Biopolymer Coatings Market Outlook:

Biopolymer Coatings Market size was valued at USD 38 billion in 2025 and is expected to reach USD 118 billion by the end of 2035, expanding at a CAGR of 12% during the forecast period, i.e., 2026-2035. In 2026, the industry size of biopolymer coatings is assessed at USD 42.6 billion.

The key biopolymer coatings market drivers in 2025 were the development of strategic agendas by key players to transition to biopolymers and offer substitutes for petrochemical products to critical end use industries, thereby building a circular economy. The potent way to achieve this transition is to gradually phase out fossil carbon with renewable alternatives, including biomass. The key players are diversifying their feedstock portfolio to render renewable carbon along with fossil-based carbon. This is leading the way from a prevalent conservative market perspective. In particular, biomass use for coating production has increased in the past decade and is expected to continue to surge in supply of bio-based polymers.

In 2022, although the conventional fossil fuels provided 80% of the worldwide energy supply, biofuels maintained a steady share of 9%. According to the World Bioenergy Association, Renewable energy sources, biofuels contributed 89 Exajoules (EJ) of the overall 622 EJ energy supply worldwide, marking a 30% spike over the last 10 years. In 2021, the biomass supply was 54 EJ, wherein solid biomass, such as pellets and wood chips, held for 85% of the share. In terms of geography, Europe was the top wood pellet producer and consumer, while Vietnam emerged as the key exporter to South Korea and Japan and witnessed a 33% growth in production. In 2023, the cumulative biomass supply was 56 EJ: 83% contribution from solid biomass, about 9% from liquid biofuels, and 3% from biogas (last two attaining their highest shares in the past five years).

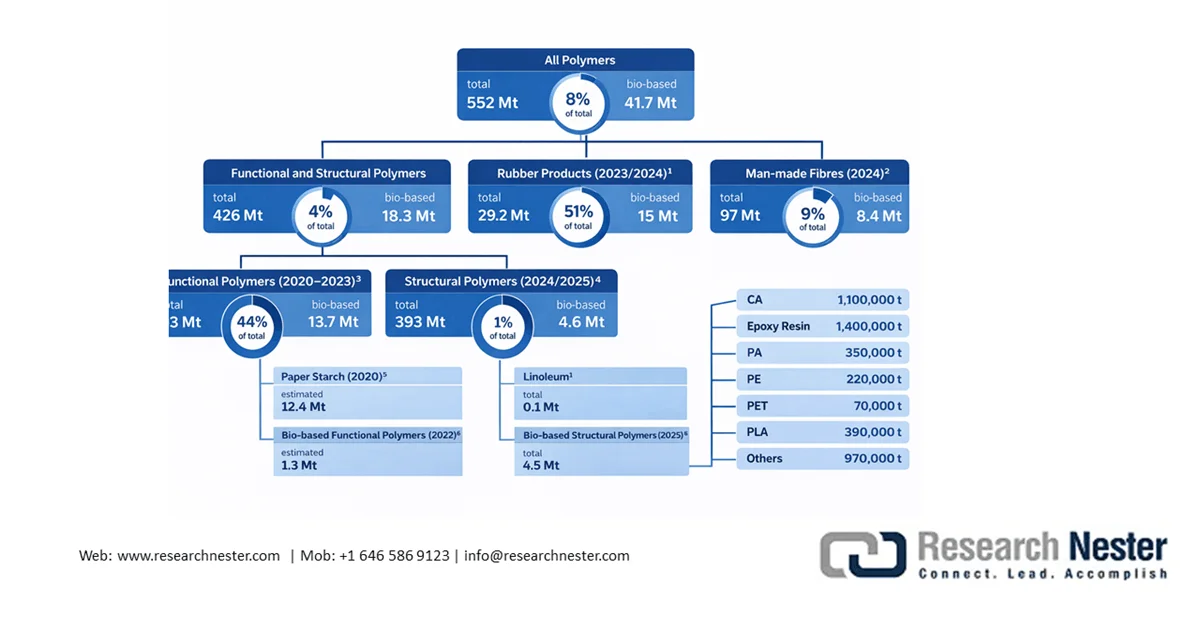

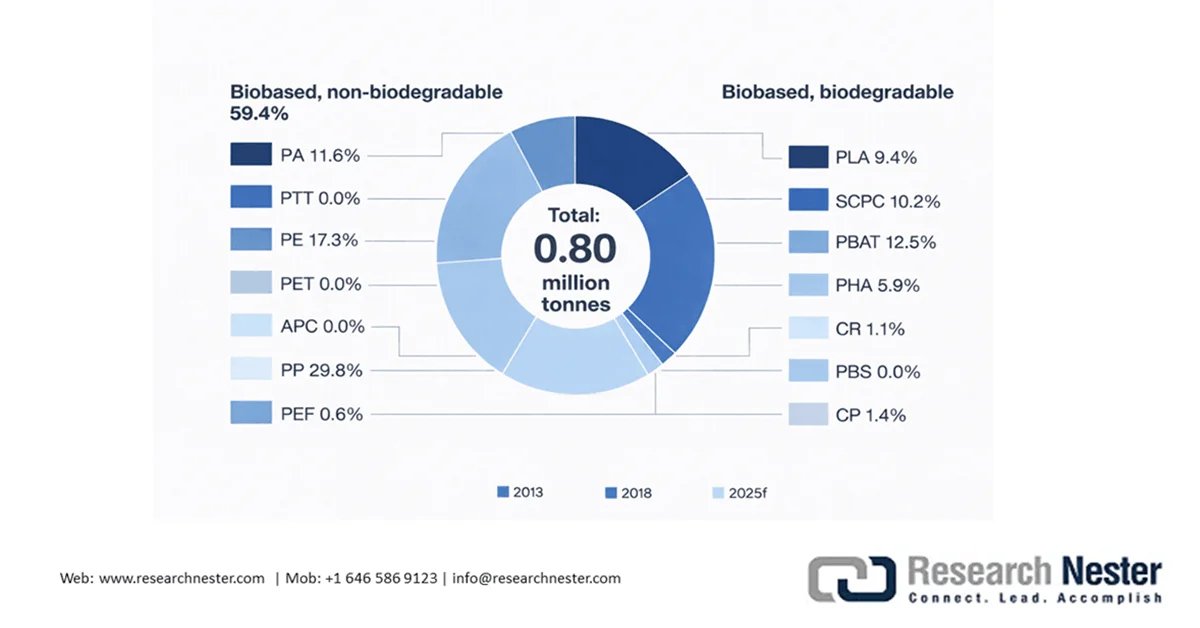

Worldwide Polymers & Bio-based Shares, 2020-2025

Source: Nova Institute EU

The biopolymer coatings market comprises structural and functional polymers made from natural rubber and industrially produced fibers. Bio‑based structural polymers are developed form bio‑based linoleum and structural plastic mass, which cumulatively amount to 4.6 million tons. As per the Nova Institute, EU report from February 2026, the bio‑based functional polymers consist of paper starch and bio‑based functional polymers, totaling 13.7 million tons. These two groups amounted to 18 million tons of bio‑based structural and functional polymers. Furthermore, 8.4 million tons of man‑made fibers and 15 million tons of rubber products are typically made from bio‑based resources, 9 % and 51 %, respectively. In 2025, functional biobased polymers (including coatings, adhesives, cosmetics, etc.) contributed 17% of the overall biopolymer coatings market.

2025 was a rewarding year for biobased polymers and is projected to register a CAGR of 11 % by 2030, with an average capacity utilization of 86 %. Overall, non-biodegradable polymers have higher utilization rates and greater installed capacities than bio-based and biodegradable polymers. 42 % of the installed capacities are biodegradable polymers, and 58 % are bio-based non-biodegradable polymers. Bio-based non-biodegradable polymers have 90% average utilization (10% CAGR), and bio-based biodegradable polymers have 81% average utilization rate (11% CAGR). In 2025, bio‑based building blocks production capacity was 5.8 million tons, denoting 15 % surge (746,000 t/a) between 2024 and 2025. This is driven by high adoption of epichlorohydrin (ECH), L‑lactic acid (L-LA), 1,4‑butanediol (1,4-BDO), 1,5-Pentamethylenediamine (DN5), succinic acid (SA), and naphtha.

Key Biopolymer Coatings Market Insights Summary:

Regional Highlights:

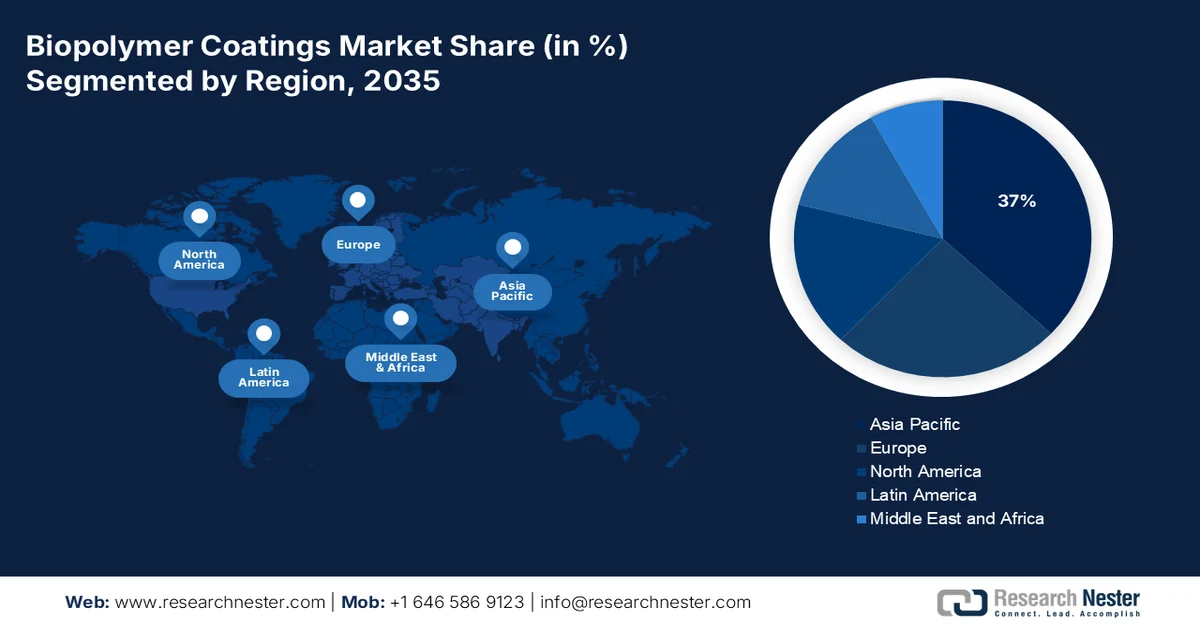

- Asia Pacific is expected to dominate the biopolymer coatings market with a 37% share by 2035, attributed to the strong regional trade and production of natural polymers

- North America is projected to hold a 21% share in the forecast period, impelled by increasing government initiatives supporting bioenergy infrastructure and biomass production

Segment Insights:

- The soy protein product segment in the biopolymer coatings market is projected to account for a 35% share by 2035, propelled by the surge in global soy cultivation and rising biomass generation

- The agriculture segment is anticipated to capture a significant share by 2035, driven by increasing adoption of sustainable seed coatings enhancing germination and reducing microplastic usage

Key Growth Trends:

- Growing emphasis on biopolymer coating research and development

- Production capacity expansion

Major Challenges:

- Technical challenges with biopolymer coating usage

- Distribution and commercial barrier limitations

Key Players: AG (GeBASF SE (Germany), AkzoNobel N.V. (Netherlands), Arkema S.A. (France), Solenis (United States), EcoSynthetix Inc. (Canada), Evonik Industries rmany).

Global Biopolymer Coatings Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 38 billion

- 2026 Market Size: USD 42.6 billion

- Projected Market Size: USD 118 billion by 2035

- Growth Forecasts: 12% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (37% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Brazil, Germany, Japan

- Emerging Countries: India, South Korea, Canada, Spain, Italy

Last updated on : 21 April, 2026

Biopolymer Coatings Market - Growth Drivers and Challenges

Growth Drivers

- Growing emphasis on biopolymer coating research and development: Biopolymer coatings market are being considered a promising alternative to conventional petroleum-based coatings owing to their versatile properties and eco-friendly nature. These can be tailored to customized end use requirements by mixing additives, functional molecules, or reinforcing agents, thereby expanding their adoption across diverse fields such as biomedical devices, food packaging, electronic components, and textiles. Researchers have been extensively focused on innovating biopolymer coatings using chitosan, starch, cellulose derivatives, and proteins (casein and gelatin). Apart from traditional biopolymer coatings usage as protective barriers against UV radiation, moisture, oxygen, and fungal growth, they have been utilized for controlled release of active compounds, biocompatibility, and antimicrobial activity, thus creating opportunities in biomedical applications.

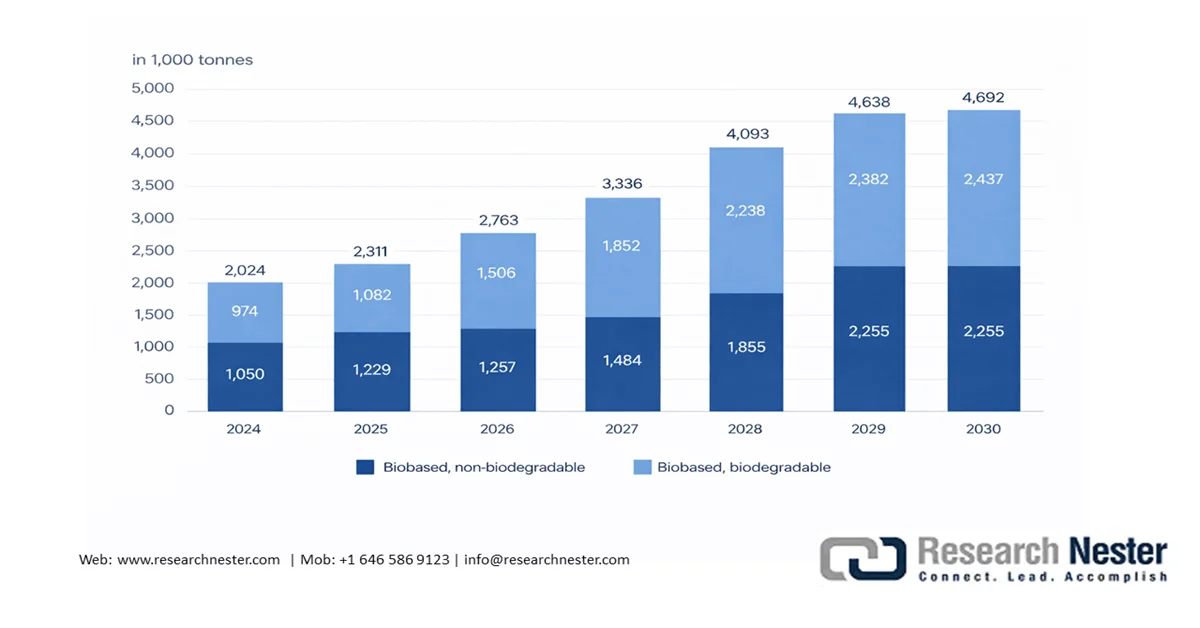

Ongoing R&D and government funding are aimed at enhancing the mechanical strength, stability, and durability of biopolymer films. In June 2024, the Food and Agricultural Organization of the United Nations (FAO) launched the FAOSTAT domain to streamline bioenergy feedstock availability. Moreover, scalable and affordable production methods are expected to be developed by the FAO to facilitate the widespread commercialization of biopolymer coatings and films. Similarly, Omics Online in 2023 published research on spraying, spin coating, dip coating, and brush coating technologies. - Production capacity expansion: The biopolymer coatings market has found application in industries such as agriculture, consumer goods, and automobiles. The European Bioplastics predicts that, given the high market demand, the biobased plastics production capacity globally will double to 4.69 million tons by 2030 from 2.31 million tons in 2025, denoting the gradual integration of advanced manufacturing technologies. Bioplastic alternatives are available for approximately all regular plastic materials and coatings. Due to a robust biobased and biodegradable polymer development, such as polyhydroxyalkanoates (PHA), polypropylene (bioPP), and polylactic acid (PLA), the production capacities is set to uptick considerably in the next 5 years. Of the 2025 4.5 million tons of bio-based polymers produced, cellulose acetate (CA) with a 50% bio-based content and epoxy resins with a 45% bio-based content accounted for 25 % and 30 %, of the bio-based production.

Global Production Capacities of Biobased Plastics 2025-2030

Source: European Bioplastics

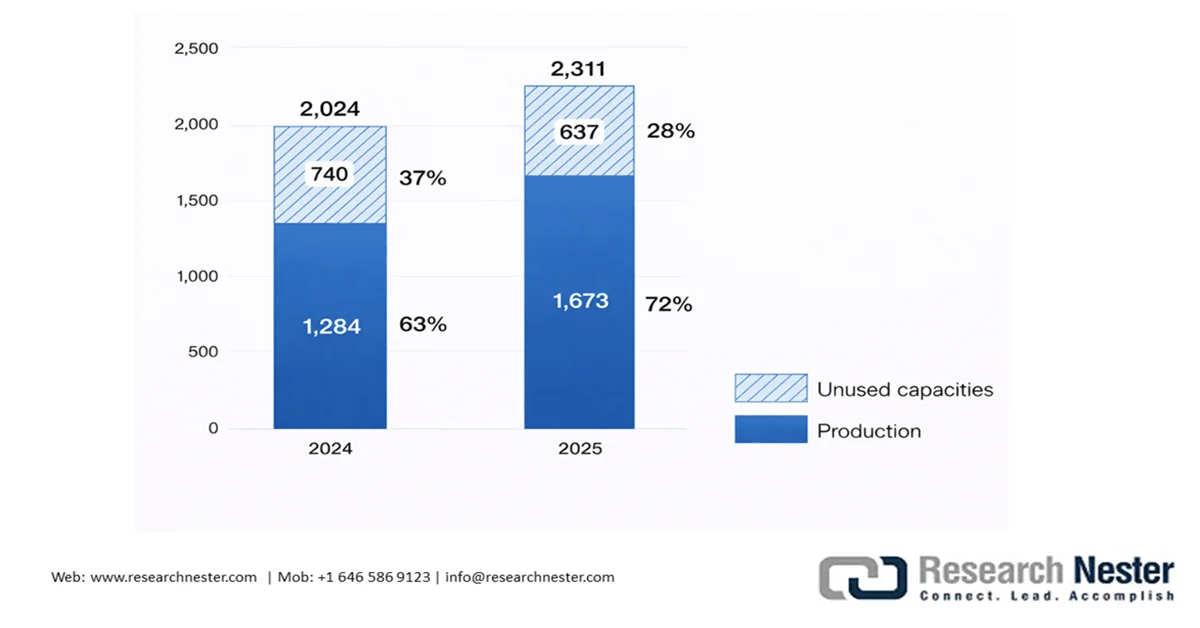

Global Utilization Rates of Biobased Plastics 2024 Vs 2025, in 1,000 Tons

Source: European Bioplastics

Challenges

- Technical challenges with biopolymer coating usage: In subtropical and tropical regions with ambient humidity, weakens hydrophilic coatings efficacy with are typically made from proteins and polysaccharides. These hydrophilic coatings absorbs moisture, thus damaging film integrity and increasing microbial growth. Despite the fact that lipid-based coatings offer superior moisture resistance, they are prone to cracking. Furthermore, constrained availability of application methods and low-tech preparation is a key biopolymer coatings market roadblock. Many countries are producing non-urban supplies that lack atomization equipment access, continuous coating lines, and vacuum drying.

- Distribution and commercial barrier limitations: Biopolymer coatings market’s commercial penetration is limited owing to lack of necessary infrastructure and cost constraints. Functional additives, including cross-linkers and essential oils is regarded as expensive or has poor availability in rural areas. Moreover, the lack of cold storage, particularly in tropical climates, limits overall longevity. The widespread availability of traditional plastic coatings at comparative low prices is hindering biopolymer coatings market adoption.

Biopolymer Coatings Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12% |

|

Base Year Market Size (2025) |

USD 38 billion |

|

Forecast Year Market Size (2035) |

USD 118 billion |

|

Regional Scope |

|

Biopolymer Coatings Market Segmentation:

Product Type Segment Analysis

The soy protein product segment is projected to garner a share of 35% in the biopolymer coatings market during the assessment period, owing to the staggering growth in soy cultivation and the subsequent high volume biomass generation. The current boom in conscious eating habits and advent of vegetarianism fostered plant‐based protein cultivation. The National Library of Medicine 2025 publication disclosed that in 2023-2024, soy was grown in 137.10 million hectares worldwide. Brazil had the biggest area of 45.8 million hectares. 153 million tons of seeds were reaped, which yielded 3.3 t per hectare. The U.S. stood at the second position and cultivated 113.27 million tons of seeds, which was 3.4 t per hectare. Then comes Paraguay (48.10 million metric tons), Argentina (48.10 million metric tons), China (20.84 million metric tons), Canada (6.98 million metric tons), India (11.88 million metric tons), and Russia (6.8 million metric tons). The U.S., Brazil, Paraguay, and Argentina cumulatively contribute 91.7% of all soybean production.

Application Segment Analysis

The agriculture segment is anticipated to account for a significant revenue share by the end of 2035. Biopolymer seed coatings have proven pivotal in minimizing crop contamination, enhancing seed germination, and improving beneficial microbial species concentration in soil. The use of carbon-based materials sourced from natural resources such as plant biomass, algae, and fungi have showcased promising effects on agriculture. Furthermore, some biopolymers, except for biocompatible ones, can offer antibacterial and antifungal advantages. As per the Agricultural Science & Technology, biopolymer coatings market in terms of germination rates, outperform synthetic polymers (90%) and uncoated seeds (85%), reaching up to 97.4%. Another key factor contributing to the segment growth the rising focus on limiting microplastics with the help of alternative materials. Regular seed film coatings or adhesive polymers typically used are styrene acrylate copolymer dispersion, polyvinyl acetate dispersion, and ethylene acrylic copolymer dispersion.

Our in-depth analysis of the biopolymer coatings market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Product Type |

|

|

Functional Property |

|

|

Application |

|

|

End use |

|

|

Coating Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Biopolymer Coatings Market - Regional Analysis

APAC Market Insights

Asia Pacific has been dominating the worldwide trade of natural polymers and accounted for 37% of biopolymer coating production in 2025. In 2024, natural polymer worldwide trade was USD 3.78 billion, denoting a slight decline by 5.41% from 2023, wherein the trade was USD 4 billion. In 2024, China (USD 1.09 billion) and South Korea (USD 263 million) were among the top five suppliers of natural polymers. In the span of the last five years, the trade grew at a CAGR of 7.44%. Four countries accounted for 87% of the overall coatings demand in terms of value and volume: China held 60+% of regional value and 59+% of regional volume, India (12% of regional value; 18% of regional volume), Japan (8% of regional value; 6% of regional volume), and South Korea (6% of regional value and 4% of regional volume).

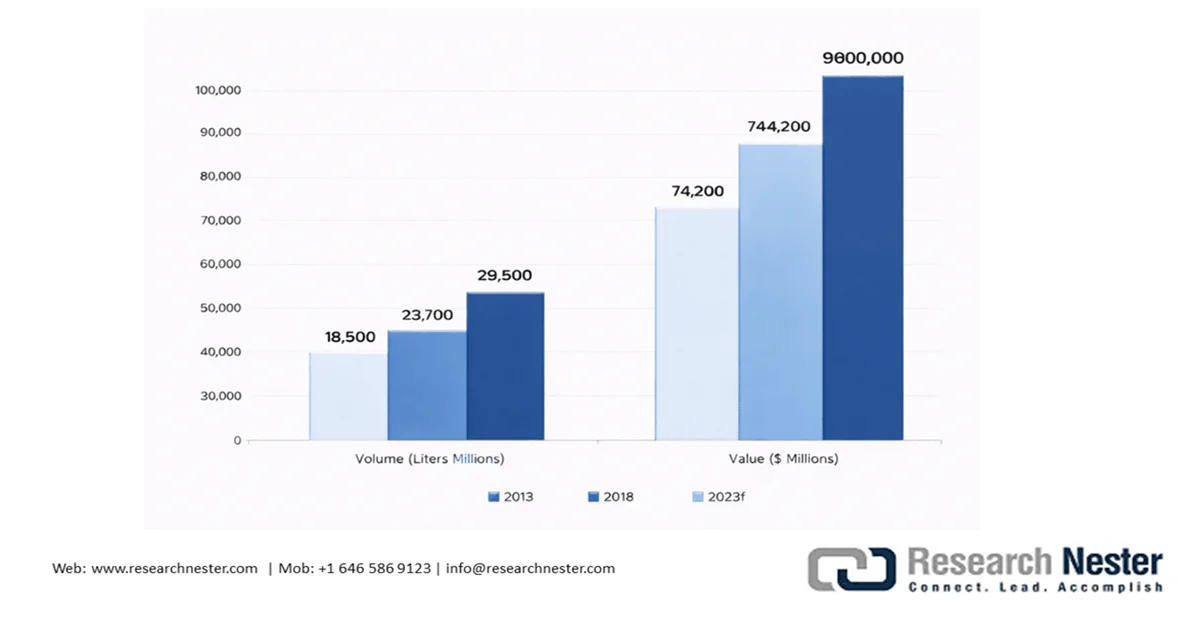

APAC Coating Market, 2013-2030F

Source: American Coatings Association

China, with about 60% of the Asia Pacific coatings volume, has emerged as a vital producer and consumer in the region. As per the American Coating Association 2024 report, China has roughly 10,000 coating manufacturers, and the leading 100 companies account for 50% of the volume, and roughly 70% is OEM (top 1,000 manufacturers were responsible 80% of the total coatings produced in China). Moreover, China has 4,000 powder coating companies, with smaller entities producing under 1,000 kilograms/annum. Evidently, consolidation (already underway among the joint venture and multinational producers) is expected to elevate operations, abetted by increasing raw material prices and evolving regulatory requirements. China’s revenue in 2018 constituted USD 44.5 billion of Asia Pacific cumulative sales of USD 74.2 billion and 14.2 billion liters of the region’s 23.7 billion liters.

India biopolymer coatings market is set to capture a staggering share by the end of 2035, owing to the growing government influence in product development and innovation. As per the January 2024 update by the Department of Science and Technology, the Institute of Advanced Study in Science and Technology (IASST) developed a novel biopolymer xerogel film (in August 2022) made from sodium alginate, chitosan, and mushrooms. This one-of-a-kind biopolymer nanocomposite coating innovation was synthesized using a green fabrication method, with a banana corm nanomaterial for cross-linking biopolymers.

North America Market Insights

North America was the second largest region in terms of biopolymer coating production and held a share of 17% in 2025 and by 2030 the region is expected to grow its share by 4%. In terms of natural polymer trade, the U.S. was among the top five suppliers in 2024 and held an export value of USD 344 million. Canada biopolymer coatings market dynamic is shaped by the growing government influence in establishing bioenergy infrastructure to boost biomass production in the country.

The U.S. biopolymer coatings market is driven by the robust feedstock production capacity. As of November 2025, the annual capacity of densified biomass fuel producing facilities was 13,429,015 tons per year. The monthly data gathered by the U.S. Energy Information Administration (EIA) included 74 operating manufacturers. They had an overall production capacity annually of 13.03 million tons and employed roughly 2,435 full-time individuals. The monthly respondents in November 2025 procured 1.6 million tons of biomass raw material and generated 0.9 million tons of sold 0.97 million tons (both in volume terms) of densified biomass fuel. Densified biomass domestic sales in November 2025 were 0.17 million tons, which averaged at USD 239.40 per ton, whereas exports were 0.80 million tons, which averaged at USD 203.33 per ton during the same timeline.

Europe Market Insights

Europe is projected to hold a prominent biopolymer coatings market share during the forecast period, due to the expanding PEF capacities. Furthermore, Europe is likely to proliferate its existing share by 4% by 2030. In 2025, Europe garnered a 14% share in installed capacities for PA, PBAT, and SCPC. EU bioeconomy is flourishing and is a 5% contributor to the GDP, employing 17.5 million in 2023. Biobased chemicals (excluding biofuels) employed 123.46k people in 2023. Even though the policy landscape for bio-based polymers in Europe is continuously evolving, it is anticipated to present noteworthy opportunities for players with respect to other regions.

In Europe, bioplastics growth primarily was driven by surging additional polyethylene (bioPE), polypropylene (bioPP), and polyhydroxyalkanoates (PHA) capacities. In 2025, has an average of 73% production capacity Bioplastics are used for an increasing variety of applications, ranging from packaging and fibers to consumer goods, automotive, and agricultural products. Packaging emerged as the dominating segment for bioplastics with 41.3% (0.95 million tons) in 2025 of the cumulative bioplastics biopolymer coatings market. The automotive & transport application has expanded to 0.24 million tons, accounting for 10.3% of applications.

Europe Production Capacities of Biobased Plastics 2030, By Material Type

Source: European Bioplastics

Key Biopolymer Coatings Market Players:

- BASF SE (Germany)

- AkzoNobel N.V. (Netherlands)

- Arkema S.A. (France)

- Solenis (United States)

- EcoSynthetix Inc. (Canada)

- Evonik Industries AG (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BASF SE is a global leader in chemical manufacturing and a frontrunner in the development of biopolymer coatings. The company leverages its highly integrated value chain, spanning renewable feedstocks to advanced polymer formulations, to deliver scalable bio-based coating solutions. Its portfolio includes biodegradable and compostable materials such as ecovio and Ecoflex®, which are widely used in packaging and agricultural coating applications. BASF has been actively advancing biomass-balanced coatings, enabling partial substitution of fossil inputs with renewable resources without compromising performance.

- AkzoNobel N.V. is one of the world’s leading coatings companies, with a growing emphasis on bio-based and sustainable coating technologies. The company integrates renewable raw materials into its formulation platforms to develop low-carbon, high-performance coatings for packaging, construction, and industrial applications. AkzoNobel’s expertise lies in advanced coating chemistry and application-specific customization, enabling it to translate biopolymer innovations into commercially viable products. The company has been actively expanding its portfolio of water-based and powder coatings incorporating bio-attributed resins and additives.

- Arkema S.A. is a specialty chemicals company with a strong focus on high-performance bio-based materials, including resins used in biopolymer coatings. The company’s innovation is anchored in advanced polymer chemistry, particularly in bio-based polyamides such as the Rilsan® range, derived from renewable castor oil feedstock. Arkema supplies critical intermediates and resins that are widely used in sustainable coating formulations across packaging, automotive, and industrial segments. Its strategy emphasizes reducing carbon intensity while maintaining high durability and barrier performance.

Here is a list of key players operating in the global biopolymer coatings market:

The global biopolymer coatings market is highly fragmented but vertically integrated with chemical giants developing formulation and coating expertise, agritech or biotech firms that controlling raw material procurement and supply, and biopolymer specialists driving innovation and gaining a sustainability edge. All are competing to gain significant biopolymer coatings market share and strengthen their positions with strategic collaborations, new product launch, mergers and acquisitions, and geographical expansions.

Competitive Landscape of the Biopolymer Coatings Market:

Recent Developments

- In May 2025, BASF Coatings announced the expansion of its biomass-balanced product pipeline. BASF, with this strategic move, aims at strengthening its commitment to sustainability in biopolymer coating under the R-M eSense and Glasurit Eco Balance brands.

- In April 2025, U of T and BASF entered in a collaboration to develop advanced biopolymer coating catering to industries such as agriculture and pharmaceuticals, with the help of AI-based self-driving labs.

- In June 2021, Braskem unveiled its novel renewable-source polyethylene (PE) wax, which is typically used for adhesives, cosmetics, coatings, and compounds. This will help Braskem solidify its position in the global biopolymer coatings market.

- Report ID: 8520

- Published Date: Apr 21, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.