Geotechnical Instrumentation and Monitoring Market Outlook:

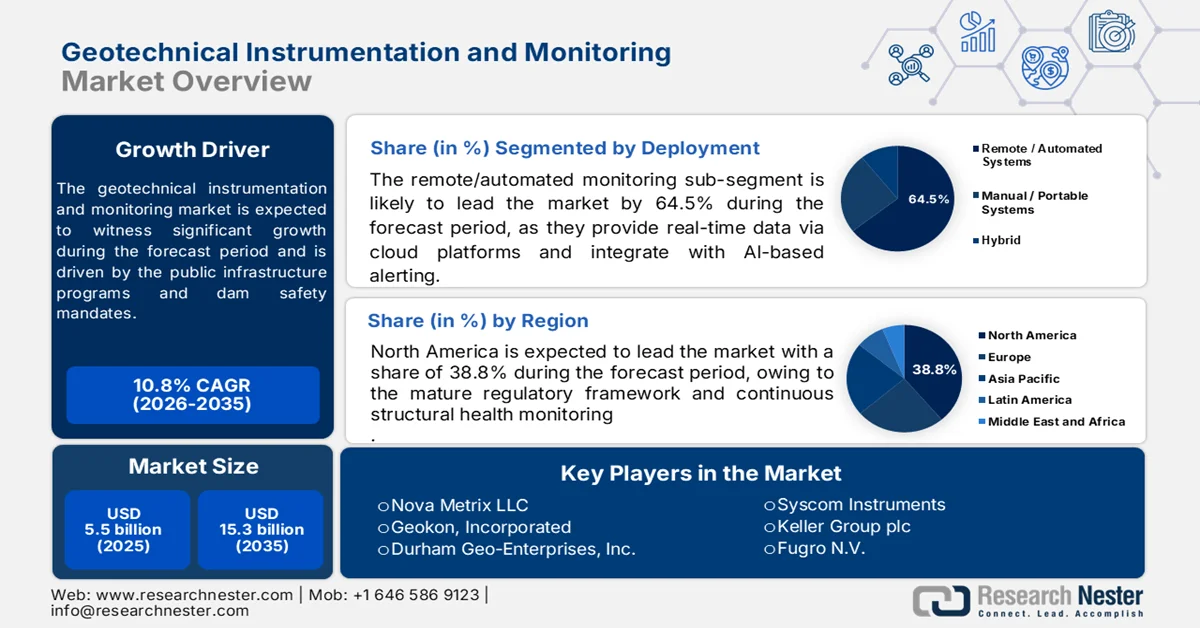

Geotechnical Instrumentation and Monitoring Market size was valued at USD 5.5 billion in 2025 and is projected to reach USD 15.3 billion by 2035, rising at a CAGR of 10.8% during the forecast period 2026 to 2035. In 2026, the industry size of geotechnical instrumentation and monitoring is evaluated at USD 6.1 billion.

Public infrastructure programs, dam safety mandates, and transportation asset rehabilitation are sustaining the demand for geotechnical instrumentation and monitoring market across both developed and emerging economies. According to the CFR September 2023 data, in the U.S., federal capital allocation continues to prioritize asset integrity and risk reduction. The Infrastructure Investment and Jobs Act assigns over USD 550 billion in new spending, including USD 110 billion for roads and bridges and USD 25 billion for airports, all of which require ongoing structural and subsurface monitoring during construction and operation phases. The USACE April 2024 data reports that it operates and maintains nearly 700 dams and over 14,000 miles of levees with instrumentation programs embedded in Dam Safety and Levee Safety initiatives to monitor seepage deformation and pore pressure conditions.

Bipartisan Infrastructure Law Fund Allocation, 2023

|

Metric |

Fund Allocation (USD billion) |

|

Roads and bridges |

110 |

|

Rail |

66 |

|

Power grid |

65 |

|

Broadband internet |

65 |

|

Drinking water |

65 |

|

Resilience |

50 |

|

Public transit |

39 |

|

Airports |

25 |

|

Pollution reduction |

21 |

|

Ports and waterways |

17 |

|

Electric vehicle charging |

8 |

Source: CFR September 2023

Besides the regulatory frameworks, climate resilience priorities are expanding monitoring requirements. The increasing flood risks affecting the landscape are prompting EU member states to strengthen levee and embankment monitoring systems under the Flood Directive. Moreover, the PRS India February 2026 data depicted that India’s Ministry of Jal Shakti reports over 6,000 large dams, many of which are undergoing safety rehabilitation under the Dam Rehabilitation and Improvement Project supported by the World Bank. Across these regions, procurement is increasingly tied to compliance with safety codes, lifecycle asset management, and public accountability, positioning instrumentation and monitoring systems as a required component of capital project delivery and long-term infrastructure stewardship rather than discretionary investment.

Key Geotechnical Instrumentation and Monitoring Market Insights Summary:

Regional Highlights:

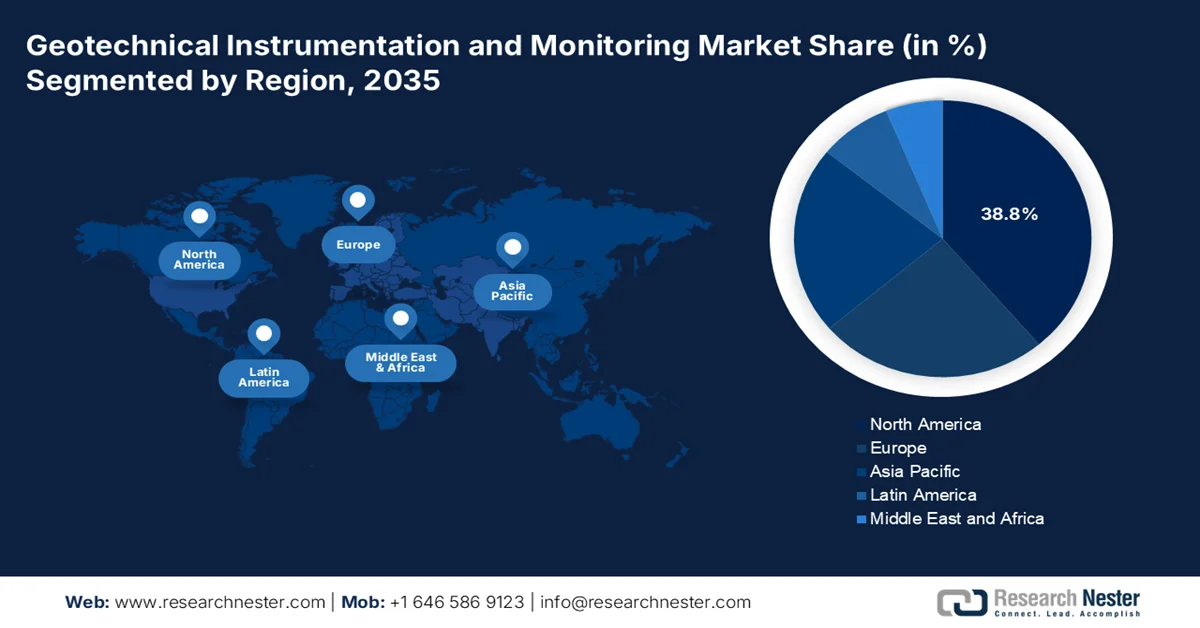

- In the geotechnical instrumentation and monitoring market, North America is anticipated to secure a 38.8% revenue share by 2035 attributed to stringent regulatory mandates and widespread adoption of continuous structural health monitoring systems

- Asia Pacific is projected to be the fastest-growing region during 2026–2035 registering a CAGR of 9.5% fueled by rapid infrastructure expansion and increasing deployment of automated geohazard monitoring technologies

Segment Insights:

- In the geotechnical instrumentation and monitoring market, the remote/automated monitoring systems sub-segment under deployment is projected to command a 64.5% share by 2035 propelled by elimination of manual readings and real-time cloud-integrated AI-based alerting

- Within the component segment, the hardware sub-segment is expected to witness notable growth over the forecast period 2026–2035 impelled by rising federal investments in durable, low-power geotechnical instrumentation for critical infrastructure monitoring

Key Growth Trends:

- Aging dam infrastructure and safety mandates

- Aging transportation infrastructure and rehabilitation backlogs

Major Challenges:

- High expenditure for installation

- Sensor accuracy issues

Key Players: Nova Metrix LLC, Geokon Incorporated, Durham Geo-Enterprises Inc., Syscom Instruments, Keller Group plc, Fugro N.V., SISGEO S.r.l., Roctest, Soil Instruments Ltd, Geokon, International (Sweden), Encardio-Rite Electronics Pvt. Ltd, Mine Design Technologies, Geosense Ltd, Measurand Inc., Kyowa Electronic Instruments Co., Ltd., Tokyo Sokki Kenkyujo Co., Ltd., Certerra, Orica, Vista Clara Inc., Eddyfi Technologies.

Global Geotechnical Instrumentation and Monitoring Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.5 billion

- 2026 Market Size: USD 6.1 billion

- Projected Market Size: USD 15.3 billion by 2035

- Growth Forecasts: 10.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, Canada

- Emerging Countries: India, Australia, South Korea, United Arab Emirates, Brazil

Last updated on : 4 May, 2026

Geotechnical Instrumentation and Monitoring Market - Growth Drivers and Challenges

Growth Drivers

- Aging dam infrastructure and safety mandates: The rising number of aging dams mandates the requirement of a monitoring device, thus driving the geotechnical instrumentation and monitoring market. According to the PIB February 2024 data, there are 234 large dams in India, which are more than 100 years old, requiring immediate safety updates. Moreover, the global stock of large dams is creating a substantial addressable market for retrofit instrumentation. Many of these structures were designed under conservative hydrological models that no longer reflect current extreme rainfall patterns, necessitating more frequent and precise pore pressure and movement data. Further, the multilateral funding agencies and national disaster management authorities are increasingly mandating instrumentation upgrades as a precondition for dam rehabilitation loans and grants.

- Aging transportation infrastructure and rehabilitation backlogs: Deferred maintenance across highways, tunnels, and bridges is driving the geotechnical instrumentation and monitoring market demand tied to rehabilitation budgets. According to the ACMA February 2026 data, over 222,000 U.S. bridges require repair, representing substantial monitoring needs during retrofitting. Similarly, in Europe, the European Commission highlights increasing funding under the Connecting Europe Facility (CEF) to modernize the transport corridors. These programs require geotechnical instrumentation for slope stability, tunnel safety, and foundation performance. Vendors should prioritize integration with the asset management systems as governments are shifting toward condition-based monitoring to extend asset life and optimize maintenance budgets.

- Mining sector regulation and environmental compliance: Government oversight of mining safety and tailings storage facilities is increasing demand for geotechnical instrumentation and monitoring systems. Following the major tailings dam failures, regulators have strengthened the compliance requirements. For example, Brazil’s National Mining Agency enforces the stricter monitoring obligations after the Brumadinho disaster, impacting hundreds of dams. Globally, the International Council on Mining and Metals introduced the Global Industry Standard on Tailings Management, influencing regulatory adoption. Governments are requiring continuous deformation and seepage monitoring for risk mitigation. The actionable insight is that mining companies are shifting toward automated monitoring to meet compliance thresholds, creating opportunities for long-term service contracts and integrated risk management platforms.

Challenges

- High expenditure for installation: The substantial upfront investment required for sensor networks and data acquisition systems remains the primary barrier to entry in the geotechnical instrumentation and monitoring market. Complete monitoring systems can cost hundreds of thousands of dollars per project site, straining the budgets mainly in price-sensitive regions. This constrained fiscal environment leaves minimal capital flexibility for comprehensive monitoring networks. Project managers often prioritize the fundamental structural spending over advanced safety systems, limiting broader solution deployment.

- Sensor accuracy issues: Environmental factors causing sensor drift and data inaccuracy present major technical hurdles in the geotechnical instrumentation and monitoring market. Recent research by the National Science Foundation on the seafloor pressure monitoring revealed that uncorrected sensor drift rates represent significant errors in long-term monitoring applications. For new players without established calibration protocols, these accuracy challenges can destroy credibility. The complex and variable geological environments create additional risks for data accuracy and equipment durability, increasing market operation uncertainties.

Geotechnical Instrumentation and Monitoring Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

10.8% |

|

Base Year Market Size (2025) |

USD 5.5 billion |

|

Forecast Year Market Size (2035) |

USD 15.3 billion |

|

Regional Scope |

|

Geotechnical Instrumentation and Monitoring Market Segmentation:

Deployment Segment Analysis

Under the deployment segment, the remote/automated monitoring systems sub-segment is projected to hold the largest share value of 64.5% by 2035. The segment is driven as they eliminate manual reading, provide real-time data via cloud platforms, and integrate with AI-based alerting. According to the USGS October 2024 data streamgage network, which partners with more than 1,885 Federal, State, Tribal, and local agencies to maintain over 11,300 streamgages. Moreover, nearly 8,500 of these operate year-round as part of the National Streamflow Network (NSN) with 40% designated as Federal Priority Streamgages (FPS), a backbone network hardened against extreme events. This nationwide deployment monitors water levels and streamflow with data made available online for flood hazard protection, freshwater management, and economic decision-making.

Component Segment Analysis

Within the component segment, the hardware sub-segment is fueling the geotechnical instrumentation and monitoring market. This category includes vibrating wire piezometers, MEMS inclinometers, share arrays, and dataloggers. According to the Association of State Dam Safety Officials, November 2021 data, FEMA allocated 67 million under Operations and Support for the National Dam Safety Program, specifically covering Sections 7 through 12 for state assistance grants. Moreover, nearly 35% to 40% was directed toward procuring geotechnical instrumentation hardware, including vibrating wire piezometers, MEMS inclinometers, and automated dataloggers for state-managed high-hazard potential dams. This federal investment directly boosts demand for rugged, low-power hardware capable of interfacing with cloud-based remote systems.

End user Segment Analysis

The civil infrastructure sub-segment is the leading end-user segment within the geotechnical instrumentation and monitoring market. This dominance arises from the sheer scale and longevity of the public assets, which require continuous structural health monitoring throughout their design, construction, and operational phases. Government entities worldwide mandate instrumentation for tunnels, bridges, high-speed rail corridors, and water retention structures to ensure public safety and regulatory compliance. Furthermore, the increasing frequency of extreme weather events has compelled transportation departments and dam safety authorities to prioritize real-time slope stability and settlement monitoring. As cities expand underground and megaprojects proliferate across developing nations, civil infrastructure remains the most reliable and voluminous end-user segment, consistently outpacing industrial applications in both project count and instrumentation density per structure.

Our in-depth analysis of the geotechnical instrumentation and monitoring market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Component |

|

|

Technology |

|

|

Application |

|

|

End user |

|

|

Deployment |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Geotechnical Instrumentation and Monitoring Market - Regional Analysis

North America Market Insights

The North America is dominating the geotechnical instrumentation and monitoring market and is poised to hold the regional revenue share of 38.8% by the end of 2035. The region is defined by the mature regulatory framework that mandates continuous structural health monitoring for federally funded infrastructure projects. Aging dams, bridges, and transit tunnels across the region require systematic retrofitting with automated sensor networks, shifting away from periodic manual inspections. Climate resilience planning at both federal and municipal levels has accelerated deployment of real-time slope stability and settlement monitoring along coastal highways, river embankments, and mountain rail corridors. Public agencies favor turnkey solutions that bundle hardware, data visualization platforms, and long-term maintenance agreements, placing a premium on manufacturer reputability and technical support capacity. The geotechnical instrumentation and monitoring market remains fragmented, with U.S.-based manufacturers Geokon and Nova Metrix leading alongside Canadian firm RST Instruments.

The sustained federal spending on water infrastructure, disaster mitigation, and environmental remediation is driving the geotechnical instrumentation and monitoring market in the U.S. According to the Environmental Protection Agency, October 2024 data, USD 50 billion is allocated in funding under the Bipartisan Infrastructure Law for water infrastructure upgrades, including dams, levees, and wastewater systems requiring subsurface monitoring. The DEM May 2023 data indicated that there are nearly 48 high and 16 significant hazard dams under its jurisdiction requiring continuous evaluation and instrumentation. Additionally, the U.S. Geological Survey's October 2023 data recorded over 27,000 landslides annually across the country, reinforcing the demand for slope stability monitoring systems. These indicators reflect a compliance-driven market where federal agencies prioritize real-time monitoring investments to reduce the infrastructure risk and improve asset reliability.

High and Significant Hazard Dam Owner Types

|

|

Private |

Local Government |

Unknown |

Public Utility |

State |

|

High Hazard |

37 |

28 |

15 |

13 |

7 |

|

Significant Hazard |

22 |

28 |

28 |

13 |

8 |

|

High and Significant Hazard |

31 |

28 |

21 |

13 |

8 |

Source: DEM May 2023

The federal infrastructure renewal, mining oversight, and climate resilience funding are fueling the geotechnical instrumentation and monitoring market in Canada. The Government of Canada's September 2025 data reported over USD 180 billion committed under the Investing in Canada Plan for public infrastructure, including transit, water, and green projects requiring geotechnical monitoring. Moreover, the Government of Canada's February 2026 data stated that the mining and mineral processing sector contributed USD 117.1 billion, driving the demand for tailings and ground stability monitoring systems. Additionally, a significant number of dams are classified as high consequence, necessitating continuous surveillance and instrumentation. These figures indicate a regulatory-driven market where monitoring adoption is closely tied to public safety compliance and resource sector risk management.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the geotechnical and instrumentation monitoring market and is expected to expand at a CAGR of 9.5% during the assessed period, 2026 to 2035. The region is driven by rapid urbanization, massive infrastructure, pipelines, and climate-induced geohazards. China leads with its Belt and Road initiative and domestic high-speed rail expansion, requiring continuous settlement monitoring for thousands of kilometers of track. India’s Dam Rehabilitation and Improvement Project Phase II is retrofitting with automated piezometers and deformation sensors following the Central Water Commission safety mandates. Key trends include the shift from manual inclinometer readings to wireless IoT arrays, government mandates for cloud-based centralized data platforms, and integration of satellite InSAR with ground-based sensors. The geotechnical instrumentation and monitoring market is fragmented with strong domestic players in China and India alongside Japanese and international manufacturers.

Large-scale public infrastructure and water management investments are driving the geotechnical instrumentation and monitoring market in India. According to the PIB July 2024, the Government of India allocated USD 133 billion for the capital expenditure with a strong focus on transport and urban infrastructure requiring geotechnical oversight. The PIB January 2025 article depicted that over 146,195 km of National Highways are under ongoing expansion and slope stabilization projects, driving the monitoring demand. Additionally, the August 2023 article indicated that over 5,745 large dams across India are undergoing safety assessments and rehabilitation. These indicators reflect a government-driven market where the monitoring systems are increasingly integrated into the infrastructure execution to improve safety compliance and long-term asset performance.

State-wise Dam Information, 2023

|

State/UT |

No. of Constructed Large Dams |

No. of Under construction Large dams |

|

Andaman and Nicobar |

2 |

0 |

|

Andhra Pradesh |

149 |

17 |

|

Arunachal Pradesh |

1 |

3 |

|

Assam |

3 |

1 |

|

Bihar |

24 |

2 |

|

Chhattisgarh |

249 |

9 |

|

Goa |

5 |

0 |

|

Gujarat |

620 |

12 |

|

Haryana |

1 |

0 |

|

Himachal Pradesh |

19 |

1 |

|

Jammu & Kashmir and Ladakh |

15 |

2 |

|

Jharkhand |

55 |

24 |

|

Karnataka |

230 |

2 |

|

Kerala |

61 |

0 |

|

Madhya Pradesh |

899 |

7 |

|

Maharashtra |

2117 |

277 |

|

Manipur |

3 |

1 |

|

Meghalaya |

8 |

2 |

|

Mizoram |

1 |

0 |

|

Nagaland |

1 |

0 |

|

Odisha |

200 |

4 |

|

Punjab |

14 |

2 |

|

Rajasthan |

204 |

8 |

|

Sikkim |

2 |

0 |

|

Tamil Nadu |

118 |

0 |

|

Tripura |

1 |

0 |

|

Telangana |

168 |

16 |

|

Uttar Pradesh |

117 |

13 |

|

Uttarakhand |

17 |

8 |

|

West Bengal |

30 |

0 |

Source: PIB August 2023

The large-scale government investment in transport infrastructure and network expansion is driving the geotechnical instrumentation and monitoring market in China. According to the People’s Republic of China, February 2024 data, fixed asset investment in the transport sector reached USD 548.7 billion, reflecting sustained demand for monitoring across highways, railways, and waterways. The government added 7,000 km of expressways and 2,776 km of high-speed rail in the same year, requiring continuous monitoring of slopes and tunnels, as well as foundations, during construction and operation. Additionally, China’s total transport network exceeded 6 million km in 2023, indicating significant long-term maintenance and rehabilitation needs. These data highlight a government-driven market where geotechnical monitoring systems are integrated into the large-scale infrastructure development and lifecycle asset management programs.

Europe Market Insights

The geotechnical instrumentation and monitoring are shaped by the stringent safety regulations, aging transport infrastructure, and climate adaptation mandates. The European Commission’s Trans European Transport Network program allocates billions annually for rail and road corridor upgrades, with instrumentation requirements embedded in all tunnel and bridge contracts. The Alpine region, spanning France, Italy, Germany, Austria, and Switzerland, requires continuous thermal and mechanical monitoring for base tunnels, including the Brenner and Mont Cenis passes. National highway agencies across Germany, France, and the UK now mandate automated deformation monitoring for all deep excavations exceeding ten meters. The geotechnical instrumentation and monitoring market is shifting toward fiber optic distributed sensing and low-power wireless networks, reducing manual inspection costs.

Transport infrastructure investments and a large rehabilitation backlog are driving the geotechnical instrumentation and monitoring market in Germany. According to the Business Sweden August 2025 data, the federal government allocated USD 36.5 billion for trunk roads, railways, and waterways, with USD 12.8 billion directed toward bridge modernization and rail upgrades, both requiring continuous structural and subsurface monitoring. Additionally, the USD 545 billion Special Fund for Infrastructure and Climate Neutrality is accelerating long-term infrastructure renewal. Government data indicates that one in three motorway bridges and over half of railway bridges are in poor condition, necessitating instrumentation during refurbishment. These trends highlight a compliance-driven market where monitoring systems are increasingly embedded in large-scale public infrastructure modernization programs.

The government-led infrastructure renewal and flood risk management programs are shaping the geotechnical instrumentation and monitoring market in the UK. According to the Government of the UK, in a March 2023 article, HM Treasury confirmed USD 765 billion in planned public sector gross investment over the next five years, covering transport, energy, and water assets that require geotechnical monitoring. The Water March 2024 article indicated that it maintains over 14,000 flood defense assets, including embankments and barriers, requiring continuous condition monitoring. Additionally, the Department of Transport's March 2026 data allocated USD 4.9 billion for road enhancement schemes, with ongoing upgrades driving demand for slope stability and foundation monitoring. These data indicate a compliance-driven market where monitoring adoption is closely tied to asset resilience, regulatory oversight, and lifecycle infrastructure management.

Key Geotechnical Instrumentation and Monitoring Market Players:

- Nova Metrix LLC (U.S.)

- Geokon, Incorporated (U.S.)

- Durham Geo-Enterprises, Inc. (U.S.)

- Syscom Instruments (U.S.)

- Keller Group plc (UK)

- Fugro N.V. (Netherlands)

- SISGEO S.r.l. (Italy)

- Roctest (Canada)

- Soil Instruments Ltd (UK)

- GEOKON (Europe)

- International (Sweden)

- Encardio-Rite Electronics Pvt. Ltd (India)

- Mine Design Technologies (Australia)

- Geosense Ltd (UK)

- Measurand Inc. (Canada)

- Kyowa Electronic Instruments Co., Ltd. (Japan)

- Tokyo Sokki Kenkyujo Co., Ltd. (Japan)

- Certerra (UK)

- Orica (Australia)

- Vista Clara Inc. (U.S.)

- Eddyfi Technologies (Canada)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Nova Metrix LLC is a leading player in the geotechnical instrumentation and monitoring market and provider of structural monitoring solutions mainly via its mature concrete embedment vibrating wire strain gauges and corrosion monitoring systems. The company has advanced the market by integrating wired and wireless data loggers with cloud-based platforms, enabling real-time alerts.

- Geokon Incorporated is a cornerstone in the geotechnical instrumentation and monitoring market, renowned for its high-precision vibrating wire technology used in dams, excavations, and nuclear facilities. The company has strategically expanded its portfolio by developing automated data acquisition systems that interface with remote telemetry units, ensuring long-term stability and accuracy.

- Durham Geo Enterprises, Inc specializes in the geotechnical instrumentation and monitoring market in slope inclinometers, extensometers, and settlement monitoring systems for earthworks and foundations. The company has advanced its offerings by incorporating digital MEMS-based inclinometer arrays and real-time data visualization software, reducing manual reading errors.

- Syscom Instruments plays a specialized role in the geotechnical instrumentation and monitoring market, focusing on vibrating wire readouts, dataloggers, and multiplexers that serve as critical interfaces between sensors and central control systems. The company has advanced the geotechnical instrumentation and monitoring market by developing low-power solar-ready remote monitoring units capable of operating in extreme temperatures. In 2024, the company made a revenue of USD 220.1 million.

- Keller Group plc has a substantial footprint in the geotechnical instrumentation and monitoring market, providing integrated instrumentation services for ground engineering and foundation projects globally. The company has advanced the market via strategic acquisitions and by deploying wireless IoT sensor networks that feed real-time data into central geotechnical models. According to the 2024 annual report, the company has made a revenue of USD 3.79 billion.

Here is a list of key players operating in the global geotechnical instrumentation and monitoring market:

The geotechnical instrumentation and monitoring market is fragmented with a mix of specialized regional players and globally diversified engineering firms. The key players focus on strategic initiatives such as product innovation in wireless and IoT-enabled sensors, mergers and acquisitions to expand geographic reach, and forming long-term partnerships with construction and civil engineering contractors. For example, in March 2025, Certerra announced the acquisition of Tierra, Inc. To reduce downtime and improve safety, analytics companies are increasingly investing in cloud-based data visualization and automated warning systems. Additionally, manufacturers are targeting the emerging economies for infrastructure development, while Europe and North America firms highlight high precision and regulatory compliance solutions to maintain premium positioning.

Corporate Landscape of the Geotechnical Instrumentation and Monitoring Market:

Recent Developments

- In April 2026, Orica announced the launch of its next-generation GroundProbe geotechnical monitoring solution, designed to help mining operations improve safety, streamline deployment, and make faster, higher-confidence decisions.

- In January 2026, Vista Clara Inc. announced the launch of Vista Clara Geotech Ltd., a new Canadian company based in Surrey, British Columbia. Vista Clara Geotech Ltd. will manufacture magnetic resonance (NMR) instruments for geoscience applications and provide instrument sales, rentals, and customer service to organizations across Canada and internationally.

- In June 2025, Eddyfi Technologies announced the acquisition of Sisgeo, a leading provider of geotechnical and structural monitoring instrumentation. Sisgeo becomes part of Eddyfi’s Remote Monitoring Solutions, the company’s product line dedicated to monitoring technologies for geotechnical and structural assets.

- Report ID: 8555

- Published Date: May 04, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.