Battery Coatings Market Outlook:

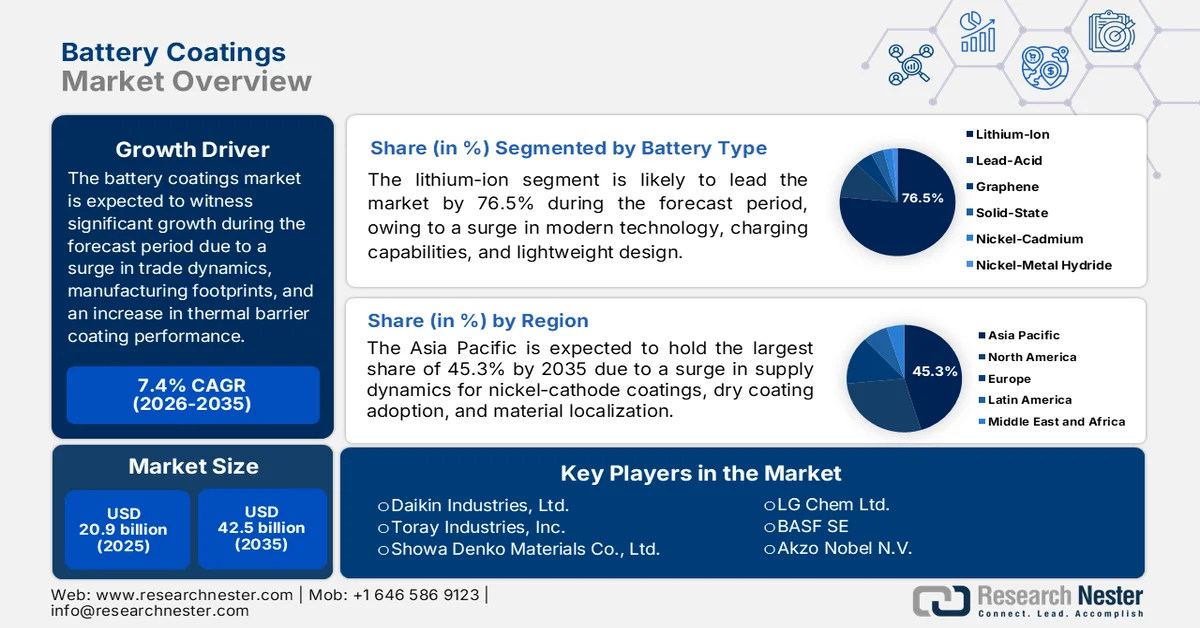

Battery Coatings Market size was valued at USD 20.9 billion in 2025 and is projected to cross USD 42.5 billion by the end of 2035, expanding at more than 7.4% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of battery coatings is estimated at USD 22.4 billion.

The worldwide battery coatings market is readily shaped by different macroeconomic and structural factors, including raw material pricing volatility, an increase in the demand for thermal barrier coating performance, trade dynamics, regional manufacturing footprints across different regions, and electric vehicle battery solutions. According to official statistics published by the IEA Organization in 2025, the battery requirement in the energy industry, both for storage applications and electric vehicle batteries, has reached the milestone of 1 TWh as of 2024. In addition, the demand was massively fueled by growth in electric vehicle sales, due to which batteries surged to more than 950 GWh, demonstrating roughly 25% more in 2023. Besides, electric cars continue to remain the ultimate factor behind the electric vehicle battery demand, accounting for over 85%, thereby positively impacting the market upliftment.

Region-Wise Electric Vehicle Battery Demand, 2018-2024

|

Year |

Europe |

China |

U.S. |

Other EMDEs |

Other AEs |

|

2018 |

7.0% |

63.0% |

18.0% |

2.0% |

10.0% |

|

2019 |

13.0% |

59.0% |

15.0% |

2.0% |

12.0% |

|

2020 |

22.0% |

50.0% |

11.0% |

2.0% |

14.0% |

|

2021 |

19.0% |

55.0% |

11.0% |

2.0% |

13.0% |

|

2022 |

16.0% |

57.0% |

12.0% |

2.0% |

12.0% |

|

2023 |

16.0% |

56.0% |

13.0% |

3.0% |

12.0% |

|

2024 |

13.0% |

59.0% |

13.0% |

5.0% |

11.0% |

Source: IEA Organization

Furthermore, the presence of laser-driven coatings curing technologies, electrode graded coating architectures, and in-situ coating repair systems are certain trends that are responsible for driving the market globally. As stated in an article published by NLM in April 2024, diamond, a third-generation semiconductor and ultra-wideband material, constitutes a cubic structure of 0.3 nm, along with 0.1 nm of bond length, and 109°28′ bond angle. In addition, this material is further characterized by increased hardness of 10 on the Moh’s scale, as well as thermal conductivity of 1.2 × 10−6 K−1 and high transmission in the UV-to-microwave range between 0.2 to 8,000 μm. Therefore, with all these properties, diamond has emerged as a suitable micro-fabrication material for enabling progress in laser-processing technology, which in turn, is bolstering the market exposure.

Key Battery Coatings Market Insights Summary:

Regional Highlights:

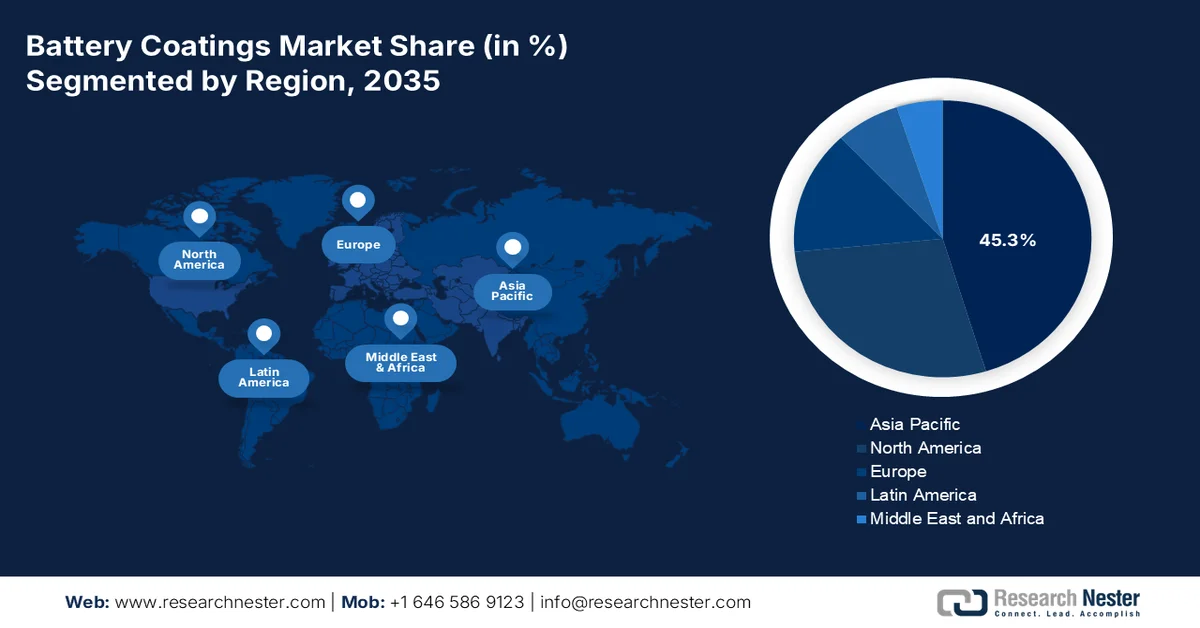

- Asia Pacific battery coatings market is anticipated to capture a dominant 45.3% share by 2035, stimulated by established supply chains, rising high-nickel cathode coatings adoption, and increasing EV battery manufacturing activities

- Europe is projected to witness the fastest growth throughout 2026–2035, accelerated by climate-neutrality targets, localized battery manufacturing, and expanding utility-scale battery storage deployment

Segment Insights:

- The lithium-ion segment in the battery coatings market is expected to account for a leading 76.5% share by 2035, driven by high energy density, rapid charging capabilities, lightweight design, and expanding electric vehicle battery deployment

- The transportation sub-segment is poised to secure the second-largest share during 2026–2035, attributed to the accelerating transition toward electric vehicles and the reduction of carbon emissions

Key Growth Trends:

- Second-life battery refurbishment

- Port infrastructure and marine electrification

Major Challenges:

- Regulatory fragmentation and compliance complexity

- Accelerated material obsolescence cycles

Key Players: Arkema SA (France), Solvay SA (Belgium), Asahi Kasei Corporation (Japan), PPG Industries, Inc. (U.S.), 3M Company (U.S.), Mitsubishi Chemical Corporation (Japan), Ube Industries Ltd. (Japan), Tanaka Chemical Corporation (Japan), Daikin Industries, Ltd. (Japan), Toray Industries, Inc. (Japan), Showa Denko Materials Co., Ltd. (Japan), Sumitomo Chemical Co., Ltd. (Japan), SK Innovation Co., Ltd. (South Korea), LG Chem Ltd. (South Korea), BASF SE (Germany), Akzo Nobel N.V. (Netherlands), Henkel AG & Co. KGaA (Germany), SGL Carbon SE (Germany), Targray Technology International Inc. (Canada), Nano One Materials Corp. (Canada), Axalta Coating Systems Ltd. (U.S.), Jotun (Norway), Xaar (UK).

Global Battery Coatings Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 20.9 billion

- 2026 Market Size: USD 22.4 billion

- Projected Market Size: USD 42.5 billion by 2035

- Growth Forecasts: 7.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.3% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: China, United States, South Korea, Japan, Germany

- Emerging Countries: India, Poland, Hungary, Indonesia, Vietnam

Last updated on : 13 May, 2026

Battery Coatings Market - Growth Drivers and Challenges

Growth Drivers

- Second-life battery refurbishment: The proliferation of retired electric vehicle batteries significantly entering stationary storage applications has created a distinctive coating demand, which is positively driving the battery coatings market globally. According to official statistics published by NLM in April 2024, by the end of 2025, more than 800,000 metric tons of electric vehicle batteries increased, which was followed by a surge in end-of-life (EoL), especially when a battery usually reaches 70% to 80% of its original storage capacity. Additionally, this 80% EoL criterion was usually established for nickel and cadmium batteries. Meanwhile, lithium-ion batteries comprise an energy between 240 and 300 Wh/kg, along with 200 to 950 W/kg of power and a long-lasting lifetime of 6 to 15 years, thus fueling the market growth.

- Port infrastructure and marine electrification: The maritime industry represents a rapidly expanding demand source with distinct coating requirements, which is also driving the market demand. As stated in a data report published by the Department of Energy in December 2024, the Action Plan for Maritime Energy and Emissions Innovation demonstrated that large-scale ocean-going vessels represent an estimated 68% of overall greenhouse gas emissions from bunkered fuel, particularly in the U.S. Besides, globally, 92.6% of vessels burn traditional fuels, and almost half of vessels on order or under construction tend to accept low-greenhouse gas emissions. Meanwhile, the U.S.-specific flagged vessels per maritime industrial segment are readily proliferating the market exposure globally.

U.S.-Flagged and Foreign-Flagged Vessels Per Maritime Industry, 2024

|

Vessel Type |

Vessels |

Nautical Miles Travelled |

Energy Consumed |

Stack Greenhouse Gas Emissions |

|

Ocean-Going Vessels |

0.3% |

16.0% |

66.0% |

68.0% |

|

Harbor Craft |

0.3% |

5.0% |

8.0% |

8.0% |

|

Department of Defense |

0.03% |

5.0% |

7.0% |

7.0% |

|

Non-Commercial Vessels |

99.0% |

73.0% |

18.0% |

17.0% |

|

Total |

11.1 million |

7,074 million |

1,935 trillion Btu |

81 mmt CO2e |

Source: Department of Energy

- Underground safety and mining electrification: Heavy mining equipment manufacturers are increasingly shifting diesel-powered underground vehicles to battery-electric propulsion to eliminate exhaust emissions in confined tunnels. As per a data report published by the IEEE Power and Energy Society Organization in March 2024, in terms of mining electrification, the industry of silicon carbide (SiC) and Gallium nitride (GaN) power devices was worth USD 1 billion as of 2022. In addition, it has been estimated that the overall industry is poised to expand to USD 4.3 billion by the end of 2028, accounting for a yearly growth rate of 33.7%. Therefore, based on this, coating formulators have created sulfur-scavenging layers that tend to neutralize electrolyte decomposition products, thereby denoting an optimistic outlook for the battery coatings market expansion.

Electronvolt Levels Analysis of Mining Solids, 2024

|

Solids |

Electronvolt Level (eV) |

|

Germanium (Ge) |

0.6 |

|

Silicon (Si) |

1.1 |

|

Gallium arsenide (GaAr) |

1.4 |

|

Silicon carbide (SiC) |

3.3 |

|

Gallium nitride (GaN) |

3.4 |

|

Gallium oxide (GaO) |

5.0 |

|

Dimond (C) |

5.5 |

|

Aluminum nitride (AlN) |

6.2 |

|

Glass |

More than 4.4 |

Source: IEEE Power and Energy Society Organization

Challenges

- Regulatory fragmentation and compliance complexity: The battery coatings market operates within a rapidly tightening and geographically fragmented regulatory web. For instance, Europe's Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework imposes strict limits on certain fluoropolymers and solvents commonly used in coating formulations. Meanwhile, China's increasingly stringent volatile organic compound (VOC) regulations differ significantly from North America's Toxic Substances Control Act (TSCA) rules. Likewise, South Korea and Japan enforce their own unique hazardous substance lists. Besides, for a global coating supplier, this means maintaining multiple formulation variants for the same functional product, increasing R&D costs, complicating inventory management, and raising the risk of compliance violations at customs checkpoints.

- Accelerated material obsolescence cycles: Battery technology is evolving faster than coating validation protocols, with solid-state batteries, lithium-sulfur chemistries, and sodium-ion systems each demanding fundamentally different coating interfaces, thermal management profiles, and adhesion properties. A coating optimized for the present nickel-manganese-cobalt lithium-ion cell has become functionally obsolete within a single product generation cycle. Besides, research institutions and startups announce breakthrough chemistries quarterly, yet coating suppliers cannot realistically parallel-develop solutions for every emerging platform due to resource constraints. This creates a perpetual chasing-the-target syndrome, which, in turn, is causing a hindrance in the market growth.

Battery Coatings Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.4% |

|

Base Year Market Size (2025) |

USD 20.9 billion |

|

Forecast Year Market Size (2035) |

USD 42.5 billion |

|

Regional Scope |

|

Battery Coatings Market Segmentation:

Battery Type Segment Analysis

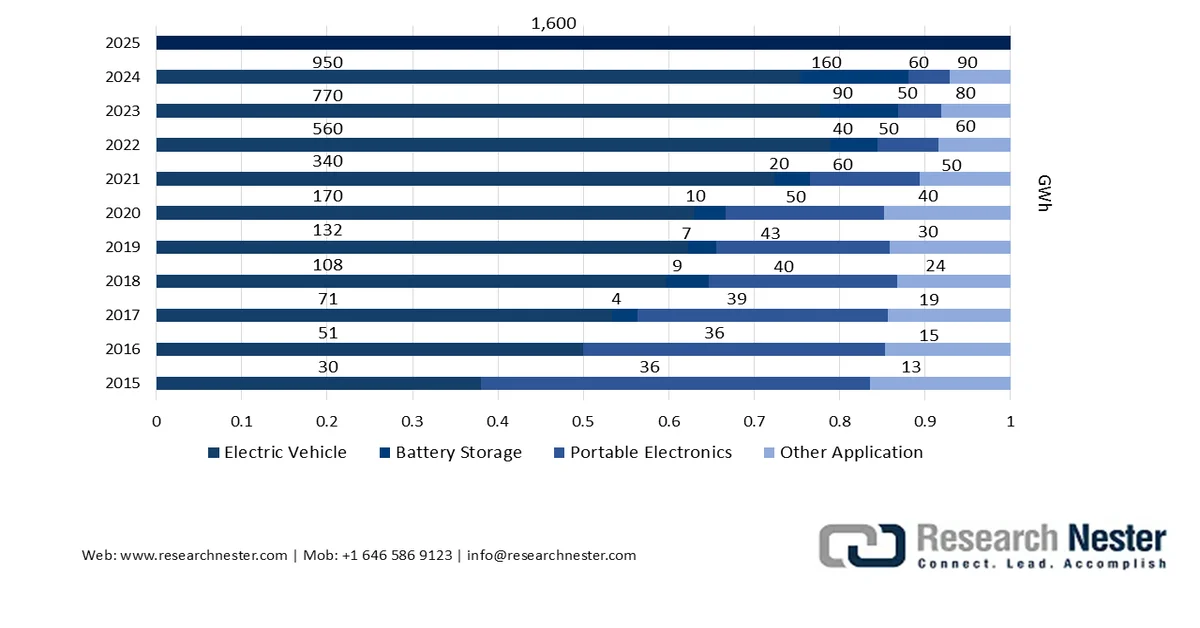

Based on the battery type, the lithium-ion segment is anticipated to account for the largest share of 76.5% in the battery coatings market by the end of 2035. The segment’s upliftment is primarily driven by its importance for modernized technology, owing to its high energy density, long-lasting cycle life, rapid charging capabilities, and lightweight design. According to official statistics published by the IEA Organization in February 2026, the worldwide lithium-ion battery industry has surpassed USD 150 billion as of 2025, demonstrating an increase of more than 20% from 2024. Regarding this growth, electric vehicles readily account for over 70% of overall lithium-ion battery deployment. Additionally, this is followed by battery energy storage at more than 15%, indicating the role of batteries in offering flexibility in power systems, thereby bolstering the segment’s growth.

Lithium-Ion Battery Deployment Analysis by Application, 2015-2025

Source: IEA Organization

End use Industry Segment Analysis

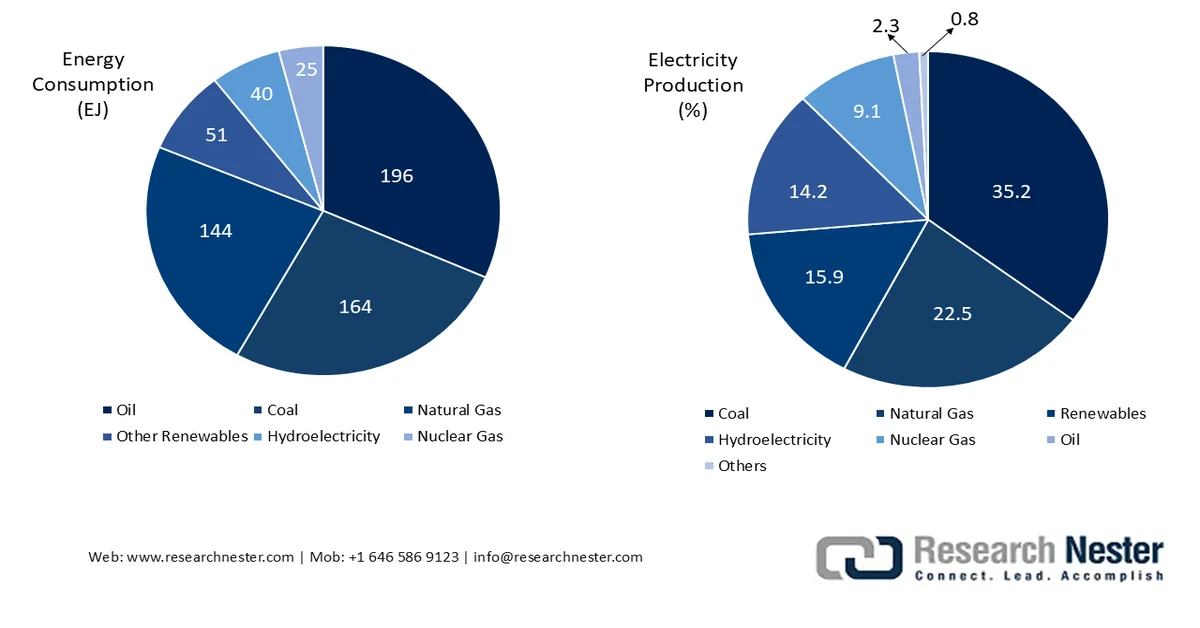

During the forecast period, the transportation sub-segment, part of the end use industry segment, is projected to garner the second-largest share in the market. The sub-segment’s growth is highly fueled by the aspect of enabling the global shift to electric vehicles and diminishing carbon emissions. As stated in an article published by Renewable and Sustainable Energy Reviews in January 2026, the transportation industry significantly contributes an estimated 8.7 gigatons of carbon dioxide equivalent in direct greenhouse gas emissions, demonstrating almost 23% of the worldwide energy-based carbon dioxide emissions. Besides, road vehicles cater for 70% of these emissions, while rail, maritime, and aviation account for 1%, 11%, and 12%, respectively. Moreover, the industry is readily utilizing different energy sources, thus enhancing the market demand globally.

Total Energy Consumption and Electricity Production by the Transport Industry, 2023

Source: Renewable and Sustainable Energy Reviews

Battery Component Segment Analysis

The electrode coating sub-segment, which is part of the battery component segment, is expected to grab the third-largest share in the market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by its usability in arc welding for producing sound welds by shielding the molten pool from atmospheric contamination, either oxygen or nitrogen, improving mechanical properties, and stabilizing the electrical arc. As per the 2026 Royal Society of Chemistry article, 6% of lithium-ion battery waste tends to get recycled, and the remaining ends up in landfills, which poses the risk of environmental contamination and metal toxicity. Therefore, to overcome this, pyrometallurgy has the capability to ensure massive metal recovery, with 100% leaching efficiencies that can be gained for elements such as nickel, cobalt, and lithium, thus enabling waste-specific carbon electrodes for sustainable batteries.

Our in-depth analysis of the battery coatings includes the following segments:

|

Segment |

Subsegments |

|

Battery Type |

|

|

End use Industry |

|

|

Battery Component |

|

|

Coating Methods |

|

|

Technology Type |

|

|

Material Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Battery Coatings Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the battery coatings market is anticipated to account for the highest share of 45.3% by the end of 2035. The market’s upliftment in the region is primarily attributed to an established supply chain, an increase in high-nickel cathode coatings, the adoption of dry coating, the localization of precursor materials, and suitable compliance spending. According to official statistics published by Invest Korea in 2022, Korea is considered the world’s second-largest battery producer, readily accounting for 21% of electric vehicle batteries. Based on this, the country comprises competitive manufacturers, pertaining to finished battery products, and a focus on high-performance in the materials segment, such as cathode and anode materials. Besides, the country has witnessed an upsurge in electric vehicle sales, increasing from 46,909 units as of 2020 to 101,112 units and further 162,987 units in 2022, thus positively driving the market growth in the overall region.

Electric Vehicle Battery Production Capacity in Korea, Japan, and China, 2021-2030

|

Year |

Korea |

Japan |

China |

|

2021 |

21.0% |

7.0% |

69.0% |

|

2025 |

18.0% |

4.0% |

70.0% |

|

2030 |

20.0% |

5.0% |

63.0% |

Source: Invest Korea

The battery coatings market in China is growing significantly, owing to scale-driven electric vehicle sales, an increase in coating materials, suitable government policies for supporting the growth, technological localization, and industrial integration. As stated in an article published by Transportation Research Part A: Policy and Practice in December 2024, the energy capacity of the power battery pack in the country accounted for USD 439.2/kWh, with the maximum subsidy allocated for battery electric vehicles. Besides, the subsidy standard for these particular vehicles varied from USD 8,784.3 in 2009, which is followed by USD 7,905.8 in 2015, USD 6,441.8 in 2017, USD 7,320.2 in 2018, USD 3,660.1 in 2019, and USD 3,294.1 in 2021, and USD 1,844.7 in 2022. Therefore, with this continuous subsidy allowance, the market is gradually expanding in the overall country.

The aspects of premium quality positioning, an increase in the demand for high-nickel cathode, a surge in research and development in next-generation battery, the transition of regulatory-based low-carbon, and the localization of the supply chain are certain factors that are bolstering the market in Japan. The market’s growth in the country depends on the industrial size, which was worth USD 62.5 million as of 2025. Based on this, the market is projected to be valued at USD 75.6 million by the end of 2026, followed by USD 342.2 million by the end of the forecast duration. Besides, as per a data report published by the International Institute for Sustainable Development in February 2026, the country is largely responsible for 18% of the global nickel value chain distribution, thus denoting an optimistic outlook for the market growth and upliftment.

Europe Market Insights

Europe in the battery coatings market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by strong climate-neutrality targets, localized battery manufacturing, the existence of private and public partnerships, raw materials recycling, and domestic battery cell production. According to official statistics published by SolarPowerEurope in January 2026, the region has successfully installed 27.1 GWh of the newest battery capacity as of 2025, marking the 12th consecutive record year for battery storage deployment. Regarding this, 55% of the total capacity derived from utility-scale systems, which confirmed large-scale storage as the ultimate engine of the regional industry growth. Moreover, the regional battery manufacturing reached 252 GWh of nominal cell production capacity, thus enhancing the market.

Battery Storage Deployment in Europe, 2019-2025

|

Year |

Deployment Growth |

|

2020-2021 |

145.0% |

|

2021-2022 |

130.0% |

|

2022-2023 |

73.0% |

|

2023-2024 |

23.0% |

|

2024-2025 |

45.0% |

Source: SolarPowerEurope

The battery coatings market in Germany is gaining increased traction, owing to the presence of the largest automotive manufacturing industry, extensive chemical industrial infrastructure, strong government funding for battery material innovation, and generous funding for battery projects. Based on the government estimate published by the ITA in August 2025, there has been an increase in domestic automation exports from USD 955 billion as of 2022 to more than USD 1 trillion in 2023, which later diminished to USD 991 billion in 2024. Despite this slight downfall, the 2024 U.S.-based advanced manufacturing exports to the country amounted to USD 37 billion. In addition, the export valuation from the U.S. to the country was worth USD 43 billion, thereby making it extremely suitable for developing and expanding the market.

The expansion in the gigafactory facility, supported by generous funding opportunities, an increase in battery supply chain, the existence of abundant solar energy for low-carbon coating production, sustainability, and focus on decarbonization are a few trends that are responsible for enhancing the battery coatings market in Spain. As per an article published by the UN Trade and Development in November 2023, the Europe Commission accepted 2 State aid schemes in the country that totaled USD 2.2 billion for supporting suitable investments in green technology equipment and battery production under the Green Deal Industrial Plan. Meanwhile, the USD 984.4 million scheme, approved in May 2023, focused on suitable battery production that involved manufacturing batteries, along with necessary raw materials and components, thus boosting the market development.

North America Market Insights

North America in the battery coating market is projected to witness suitable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by strong electric vehicle manufacturing localization policies, the successful establishment of regional gigafactory networks, production of battery components, the presence of automotive OEMs, and the increased demand for consistent coating material supplies. According to official statistics published by the CSIS Organization in April 2026, the overall battery production in the U.S. increased by almost 140% by the end of 2025. Based on this growth, there has been the generous provision of investments for battery projects, ranging from USD 2.3 million to USD 17,814 million. Besides, the continuous supply of coated textile fabric within the region is also boosting the market exposure.

2024 Coated Textile Fabric Export and Import Analysis in North America

|

Countries/Component |

Export (USD) |

Import (USD) |

|

U.S. |

50.3 million |

112.0 million |

|

Canada |

14.2 million |

14.1 million |

|

Mexico |

213,000 |

37.4 million |

|

Honduras |

28,900 |

1.2 million |

|

Guatemala |

27,800 |

280,000 |

|

Panama |

23,900 |

182,000 |

|

El Salvador |

17,000 |

289,000 |

|

Bahamas |

15,500 |

112,000 |

Source: OEC

The battery coatings market in the U.S. is gaining increased exposure, owing to massive federal investment in domestic battery supply chains, robust foreign entity of concern (FEOC) restrictions, increased focus on lithium-ion cell safety and thermal management, along with qualified domestic downstream consumer requirements. As stated in an article published by the Battery Council International in March 2025, the battery industry in the country is continuously thriving, with its yearly direct and downstream economic activity creating USD 10 trillion in domestic economic output. In addition, this industrial upliftment has resulted in more than 54 million employment opportunities in the country that are reliant on batteries. Besides, the industry effectively powers 21% of the domestic economy, thereby denoting an optimistic outlook for the market expansion.

Battery Industry Powering the USD 10 Trillion U.S. Economy, 2024

Source: Battery Council International

The tactical innovation fund to support clean technology manufacturing, an escalation in electric vehicle manufacturing localization, collaborative research and development networks and innovative partnerships, and suitable alignment with the net zero accelerator are a few factors that are driving the battery coatings market in Canada. Based on an article published by the Government of Canada in April 2026, the Parliamentary Secretary to the Minister of Industry proclaimed USD 10.6 million for 14 electric vehicle charging infrastructure programs across the country. This generous funding is expected to ensure that these projects will install more than 1,600 chargers across the overall country. In addition, the Plug’n Drive is projected to continue providing a cross-country electric vehicle test drive tour with another USD 1.1 million in funding, thus enhancing the market exposure.

Key Battery Coatings Market Players:

- Arkema SA (France)

- Solvay SA (Belgium)

- Asahi Kasei Corporation (Japan)

- PPG Industries, Inc. (U.S.)

- 3M Company (U.S.)

- Mitsubishi Chemical Corporation (Japan)

- Ube Industries Ltd. (Japan)

- Tanaka Chemical Corporation (Japan)

- Daikin Industries, Ltd. (Japan)

- Toray Industries, Inc. (Japan)

- Showa Denko Materials Co., Ltd. (Japan)

- Sumitomo Chemical Co., Ltd. (Japan)

- SK Innovation Co., Ltd. (South Korea)

- LG Chem Ltd. (South Korea)

- BASF SE (Germany)

- Akzo Nobel N.V. (Netherlands)

- Henkel AG & Co. KGaA (Germany)

- SGL Carbon SE (Germany)

- Targray Technology International Inc. (Canada)

- Nano One Materials Corp. (Canada)

- Axalta Coating Systems Ltd. (U.S.)

- Jotun (Norway)

- Xaar (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Arkema SA has established itself as a leading supplier of specialty fluoropolymers, particularly PVDF, which is essential for both electrode binders and separator coatings in lithium-ion batteries. The company has aggressively expanded its production footprint in North America to support the region's rapidly growing EV gigafactory ecosystem.

- Solvay SA leverages its deep expertise in advanced fluorinated materials to provide high-purity coating solutions that enhance battery safety and thermal stability. The company has directed significant research investments toward developing alternative binder systems that reduce dependency on legacy supply chains while maintaining electrochemical performance.

- Asahi Kasei Corporation combines its heritage in separator technology with specialized ceramic coating capabilities, offering integrated solutions for battery thermal runaway prevention. The company has focused on improving coating uniformity at high production speeds, addressing a critical manufacturing challenge for mass-scale battery production.

- PPG Industries, Inc. applies its century-long experience in industrial coatings to the battery sector, developing multifunctional layers that protect against corrosion, manage heat dissipation, and improve electrical insulation. The company has prioritized waterborne and solvent-free coating formulations to align with tightening global environmental regulations on volatile organic compounds.

- 3M Company utilizes its core competency in material science and adhesives to create specialized coating formulations that strengthen the bond between electrode particles and current collectors. The company has also pioneered ceramic-based thermal barrier coatings designed to contain and prevent thermal propagation within battery modules.

Here is a list of key players operating in the global market:

The battery coatings market is characterized by intense competition among chemical manufacturers, with key players concentrated in Japan, the U.S., and Europe. Strategic initiatives have increasingly focused on vertical integration and capacity expansion to meet surging EV demand. Moreover, Japan-based companies, such as Asahi Kasei, Mitsubishi, and Ube, have leveraged their expertise in specialty polymers, particularly PVDF, to secure long-term supply agreements with battery giants such as Panasonic and CATL. Besides, in February 2025, Arkema expanded its PVDF capacity by 15%, particularly in North America. This was possible by generously investing almost USD 20 million and readily aligned with the organizational strategy to enhance its worldwide PVDF footprint, thereby making it suitable for fueling the battery coatings industry globally.

Corporate Landscape of the Battery Coatings Market:

Recent Developments

- In October 2025, Axalta Coating Systems Ltd. introduced 2 advanced products- Alesta® e-PRO FG Black and Alesta® e-PRO Dielectric Gray, and reinforeced its commitment to performance, innovation, and technical service in energy storage solutions and the automotive industry value chain.

- In June 2025, Jotun unveiled new powder coating technologies for safeguarding batteries by investing in electrification that has created a growing industry for batteries, especially for electric vehicles and energy storage systems.

- In June 2025, Xaar effectively strengthened its positive in electric vehicle battery coatings by partnering with Sokan New Materials Group, marking a suitable approach of transition from conventional film coating materials.

- Report ID: 8561

- Published Date: May 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Battery Coatings Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.