Li-ion Batteries Recycling Market Outlook:

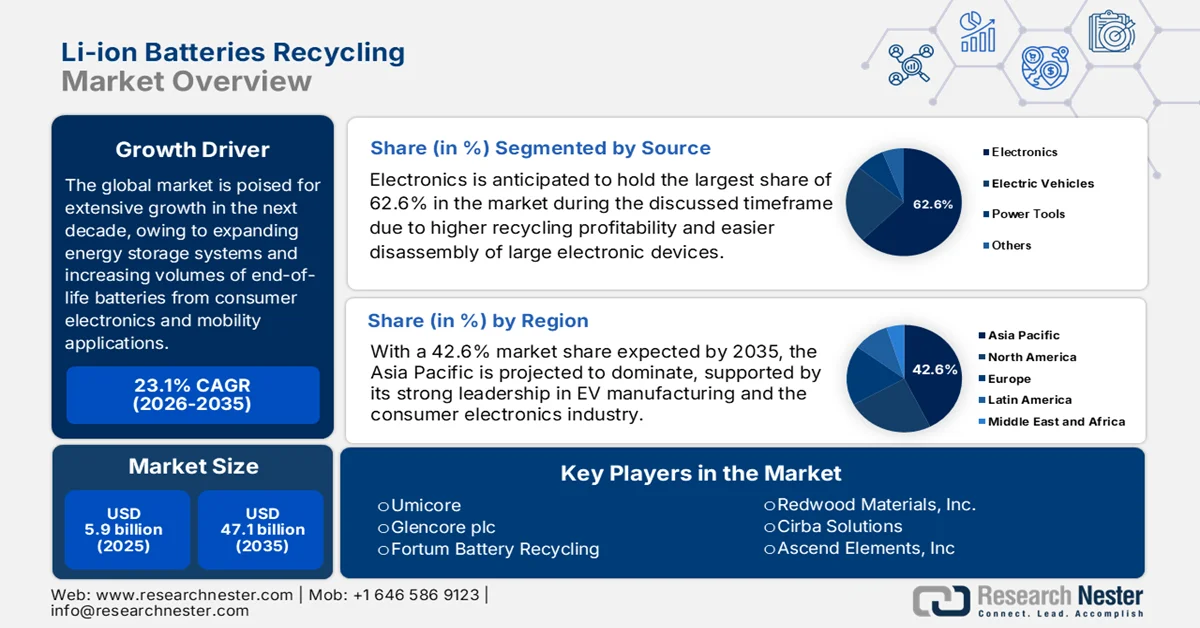

Li-ion Batteries Recycling Market size was valued at USD 5.9 billion in 2025 and is expected to cross USD 47.1 billion by the end of 2035, expanding at more than 23.1% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of Li-ion batteries recycling is evaluated at USD 7.2 billion.

The rising adoption of electric vehicles, expanding energy storage systems, and increasing volumes of end-of-life batteries from consumer electronics and mobility applications are the factors behind the extensive growth of the global Li-ion batteries recycling market. Industry participants are highly focused on recovering valuable materials such as lithium, cobalt, nickel, manganese, and copper with the main goal to support circular economy initiatives and reduce dependence on virgin raw materials. In March 2025, the article published by CAS Organization revealed that the lithium-ion battery recycling industry is scaling fast, wherein the global capacity reached 1.6 million tons per year in 2025, and is projected to exceed 3 million tons annually once planned facilities come online. In addition, it also mentioned that EV battery retirements are surging, expected to grow at a 43% CAGR from 2021 to 2030, hitting 1483 GWh per year by 2030. Recycling is also a major decarbonization lever. Studies show that processing 1 kg of LIBs can cut 2.7 to 4.6 kg CO₂ equivalent, thus making it critical for sustainable EV supply chains.

2024 Global Lithium-Ion Battery Analysis: Shipments Value, Leading Importers, and Share Trends

|

Country |

Imports (USD Billion) |

Share of Global Imports (%) |

|

U.S. |

25.20 |

21.7 |

|

Germany |

23.00 |

19.8 |

|

South Korea |

4.75 |

4.1 |

|

Vietnam |

4.45 |

3.8 |

|

Mexico |

4.29 |

3.7 |

|

France |

3.51 |

3.0 |

|

Australia |

3.35 |

2.9 |

|

Czechia |

3.03 |

2.6 |

|

UK |

2.96 |

2.6 |

|

India |

2.90 |

2.5 |

Source: OEC

Furthermore, advancements in terms of hydrometallurgical, direct recycling, and material recovery technologies are improving recycling efficiency and enabling higher-quality output for reuse in battery manufacturing, benefiting the overall market. Growing investments in recycling infrastructure and strategic partnerships between battery manufacturers, automakers, and recyclers are also strengthening the market outlook. In March 2025, the article published by the U.S. Geological Survey reported that in 2024, construction of lithium battery recycling plants readily advanced as automakers partnered with recyclers to secure sustainable material supplies. In addition, the U.S. Department of Energy supported this with a total of USD 44.8 million in funding for eight projects under the Bipartisan Infrastructure Law, with a main aim to lower EV battery recycling costs and, ultimately, vehicle prices.

U.S. Lithium Import Sources 2020 - 2023

Source: USGS

Key Li-ion Batteries Recycling Market Insights Summary:

Regional Highlights:

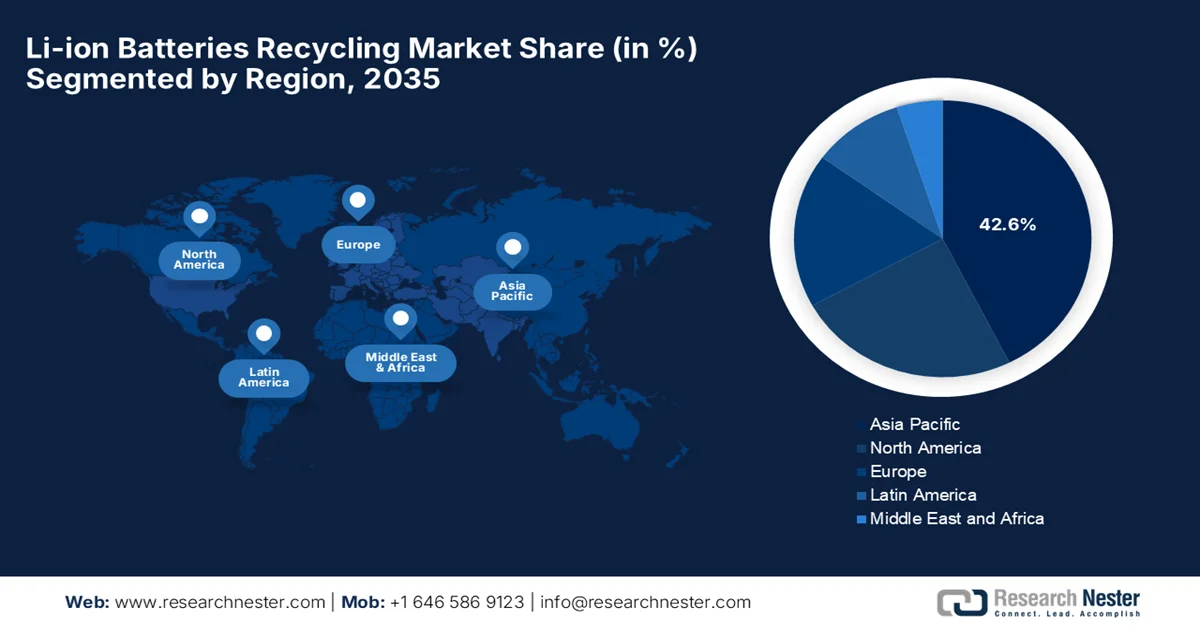

- Asia Pacific is projected to capture 42.6% of the Li-ion batteries recycling market by 2035, bolstered by its leadership in electric vehicle manufacturing, battery production, and consumer electronics industries

- North America is anticipated to register exponential growth in the market throughout 2026-2035, accelerated by efforts to establish localized critical mineral supply chains supported by green energy incentives and domestic manufacturing policies

Segment Insights:

- The electronics segment is expected to account for 62.6% of the Li-ion batteries recycling market by 2035, fueled by higher recycling profitability, easier disassembly of large electronic devices, and the long operational lifespan of batteries used in consumer electronics

- The lithium cobalt oxide segment is forecast to secure a considerable revenue share during 2026-2035, supported by the extensive installed base of LCO batteries in consumer electronics and the high recycling value of cobalt-rich battery materials

Key Growth Trends:

- Escalating EV adoption and end-of-life volume

- Tightening regulatory frameworks

Major Challenges:

- High collection and transportation complexity

- Technological challenges from evolving battery chemistries

Key Players: Umicore (Belgium), Glencore plc (Switzerland), Fortum Battery Recycling (Finland), Redwood Materials, Inc. (U.S.), Cirba Solutions (U.S.), Ascend Elements, Inc. (U.S.), Ecobat Technologies Ltd. (UK), GEM Co., Ltd. (China), Brunp Recycling Technology Co., Ltd. (China), Attero Recycling Pvt. Ltd. (India), American Battery Technology Company (U.S.), RecycLiCo Battery Materials Inc. (Canada), Ace Green Recycling, Inc. (U.S.), Lyten, Inc. (U.S.), TES-AMM Pte. Ltd. (Singapore).

Global Li-ion Batteries Recycling Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.9 billion

- 2026 Market Size: USD 7.2 billion

- Projected Market Size: USD 47.1 billion by 2035

- Growth Forecasts: 23.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, South Korea, Germany

- Emerging Countries: India, Canada, France, Sweden, Australia

Last updated on : 23 June, 2026

Li-ion Batteries Recycling Market - Growth Drivers and Challenges

Growth Drivers

- Escalating EV adoption and end-of-life volume: The growth in electric vehicle sales is efficiently generating a large future pool of end-of-life batteries. Early generation of EVs are currently in the retirement stage, which is creating encouraging growth opportunities for pioneers in the Li-ion batteries recycling market. In addition, manufacturing scrap from gigafactories provides immediate recyclable material, ensuring a consistent supply for recyclers and accelerating market expansion globally across different industrial ecosystems. The European Commission, in July 2023, opted for regulation (EU) 2023/1542, which sets out strict sustainability, safety, and circular economy requirements for batteries and waste batteries. Member states need to achieve collection targets 63% by 2027 and 73% by 2030 and enforce minimum recycled content in EV and industrial batteries, which includes 16% cobalt, 85% lead, 6% lithium, and 6% nickel by 2031.

- Tightening regulatory frameworks: Governments across different nations are enforcing strict regulations such as mandatory recycled content requirements, extended producer responsibility, and landfill bans. The existence of these policies compels manufacturers to recycle lithium-ion batteries responsibly, thereby accelerating investments in the market. In November 2023, the article published by the National Institute of Health (NIH) reported that the environmental burden of the global lithium-ion battery supply chain, showing that China, with 45%, Indonesia, with 13%, and Australia 9% account for two-thirds of current emissions. It also mentioned that switching from nickel-based to lithium iron phosphate chemistries could save 1.5 GtCO₂eq, and recycling reduces impacts, with direct methods lowering emissions by 61%, hydrometallurgical by 51%, and pyrometallurgical by 17%, thus benefiting the overall market’s growth.

Challenges

- High collection and transportation complexity: One of the primary challenges witnessed in the market is the proper collection and transportation of spent batteries, i.e., logistics. These end-of-life batteries are being dispersed across consumer electronics, electric vehicles, industrial equipment, and energy storage systems, which in turn makes aggregation costly and logistically complex. Apart from this, the lithium-ion batteries are considered to be hazardous owing to their potential fire and thermal runaway risks, which necessitate specialized packaging, handling, and transportation procedures. In most regions, collection infrastructure is underdeveloped, which leads to low recovery rates and significant volumes of batteries being stored, improperly disposed of, or exported, negatively impacting the market’s expansion.

- Technological challenges from evolving battery chemistries: The surging innovations in battery technologies are also a major burden for the recyclers in the market. Manufacturers are introducing new battery chemistries, which include lithium iron phosphate, high-manganese cathodes, and next-generation battery designs, wherein each requires different recycling approaches. On the other hand, the existing recycling processes cannot completely achieve necessary recovery rates or economic returns across all battery types, thereby creating operational inefficiencies. LFP batteries contain lower concentrations of high-value metals such as cobalt and nickel, reducing the financial incentives for recycling. In addition, battery packs keep changing in terms of design, assembly methods, and material composition, making automated disassembly difficult.

Li-ion Batteries Recycling Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

23.1% |

|

Base Year Market Size (2025) |

USD 5.9 billion |

|

Forecast Year Market Size (2035) |

USD 47.1 billion |

|

Regional Scope |

|

Li-ion Batteries Recycling Market Segmentation:

Source Segment Analysis

Electronics, which is under the source segment, is anticipated to hold the largest share of 62.6% in the Li-ion batteries recycling market during the discussed timeframe. The dominance is majorly propelled by factors such as higher recycling profitability, easier disassembly of large electronic devices, and the long operational lifespan of batteries embedded in consumer electronics. In March 2023, KION Group and Li-Cycle announced a strategic partnership to advance lithium-ion battery recycling with up to 95% recovery efficiency through Li-Cycle’s sustainable Spoke & Hub process. This particular collaboration is set to run until 2030, and it will begin recycling operations in Magdeburg, Germany, with plans to expand into France and other regions, thus denoting a wider segment scope.

Chemistry Segment Analysis

The lithium cobalt oxide, which is under the chemistry segment, is expected to grow with a considerable revenue share in the market by the end of 2035. The segment’s growth is effectively driven by an extensive installed base of LCO batteries in consumer electronics such as smartphones, laptops, and portable devices, which continue to generate a steady stream of end-of-life batteries for recycling. In addition, LCO batteries contain a high proportion of cobalt, which is a critical and high-value metal that enhances the economic viability of recycling processes. In April 2023, Apple announced that all Apple‑designed batteries will use 100% recycled cobalt, whereas magnets will rely entirely on recycled rare earth elements, and circuit boards will feature recycled tin and gold. Apple is accelerating toward its Apple 2030 carbon‑neutral goal and is supported by innovations such as the Daisy disassembly robot, and hence contributing to the segment’s expansion.

Recycling Process Segment Analysis

The hydrometallurgical recycling process is expected to progress in the market owing to its superior metal recovery efficiency, lower environmental impact, and compatibility with different sorts of battery chemistries. Besides, this hydrometallurgy operates at lower temperatures and enables higher recovery rates of critical materials such as lithium, cobalt, and nickel through chemical leaching and solvent extraction techniques. Its cleaner operation, reduced greenhouse gas emissions, and minimal energy consumption also strengthen its adoption across large-scale recycling facilities. In addition, continuous advancements in terms of closed-loop processing and purification technologies are also enhancing yield quality and operational efficiency, making hydrometallurgy the preferred and most scalable solution.

Our in-depth analysis of the Li-ion batteries recycling includes the following segments:

|

Segment |

Subsegments |

|

Source |

|

|

Chemistry |

|

|

Recycling Process |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Li-ion Batteries Recycling Market - Regional Analysis

APAC Market Insights

The Asia Pacific Li-ion batteries recycling market is predicted to attain the largest share of 42.6% during the forecast period. The dominance of the region is driven by its strong position in electric vehicle manufacturing, battery production, and consumer electronics industries. Major economies such as China, Japan, South Korea, and India are producing significant volumes of end-of-life batteries due to rising EV penetration and growing energy storage installations. Resources, Conservation and Recycling in March 2026 reported that in Japan, end‑of‑life portable lithium‑ion batteries present major challenges, with almost 8160 tons generated in a year, mainly from smartphones, laptops, tablets, cordless vacuums, power banks, and motor‑assisted bicycles. The country’s official schemes are covering 77% of potential flows, but only 14% were actually collected. Therefore, this underscores the urgent need for stronger collection frameworks and unified policies to ensure safe disposal, resource recovery, and reduced fire risks in waste facilities.

An immense wave of retiring first-generation electric vehicles and a vast supply of domestic gigafactory manufacturing scrap are boosting the overall Li-ion batteries recycling market in China. Strict state-enforced life-cycle management policies, unified national dismantling standards, and extended producer responsibility rules are compelling top-tier automotive OEMs, cell manufacturers, and hydrometallurgical refiners to form expansive strategic alliances. Based on the government data published in June 2025, China’s booming EV battery recycling industry is turning retired batteries into valuable resources, with forecasts showing that the number of retired batteries will rise to 3.5 million tons by 2030. In this context, companies such as Tianjin Battery Technology and GEM are achieving lithium recovery rates above 90%, whereas expanding nationwide networks and overseas partnerships to build a circular supply chain.

In India, the market is positioned for solid upliftment in the upcoming years, owing to the accelerating domestic adoption of electric two and three-wheeled vehicles. The market is making a shift from an unorganized scrap sector into a structured, formal ecosystem, catalyzed by the government's mandates and hazardous waste management frameworks. According to the Press Information Bureau (PIB), in December 2025, India’s Battery Waste Management Rules 2022, notified on 24 August 2022, mandate Extended Producer Responsibility for producers and importers regarding proper collection, recycling, or refurbishment of waste batteries. It also mentioned that a centralized online portal has already registered 3,391 producers and 43 recyclers, enabling certificate exchange and compliance tracking. Since the rules came into effect, about 15,370 tons of lithium-ion battery waste have been recycled, whereas the PLI ACC scheme further incentivizes advanced technologies, R&D, and reduced import dependency to strengthen India’s battery ecosystem.

North America Market Insights

The North America Li-ion batteries recycling market is predicted to experience exponential growth from 2026 to 2035. The region’s upliftment in this field is driven mainly by a push to establish localized, secure supply chains for critical minerals. The region’s market is also spurred by federal green energy tax incentives, strict domestic manufacturing quotas, and regional extended producer responsibility policies. For instance, in August 2024, scientists at the U.S. Department of Energy’s Ames National Laboratory introduced the BRAWS recycling process, which is a method that uses only water and carbon dioxide to recover lithium from spent batteries. BRAWS avoids toxic chemicals and high heat, and it achieves near‑complete lithium recovery while also producing green hydrogen as a valuable byproduct, thus making it suitable for bolstering the region’s market growth.

The federal policies that mandate localized mineral sourcing for clean energy incentives are responsibly driving the U.S. Li-ion batteries recycling market. Major domestic automakers and electronics producers are forging tight, closed-loop alliances with recycling technology firms with a main goal to capture factory-floor manufacturing scrap and a rising stream of retired electric vehicle packs. For instance, in November 2023, researchers at the U.S. Department of Energy’s Oak Ridge National Laboratory developed a green recycling solution using citric acid and ethylene glycol to recover metals from spent lithium‑ion batteries. It also mentioned that this method leached nearly 100% of cobalt and lithium from the cathode, achieving over 96% cobalt recovery within hours, without hazardous chemicals or secondary wastes, hence indicating a positive outlook for the market’s expansion.

In Canada, the Li-ion batteries recycling market has gained traction, propelled by its mining heritage and stringent environmental regulations. The country’s recyclers are forming deep strategic alliances with international automotive groups and regional battery gigafactories for a steady intake of manufacturing scrap and end-of-life electric vehicle packs. As of May 2026, data published by the government of Canada underscores multiple lithium battery recycling pathways to address growing end‑of‑life challenges. These include hydrometallurgical methods, pyrometallurgical methods, and direct recycling, which dismantles batteries wherein each pathway offers trade‑offs in efficiency, cost, and environmental impact. Together they form a critical strategy for reducing waste, recovering valuable resources such as lithium and cobalt, and supporting Canada’s clean energy transition.

Europe Market Insights

In Europe, the Li-ion batteries recycling market is progressing at a robust pace of progress as a most stringently regulated and policy-driven circular economies, due to substantial regional sustainability frameworks. To achieve compliance and secure localized access to critical minerals, industry players are focused on developing a highly sophisticated network of commercial-scale pre-treatment and hydrometallurgical refining hubs. For instance, the joint EU–India EV battery recycling initiative, announced in May 2026, carries a funding pool of USD 16.5 million. This program, co‑funded by Horizon Europe and India’s Ministry of Heavy Industries, will support advanced recycling technologies, pilot‑scale demonstrations, and a joint pilot line in India. By turning battery waste into a virtual mine for critical materials such as lithium, cobalt, and graphite, the initiative strengthens circular value chains.

The nation's prominent automotive manufacturing sector and presence of domestic automakers, chemical giants, and waste management specialists are fueling the growth of the market in Germany. The market places an immense premium on minimizing the environmental footprint of the recycling process itself, thereby fostering engineering innovations that optimize energy efficiency and wastewater treatment during material recovery. In this context, in June 2023, BASF announced the inauguration of Europe’s first co-located center for battery materials production and recycling in Schwarzheide, Germany, which is a major milestone in closing the loop of the regional battery value chain. This facility includes a plant for high-performance cathode active materials and a recycling plant for producing black mass, both of which are designed to significantly reduce the carbon footprint.

The UK Li-ion batteries recycling market is being supported by the development of industrial-scale recycling infrastructure and strong involvement from domestic waste management and automotive-linked recycling firms. Along with this, partnerships with automotive and service-sector networks, such as EV repair and battery collection schemes, also shape the market dynamics in the country. In May 2026, Technology Minerals' subsidiary, Recyclus, secured a total of USD 510,000 from the UK’s Battery Innovation Programme to develop ReCAM, which is a system that converts black mass from Li-ion battery waste into reusable cathode active materials. This innovation will allow local processing of battery waste, strengthening the UK’s circular battery supply chain, reducing emissions, and cutting reliance on overseas processing.

Key Li-ion Batteries Recycling Market Players:

- Umicore (Belgium)

- Glencore plc (Switzerland)

- Fortum Battery Recycling (Finland)

- Redwood Materials, Inc. (U.S.)

- Cirba Solutions (U.S.)

- Ascend Elements, Inc. (U.S.)

- Ecobat Technologies Ltd. (UK)

- GEM Co., Ltd. (China)

- Brunp Recycling Technology Co., Ltd. (China)

- Attero Recycling Pvt. Ltd. (India)

- American Battery Technology Company (U.S.)

- RecycLiCo Battery Materials Inc. (Canada)

- Ace Green Recycling, Inc. (U.S.)

- Lyten, Inc. (U.S.)

- TES-AMM Pte. Ltd. (Singapore)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Umicore is one of the most established and influential players in the global market, which has decades of experience in materials technology and precious metal recovery. The company operates advanced battery recycling facilities in Europe, and it is highly focused on closed-loop recycling solutions that recover critical materials such as cobalt, nickel, lithium, and copper.

- Redwood Materials, Inc. is based in the U.S., which benefits from a comprehensive circular supply-chain approach. The firm specializes in recovering battery materials from manufacturing scrap and end-of-life batteries and converting them into battery-grade components.

- GEM Co., Ltd. is one of China's largest battery recycling and resource recovery companies, which possesses extensive operations across the battery value chain. The company is focused mostly on recycling lithium-ion batteries and producing precursor materials for new battery manufacturing.

- Fortum Battery Recycling has established a strong presence in Europe through its low-carbon hydrometallurgical recycling technology. In addition, the company offers end-to-end battery recycling services, including collection, dismantling, and material recovery, allowing it to maintain a leading position in this market.

- Glencore plc is a foundational player in this sector that has expanded its presence in the battery recycling sector with the help of strategic investments, partnerships, and acquisitions. The firm leads with extensive knowledge in metal processing and refining, and it focuses on recovering valuable battery materials and reintegrating them into the supply chain.

Here is a list of key players operating in the global market:

The Li-ion batteries recycling market hosts well-established recyclers, battery material specialists, and emerging circular-economy companies who are intensely competing to secure feedstock and expand processing capacity. Leading companies such as Umicore, Redwood Materials, Fortum, and GEM Co., Ltd. are focused mainly on capacity expansion, hydrometallurgical recycling technologies, and closed-loop supply chains. Partnerships with EV manufacturers, long-term battery collection agreements, investments in critical mineral recovery, and geographic expansion into high-growth regions are certain strategies opted for by the market participants. In March 2025, Panasonic Energy Co., Ltd. and Sumitomo Metal Mining announced a collaboration to recycle nickel for lithium-ion batteries with the main goal of advancing closed-loop circular economy initiatives. This partnership supports sustainable EV solutions by reusing critical materials and reducing reliance on mined resources.

Corporate Landscape of the Market:

Recent Developments

- In June 2026, American Battery Technology Co. announced the reinstatement of its USD 57 million DOE grant to build a USD 115 million lithium refinery in Tonopah Flats, Nevada, after winning its appeal against last year’s cancellation. The facility is expected to produce 5,000 metric tons of battery-grade lithium hydroxide annually.

- In March 2026, Lyten announced it had entered into a binding agreement to acquire Northvolt’s Revolt Ett battery recycling plant in Skellefteå, Sweden, and it will expand Lyten’s recycling capacity and support its mission of reducing mined mineral content in batteries.

- Report ID: 8625

- Published Date: Jun 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.