Medical Laser Market Outlook:

Medical Laser Market size was valued at USD 6.6 billion in 2025 and is projected to reach USD 18.6 billion by the end of 2035, rising at a CAGR of 12.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of medical laser is assessed at USD 7.4 billion.

The medical laser market is experiencing dynamic growth, owing to the rising adoption rates across diverse healthcare applications such as surgery, dermatology, ophthalmology, and dental procedures. With the expanding applications, governments across major countries are exploring lasers’ complete potential with significant R&D investments. Based on the August 2023 data from the U.S. Department of Energy, the Office of Science has granted a total of USD 28.5 million in funding for LaserNetUS, which is North America’s high-intensity laser research network, to advance discovery science and inertial fusion energy. This investment will support projects in areas such as astrophysics, plasma science, cancer radiotherapy, materials science, and inertial confinement fusion. Moreover, with over 1,200 members, LaserNetUS will play a key role in improving both discovery science and the future of inertial fusion energy.

Furthermore, a rising awareness of the benefits of laser-based therapies, coupled with the incorporation of lasers into outpatient and cosmetic procedures, is fueling demand in the market. As per an article published by NIH in May 2025, a U.S. study of fellowship-trained laser dermatologists found that only 124 specialists across the nation, which equates to roughly one laser dermatologist per 2.7 million people. It also stated that these dermatologists dedicate significantly more clinical time to laser procedures, wherein 19% spending more than 50% of their practice on lasers when compared to minimal time in medical spas or plastic surgery offices. Hence, the increasing patient demand and expanding outpatient applications indicate a strong market opportunity for investment in medical laser technologies.

Medical Laser Procedure Utilization and Provider Involvement: Officially Reported Statistics (2025)

|

Metric |

Fellowship-Trained Dermatologists |

Plastic Surgeons |

Medical Spas |

|

Number of specialists |

124 |

- |

- |

|

Average wait time (days) |

23 |

11 |

4 |

|

Average consultation fee (USD) |

153 |

78 |

30 |

|

Physician involvement in procedures (%) |

60 |

33 |

9 |

|

Nonphysician provider involvement (%) |

4 |

18 |

26 |

|

Laser technician involvement (%) |

3 |

35 |

56 |

|

Direct on-site supervision (%) |

93 |

90 |

41 |

|

Customization of laser treatments (%) |

98 |

98 |

63 |

|

Clinical time dedicated to lasers (>50%) (%) |

19 |

0 |

0 |

Source: NIH

Key Medical Laser Market Insights Summary:

Regional Highlights:

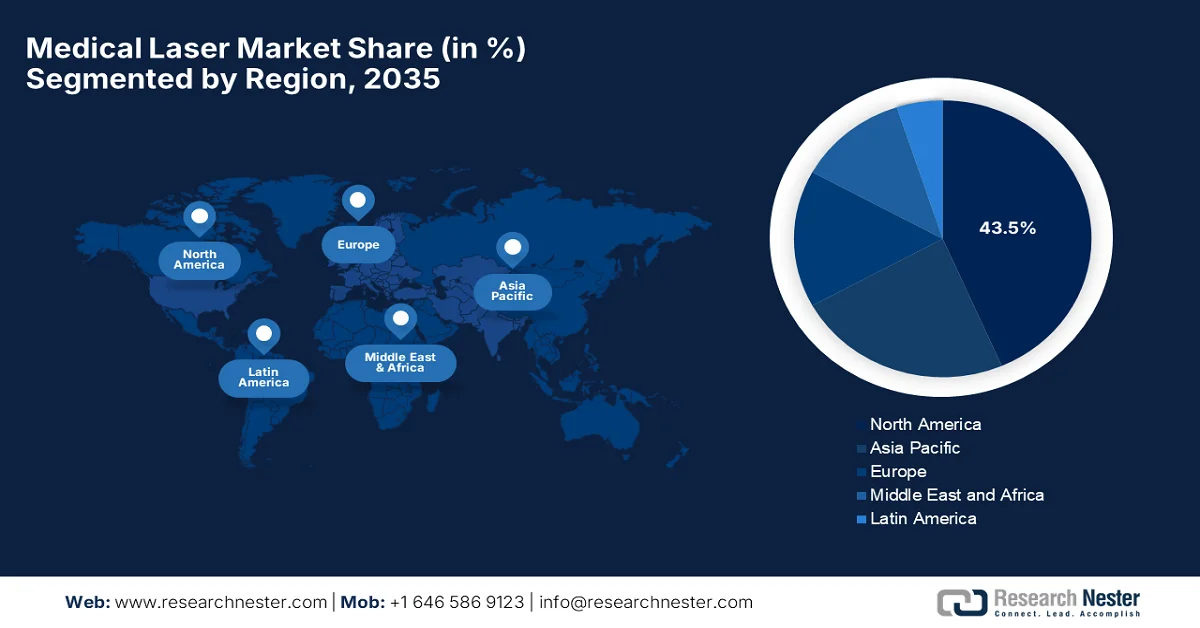

- North America medical laser market is projected to hold the largest revenue share of 43.5% by 2035, supported by a robust research ecosystem, strong preference for cosmetic treatments, and rapid adoption of advanced laser technologies.

- Asia Pacific is anticipated to witness the fastest growth in the market through 2035, impelled by expanding healthcare infrastructure and a rising number of laser clinics.

Segment Insights:

- The consumables segment of the medical laser market is projected to account for 74.4% share by 2035, attributed to the escalating volume of consumables required per laser system and the rising demand for diverse surgical procedures.

- By 2035, the surgical laser subtype is anticipated to capture a considerable share of the market, propelled by the global shift toward minimally invasive procedures that reduce recovery time and complications.

Key Growth Trends:

- Technological improvements & innovation

- Growing prevalence of chronic & age-related diseases

Major Challenges:

- Regulatory compliance and approval hurdles

- Safety Concerns and patient risk management

Key Players: Lumenis Ltd. (Israel), Candela Medical / Candela Corporation (U.S.), Alma Lasers Ltd. (Israel), BIOLASE, Inc. (U.S.), Cynosure, Inc. (Hologic) (U.S.), Boston Scientific Corporation (U.S.), Alcon Laboratories, Inc. (Switzerland), IRIDEX Corporation (U.S.), Fotona d.o.o. (Slovenia), Quanta System S.p.A. (Italy), Sciton, Inc. (U.S.), IPG Photonics Corporation (U.S.), Bausch + Lomb (U.S./Canada), Topcon Corporation (Japan), El.En. S.p.A. (Italy), Nidek Co., Ltd. (Japan), ZEISS (Carl Zeiss Meditec AG) (Germany), BTL International (Czech Republic), BISON Medical (South Korea), SOLAR LS (Russia).

Global Medical Laser Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.6 billion

- 2026 Market Size: USD 7.4 billion

- Projected Market Size: USD 18.6 billion by 2035

- Growth Forecasts: 12.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (43.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, France

- Emerging Countries: India, South Korea, Brazil, Italy, Australia

Last updated on : 16 February, 2026

Medical Laser Market - Growth Drivers and Challenges

Growth Drivers

- Technological improvements & innovation: This is the major driving factor for the medical laser market. The newer laser types, such as picosecond, femtosecond, diode, and solid-state lasers, integrated with AI, robotics, and smart sensors, broaden clinical applications. Also, these improved systems enhance outcomes, making lasers more attractive to healthcare providers across different nations. In July 2024, ViaLase, Inc. stated that it received CE mark approval for its ViaLase Laser, which is the first femtosecond laser system approved for treating primary open-angle glaucoma. Besides, this particular system combines femtosecond laser technology with micron-level image guidance to enable a non-invasive, image-guided, high-precision trabeculotomy (FLigHT), addressing unmet needs in glaucoma care by reducing reliance on invasive surgery. Hence, with such continuous developments, the market will grow at a rapid pace in the upcoming years.

- Growing prevalence of chronic & age-related diseases: The aging worldwide population and rising rates of chronic diseases such as ocular disorders, i.e., glaucoma, age-related macular degeneration, skin conditions, and cardiovascular diseases, also drives growth of this sector. These instances are increasing demand for effective, laser-based therapeutic and diagnostic solutions, thereby driving business in the market. According to official statistics published by the World Health Organization in August 2023, vision impairment and blindness predominantly affect older adults above 50 years, wherein age-related conditions such as glaucoma, age-related macular degeneration, diabetic retinopathy, cataract, and refractive errors are major causes. It also notes that population growth and ageing are expected to increase the vision impairment rates worldwide, creating sustained demand for effective diagnostic and therapeutic interventions.

Officially Reported Global Vision Impairment Statistics by Cause (2023)

|

Indicator |

WHO Reported Data |

|

Total number of people with vision impairment (near or distance) |

≥ 2.2 billion globally |

|

Cases are preventable or yet to be addressed |

Nearly 1 billion people |

|

People with cataract-related vision impairment |

94 million |

|

People with refractive error-related vision impairment |

88.4 million |

|

Age-related macular degeneration cases |

8 million |

|

Glaucoma cases |

7.7 million |

|

Diabetic retinopathy cases |

3.9 million |

|

People affected mainly over the age of |

50 years and above |

|

Annual global productivity loss due to vision impairment |

USD 411 billion |

Source: World Health Organization

- Expansion of aesthetic & cosmetic applications: The aesthetic medicine sector is efficiently growing, positively influenced by rising consumer interest in non-invasive cosmetic procedures. Also, the laser hair removal, skin resurfacing and rejuvenation, tattoo removal, and body contouring have gained traction, boosting adoption in both dermatology clinics as well as medical spas. In this context American Society of Plastic Surgeons states that skin resurfacing procedures that include ablative and non-ablative laser treatments reached 3,703,305 procedures in 2024, which is an increase from 3,501,696 procedures in 2023, i.e., a 6% year-on-year growth. From a strategic perspective, this measurable rise in procedural volumes indicates that there is a growing consumer preference for laser-based treatments and supports the expansion of the market and technologies in dermatology clinics.

Officially Reported Laser-Based Cosmetic Procedures in the U.S. (2023-2024)

|

Laser-Based Cosmetic Procedure Category |

2024 Procedures |

2023 Procedures |

|

Skin treatment using lasers (laser hair removal, IPL treatment, laser tattoo removal, laser leg vein treatment) |

3,112,056 |

3,101,772 |

|

Non-surgical skin tightening (energy-based devices incl. laser/radiofrequency systems) |

439,032 |

438,211 |

Source: American Society of Plastic Surgeons

Challenges

- Regulatory compliance and approval hurdles: Medical lasers are mostly subject to strict regulations in almost all nations. The approval process can be lengthy and costly, especially in the case of devices that utilize new wavelengths or novel delivery mechanisms. Therefore, for players in the market, compliance extends beyond premarket approval to ongoing quality control, safety standards, and reporting requirements. In this context, delays in regulatory clearance can cause hindrance to market entry, thereby exacerbating development costs. Furthermore, companies need to make investments in clinical trials, documentation, and regulatory procedures that can be restrictive for smaller manufacturers who are vying to enter multiple international markets simultaneously.

- Safety Concerns and patient risk management: Medical lasers are involved with high-energy light interacting with tissue, which can lead to inherent safety risks if not used properly. Complications such as burns, scarring, or unintended tissue damage can occur, harming patients and damaging the manufacturer’s reputation among the public. Therefore, the regulatory bodies, hospitals, and clinicians place a premium on device safety, reliability, and operator training. Also, to address this challenge, proper device design, fail-safe mechanisms, and clinician education are necessary, all of which increase development and operational costs. Moreover, any negative publicity from any events can slow market adoption, making survival in this highly regulated sector challenging.

Medical Laser Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.2% |

|

Base Year Market Size (2025) |

USD 6.6 billion |

|

Forecast Year Market Size (2035) |

USD 18.6 billion |

|

Regional Scope |

|

Medical Laser Market Segmentation:

Product Segment Analysis

In the product segment, the consumables are expected to garner the largest revenue share of 74.4% in the medical laser market during the forecast period. The dominance of the segment is mainly driven by the increasing number of consumables required per laser system and the rising demand for various surgical procedures. In March 2023, the U.S. FDA reported that it has cleared Wuhan Pioon Technology Co., Ltd’s medical diode laser (M2), which is a Class II device intended for incision, excision, ablation, vaporization, hemostasis, and coagulation of soft tissue. The device uses a fiber delivery system, which is considered a consumable that must be periodically replaced. Hence, this clearance highlights the regulatory recognition of consumable components in medical laser systems, thereby supporting ongoing demand in surgical procedures.

Type Segment Analysis

By the conclusion of 2035, the surgical laser subtype is anticipated to grow with a considerable share in the market. The growth of the segment is mainly propelled by global trends toward minimally invasive procedures that reduce recovery time and complications. Besides the laser-assisted surgeries in ophthalmology, cardiovascular, and general surgery are increasingly preferred due to precision and reduced tissue damage, supporting higher revenue capture over the upcoming years. Based on the government data from India in August 2025, the Army Hospital Research and Referral (AHRR) became the first government institute in the country to perform robotic custom laser cataract surgery by using the ALLY adaptive cataract treatment system. This femtosecond laser-assisted procedure automates critical steps such as corneal incisions and lens fragmentation with micron-level precision, enhancing surgical accuracy and patient outcomes, hence benefiting the segment’s growth.

End user Segment Analysis

In the market, the clinics, which are a part of end use segment, will grow with a significant share during the stipulated timeframe. The growth of the segment is mainly ascribable to their growing role in providing targeted, outpatient laser treatments. The expansion of specialty clinics in developing countries is considered to be yet another key driver, supported by rising per capita healthcare expenditure and increasing consumer awareness of advanced medical technologies. In addition, the rising preference for aesthetic and cosmetic procedures, such as dermatology and ophthalmology treatments, has also bolstered the adoption of laser systems in these clinics. Specialty clinics also benefit from shorter treatment times, personalized care, and specialized expertise, which attract those who are looking for minimally invasive procedures. As a result, this segment is expected to continue its strong growth trajectory throughout the forecast period.

Our in-depth analysis of the global market includes the following segments:

|

Segment |

Subsegments |

|

Product |

|

|

Type |

|

|

End user |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Medical Laser Market - Regional Analysis

North America Market Insights

The North America medical laser market is projected to garner the largest revenue share of 43.5% by the end of the stipulated timeline. The region’s leadership is mainly attributable to the supportive research ecosystem, a strong preference for cosmetic treatments, and the rapid adoption of advanced technologies. As of July 2025, data from NLM, the LaSAR BeaM study, which started in December 2025, will complete primary endpoints by December 2026, and is expected to be fully completed by December 2028, enrolling around 155 participants. The study is being sponsored by M.D. The Anderson Cancer Center is a Phase 2 interventional trial to evaluate laser interstitial thermal therapy or surgery followed by stereotactic radiosurgery (SRS2) versus close surveillance for patients with recurrent, previously irradiated brain metastases to determine if SRS2 after surgery/LITT delays local recurrence versus surveillance. Hence, such a supportive ecosystem will boost clinical adoption and increase investment in various laser applications across the region.

The extensive use of laser systems across ophthalmology, dermatology, oncology, and surgical specialties propels growth in the U.S. medical laser market. Simultaneously, the continued regulatory support from agencies such as the U.S. FDA ensures that a wide range of laser procedures are recognized and reimbursable where medically necessary. In February 2025, the U.S. FDA reported that it had cleared medical diode laser systems called CHARISMA and REGAL from Reveal Lasers Ltd. under 510(k) K234004 for use in general and plastic surgery and dermatology. Also, this clearance confirmed the devices were substantially equivalent to legally marketed predicate devices, allowing them to be marketed under Class II regulatory controls. Hence, such regulatory support promotes broader adoption of laser technologies and drives growth in the U.S. market across multiple specialties.

The publicly funded healthcare frameworks and burgeoning investments in modern healthcare facilities are the main fueling factors for the market in Canada. The growth of the market is also carried forward by regulatory approvals, public and private healthcare providers, who are integrating lasers for surgical, dermatological, and ophthalmic applications. In January 2025, Norlase reported that it had received Health Canada licensing for its ECHO green pattern laser, which is a portable, pattern-scanning photocoagulator that integrates laser and scanner into a single device for ophthalmic use. Also, NIH in April 2023 revealed that the Erchonia FX 635 low-level laser system has been licensed and is used in private pain and chiropractic clinics for treating chronic low back pain. This noninvasive, pain-free therapy provides relief through photobiomodulation, and with such consistent bureaucratic support, the market will grow at a rapid pace in the country.

APAC Market Insights

The Asia Pacific medical laser market has registered itself as the fastest-growing marketplace owing to its expanding healthcare infrastructure and a rising number of laser clinics. The heightened demand for anti-aging treatments, coupled with hair removal procedures, also boosts the adoption of aesthetic lasers in this region. In this regard, JETRO in December 2022 reported that the National Hospital Organization Sendai Medical Center in Japan published a government procurement notice for one laser device for skin treatment, classified under medical and surgical equipment. It also mentioned that this procurement was open to suppliers meeting legal, regulatory, and after-sales service requirements, which include registration under the Pharmaceutical Affairs Law as well as regional sales qualifications. Therefore, the aspect of government procurement agreements highlights Japan’s adoption of advanced medical laser technologies in public healthcare facilities, encouraging more players to establish their presence in the region.

The surging demand for cosmetic procedures, ophthalmic treatments, and oncology interventions provides an encouraging opportunity for pioneers in the China medical laser market. The country’s market growth is also taken forward by the government's focus on modernizing healthcare infrastructure, coupled with rising disposable income, which efficiently drives the adoption of innovative lasers. Based on the government data from China in January 2025, the Southern Medical University Dermatology Hospital officially procured one dual-wavelength medical laser treatment system, i.e., Nd: YAG picosecond/dual‑wavelength laser, brands PicoWay/GentleMax Pro Plus, which was procured through a government-managed tender. The contract was awarded to Guangzhou Jianxing Medical Equipment Co., Ltd. for ¥3,850,000 (approximately USD 550,000), which was followed by an evaluation by 5 appointed experts across technical, commercial, and price criteria, hence denoting an optimistic opportunity for the market’s growth in the country.

China Medical Laser Market: Government Procurement Projects and Strategic Insights (2025)

|

Procurement Project |

Procuring Entity |

Laser Type |

Contract Value (RMB / USD) |

Key Notes |

Medical Laser Market Opportunity |

|

Holmium Laser Therapy Machine |

Peking Union Medical College Hospital, Chinese Academy of Medical Sciences |

Lumenis Pulse 120H |

¥2,950,000 (approximately) USD 435,000) |

Single-source procurement, 5 experts reviewed |

Highlights the demand for advanced therapeutic lasers in Chinese hospitals |

|

Carbon Dioxide Surgical Laser System (Skin Laser Treatment System) |

Guangdong Provincial People's Hospital |

CO₂ Surgical Laser System |

¥3,050,000 (approximately USD 450,000) |

Open tender, electronic bidding |

Indicates growth in aesthetic & surgical laser adoption in public healthcare |

Source: Official Press Releases

The rising healthcare access, awareness of non-invasive treatments, and rapid expansion of private healthcare facilities are the major fueling factors behind the robust growth of the medical laser market in India. The laser utilization in the country is extensively supported by financial backing, academic research centers, and proper skill development programs for medical professionals. In March 2025 Centre for Sight notified that it has launched Asia’s first-ever AI-based Lasik machine, AMARIS 1050RS, which is capable of correcting vision in about 10 seconds per eye and completing the entire procedure in approximately 10 minutes, thereby halving the time of traditional Lasik surgeries. The system features predictive AI foresight, improved eye-tracking, and a 1050 Hz laser repetition rate, enabling a very precise treatment and faster patient recovery within 24 to 48 hours. Therefore, with such fast-paced technological improvements, the country is all set to witness unprecedented growth in the upcoming years.

Government Medical College & Hospital (GMCH) Chandigarh Laser Procedure Costs based on Monthly Income (INR & USD) 2026

|

Procedure |

Income up to ₹5,000 |

Income ₹5,001-₹25,249 |

Income >₹25,250 |

|

Laser treatment (full course) |

- |

90 (USD 1.08) |

180 (USD 2.16) |

|

LASIK with Microkeratome |

5,000 (USD 60) |

6,000 (USD 72) |

6,000 (USD 72) |

|

PRK (Photorefractive Keratectomy) |

5,000 (USD 60) |

6,000 (USD 72) |

6,000 (USD 72) |

|

Photocoagulation / Laser coagulation |

- |

90 (USD 1.08) |

180 (USD 2.16) |

|

YAG Capsulotomy |

- |

20 (USD 0.24) |

40 (USD 0.48) |

Source: GMCH

Europe Market Insights

There is a huge growth opportunity for Europe medical laser market, heavily propelled by the well-established healthcare infrastructure, and strong emphasis on R&d Countries across the region are opting for these improved laser technologies with regulatory harmonization, which is facilitating cross-border commercialization. The European Union-funded Lasers4EU project was launched in 2024 and is coordinated by Forschungsverbund Berlin e.V., which aims to create a virtual distributed laser research infrastructure by integrating major regional laser facilities. Besides, this project amounts to a total cost of €7.18 million (USD 7.9 million) and an EU contribution of €5 million (USD 5.5 million), and it provides academic and industrial users access to laser technologies for applications in terms of biomedical optics, photonics, and high-field science. Therefore, this initiative exemplifies the prominence of government-backed research funding, which is strengthening the region’s medical laser industry.

The advanced healthcare system, a huge focus on clinical research, and integration of enhanced technologies in hospitals and clinics present a lucrative growth opportunity for Germany medical laser market. The country has been identified as one of the leading adopters of minimally invasive surgical solutions and aesthetic laser procedures, which is also being supported by robust regulatory frameworks. In January 2025, the TheraOptik project, which was funded by the German Federal Ministry of Education and Research, witnessed researchers at Leibniz IPHT Jena, in collaboration with University Hospital Jena and Grintech, developing an AI-enhanced endoscopic laser system that identifies and selectively removes tumor tissue in real time. Leibniz also notes that the device integrates diagnosis and therapy, using a femtosecond laser to precisely ablate diseased tissue by achieving 96% accuracy in preclinical tests. These publicly supported instances in the country are creating strong growth potential for the market to progress.

The UK medical laser market is expanding in the regional landscape, effectively propelled by a combination of public and private healthcare providers, increasing demand for non-invasive procedures, and research collaborations with universities and medical institutions. In May 2024, NHS England stated that it had rolled out laser interstitial thermal therapy for patients with drug-resistant epilepsy at King’s College Hospital (London) and The Walton Centre (Liverpool). In addition, this minimally invasive, MRI-guided laser procedure precisely targets and destroys seizure-causing brain tissue, reducing recovery time and surgical risks. Furthermore, the initiative was supported by national healthcare policy and research collaborations, underscoring the country’s integration of laser technologies into clinical care for improved patient outcomes, hence indicating a positive market outlook.

Key Medical Laser Market Players:

- Lumenis Ltd. (Israel)

- Candela Medical / Candela Corporation (U.S.)

- Alma Lasers Ltd. (Israel)

- BIOLASE, Inc. (U.S.)

- Cynosure, Inc. (Hologic) (U.S.)

- Boston Scientific Corporation (U.S.)

- Alcon Laboratories, Inc. (Switzerland)

- IRIDEX Corporation (U.S.)

- Fotona d.o.o. (Slovenia)

- Quanta System S.p.A. (Italy)

- Sciton, Inc. (U.S.)

- IPG Photonics Corporation (U.S.)

- Bausch + Lomb (U.S./Canada)

- Topcon Corporation (Japan)

- El.En. S.p.A. (Italy)

- Nidek Co., Ltd. (Japan)

- ZEISS (Carl Zeiss Meditec AG) (Germany)

- BTL International (Czech Republic)

- BISON Medical (South Korea)

- SOLAR LS (Russia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Lumenis Ltd. is a pioneer and one of the largest global medical laser manufacturers, which benefits from a broad portfolio covering aesthetic, surgical, and ophthalmic lasers. The company has spent years in terms of global expansion and innovation in multi-application platforms, with a prime focus on skin rejuvenation, hair removal, and minimally invasive surgical lasers.

- Cynosure, Inc., which is currently a part of Hologic, is a specialist in terms of aesthetic and dermatologic laser systems, i.e., diode, Nd: YAG, and picosecond platforms for hair removal, pigment correction, and body contouring. The firm has a very strong direct sales and distribution network in North America, Europe, and the Asia Pacific.

- Alma Lasers Ltd. is primarily focused on cosmetic laser and energy-based devices, which are utilized for skin, body, and hair treatments. It is a part of the Sisram Medical group, and it leverages modular, cost-effective systems that address a wide range of aesthetic needs.

- BIOLASE, Inc. is based in the U.S. and is well-known for dental laser systems, which offer solutions for both hard and soft tissue procedures that enhance precision and patient comfort. BIOLASE’s corporate strategy revolves around expanding product portfolios with all‑tissue lasers and increasing its presence in the dental sector through strategic partnerships and regulatory clearances.

- Candela Corporation is yet another prominent player in aesthetic and dermatologic laser platforms, which is best known for innovations such as pulsed‑dye and picosecond systems. Besides, the firm makes continued investments in improving treatment versatility, such as platforms for vascular and pigmented lesions, and maintains a robust pipeline of efficient devices for energy-based medical aesthetics.

Below is the list of some prominent players operating in the global market:

Pioneers involved in the medical laser market are opting for distinct growth strategies to strengthen their international presence. The competitive landscape is identified to be highly intense, which is led by firms leveraging enhanced portfolios around surgical, aesthetic, ophthalmic, and dental applications. Leading pioneers such as Lumenis, Candela, and Boston Scientific dominate this field with their continuous innovation, profitable mergers, and international distribution networks, whereas others, such as Fotona, Quanta System, and IPG Photonics, compete in terms of specialized niches. Extensive investments in R&D, acquisitions, partnerships, and expansion into emerging markets are a few strategies undertaken by players to secure their market positions. In March 2025, Alcon announced its agreement to acquire LENSAR, Inc. for up to USD 430 million by including LENSAR’s ALLY robotic cataract laser system and streamlining software to strengthen its femtosecond laser-assisted cataract surgery portfolio.

Corporate Landscape of the Medical Laser Market:

Recent Developments

- In February 2026, Mauna Kea Technologies announced the formation of a new commercial organization to accelerate international growth of CellTolerance and Cellvizio, focusing on Europe, the Middle East, and Australia, expanding usage of its confocal laser endomicroscopy and diagnostic laser technologies.

- In January 2026, Laser Photonics Corporation announced that it had received a USD 0.5 million order for its CMS Laser processing system from a U.S.-based medical device manufacturer. The custom system uses two fiber lasers, one for marking and the other for selective ablation of metal components.

- Report ID: 4437

- Published Date: Feb 16, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Medical Laser Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.