SiC and GaN Power Semiconductor Market Outlook:

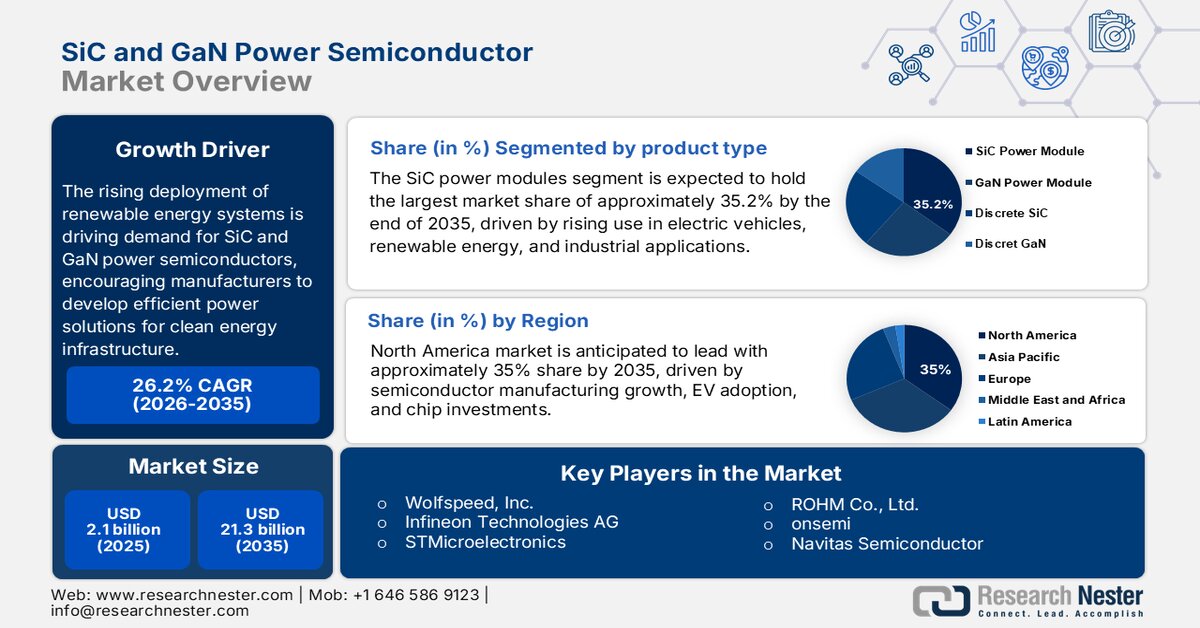

SiC and GaN Power Semiconductor Market size was over USD 2.1 billion in 2025 and is projected to exceed USD 21.3 billion by the end of 2035, registering a CAGR of 26.2% during the forecast period of 2026-2035. In 2026, the industry size of SiC and GaN power semiconductor is evaluated at USD 2.6 billion.

The SiC and GaN power semiconductor market is growing steadily with the rising adoption of electric vehicles globally. As the automotive industry pay attention on improving vehicle performance, energy efficiency, and charging capabilities, manufacturers are increasingly using these advanced power semiconductors in EV systems. Their ability to support efficient power management and fast charging is anticipated to encourage large adoption, which is one of the reasons for the market’s growth during the forecast period.

The market is also supported by growing investments in semiconductor manufacturing across several countries. Governments are enhancing domestic chip production to strengthen supply chains and meet rising demand. According to the U.S. CHIPS and Science Act allocated approximately USD 52.7 billion for semiconductor manufacturing, research, and workforce development. This is anticipated to create new opportunities for SiC and GaN power semiconductors.

The market is also supported by the rising adoption of advanced power technologies across North America, Europe, and Asia Pacific. This trend is expected to support market growth throughout the forecast period. While investments in digital infrastructure and energy systems are continuously increasing, this is one of the reasons for the demand of SiC and GaN power semiconductors is expected to increase.

Key SiC and GaN Power Semiconductor Market Insights Summary:

Regional Highlights:

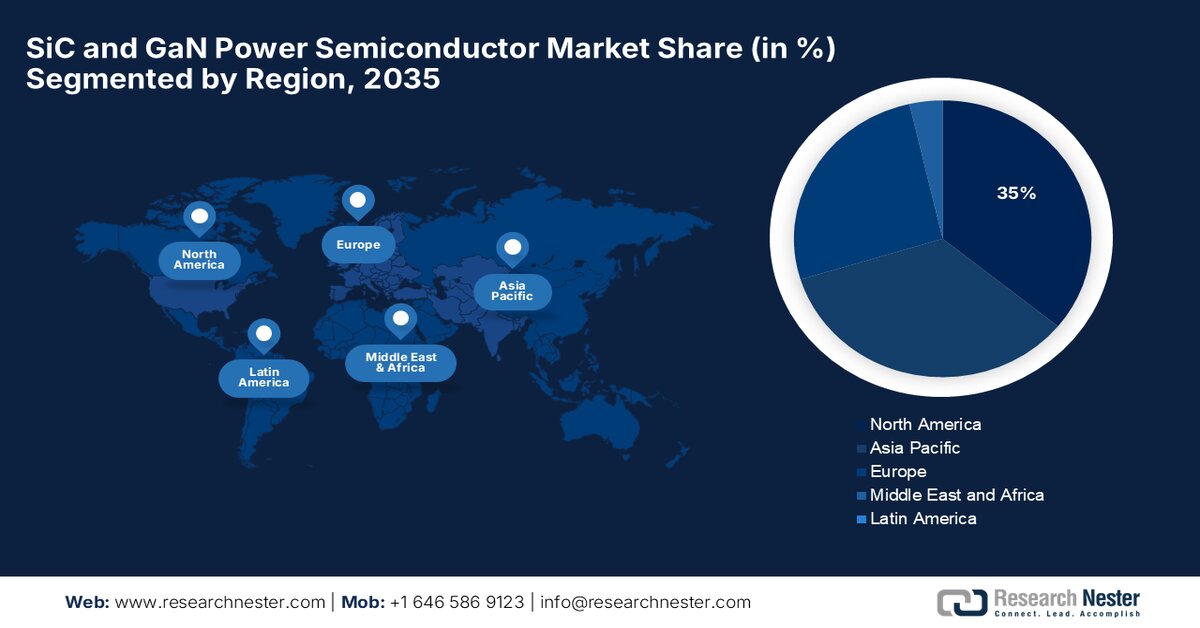

- The sic and gan power semiconductor market in North America is projected to capture a 35% share by 2035, bolstered by the presence of leading semiconductor manufacturers, growing electric vehicle adoption, and expanding domestic chip manufacturing

- Asia Pacific is expected to secure a significant market share by 2035, fueled by its well-established chip manufacturing ecosystem, expanding electric vehicle and renewable energy industries, and supportive government initiatives for semiconductor production

Segment Insights:

- The sic and gan power semiconductor market's SiC power modules segment is projected to account for a 35.2% share by 2035, reinforced by rising adoption across electric vehicles, renewable energy projects, and industrial equipment

- The power supplies segment is expected to secure the largest share by 2035, supported by increasing emphasis on improving power efficiency and reducing operating costs

Key Growth Trends:

- Expansion of aerospace and defense electronics

- Rising deployment of fast-charging infrastructure

Major Challenges:

- High manufacturing costs and complex production processes

- Limited industry standardization and design compatibility

Key Players: Wolfspeed, Inc., Infineon Technologies AG, STMicroelectronics, ROHM Co., Ltd., onsemi, Navitas Semiconductor.

Global SiC and GaN Power Semiconductor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.1 billion

- 2026 Market Size: USD 2.6 billion

- Projected Market Size: USD 21.3 billion by 2035

- Growth Forecasts: 26.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Vietnam, Malaysia, Saudi Arabia, Brazil

Last updated on : 24 July, 2026

SiC and GaN Power Semiconductor Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of aerospace and defense electronics: The growing investments in the aerospace and defense sector are creating new opportunities for the SiC and GaN power semiconductor market. The U.S. Department of Defense continues to invest in advanced electronics and microelectronics to strengthen defense capabilities, which supports the demand for high-performance power semiconductors. As countries continue to modernize their defense capabilities, demand for SiC and GaN power semiconductors is anticipated to grow throughout the forecast period. These semiconductors are being highly adopted in advanced systems that needed reliable and efficient power management.

- Rising deployment of fast-charging infrastructure: The expansion of fast-charging infrastructure is creating new opportunities for the market. Governments and private companies are increasing investments in public and commercial charging stations to support the growing number of electric vehicles. The U.S. Department of Energy supports the expansion of a national EV charging network through programs focused on accelerating charging infrastructure deployment. As the demand for faster and more reliable charging continues to rise, the use of SiC and GaN power semiconductors is expected to increase throughout the forecast period.

- Increasing AI data center investments fueling: Growing investment in AI data center infrastructure is creating new opportunities for the market. The rising need for AI computing is helping operators to improve energy efficiency across their facilities. This is growing the use of SiC and GaN power semiconductors in modern power systems. The U.S. Department of Energy highlights the growing energy requirements of AI and data centers, highlighting the need for more efficient computing infrastructure and power technologies. The continued expansion of AI infrastructure is expected to contribute to market growth throughout the forecast period.

Challenges

- High manufacturing costs and complex production processes: For the SiC and GaN power semiconductors, the high cost remains a key challenge for market growth. These semiconductors require more advanced manufacturing compared to conventional silicon- based devices. Moreover, the limited availability of raw materials and manufacturing complexities can also affect supply.

- Limited industry standardization and design compatibility: The lack of common manufacturing standards remains a challenge for the market. Many manufacturers need to make changes to their existing products before they can use these semiconductors, making the process more time-consuming and expensive. This is one of the reasons for the delay in product launches and slows their adoption across some industries.

SiC and GaN Power Semiconductor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

26.2% |

|

Base Year Market Size (2025) |

USD 2.1 billion |

|

Forecast Year Market Size (2035) |

USD 21.3 billion |

|

Regional Scope |

|

SiC and GaN Power Semiconductor Market Segmentation:

Product Types Segment Analysis

From the type segment, the SiC power modules sub-segment is anticipated to account for the largest share of approximately 35.2% by the end of 2035. Their global use across electric vehicles, renewable energy projects, and industrial equipment continues to strengthen the segment's position in the market. With industries paying more attention on energy-efficient systems, the demand for these modules is expected to remain steady throughout the forecast period. Several manufacturers prefer SiC power modules for applications that needed reliable performance under high-power operating conditions.

Application Segment Analysis

Based on the application segment, the power supplies sub-segment is anticipated to hold the largest share of the market by the end of 2035. Power supply systems used globally continue to create a stable demand for these semiconductors. Their ability to handle electricity more efficiently while reducing energy losses makes them a suitable choice for modern equipment. For the forecast period, the segment is anticipated to maintain its leading position, with businesses paying greater attention to improving power efficiency and reducing operating costs.

Our in-depth analysis of the SiC and GaN power semiconductor includes the following segments:

|

Segment |

Sub-segment |

|

Product Type |

|

|

Application |

|

|

Power Range |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

SiC and GaN Power Semiconductor Market - Regional Analysis

North America Market Insights

North America SiC and GaN power semiconductor market is witnessing a significant share of approximately 35% by the end of 2035. The region has a well- established innovation ecosystem, while showcasing the presence of leading semiconductor manufacturers. At the same time, the increasing adoption of electric vehicles and growing focus on domestic chip manufacturing are anticipated to boost market growth during the forecast period.

The U.S. represents the largest market in North America due to its strong semiconductor manufacturing base and growing investment in domestic chip production. Where government initiatives that include CHIPS and the Science Act are encouraging the expansion of chip manufacturing, which creates favorable opportunities for the use of SiC and GaN power semiconductors.

Canada market is strengthening its position in the market by enhancing semiconductor research and supporting the electric vehicle supply chain. The country is also investing in critical minerals and advanced materials that are needed for semiconductor manufacturing. These efforts are encouraging the wider adoption of SiC and GaN power semiconductors over the forecast period.

Europe Market Insights

Europe market is anticipated to witness stable growth, which is supported by the region's focus on clean energy, electric mobility, and semiconductor production. Meanwhile, supportive government policies are strengthening Europe’s semiconductor ecosystem strong, are expected to contribute to market growth throughout the forecast period. Increasing investments in domestic chip manufacturing and the rising use of energy-efficient power technologies are creating favorable opportunities for the market.

Germany registers as one of the leading markets in Europe because of its strong automotive industry and advanced manufacturing capabilities. The country's growing electric vehicle production is increasing the demand for SiC power semiconductors used in traction inverters and charging systems. Moreover, ongoing investments in semiconductor manufacturing are expanding domestic production capacity of advanced power semiconductors.

France market is strengthening its position because of enhancing semiconductor manufacturing and supporting the development of power electronics. The country is attracting investments in advanced chip production while encouraging research and innovation in wide-bandgap semiconductor technologies. These efforts are expected to encourage the wider availability of SiC and GaN devices across Europe.

APAC Market Insights

Asia Pacific market is projected to hold a significant share, encouraged by its well-established chip manufacturing ecosystem and large electronics production base. The further expansion of electric vehicles, renewable energy, and chip manufacturing is creating favorable opportunities for the market. Moreover, government policies aimed at developing the chip industry are expected to support the large use of SiC and GaN power semiconductors across the region over the forecast period.

Japan SiC and GaN power semiconductor market remains an important contributor through its expertise in power chip materials and device development. The country is home to several leading manufacturers that are increasing the production of SiC power devices to meet the growing requirements of electric vehicles and industrial applications. Over the forecast period, because of continued investment in chip innovation, the market is expected to witness Japan’s stable position.

China SiC and GaN power semiconductor market is expanding because of domestic chip production and the development of local supply chains. The country is encouraging greater self-reliance in advanced semiconductor technologies while supporting the expansion of electric mobility and power electronics. This ongoing focus is anticipated to create favorable opportunities for SiC and GaN power semiconductor manufacturers over the forecast period.

Key SiC and GaN Power Semiconductor Market Players:

- Wolfspeed, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- ROHM Co., Ltd. (Japan)

- onsemi(U.S.)

- Navitas Semiconductor (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Wolfspeed, Inc. is a key player in the SiC power semiconductor market that is paying attention on the development of SiC materials and power devices for electric vehicles, renewable energy, and industrial applications. The company is working on enhancing its production capabilities to meet the rising demand for efficient and high-performance power solutions.

- Infineon Technologies AG offers SiC and GaN power semiconductor solutions for automotive, industrial, and energy applications. The company focuses on improving product performance, expanding manufacturing capabilities, and meeting the growing demand for efficient power devices.

- STMicroelectronics provides SiC and GaN-based semiconductor products used in applications that require better efficiency and power control. The company is working on technology development and production expansion to support the increasing use of advanced power electronics.

Here is a list of key players operating in the global market:

The rising demand for efficient power electronics in electric vehicles, industrial systems, renewable energy, and data centers is helping companies to focus more on SiC and GaN power semiconductor solutions. Manufacturers are developing devices with improved efficiency, thermal performance, and reliability while also growing production capacity to support rising market need. Along with internal technology development, collaborations with automotive manufacturers, system developers, and technology providers are helping companies introduce new solutions across different applications. Therefore, improvements in supply chain operations are further supporting companies in meeting the increasing demand for advanced power devices.

Corporate Landscape of the Market:

Recent Developments

- In March 2024, Infineon Technologies AG introduced its next-generation CoolSiC™ MOSFET Generation 2 technology, paying attention on improving efficiency and reducing power losses in applications such as EV charging, renewable energy, and industrial power systems. The company also continued rising its SiC and GaN technology portfolio for high-efficiency power applications.

- In September 2025, Wolfspeed, Inc. announced the commercial launch of its 200mm silicon carbide materials portfolio, aimed at improving production scalability and helping the increasing demand for SiC-based power devices used in electric vehicles, energy systems, and industrial applications.

- Report ID: 8440

- Published Date: Jul 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.