 |

34,610 |

|

Arizona |

1,529,649 |

110,570 |

|

New Mexico |

635,269 |

44,111 |

Source: Medicaid

The provincial and federal cooperation, the existence of digital health frameworks, an expansion in telehealth services, an increase in the adoption of wearable devices for chronic condition management, and the significant integration of AI-based analytics are certain factors that are responsible for bolstering the connected medical devices market in Canada. As stated in an article published by the Government of Canada in March 2022, based on a poll-based survey, an estimated half of the country’s population, or 47%, has been utilizing virtual care services since the pandemic, based on which 91% were readily satisfied. Besides, in yet another survey conducted by the Canada Health Infoway, 10% to 20% of the population utilized virtual care solutions. Meanwhile, territorial and provincial efforts to enhance accessibility to virtual care led to a significant boost in virtual visits, with nearly 60% of visits categorized as texting or mailing, videoconferencing, and telephonic, thus driving the market’s growth.

APAC Market Insights

The Asia Pacific market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly attributed to the rapid adoption of digital health, government-based infrastructure strategies, a rise in chronic disease burden, growth in the wireless healthcare sector, and the increased penetration of wearable technologies. According to an article published by Intelligent Pharmacy in October 2025, the digital healthcare industry, particularly in India, is continuously transforming, highly fueled by tactical government initiatives and technological innovations. In addition, the industry was significantly valued at roughly USD 1.5 billion and is further predicted to account for an estimated 25% in the upcoming 5 years, thereby making it extremely suitable for driving the market’s expansion in the overall region.

The China connected medical devices market is gaining increased traction, owing to an expansion in medical devices, the presence of administrative organizations for increased approvals, standard regulatory policies, and the promotion of high-quality industry development, with a focus on high-end imaging equipment, biomaterial devices, medical robots, and AI medical devices. As stated in an article published by NLM in March 2026, a clinical study was conducted to identify 154 AI-based medical devices (AIMDs). The study indicated an increase in yearly device approvals from 9 to 45 as of 2024, recording a 49.5% annual growth rate. In addition, 20 medical devices were approved in 2025, which deliberately suggested a potential moderation in the pace. Besides, 79.9% of the overall devices were readily categorized as class III devices, thus positively driving the market’s development.

The aspects of the standard health insurance system, generous fund allocation for software-based medical devices, regulatory consulting services, reimbursement policies for medical devices, cost-effective assessment, and healthcare expenditure are a few trends that are responsible for boosting the connected medical devices market in Japan. As per an article published by NLM in August 2025, the country has the largest aged population, with 29.1% of the population aged more than 65 years, along with a decline in birth rates from 1 million births to 750,000 as of 2023. However, contemporary modeling has suggested that the aging rate is poised to increase to 36.3% by the end of 2045. Additionally, this increased healthcare expenses by almost USD 547.9 billion (JPY 89 trillion), which is more than 1.6 times the actual level as of 2023, thus proliferating the market expansion.

Europe Market Insights

The Europe market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by a transition towards decentralized care models, the global center for medical technology, the adoption of portable medical electronics, an expansion in home healthcare networks, and the presence of favorable reimbursement policies. According to an article published by MedTech Europe in September 2025, the regional medical technology accounts for 26.4% of the global economy, roughly amounting to USD 193.7 billion (€170 billion) as of 2024. Based on this, Spain, the UK, Germany, Italy, and France are considered the top 5 countries offering medical technology solutions for different diseases, thereby demonstrating an optimistic outlook for the market’s exposure in the region.

Medica Device Industry Analysis in Europe, 2024

|

Countries |

Medical Device Share % |

|

Germany |

25.2 |

|

France |

12.8 |

|

UK |

11.9 |

|

Italy |

11.7 |

|

Spain |

6.1 |

|

Netherlands |

5.9% |

|

Switzerland |

3.8 |

|

Belgium |

3.5 |

|

Austria |

3.2 |

|

Poland |

2.7 |

|

Others |

13.2 |

Source: MedTech Europe

The Germany connected medical devices market is gaining increased exposure, owing to unparalleled healthcare facilities, the government-backed hospital reform fund, an increase in modernizing care delivery, the strong reimbursement pathways, and the demand for AI-based diagnostics surging. As stated in an article published by the Federal Ministry of Health in December 2025, there has been the provision of USD 56.9 billion (50 billion euros) for financing structural modifications in domestic hospitals. In addition, this particular fund was allocated for the upcoming 10-year period, of which the federal government is poised to cover USD 33 billion (29 billion euros). Therefore, this constitutes a robust contribution to the population in the country that further caters to modernizing the universal health coverage, thus enhancing the market growth and expansion.

The government’s strong commitment to digitalized health, the existence of a tech-savvy healthcare system, an upsurge in remote monitoring and telehealth adoption, an increase in telemedicine consultations, and suitable chronic disease management solutions are a few trends for boosting the connected medical devices market in the UK. As per an article published by the UK Government in June 2022, more than 28 million people currently have the NHS application, with over 40 million people constituting the NHS login, and the majority of trusts comprise an electronic patient record system. Based on this, an unprecedented investment of USD 198.3 million (£150 million) was initiated for digitalizing adult social care solutions in terms of digital adoption. Besides, an additional USD 2.6 billion (£2 billion) of funding for supporting electronic patient records has been allocated to assist more than 500,000 people to utilize digital tools, thus supporting the market expansion in the nation.

Key Connected Medical Devices Market Players:

- Medtronic PLC (Ireland/U.S.)

- Abbott Laboratories, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- GE Healthcare (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips NV (Netherlands)

- AliveCor, Inc. (U.S.)

- Wave Visions (India)

- Larkai Healthcare (India)

- Jamnaa Healthtech (India)

- Resmed (U.S.)

- Baxter International Inc. (U.S.)

- Aptar Digital Health (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Medtronic PLC develops connected solutions for chronic disease management, including intelligent insulin pumps, cardiac monitoring systems, and neurostimulation devices with remote capabilities. The company is advancing its connected health ecosystem through strategic alliances, such as integrating its monitoring parameters.

- Abbott Laboratories, Inc.’s medical devices business features a strong portfolio of connected technologies, including its FreeStyle Libre continuous glucose monitoring systems and advanced cardiovascular devices like the MitraClip and TriClip. The company focuses on creating smaller, more personal wearable technologies that integrate seamlessly into patients' lives.

- Boston Scientific Corporation specializes in implantable and interventional devices for cardiovascular care, including connected defibrillators and its Watchman stroke-risk reduction implant. The company is building a super-platform model and has recently acquired Penumbra to expand its neurovascular portfolio.

- GE Healthcare is a leader in connected imaging and patient monitoring solutions, advancing AI-powered diagnostics with cloud integration for comprehensive hospital data insights. The company collaborates with Medtronic to integrate next-generation monitoring technologies into its platforms.

- Siemens Healthineers AG is a market leader in imaging and precision therapy, with a focus on AI-powered solutions like its photon-counting CT scanners. The company positions itself as a key partner for large healthcare institutions through its global presence and extensive R&D investment.

Here is a list of key players operating in the global market:

The global connected medical devices market exhibits a moderately fragmented competitive structure, where established multinational MedTech conglomerates compete alongside agile, software-centric innovators. Industry leaders, such as Medtronic, Abbott, and Boston Scientific, dominate through expansive product portfolios, deep clinical expertise, and worldwide distribution networks. Concurrently, specialized players such as AliveCor are capturing market share by focusing on niche, software-driven solutions like smartphone-integrated ECG devices. Besides, in August 2024, Medtronic plc proclaimed that the U.S. FDA approved its very own Simplera™ continuous glucose monitor, which is the organization’s first-ever all-in-one and disposable medical device, thus positively contributing to the connected medical devices industry growth.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, Resmed and ŌURA readily partnered and expanded accessibility to ensure sleep health education, along with ensuring pathways for assisting and caring patients with better sleep and optimized health.

- In August 2025, Baxter International Inc. introduced the Welch Allyn Connex 360 Vital Signs Monitor, which is its very own next-generation patient monitoring device, offering an innovative connectivity and security platform.

- In June 2024, Aptar Digital Health collaborated with SHL Medical for expanding connected device technologies by readily incorporating the SaMD platform for providing wide-ranging solutions to assist patients on injectable therapies in managing their diseases.

- Report ID: 8648

- Published Date: Jul 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Connected Medical Devices Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.