Graphite Anode for Lithium-Ion Battery (LIB) Market Outlook:

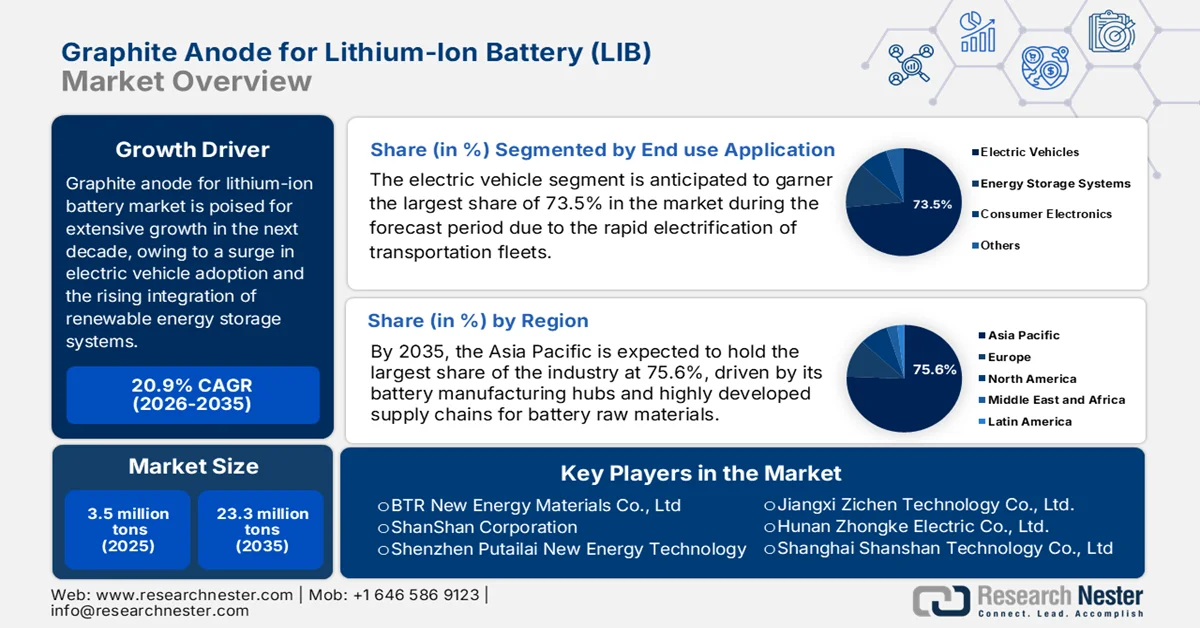

Graphite Anode for Lithium-Ion Battery Market size was valued at 3.5 million tons in 2025 and is anticipated to reach 23.3 million tons by the end of 2035, expanding at around 20.9% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of graphite anode for lithium-ion battery is estimated at 4.2 million tons.

The global graphite anode for lithium-ion battery market is projected for immense growth, effectively fueled by the exponential surge in electric vehicle adoption and the rising integration of renewable energy storage systems. The anode has exceptional electrical conductivity, stable structural integrity, and superior energy retention capabilities, due to which graphite is considered to be the definitive baseline material for battery manufacturing. According to the article published by the International Energy Agency (IEA) in 2025, worldwide battery demand reached almost 1 TWh in 2024, driven mainly by electric cars, which accounted for over 85% of EV battery use. The report also outlined that electric truck demand surged by 75%, which was led by growth in China and Europe, whereas the U.S. nearly matched Europe in demand due to larger battery sizes. In addition, EV battery demand is projected to exceed 3 TWh by 2030, wherein the electric trucks will triple their share and emerging graphite anode for LIB markets will double their contribution to global demand.

Global Electric Vehicle Battery Market Statistics and Demand Trends 2024-2030: EV Battery Demand, Regional Growth, and Industry Outlook

|

Metric |

2024 Value / Change |

|

Global battery demand (energy sector) |

>1 TWh |

|

EV battery demand |

>950 GWh |

|

Share of EV battery demand from electric cars |

>85% |

|

Growth in electric truck battery demand |

>75% |

|

Electric truck share of global EV battery demand |

3% |

|

Europe's electric truck battery demand growth |

25% |

|

China's EV battery demand growth |

>30% |

|

U.S. EV battery demand growth |

20% |

|

Emerging markets (excluding China) share of global battery demand |

5% |

|

Global EV battery demand outlook (2030) |

>3 TWh |

|

Electric truck share of EV battery demand (2030 forecast) |

>8% |

|

Emerging markets (excluding China) share of battery demand (2030 forecast) |

10% |

|

U.S. share of global battery demand (2024) |

13% |

|

China's share of global battery demand (2024) |

60% |

Source: IEA

Furthermore, the graphite anode for lithium-ion battery market dynamics is efficiently reshaped by a strategic shift toward synthetic graphite for its enhanced consistency and performance, balanced by a rising emphasis on sourcing eco-friendly natural graphite. To secure fragile supply chains, major economies are making investments in terms of localized processing infrastructure, thereby accelerating regional production hubs across North America and Europe. As per an article published by the U.S. Geological Survey (USGS), the U.S. apparent consumption of natural graphite was at historically high levels through 2025, which is supported by growing demand from the lithium-ion battery sector. Imports of natural and synthetic graphite battery anode materials increased to 43,400 tons during the first eight months of 2025, up from 28,100 tons during the same period in 2024, with China supplying 55%, followed by Indonesia being 31%, and the Republic of Korea 14%, thus making it suitable for standard graphite anode for lithium-ion battery (LIB) market growth.

Global Graphite Production, Mine Output, and Reserves 2024-2025: Country-Wise Supply Statistics and Resource Availability

|

Country |

Mine Production 2024 (t) |

Mine Production 2025 (t) |

Reserves (tons) |

|

Austria |

100 |

200 |

- |

|

Brazil |

58,000 |

65,000 |

74,000,000 |

|

Canada |

11,700 |

8,000 |

5,900,000 |

|

China |

1,270,000 |

1,400,000 |

100,000,000 |

|

Germany |

140 |

140 |

- |

|

India |

17,600 |

17,000 |

8,600,000 |

|

North Korea |

8,100 |

8,000 |

2,000,000 |

|

South Korea |

1,000 |

500 |

1,800,000 |

|

Madagascar |

85,000 |

80,000 |

27,000,000 |

|

Mexico |

706 |

740 |

3,100,000 |

|

Mozambique |

39,000 |

60,000 |

25,000,000 |

|

Norway |

5,340 |

6,600 |

600,000 |

|

Russia |

20,000 |

25,000 |

14,000,000 |

|

Sri Lanka |

3,000 |

3,200 |

1,500,000 |

|

Tanzania |

27,000 |

75,000 |

18,000,000 |

|

Turkey |

2,600 |

2,200 |

6,900,000 |

|

Ukraine |

900 |

800 |

- |

|

Vietnam |

500 |

500 |

9,700,000 |

|

World Total (rounded) |

1,550,000 |

1,800,000 |

310,000,000 |

Source: USGS

Key Graphite Anode for Lithium-Ion Battery (LIB) Market Insights Summary:

Regional Highlights:

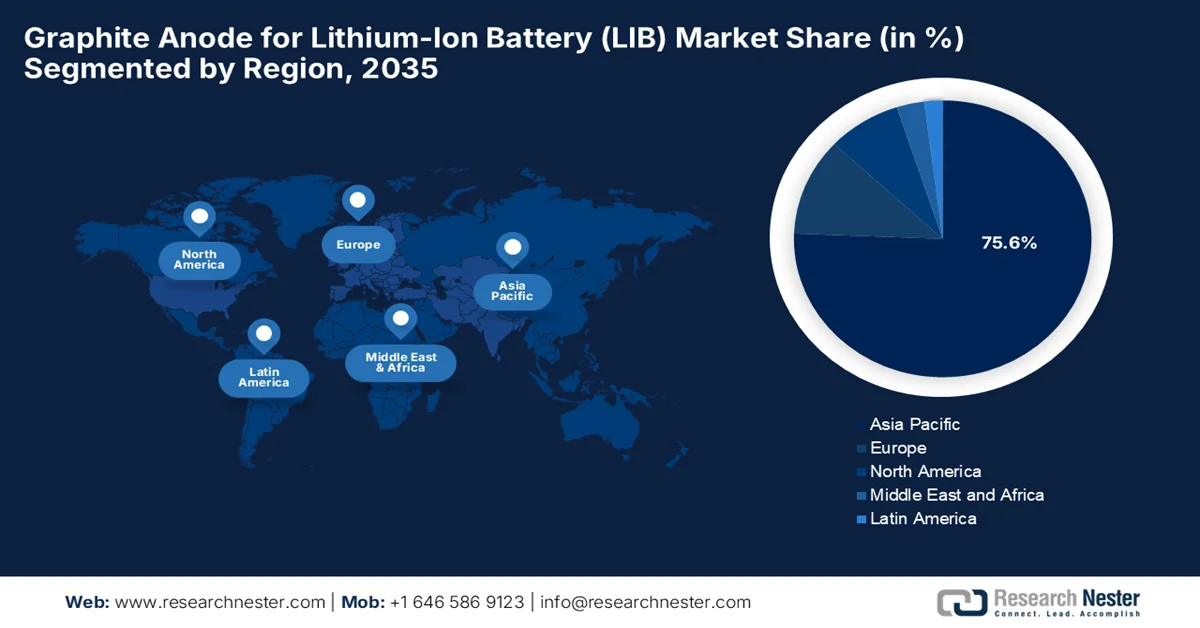

- The graphite anode for lithium-ion battery (LIB) market in Asia Pacific is projected to command 75.6% share by 2035, reinforced by large-scale battery manufacturing hubs, rapid EV production expansion, and established battery raw material supply chains

- Europe is expected to witness the fastest growth in the forecast period of 2026-2035, stimulated by aggressive decarbonization targets and the localized development of automotive gigafactories

Segment Insights:

- In the graphite anode for lithium-ion battery (LIB) market, the Electric Vehicle segment is forecast to account for 73.5% share by 2035, underpinned by accelerating transportation electrification, supportive ICE phase-out policies, and continuous charging infrastructure advancements

- The Synthetic Graphite segment is anticipated to secure a notable share by 2035, buoyed by its superior compatibility with high-energy-density lithium-ion batteries and growing adoption across electric vehicle applications

Key Growth Trends:

- Expansion of energy storage systems

- Increasing battery manufacturing capacity

Major Challenges:

- Supply chain concentration and geopolitical risk

- Environmental concerns and energy-intensive processing

Key Players: BTR New Energy Materials Co., Ltd. (China), ShanShan Corporation (China), Shenzhen Putailai New Energy Technology Co., Ltd. (China), Jiangxi Zichen Technology Co., Ltd. (China), Hunan Zhongke Electric Co., Ltd. (China), Shanghai Shanshan Technology Co., Ltd. (China), Shenzhen Kaijin New Energy Technology Co., Ltd. (China), Shenzhen Sinuo Industrial Development Co., Ltd. (China), Shenzhen XFH Technology Co., Ltd. (China), Resonac Holdings Corporation (Japan).

Global Graphite Anode for Lithium-Ion Battery (LIB) Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.5 million

- 2026 Market Size: USD 4.2 million

- Projected Market Size: USD 23.3 million by 2035

- Growth Forecasts: 20.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (75.6% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: China, United States, Japan, South Korea, Germany

- Emerging Countries: India, Canada, France, United Kingdom, Italy

Last updated on : 4 June, 2026

Graphite Anode for Lithium-Ion Battery (LIB) Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of energy storage systems: The emergence of renewable energy sources, such as solar and wind, is rapidly increasing the need for large-scale energy storage systems. Lithium-ion batteries are utilized for grid stabilization and energy management, driving demand for graphite anodes. Nations across the globe are making generous investments in energy security and renewable integration, due to which battery manufacturing requirements continue to rise. According to the article published by the International Energy Agency, global energy storage capacity needs to increase sixfold to 1,500 GW by 2030 to support the rapid expansion of renewable energy. Besides, the report also outlined that batteries are expected to account for around 90% of this growth, reaching 1,200 GW by 2030. Simultaneously, battery investments are projected to rise to USD 800 billion by 2030, while planned manufacturing capacity could increase nearly fourfold, thus strengthening the demand for graphite anodes used in energy storage applications.

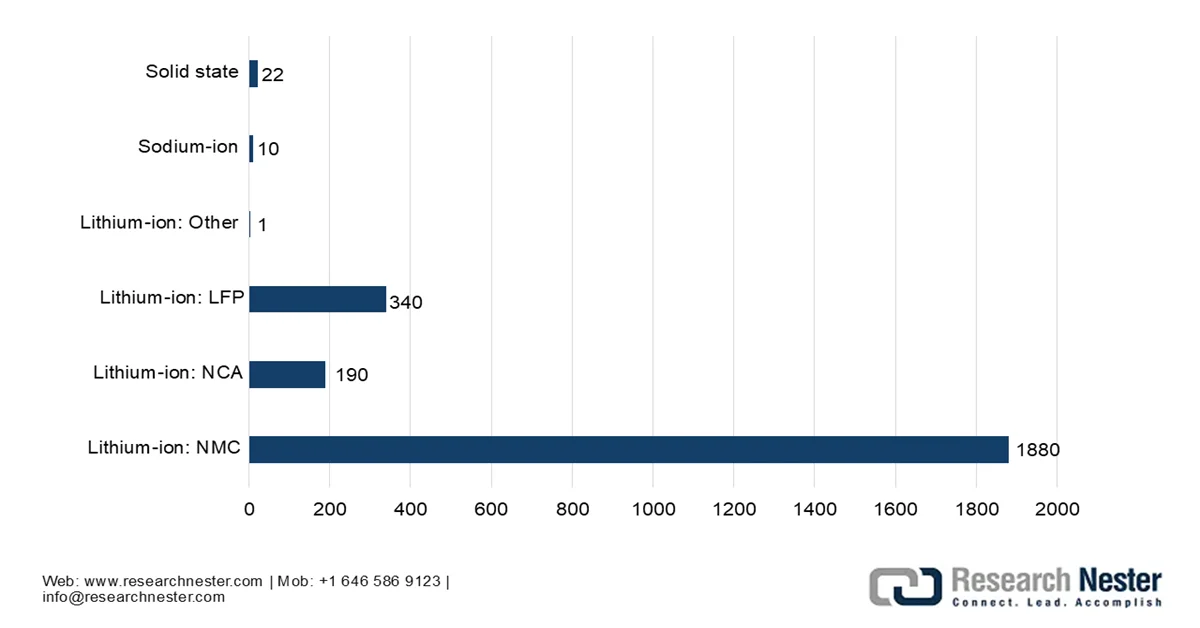

- Increasing battery manufacturing capacity: The worldwide investments in terms of battery gigafactories and lithium-ion battery production facilities are accelerating the graphite anode for lithium-ion battery market growth. In this context, manufacturers are expanding production capacities to meet rising demand from automotive, industrial, and consumer sectors. This expansion directly increases the consumption of graphite anode materials, thereby creating encouraging growth opportunities for suppliers across the battery value chain. For instance, in May 2025, the article published by WRI India revealed that India’s lithium-ion battery industry is projected to grow sharply, wherein the annual demand is rising from 10.8 GWh in 2022 to 160.3 GWh by 2030, reflecting rapid EV and energy storage expansion. Domestic manufacturing capacity is expected to reach 150 GWh annually by 2030, supported by policy incentives and private investments, thus strengthening the need for upstream materials such as graphite anodes in battery manufacturing.

Global Lithium-Ion Battery Manufacturing Capacity by Chemistry (GWh) - 2030 Forecast

Source: IEA

Challenges

- Supply chain concentration and geopolitical risk: The graphite anode for lithium-ion battery market is relying on China, which dominates mining, refining, spheroidization, and anode manufacturing. Therefore, this creates supply chain vulnerability for global battery producers, especially for those who are in North America and Europe. Any type of export restrictions, trade conflicts, or regulatory changes can impact material availability as well as pricing. Even when graphite is mined outside of China, most of the processing still occurs there, limiting diversification. Apart from this, governments are currently encouraging domestic supply chains, but building refining and anode capacity outside Asia requires high capital investment, long approval timelines, and technical expertise. This imbalance creates strategic risk for EV manufacturers and ultimately causes slow down to the global supply chain resilience development.

- Environmental concerns and energy-intensive processing: Graphite anode production, especially synthetic graphite, is extensively energy-intensive and environmentally challenging. The graphitization process requires very high temperatures, which leads to substantial carbon emissions and high electricity consumption. Natural graphite processing also involves chemical purification steps that can generate hazardous waste if not managed properly. In addition, the rising environmental regulations in Europe and North America are putting extra pressure on producers to adopt cleaner technologies. In this context, companies are being forced to make investments in terms of low-carbon production methods, renewable-powered facilities, and fluorine-free purification processes, whereas these cleaner alternatives often increase production costs and complexity. The sustainability standards keep tightening, due to which balancing cost with environmental compliance remains a major challenge for the graphite anode for lithium-ion battery market.

Graphite Anode for Lithium-Ion Battery (LIB) Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

20.9% |

|

Base Year Market Size (2025) |

3.5 million tons |

|

Forecast Year Market Size (2035) |

23.3 million tons |

|

Regional Scope |

|

Graphite Anode for Lithium-Ion Battery (LIB) Market Segmentation:

End use Application Segment Analysis

On the basis of end use application, the electric vehicle segment is anticipated to garner the largest share of 73.5% in the graphite anode for lithium-ion battery market during the forecast period. The segment’s dominance is largely attributable to the rapid electrification of transportation fleets, strong policy mandates targeting internal combustion engine phase-outs, and continuous improvements in charging infrastructure that enhance EV usability. In addition, the rising consumer preference for low-emission mobility solutions, coupled with automakers’ large-scale investment in EV platform development and battery localization strategies, also efficiently accelerates graphite anode consumption in this segment. For instance, in October 2023, LG Energy Solution and Toyota signed a long-term agreement under which LG will supply 20 GWh of high-nickel NCMA battery modules annually from 2025, produced at its Michigan facility. These modules will power Toyota’s new BEV models assembled in North America, including at Toyota Motor Manufacturing Kentucky.

Material Type Segment Analysis

In terms of material type, the synthetic graphite is anticipated to hold a notable share in the graphite anode for lithium-ion battery (LIB) market by the end of 2035. The segment’s growth is effectively propelled by the strong compatibility of synthetic graphite with high-energy-density lithium-ion battery chemistries, especially in terms of electric vehicle applications, where performance consistency and long cycle life are highly essential. Its superior purity, uniform particle structure, and controlled morphology enable better fast-charging capability and improved battery stability when compared to natural graphite. As per an article published by NIH in February 2023, the demand for synthetic graphite is expected to grow significantly along with lithium-ion battery expansion. The study also underscored that graphite demand will rise sharply, influenced by the accelerating deployment of EVs, grid storage systems, and clean energy technologies. Furthermore, it also notes that synthetic graphite is preferred in lithium-ion batteries due to its high purity and consistent performance.

Our in-depth analysis of the graphite anode for lithium-ion battery market includes the following segments:

|

Segment |

Subsegments |

|

End use Application |

|

|

Material Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Graphite Anode for Lithium-Ion Battery (LIB) Market - Regional Analysis

APAC Market Insights

The Asia Pacific graphite anode for lithium-ion battery market is poised for extensive growth, capturing around 75.6% during the forecast period. The region’s dominance is highly propelled by the strong presence of large-scale battery manufacturing hubs, the unprecedented expansion of electric vehicle production, and well-established supply chains for battery raw materials. In addition, supportive government policies, heightening investments in energy storage systems, and rising demand for consumer electronics further solidify the region’s leading position in the global graphite anode for LIB market. In February 2023, POSCO Chemical announced the expansion of its synthetic graphite anode material production by constructing a second plant in Pohang with a 10,000-ton annual capacity, thereby adding to its existing 8,000-ton facility. This combined 18,000-ton system will supply materials for about 470,000 EVs, strengthening Korea’s localization efforts and reducing reliance on imports.

The nation's exceptional vertical integration, massive gigafactory scale, and strong domestic electric vehicle adoption are allowing a massive growth of China graphite anode for lithium-ion battery (LIB) market. The country is considered to be the world's primary production and refining hub for active anode materials, and the graphite anode for LIB market is heavily characterized by an accelerating transition towards synthetic graphite. Based on the government data published in June 2024, China’s Ministry of Industry and Information Technology revised its lithium-ion battery guidelines to strengthen standardized management and promote high-quality development. These new rules are focused on ecological protection, safety, innovation, and discourage projects that expand capacity without improving technology or efficiency. Meanwhile, the output surpassed 282 GWh in the first four months of 2024, which is up 17.5% year-on-year, and thus the sector continues to show strong growth momentum under these updated standards.

In India, the graphite anode for lithium-ion battery (LIB) market is being catalyzed by the national push toward clean mobility and the buildout of domestic cell manufacturing ecosystems. The federal initiatives, such as the advanced chemistry cell (ACC) production-linked incentive scheme, and the graphite anode for LIB market are making a shift from a heavy reliance on imported active materials to localized processing hubs. As per an article published by the Institute for Energy Economics & Financial Analysis in January 2026, the ACC PLI scheme, which was launched in October 2021 to build 50 GWh of domestic battery manufacturing capacity, has achieved only 2.8% (1.4 GWh) of its target as of October 2025, with Ola Electric being the sole contributor to commissioned capacity. The execution has been delayed due to supply chain constraints, strict domestic value addition requirements, limited technical expertise, and dependence on foreign specialists for equipment installation, thus making it suitable for bolstering the country’s graphite anode for LIB market growth.

India Graphite Shipment Statistics (2024): Import-Export Data for Artificial Graphite, Carbonaceous Materials, and Battery Anode Supply Chain Inputs

|

Commodity |

Flow |

Trade (USD) |

Weight (kg) |

Notes |

|

Graphite; artificial |

Import |

57,348,867 |

65,420,881 |

Primary lithium-ion anode precursor (high relevance) |

|

Graphite; artificial |

Export |

23,686,497 |

11,095,433 |

Refined synthetic graphite exports (anode/electrode use) |

|

Graphite; colloidal or semi-colloidal |

Import |

3,902,381 |

1,505,179 |

Specialty carbon dispersion (limited battery use) |

|

Graphite; colloidal or semi-colloidal |

Export |

15,203 |

29,062 |

Minimal export volume |

|

Carbonaceous pastes (electrodes/furnace linings) |

Import |

14,166,730 |

— |

Industrial electrode binders (some battery adjacency) |

|

Carbonaceous pastes (electrodes/furnace linings) |

Export |

11,255,446 |

15,831,375 |

Electrode manufacturing materials |

|

Graphite/carbon preparations (semi-manufactures) |

Import |

65,885,268 |

43,198,542 |

Strong battery & electrode supply chain input |

|

Graphite/carbon preparations (semi-manufactures) |

Export |

19,535,673 |

10,086,150 |

Processed carbon materials for industrial use |

Source: UN Data

Europe Market Insights

Europe graphite anode for lithium-ion battery market is anticipated to grow at the fastest rate from 2026 to 2035. The region’s growth is mainly propelled by the continent's aggressive decarbonization targets and the localized buildout of automotive gigafactories. With a main goal to mitigate acute geopolitical vulnerabilities and avoid over-reliance on foreign supply chains, the regional graphite anode for LIB market is heavily shaped by strict regulatory frameworks, which mandate high environmental sustainability standards and localized sourcing quotas. The GR4FITE3 project is funded under the region’s Climate, Energy, and Mobility program with a total budget of USD 5.9 million, of which the region contributes USD 5.2 million. The project’s timeframe is from May 2023 to April 2027, and coordinated by RINA Consulting in Italy, it focuses on building a sustainable end-to-end supply chain for graphite in lithium-ion battery anodes, hence denoting a positive outlook for the region’s growth.

The presence of major domestic premium automakers, whose large-scale vehicle electrification roadmaps require an immediate and highly secure pipeline of battery active materials, is the main factor boosting the growth of Germany graphite anode for lithium-ion battery market. The country’s landscape has catalyzed deep collaborative partnerships between automotive OEMs, chemical giants, and specialized materials processors to pioneer next-generation silicon-graphite composite anodes. The EU Battery Regulation 2023/1542, which replaced the 2006 Battery Directive, became directly applicable in Germany from February 18, 2024. It establishes a proper legal framework covering the entire life cycle of batteries. In addition, this act introduces stricter rules on substance restrictions, sustainable product design, recycled material quotas, and corporate due diligence obligations for raw materials such as lithium, cobalt, nickel, and graphite.

The UK graphite anode for lithium-ion battery market is growing due to the presence of targeted automotive electrification goals and the urgent need to establish a localized battery supply chain. To maintain tariff-free trade access to the region’s markets under strict post-Brexit rules of origin requirements, the domestic industry is focusing on securing localized active anode materials. Based on the government data published in December 2023, the UK Battery Strategy identifies batteries as a key technology for net zero, in which the demand is fueled by EVs and energy storage, while noting that production is currently concentrated in East Asia. It sets out the UK’s goal to build a competitive domestic battery supply chain supported by innovation, manufacturing scale-up, and critical minerals access. Therefore, to achieve this, the government has committed more than USD 2.6 billion in funding along with investments in gigafactories, R&D, and recycling infrastructure.

North America Market Insights

In North America, the graphite anode for lithium-ion battery (LIB) market is growing significantly on account of massive federal legislative support aimed at building a fully localized clean energy supply chain. The region’s policy environment has triggered an unprecedented surge of investments into regional processing hubs, by focusing mainly on expanding both advanced synthetic graphite manufacturing facilities and eco-friendly natural graphite purification plants. The region’s market is also fueled by intense technical innovation, with leading companies pioneering high-capacity silicon-graphite composite anodes to significantly elevate energy density. In February 2024, Panasonic Energy signed a seven-year offtake agreement with Nouveau Monde Graphite in Quebec to secure natural graphite for EV battery anodes, along with an initial USD 25 million investment and plans for an additional USD 150 million with co-investors. Under NMG’s mine-to-battery-material model, graphite will be sourced from the Matawinie Mine and processed at Bécancour, thereby ensuring a vertically integrated and carbon-neutral supply chain.

The rapid growth of domestic EV manufacturing, increasing deployment of grid-scale energy storage systems, are certain drivers boosting the U.S. graphite anode for lithium-ion battery market. Simultaneously, the collaboration between automotive OEMs, battery manufacturers, and materials companies is accelerating the development of high-performance anode materials, which include synthetic graphite and silicon-enhanced blends, to meet the performance demands of next-generation electric vehicles. In March 2025, the article published by the U.S. Energy Information Administration stated that in 2024, the U.S. surpassed 26 GW of cumulative utility-scale battery storage capacity, with 10.4 GW added that year, making batteries the second-largest capacity addition after solar. This expansion underscores the growing role of battery storage in balancing renewable energy and strengthening grid reliability, thus increasing the demand for graphite anodes.

The country’s rich natural resource endowments and proactive federal support are driving the growth of graphite anode for lithium-ion battery market in Canada. Simultaneously, the federal and provincial initiatives, such as the Canadian Critical Minerals Strategy, have accelerated domestic processing investments, drawing interest from global manufacturers who are looking for ethically sourced materials. In May 2026, Libra Energy’s maiden drill program at its Stimson Project in Ontario revealed a significant graphite discovery by intersecting 4.7% graphitic carbon over 14.7 meters, with samples reaching up to 10.45% Cg. This finding confirms a graphite-bearing system within metasedimentary units, along with zinc mineralization, and highlights strong infrastructure advantages near Cochrane. Hence, such instances strengthen the country’s position in the global landscape, encouraging more players to establish their footprint in Canada.

Key Graphite Anode for Lithium-Ion Battery (LIB) Market Players:

- BTR New Energy Materials Co., Ltd. (China)

- ShanShan Corporation (China)

- Shenzhen Putailai New Energy Technology Co., Ltd. (China)

- Jiangxi Zichen Technology Co., Ltd. (China)

- Hunan Zhongke Electric Co., Ltd. (China)

- Shanghai Shanshan Technology Co., Ltd. (China)

- Shenzhen Kaijin New Energy Technology Co., Ltd. (China)

- Shenzhen Sinuo Industrial Development Co., Ltd. (China)

- Shenzhen XFH Technology Co., Ltd. (China)

- Resonac Holdings Corporation (Japan)

- Mitsubishi Chemical Group Corporation (Japan)

- Tokai Carbon Co., Ltd. (Japan)

- Nippon Carbon Co., Ltd. (Japan)

- JFE Chemical Corporation (Japan)

- SGL Carbon SE (Germany)

- Imerys S.A. (France)

- Syrah Resources Limited (Australia)

- POSCO Future M Co., Ltd. (South Korea)

- HEG Limited (India)

- Graphite India Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BTR New Energy Materials Co., Ltd. has registered itself as the predominant leader in graphite anode materials for lithium-ion batteries, with a dominant position in synthetic graphite used in electric vehicles. The company operates large-scale integrated production facilities in China and maintains strong supply relationships with leading battery manufacturers such as CATL and BYD.

- ShanShan Corporation is one of the earliest and most established players in the graphite anode for LIB market industry that consists of a fully integrated value chain from raw material processing to finished graphite anode products. The company produces both natural and synthetic graphite materials and has strong long-term relationships with major battery producers in China and internationally.

- Shenzhen Putailai New Energy Technology Co., Ltd. is yet another foundational pillar of this sector that has significant expertise in upstream graphite processing and downstream anode manufacturing. In addition, the firm benefits from strong synergies between its equipment manufacturing, coating technology, and anode material production businesses.

- Resonac Holdings Corporation, formerly Showa Denko Materials, is a leading Japan-based producer of high-performance synthetic graphite anodes. The company is best known for its advanced material engineering capabilities and strong focus on quality, purity, and consistency, which makes its products highly suitable for premium EV and electronics applications.

- POSCO Future M Co., Ltd. consists of growing capabilities in graphite anode production along with its strong cathode materials business. Material. The company is building a more secure and vertically integrated battery materials value chain, and it is highly focused on supplying high-quality graphite anodes for EV batteries.

Here is a list of key players operating in the global graphite anode for lithium-ion battery (LIB) market:

The graphite anode for lithium-ion battery market is an extremely competitive landscape dominated by China-based manufacturers, which benefit from integrated supply chains, large-scale synthetic graphite production, and strong relationships with EV battery makers. Japan-based companies such as Mitsubishi Chemical, Resonac, and Tokai Carbon compete in terms of high-purity materials and advanced process technologies. Simultaneously, Europe-specific players such as SGL Carbon and Imerys emphasize sustainability and niche high-performance applications. Growth strategies adopted by the leading players in the graphite anode for lithium-ion battery (LIB) market include capacity expansion, vertical integration, and technological innovation in synthetic and silicon-enhanced graphites. For instance, in May 2026, EcoGraf Limited was granted an India patent for its EcoGraf HFfree® purification technology, thereby strengthening its position in emerging ex-China battery supply chains. This patent is valid until 2041, and it covers applications in producing battery anode material, high-purity graphite, and recycling lithium-ion battery anodes.

Corporate Landscape of the Graphite Anode for Lithium-Ion Battery (LIB) Market:

Recent Developments

- In March 2026, Vianode signed a term sheet to supply 8,000 tons of synthetic graphite from its Norwegian facility, Via ONE, to a North America battery technology company for grid energy storage systems. The agreement includes a roadmap to expand beyond 10,000 tons annually once its Canada-based plant, Via TWO, becomes operational.

- In January 2026, Lomiko Metals completed the extraction of a 200‑ton bulk graphite sample at La Loutre, which is now being processed at Corem in Quebec to validate pilot‑scale upgrading into battery‑grade anode material. In addition, the company will settle USD 90,000 in debts by issuing 818,181 shares at USD 0.10, subject to TSX Venture Exchange approval.

- Report ID: 8606

- Published Date: Jun 04, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.