Gallium Nitride (GaN) Power Devices Market Outlook:

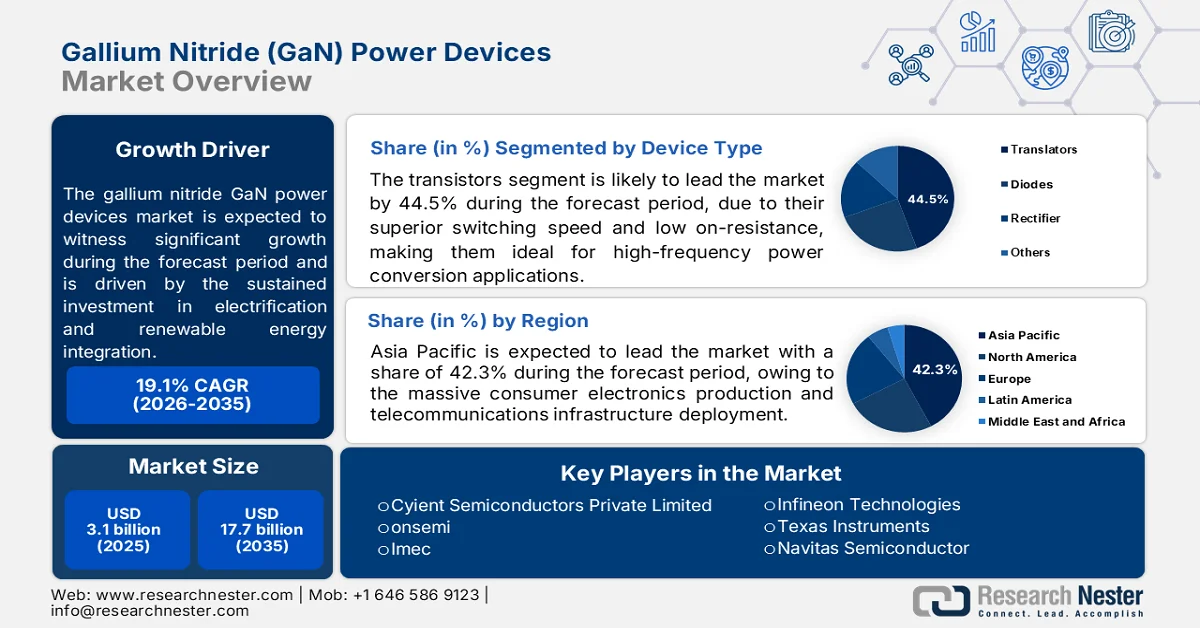

Gallium Nitride (GaN) Power Devices Market size was valued at USD 3.1 billion in 2025 and is projected to account for USD 17.7 billion by the end of 2035, rising at a CAGR of 19.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of gallium nitride (GaN) power devices is estimated at USD 3.6 billion.

The gallium nitride power devices market is benefiting from sustained investment in electrification, power infrastructure modernization, renewable energy integration, and advanced computing systems. Demand is being reinforced by rising deployment of electric vehicles, charging networks, industrial automation equipment, and energy-efficient power conversion systems. According to the International Energy Agency May 2024, global electric car sales exceeded 17 million units in 2024, representing a significant increase in the installed base of high-performance power electronics across transportation and charging applications. In parallel, utilities and grid operators are expanding investments in power transmission, distribution, and distributed energy resources to accommodate increasing electricity demand and renewable generation.

The market is also supported by accelerating growth in renewable energy installations and the expansion of digital infrastructure. The World Economic Forum April 2025 reported that global renewable power capacity additions reached approximately 585 GW in 2024, reflecting continued investment in solar, wind, and energy-storage projects that require efficient power conversion equipment. At the same time, the IEA projects that global electricity consumption from data centers, artificial intelligence workloads, and digital services will rise substantially through the end of the decade, increasing demand for advanced power management systems. As public-sector investments continue to support electrification and digitalization programs, the GaN power devices market is positioned to benefit from sustained capital expenditure across multiple end-use industries.

Key Gallium Nitride (GaN) Power Devices Market Insights Summary:

Regional Highlights:

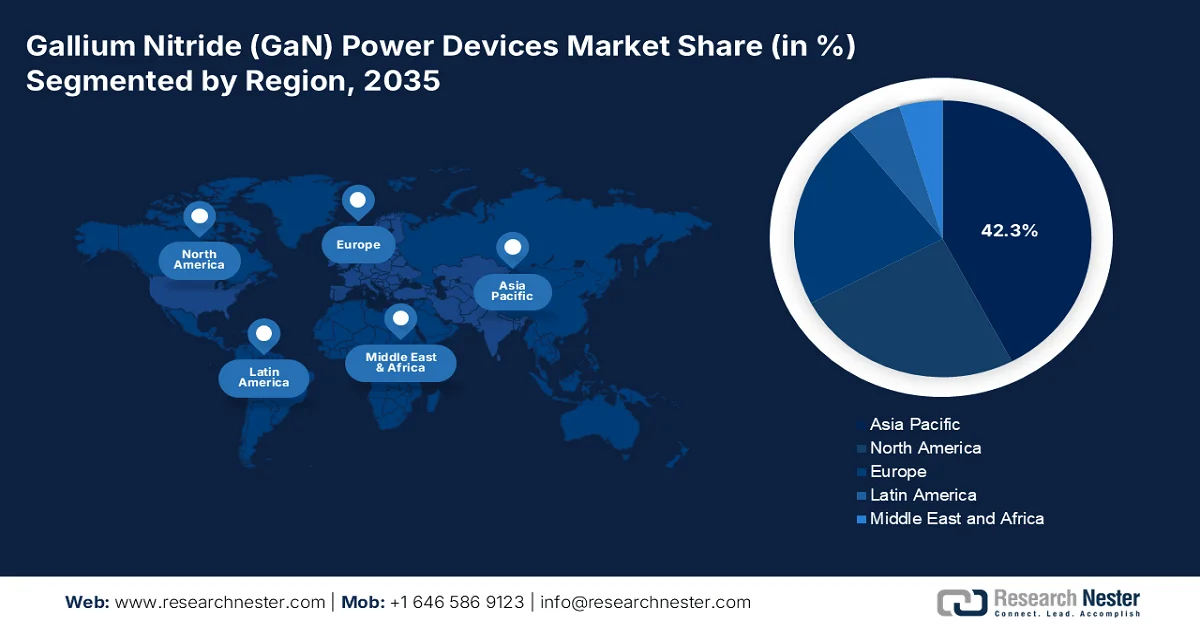

- Asia Pacific is anticipated to command 42.3% of the gallium nitride (GaN) power devices market revenue share by 2035, reinforced by massive consumer electronics production, electric-vehicle manufacturing, and telecommunications infrastructure deployment

- North America is set to witness rapid expansion throughout 2026-2035, fueled by strong demand from automotive electrification, data-center infrastructure, and defense applications

Segment Insights:

- The transistors segment is projected to capture 44.5% of the gallium nitride (GaN) power devices market by 2035, underpinned by superior switching speed and low on-resistance for high-frequency power conversion applications

- Automotive is expected to lead the application segment in the market through 2035, supported by the accelerating global transition toward electric and hybrid vehicles

Key Growth Trends:

- Expansion of electric vehicle manufacturing

- Grid modernization and power infrastructure upgrades

Major Challenges:

- High epitaxial growth costs

- Reliability and qualification hurdles

Key Players: Cyient Semiconductors Private Limited (India), onsemi (U.S.), Imec (Belgium), Infineon Technologies (Germany), Texas Instruments (U.S.), Navitas Semiconductor (U.S.).

Global Gallium Nitride (GaN) Power Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.1 billion

- 2026 Market Size: USD 3.6 billion

- Projected Market Size: USD 17.7 billion by 2035

- Growth Forecasts: 19.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.3% share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, South Korea, Germany

- Emerging Countries: India, Canada, Vietnam, Singapore, United Arab Emirates

Last updated on : 7 July, 2026

Gallium Nitride (GaN) Power Devices Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of electric vehicle manufacturing: Government-backed EV adoption programs are significantly increasing demand for advanced power electronics. GaN power devices are being evaluated for onboard chargers, DC-DC converters, and fast-charging systems because governments are prioritizing higher charging efficiency and reduced energy losses. The Earth Justice February 2026 data reported that more than USD 5 billion was allocated through the National Electric Vehicle Infrastructure Formula Program to build a nationwide charging network. These investments are increasing procurement requirements for high-performance power semiconductors throughout charging infrastructure and vehicle powertrain ecosystems. Manufacturers supplying automotive electronics are consequently expanding partnerships with semiconductor firms capable of supporting higher-power-density designs.

- Grid modernization and power infrastructure upgrades: Governments are increasing spending on transmission, distribution, and grid resilience projects to support electrification and energy security objectives. These investments create demand for advanced power conversion technologies used in substations, smart-grid equipment, energy storage systems, and power quality management solutions. The U.S. Department of Energy 2026 data announced more than USD 3.46 billion in Grid Resilience and Innovation Partnerships (GRIP) funding to strengthen electric infrastructure. As grid operators pursue modernization goals, demand is expanding for semiconductor components that enable more efficient power management across utility-scale and distributed electricity networks.

Challenges

- High epitaxial growth costs: Specialized MOCVD equipment and ultra-pure precursors make GaN wafer production significantly costlier than silicon. Small entrants struggle with high capital expenditure and limited economies of scale. Foundry partnerships often require minimum volume commitments, creating financial barriers for startups. Companies like X-FAB have invested heavily in dedicated GaN fab lines to address this challenge.

- Reliability and qualification hurdles: Automotive AEC-Q101 qualification demands extensive lifetime testing over thousands of hours. Dynamic RDS(on) drift and threshold voltage instability remain concerns for Tier-1 suppliers. Smaller manufacturers lack resources for exhaustive reliability campaigns, delaying market entry by years. Companies like Navitas have invested heavily in generating device-hours to achieve automotive certification.

Gallium Nitride (GaN) Power Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

19.1% |

|

Base Year Market Size (2025) |

USD 3.1 billion |

|

Forecast Year Market Size (2035) |

USD 17.7 billion |

|

Regional Scope |

|

Gallium Nitride (GaN) Power Devices Market Segmentation:

Device Type Segment Analysis

Under the device type segment, the transistors are dominating and is poised to hold the regional share valve of 44.5% by the end of 2035. The segment is driven by their superior switching speed and low on-resistance, making them ideal for high-frequency power conversion applications. Diodes, especially GaN Schottky diodes, are widely used in power factor correction (PFC) circuits and solar inverters. Rectifiers find applications in AC-DC conversion for consumer adapters. According to the IOP Science February 2026 study, GaN-based transistors demonstrated a 32% reduction in switching losses compared to silicon MOSFETs in 2023 testing. As manufacturing yields improve, transistors are driven by automotive and data-center demand, while diodes maintain steady growth in industrial power supplies.

Application Segment Analysis

The application segment of the gallium nitride power devices market is categorized into automotive, industrial, telecommunications, consumer electronics, and others. Among these, automotive emerges as the leading sub-segment, driven by the global transition toward electric and hybrid vehicles. GaN power devices enable highly efficient on-board chargers, DC-DC converters, and traction inverters, offering superior power density and high-frequency operation compared to traditional silicon solutions. Automotive manufacturers increasingly adopt GaN to reduce system weight, improve thermal management, and extend vehicle driving range. The growing proliferation of 400V and 800V battery architectures further accelerates GaN adoption, positioning automotive applications as the primary revenue generator within this segment.

Voltage Range Segment Analysis

The high voltage sub-segment, rated at 650V and above, leads the voltage range category of the gallium nitride power devices market, driven by automotive electrification. The NLM December 2024 study depicts that the implementation of a 6.6 kW bi-directional on-board charger (OBC) for electric vehicles utilized 650V, 25mΩ discrete GaN switches, achieving 96% efficiency and 2.2 kW/L power density including liquid cooling. The OBC operates from a 90–264 Vrms AC grid to a 200–450V battery, integrating a totem-pole PFC active front end with a dual active bridge DC-DC converter, plus an auxiliary 1 kW converter using 100V GaN switches for 12V systems. These results confirm that 650V GaN enables higher switching frequencies and power density than silicon, positioning high-voltage GaN as essential for next-generation electric and hybrid vehicles.

Our in-depth analysis of the gallium nitride (GaN) power devices includes the following segments:

|

Segment |

Subsegments |

|

Device Type |

|

|

Application |

|

|

Voltage Range |

|

|

End user |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Gallium Nitride (GaN) Power Devices Market - Regional Analysis

APAC Market Insights

Asia Pacific is dominating the gallium nitride power devices market and is expected to hold the regional revenue share of 42.3% by the end of 2035. The region is driven by the massive consumer electronics production, electric-vehicle manufacturing, and telecommunications infrastructure deployment. China leads in volume production and domestic consumption, while Japan and South Korea contribute advanced materials and process technologies. India, Malaysia, and Indonesia emerge as assembly and test hubs, benefiting from cost advantages and government incentives. The region hosts major foundries, epitaxy suppliers, and packaging houses, creating a vertically integrated ecosystem. Strong government backing through subsidies and favorable industrial policies accelerates domestic GaN fabrication. Asia Pacific excels in high-volume, cost-competitive manufacturing, serving both regional demand and global exports across automotive, consumer, and industrial segments.

The increasing investments in electronics manufacturing, electric mobility, renewable energy deployment, and digital infrastructure is shaping the gallium nitride power devices market in India. Government initiatives promoting domestic semiconductor production and power-efficient technologies are creating opportunities for advanced power device adoption across industrial and consumer applications. Demand is also being supported by the rapid expansion of the country's electronics sector. According to the PIB October 2025 data, India’s electronics production reached approximately ₹11.3 lakh crore, reflecting strong growth in manufacturing activities that require efficient power management solutions. As India strengthens its semiconductor ecosystem and expands energy-intensive infrastructure, the need for GaN-based power devices is expected to increase across multiple high-growth industries.

The investments in advanced manufacturing, electric mobility, renewable energy systems, and next-generation communications infrastructure is driving the GaN power devices market in China. Strong government support for semiconductor self-sufficiency and industrial modernization is encouraging broader adoption of high-efficiency power electronics across strategic sectors. A key demand indicator is the rapid growth of renewable power infrastructure. According to IEA 2025 data, the country added approximately 357 GW of new renewable energy capacity, representing one of the largest annual renewable energy expansions globally. The increasing deployment of solar, wind, and energy storage projects requires advanced power conversion equipment, creating favorable conditions for GaN device suppliers serving energy, industrial, and transportation applications.

North America Market Insights

North America is projected to emerge rapidly during the assessed period, 2026 to 2035. The region is driven by the strong demand from automotive electrification, data-center infrastructure, and defense applications. The United States leads with extensive R&D investments and a robust semiconductor ecosystem, while Canada complements through clean-energy initiatives and critical minerals supply. Major semiconductor IDMs and fabless designers maintain significant design, test, and manufacturing footprints across the region. Government programs focus on reducing import dependency, fostering domestic fabrication capabilities, and accelerating wide-bandgap technology commercialization. The market benefits from early adoption of 800V electric-vehicle architectures and high-efficiency server power supplies. Strategic collaborations between national laboratories, universities, and industry players drive continuous innovation.

The increase investments in advanced power electronics for data centers, industrial equipment, defense systems, and electrified transportation is shaping the gallium nitride power devices market in the U.S. Demand is supported by federal initiatives aimed at strengthening semiconductor manufacturing capacity and improving energy efficiency across critical infrastructure. A notable indicator of expanding power-electronics requirements is the growth of electricity-intensive digital infrastructure. According to the U.S. Energy Information Administration (EIA) July 2024 data, U.S. retail electricity sales reached approximately 3,861 billion kWh in 2023, reflecting rising power consumption across commercial and industrial sectors. This trend is encouraging OEMs and system integrators to adopt more efficient power-conversion technologies, supporting long-term opportunities for GaN device suppliers.

The investments in clean energy, electrification, telecommunications, and advanced manufacturing increase demand for efficient power electronics is shaping the gallium nitride (GaN) power devices market in Canada. Federal and provincial initiatives supporting grid modernization and low-carbon technologies are encouraging the adoption of next-generation semiconductor components across industrial and energy applications. Canada’s growing electricity infrastructure further supports market growth. According to Government of Canada April 2023 data, non-emitting sources accounted for approximately 84% of Canada’s electricity generation, highlighting the country’s strong focus on clean power systems that rely on advanced power conversion and energy management technologies.

Europe Market Insights

The GaN power devices market in Europe is driven by automotive electrification, renewable energy integration, and industrial automation. Germany, France, and the UK lead in R&D and automotive qualification, while Nordic countries focus on renewable inverters and grid applications. Europe hosts leading IDMs, research institutes, and foundries with strong government backing through IPCEI on Microelectronics. The region emphasizes sustainability, circular economy principles, and energy efficiency mandates, accelerating GaN adoption in EV chargers, wind converters, and rail traction systems. Collaborative public-private partnerships, including IMEC and Fraunhofer, drive innovation in GaN-on-Si epitaxy and reliability testing. Europe maintains a premium-quality positioning, prioritizing automotive and industrial reliability over high-volume consumer segments.

The gallium nitride power devices market in Germany is benefiting from the country’s focus on industrial digitalization, energy transition projects, electric mobility, and semiconductor innovation. Demand is growing across industrial automation systems, renewable energy installations, charging infrastructure, and advanced manufacturing equipment where efficient power management is increasingly important. According to the Enerdata March 2025 data, gross electricity generation from renewable energy sources reached 59.4% of total electricity generation, underscoring the scale of renewable integration within the national power system. As utilities and manufacturers seek more efficient power conversion technologies, opportunities for GaN-based devices are expected to expand across Germany’s industrial and energy sectors.

The GaN power devices market in the UK is advancing as investments in clean energy, electrified transportation, telecommunications infrastructure, and high-value manufacturing increase demand for efficient power electronics. Government initiatives supporting semiconductor research, energy security, and industrial innovation are creating favorable conditions for the adoption of advanced power devices across commercial and industrial applications. A notable indicator of growing infrastructure requirements is the expansion of the electric vehicle ecosystem. According to the Government of UK July 2025 data, the country had more than 82,000 public electric vehicle charging devices installed, reflecting continued investment in charging infrastructure. This expansion is strengthening demand for high-performance power conversion systems, supporting opportunities for GaN device manufacturers and suppliers.

Key Gallium Nitride (GaN) Power Devices Market Players:

- Cyient Semiconductors Private Limited (India)

- onsemi (U.S.)

- Imec (Belgium)

- Infineon Technologies (Germany)

- Texas Instruments (U.S.)

- Navitas Semiconductor (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Cyient Semiconductors supports the gallium nitride (GaN) power devices market through design services, offering GaN-compatible driver and controller IP. Its strategic focus includes reference designs for compact power adapters and industrial supplies. By collaborating with foundries, it enables faster prototyping for fabless GaN chip developers entering this evolving market.

- onsemi is a key IDM in the gallium nitride power devices market, offering high-voltage GaN FETs for automotive and industrial applications. Its strategy emphasizes expanding manufacturing capacity and integrating GaN into intelligent power modules. The company pursues long-term supply agreements to strengthen its position in electric-vehicle and renewable-energy segments.

- IMEC is a premier R&D institute driving innovation in the market. It develops advanced GaN-on-silicon process modules and reliability standards through collaborative industry partnerships. While not a manufacturer, its pilot lines and design kits accelerate commercialization for global semiconductor companies seeking next-generation GaN solutions.

- Infineon is a market leader in the gallium nitride power devices market, with a dual-technology portfolio covering broad voltage ranges. Its strategy includes scaling production in multiple fabs and integrating GaN with controllers and sensors. This vertical approach targets automotive, server, and consumer applications demanding high efficiency and compactness.

- Texas Instruments competes in the gallium nitride power devices market by integrating GaN FETs with gate drivers in single-package solutions. Its strategy leverages high-volume analog manufacturing and extensive design-tool ecosystems. The company focuses on simplifying GaN adoption for industrial, communications, and automotive power-conversion systems worldwide.

Here is a list of key players operating in the global gallium nitride power devices market:

The GaN power devices market is intensely competitive, characterized by a mix of IDMs, fabless designers, and foundries. Key players are aggressively pursuing vertical integration, capacity expansion, and technology differentiation. Strategic initiatives include R&D investments in 8-inch and 12-inch wafer processing to reduce costs, along with partnerships with automotive and data-center OEMs to secure long-term supply. Mergers and acquisitions are reshaping the landscape, while Asian foundries are scaling manufacturing. Simultaneously, companies are expanding portfolios to compete with SiC in electric vehicles and renewables.

Corporate Landscape of the Gallium Nitride (GaN) Power Devices Market:

Recent Developments

- In May 2026, Cyient Semiconductors Private Limited announced the launch of seven new gallium nitride (GaN) power devices for the Indian market, which is developed using Navitas Semiconductor’s industry leading GaN technology.

- In June 2026, onsemi announced the launch of GaNEXUS™, which is a new gallium nitride (GaN) power portfolio engineered to deliver higher efficiency, greater power density, and improved thermal performance across AI data centers, industrial automation, robotics, and energy infrastructure applications.

- In October 2025, Imec launched a 300mm GaN program to develop advanced power devices and reduce manufacturing costs. Transitioning to 300mm wafer sizes enables the development of more advanced power electronics devices and a reduction of manufacturing costs.

- Report ID: 8656

- Published Date: Jul 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.