Connected Mining Market Outlook:

Connected Mining Market size was valued at USD 19.4 billion in 2025 and is projected to reach USD 56.8 billion by the end of 2035, rising at a CAGR of 11.3% during the forecast period, 2026 to 2035. In 2026, the industry size of connected mining is estimated at USD 21.6 billion.

The connected mining market is expanding as governments and mining operators increase investment in digital infrastructure, automation support, and industrial connectivity to improve productivity, worker safety, and resource efficiency. According to the IISD September 2023 data, lithium demand is rising by over 30%. This increase is placing pressure on mining operators to improve operational visibility, fleet coordination, predictive maintenance, and remote asset management across large extraction sites. The U.S. Geological Survey March 2025 data reported that the U.S. mine production value reached approximately USD 106 billion in 2024, reflecting continued capital deployment toward modernization and efficiency improvement in mineral extraction operations.

In parallel, the DOL 2025 data recorded the injuries in the mining sector rate was 1.74 per 200,000 hours worked over recent reporting periods, reinforcing industry demand for connected monitoring systems that support worker tracking, environmental sensing, and centralized operational control. Governments are also increasing funding toward industrial broadband and smart infrastructure programs that indirectly support mining digitization in remote regions. Industrial connectivity investments are also being supported through national infrastructure programs. For example, the U.S. National Telecommunications and Information Administration allocated a billion dollars to expand high-speed connectivity in underserved areas, including industrial corridors and remote mining regions. These developments are driving the demand for market growth.

Key Connected Mining Market Insights Summary:

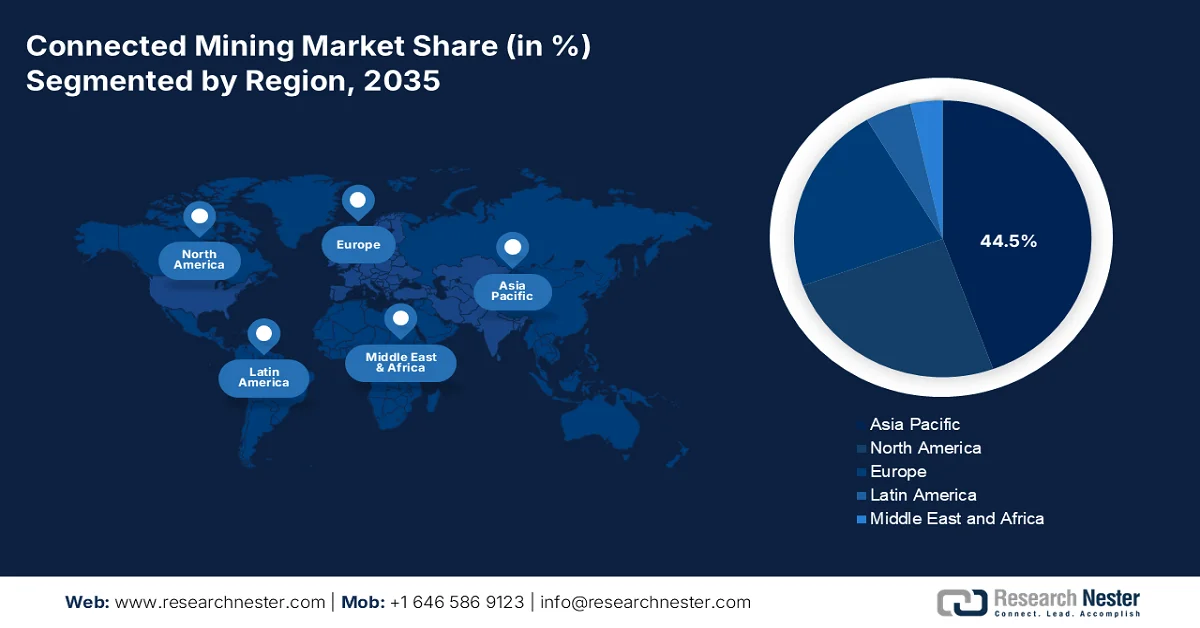

Regional Insights:

- Asia Pacific is anticipated to command 44.5% of the connected mining market share by 2035, underpinned by rapid mechanization of coal and metal mines, government-backed critical minerals self-sufficiency targets, and the need to improve safety in deep underground operations

- North America is projected to witness notable expansion throughout 2026–2035, fueled by stringent safety enforcement, rising critical minerals demand, and the growing need to automate remote operations

Segment Insights:

- The solutions sub-segment is projected to account for 79.5% of the connected mining market share by 2035, bolstered by the increasing focus on worker safety and regulatory compliances

- Surface mining is expected to maintain its leading position in the mining type segment through 2035, supported by large-scale open-pit operations that readily integrate wireless networks, autonomous haulage, and real-time fleet analytics alongside strong regulatory backing for land restoration

Key Growth Trends:

- Expansion of industrial broadband and remote connectivity

- Government investment in critical mineral supply chains

Major Challenges:

- Interoperability issues with legacy mining equipment

- Harsh environmental conditions affecting hardware reliability

Key Players: Caterpillar Inc. (U.S.),Komatsu Ltd. (Japan),Rockwell Automation (U.S.),ABB Ltd. (Switzerland),Sandvik AB (Sweden),Hitachi Construction Machinery (Japan),Hexagon AB (Sweden),Siemens AG (Germany),Epiroc AB (Sweden),Cisco Systems, Inc. (U.S.),Nokia Corporation (Finland),SAP SE (Germany),MineSense Technologies Ltd. (Canada),RCT Global (Australia),Hyundai Heavy Industries (South Korea),Vedanta Limited (India),Huawei Technologies Co., Ltd. (China),Malaysia Digital Economy Corporation (MDEC) (Malaysia),Tata Consultancy Services (TCS) (India),Doosan Corporation (South Korea).

Global Connected Mining Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 19.4 billion

- 2026 Market Size: USD 21.6 billion

- Projected Market Size: USD 56.8 billion by 2035

- Growth Forecasts: 11.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (44.5% share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Australia, Canada, India

- Emerging Countries: Indonesia, Chile, Brazil, Saudi Arabia, Mexico

Last updated on : 4 June, 2026

Connected Mining Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of industrial broadband and remote connectivity: Public investment in broadband infrastructure is directly supporting connected mining adoption, especially in remote extraction zones where real-time operational monitoring has historically been limited. The TRAI April 2026 data depicted that USD 42.45 billion is allocated through the Broadband Equity, Access, and Deployment (BEAD) Program to expand high-speed internet infrastructure across underserved industrial regions. Mining operators are leveraging these expanded networks to support centralized fleet management, remote diagnostics, environmental monitoring, and worker communication systems. Increased industrial broadband deployment across North America and Australia is expected to accelerate investment in connected underground communication systems and cloud-based mining coordination platforms.

- Government investment in critical mineral supply chains: Government-backed critical mineral programs are significantly increasing demand for connected mining infrastructure. Mining operators are under pressure to improve extraction efficiency, workforce visibility, and operational continuity as governments accelerate domestic mineral production. In the United States, the Department of Energy February 2022 announced more than USD 2.91 billion in funding to strengthen domestic mineral and battery supply chains. These programs require mining companies to improve production monitoring, equipment coordination, and reporting systems across remote operations. Connected operational systems are becoming necessary to manage geographically distributed sites and comply with federal reporting requirements.

Challenges

- Interoperability issues with legacy mining equipment: Most active mines operate mixed fleets of older machinery from different original equipment manufacturers. New connected solution providers face immense difficulty integrating their software with proprietary telematics protocols used by Caterpillar, Komatsu, Hitachi, and Sandvik. Without universal communication standards, suppliers must build custom APIs for each OEM, driving up development costs.

- Harsh environmental conditions affecting hardware reliability: Mining environments expose connected devices to extreme dust, vibration, humidity, temperature swings, and electromagnetic interference. Consumer-grade or industrial-grade components fail within weeks underground. Entrants must invest heavily in ruggedization, IP68-rated enclosures, and MIL-STD shock resistance, which increases bill-of-materials costs.

Connected Mining Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.3% |

|

Base Year Market Size (2025) |

USD 19.4 billion |

|

Forecast Year Market Size (2035) |

USD 56.8 billion |

|

Regional Scope |

|

Connected Mining Market Segmentation:

Component Segment Analysis

Under the component segment, the solutions sub-segment is dominating and is poised to hold the share value of 79.5% by the end of 2035. The segment is driven due to the focus on worker safety and regulatory compliances. Solutions include fleet management systems, predictive analytics dashboards, real‑time safety monitoring, and cloud‑based data integration services. Unlike discrete hardware components, solutions offer continuous value through automated alerts, remote equipment control, and production optimization workflows. Mining operators prefer bundled solution packages because they reduce internal IT burdens, enable seamless scalability across multiple sites, and provide actionable intelligence without requiring deep data science expertise. This preference for integrated, subscription‑ready offerings ensures that solutions remain the dominant component category, driving nearly half of all connected mining investments globally.

Mining Type Segment Analysis

Surface mining dominates the mining type segment in the market due to large-scale open-pit operations that readily integrate wireless networks, autonomous haulage, and real‑time fleet analytics. The sub-segment also benefits from strong regulatory backing for land restoration. In May 2026, the Office of Surface Mining Reclamation and Enforcement announced nearly USD 679.4 million in abandoned mine land reclamation grants for eligible states and tribes. This funding directly addresses legacy surface mining hazards such as unstable highwalls, open pits, and acid mine drainage. By mandating real‑time environmental monitoring and drone-based topographic surveys for reclamation projects, such initiatives further drive the adoption of connected technologies across surface mining operations, reinforcing its leadership.

End user Segment Analysis

Metal mining leads the market due to high commodity values and early adoption of automation, real-time grade control, and ore tracking. Copper in particular has demonstrated strong production momentum. Copper mine production achieved a compound annual growth rate of approximately 2.4% as per the Government of India 2025 data, with mining capacity projected to reach approximately 32 MT within the next five years. This sustained expansion forces copper operators to deploy connected technologies, including AI-based ore sorting, conveyor monitoring, and mill throughput optimization to maximize recovery from lower‑grade ores. As copper production scales toward 32 MT, the need for real-time data integration between pit and processing plant will further cement metal mining as the dominant end‑user segment.

Mine Production in Terms of Metals

|

Year |

Production (MT) |

|

2019 |

20.4 |

|

2020 |

20.6 |

|

2021 |

21.0 |

|

2022 |

21.9 |

|

2023 |

22.4 |

|

2024 |

23.0 |

Source: Government of India 2025

Our in-depth analysis of the connected mining market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Mining Type |

|

|

Technology |

|

|

Application |

|

|

Communication Type |

|

|

Operation |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Connected Mining Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating the connected mining market and is expected to hold the regional revenue share of 44.5% by the end of 2035. The market is driven by rapid mechanization of coal and metal mines, government-backed critical minerals self-sufficiency targets, and the need to improve safety in deep underground operations. China leads with state-directed deployment of autonomous haulage and real-time gas monitoring across large-scale coal complexes. Australia follows with widespread adoption of tele-remote operating centers and autonomous drill systems in iron ore and lithium mines. India focuses on retrofittable collision avoidance and personnel tracking systems to reduce fatalities in older underground workings. Japan and South Korea contribute advanced sensor and robotics technologies. Indonesia, Malaysia, and other Southeast Asian nations are gradually implementing digital ventilation monitoring and fleet management. Workforce shortages and stricter environmental reporting requirements accelerate regional demand for connected solutions.

Large-scale investments in intelligent mining systems, industrial automation, and digital infrastructure upgrades across coal and metal extraction operations is driving the market in China. According to the IGDP July 2024 data, the country produced approximately 4.66 billion tonnes of raw coal, reinforcing demand for integrated monitoring, communication, and automated operational systems across mining sites. In addition, the country’s rising 5G base stations is supporting industrial connectivity expansion in remote production regions, including mining corridors. Mining enterprises are increasingly implementing AI-enabled monitoring, autonomous haulage, and centralized operational platforms to improve productivity, worker safety, and resource management efficiency across large-scale extraction projects.

The Japan connected mining market is expected to expand from USD 669.2 million in 2025 to USD 1,598.8 million by 2035 at a CAGR of 9.1% over the forecast period from 2026 to 2035. The market poised to reach USD 730.2 million by the end of 2026. The market is driven by the long-standing mining heritage and growing focus on preserving and modernizing mineral resource management practices. Historical records from Sado Island, highlighted by the Government of Japan in June 2022, show that traditional gold production methods achieved gold purity levels of 99.54%, supported by highly organized mining settlements and coordinated production systems. The preservation of over 100 historical mining process scrolls and mining infrastructure also reflects Japan’s continued institutional investment in mining knowledge management and industrial documentation systems.

North America Market Insights

The North America is projected to emerge rapidly during the assessed period, 2026 to 2035 in the market. The market is driven by the stringent safety enforcement, critical minerals demand, and the need to automate remote operations. The United States drives adoption through federal mandates requiring electronic proximity detection, real-time ventilation monitoring, and digital reclamation reporting. Canada follows closely with provincial investments in tele-remote operating centers that allow urban-based personnel to manage underground equipment from distance. Cross-border interoperability standards and shared tailings dam monitoring requirements further unify the regional market, creating steady demand for ruggedized sensors, wireless networks, and predictive maintenance software across active coal, metal, and mineral mines.

The rising federal support for domestic mineral production, industrial automation, and digital infrastructure modernization is shaping the market in the U.S. According to the U.S. Energy Information Administration, April 2025 data, U.S. coal production reached approximately 578 million short tons, highlighting the continued scale of mining operations requiring advanced monitoring and operational coordination systems. In addition, the private construction spending for manufacturing facilities, reflecting broader industrial digitization investments that also support mining technology deployment and industrial connectivity expansion. Mining companies are increasingly investing in remote asset monitoring, predictive maintenance, and integrated operational control systems to improve productivity, workforce safety, and supply-chain resilience across critical mineral and metal extraction activities.

The digital infrastructure investments across critical mineral extraction projects is shaping the connected mining market in Canada. Start Company Formations April 2025 data reported that the country’s mineral production value reached approximately USD 71.9 billion in 2023, supported by strong output in gold, potash, copper, and nickel mining activities. In addition, Statistics Canada stated that capital expenditures in the mining and quarrying sector reflects a continued investment in automation, operational connectivity, and equipment modernization. Mining companies across Ontario, Quebec, and British Columbia are increasingly deploying connected fleet management, remote monitoring, and predictive maintenance systems to improve operational efficiency and workforce safety while supporting Canada’s expanding role in global battery mineral and clean energy supply chains.

Europe Market Insights

The Europe market is shaped by stringent environmental regulations, carbon reduction mandates, and a strong focus on worker safety across deep underground operations. Germany and Poland lead in deploying real-time ventilation monitoring and methane detection systems in active coal mines. The Nordic countries—Sweden, Finland, and Norway—drive adoption of autonomous haulage, battery-electric fleet management, and digital twin technology in metal and mineral mines. Russia focuses on retrofittable collision avoidance and remote operation centers for its vast Arctic and Siberian mining zones. The European Union's critical raw materials strategy pushes member states toward real-time grade control and ore tracking solutions. Cross-border tailings dam monitoring standards and energy efficiency reporting requirements further accelerate demand for connected technologies across the continent.

Increased government-backed industrial investment programs aimed at strengthening critical raw material supply chains and advanced industrial infrastructure is driving the connected mining market in Germany. The German government announced that projects supported through the state-owned development bank KfW will be eligible for funding between USD 58 million and USD 174 million, supporting large-scale industrial modernization and resource-related projects, as per the GTAI June 2025 data. This financial support is encouraging mining and raw material operators to adopt connected operational systems, automated monitoring, and digital infrastructure to improve efficiency and supply-chain security. Rising investment in industrial connectivity and strategic mineral projects is expected to support broader deployment of intelligent mining technologies across Germany.

The industrial digitalization and critical mineral supply chain development initiatives is shaping the market in UK. According to the Government of UK 2024 data, more than USD 1.76 billion was allocated in 2023 to strengthen digital infrastructure and advanced connectivity programs across industries. In addition, the UK Critical Minerals Intelligence Centre reported that the country identified critical minerals essential for energy transition and industrial manufacturing, increasing focus on secure mineral sourcing and operational efficiency. Mining and resource companies are increasingly adopting connected monitoring systems, predictive analytics, and remote operational technologies to improve productivity, compliance, and infrastructure coordination across extraction and processing activities.

Key Connected Mining Market Players:

- Caterpillar Inc. (U.S.)

- Komatsu Ltd. (Japan)

- Rockwell Automation (U.S.)

- ABB Ltd. (Switzerland)

- Sandvik AB (Sweden)

- Hitachi Construction Machinery (Japan)

- Hexagon AB (Sweden)

- Siemens AG (Germany)

- Epiroc AB (Sweden)

- Cisco Systems, Inc. (U.S.)

- Nokia Corporation (Finland)

- SAP SE (Germany)

- MineSense Technologies Ltd. (Canada)

- RCT Global (Australia)

- Hyundai Heavy Industries (South Korea)

- Vedanta Limited (India)

- Huawei Technologies Co., Ltd. (China)

- Malaysia Digital Economy Corporation (MDEC) (Malaysia)

- Tata Consultancy Services (TCS) (India)

- Doosan Corporation (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Caterpillar Inc. is dominating the connected mining market and leverages its Cat® MineStar™ ecosystem to deliver industry-leading fleet management, autonomous haulage, and real-time machine health analytics. The company integrates onboard sensors, satellite communications, and AI-driven diagnostics to optimize truck and shovel operations.

- Komatsu Ltd. strengthens its position in the market via its FrontRunner autonomous haulage system and the Komatsu Connectivity solutions. By embedding IoT modules and edge computing into dump trucks, drills, and loaders, the company enables seamless data exchange between equipment and control centers.

- Rockwell Automation addresses the connected mining market with its FactoryTalk® and Pavilion8® software platforms, which unify control information and predictive analytics for mineral processing and material handling.

- ABB Ltd. competes in the market through its ABB Ability™ portfolio, which includes eMine™ for electrification and automated hoisting systems with real-time vibration monitoring. In 2024, the company has made a revenue of USD 1.54 billion.

- Sandvik AB advances the market with its AutoMine® platform for underground loaders and trucks, alongside OptiMine® for data analytics and process optimization. In 2024, the company has made 51% of revenue in mining.

Here is a list of key players operating in the global market:

The connected mining market is moderately fragmented, dominated by industrial giants leveraging IIoT and AI for autonomous operations. Key players from the USA, Europe, and Australia lead through strategic initiatives such as partnerships with telecom providers, acquisitions of analytics startups, and development of interoperable software platforms. For example, in November 2024, Hexagon announced the acquisition of Indurad. Europe firms focus on sustainability-driven automation, while Japan and South Korea companies contribute advanced sensor and robotics technology. India and Malaysia players are emerging through cost-effective solutions and local government digitalization mandates. Major strategies include launching predictive maintenance suites, autonomous haulage systems, and cloud-based fleet management to reduce downtime and enhance safety.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, Epiroc launched a comprehensive set of digital mine planning solutions to strengthen the mining companies’ operations. The launch marks a milestone in Epiroc’s strategy to consolidate its digital technology acquisitions into one connected offering, bringing together years of integration, development, and deep mining domain expertise.

- In April 2025, Hitachi Construction Machinery Co., Ltd. announced the development of the LANDCROS Connect Insight solution, which analyzes the operational data of mining machinery collected in near-real time to help customers increase the efficiency of their operations.

- In September 2024, Komatsu announced the launch of the new Modular ecosystem, an expanding set of interconnected platforms and products which is designed to simplify existing workflows while creating a bold vision for the future of mine site optimization and data utilization.

- Report ID: 7912

- Published Date: Jun 04, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Connected Mining Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.