Cognac & Brandy Market Outlook:

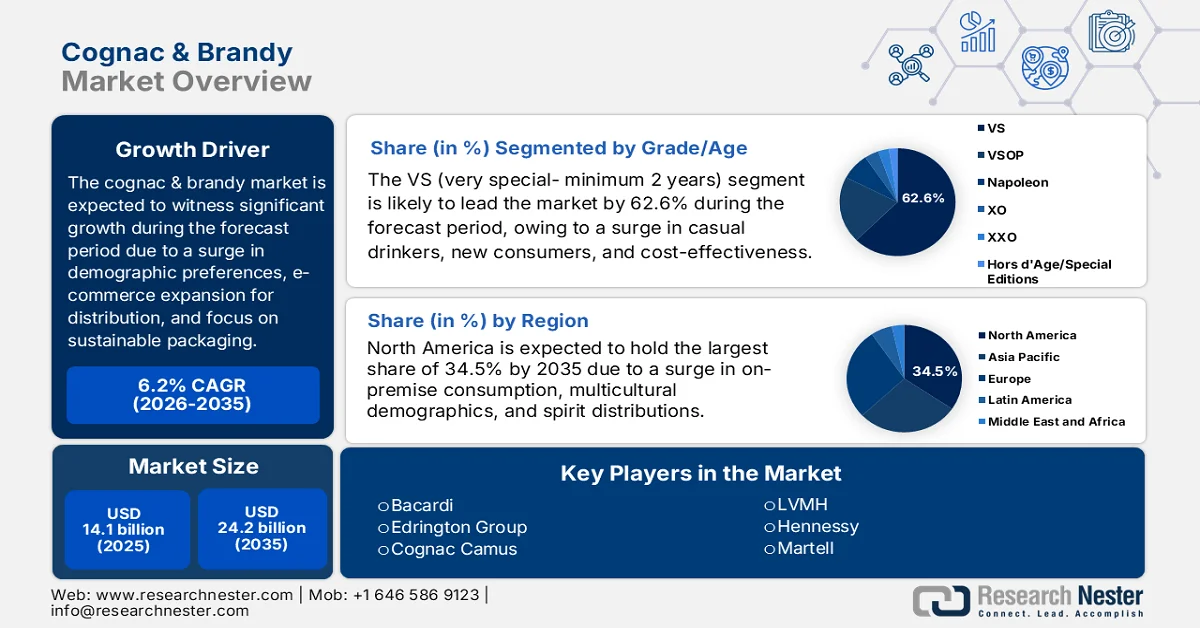

Cognac & Brandy Market size was valued at over USD 14.1 billion in 2025 and is expected to reach USD 24.2 billion by the end of 2035, growing at a CAGR of 6.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of cognac & brandy is assessed at USD 14.9 billion.

The global cognac & brandy market is being significantly shaped by factors, including sustainable packaging materials, conventional barrels for aging, shift in demographic preferences, and the rapid expansion of e-commerce for distribution. According to official statistics published by NLM in August 2022, in terms of packaging materials, the chemical composition of cork comprises of 0.7% ash, 15.3% total extractives, 38.6% of suberin, 21.7% of lignin, and 18.2% of polysaccharides. In addition, the carbohydrate composition analysis demonstrates that glucose represents 50.6% of overall monosaccharides, along with 35% of xylose, 7% of arabinose, 3.6% of galactose, and 3.4% of mannose, respectively. Therefore, based on these compositions, there is a huge demand for cork through continuous supply across different countries, which is positively uplifting the market growth.

Global Corks and Stoppers, Natural Cork Export/Import Analysis (2024)

|

Countries/Components |

Export (USD) |

Import (USD) |

|

Portugal |

425 million |

- |

|

France |

22.1 million |

110 million |

|

Spain |

22.1 million |

- |

|

U.S. |

- |

143 million |

|

Italy |

- |

52.7 million |

|

Global Trade Valuation |

532 million |

|

|

Global Trade Share |

Less than 0.005% |

|

Source: OEC

Furthermore, the rise of mindful drinking and health-conscious positioning, experiential e-commerce, digitalized transformation, along with the emergence of mizunara oak and cross-cultural innovation, are a few trends that are bolstering the market globally. As stated in an article published by Alcohol in March 2023, there is a continuous increase in aged people of more than 65 years, particularly in the U.S., eventually growing by 36%, which is equivalent to 54.1 million people. Besides, these people belong to the Baby Boomer generation, and are poised to be over 65 years by the end of 2030, indicating a demographic shift, which is known as the gray tsunami. Moreover, by the end of 2040, there will be approximately 80.8 million falling under this age category, which is gradually uplifting the market growth and exposure.

Key Cognac & Brandy Market Insights Summary:

Regional Highlights:

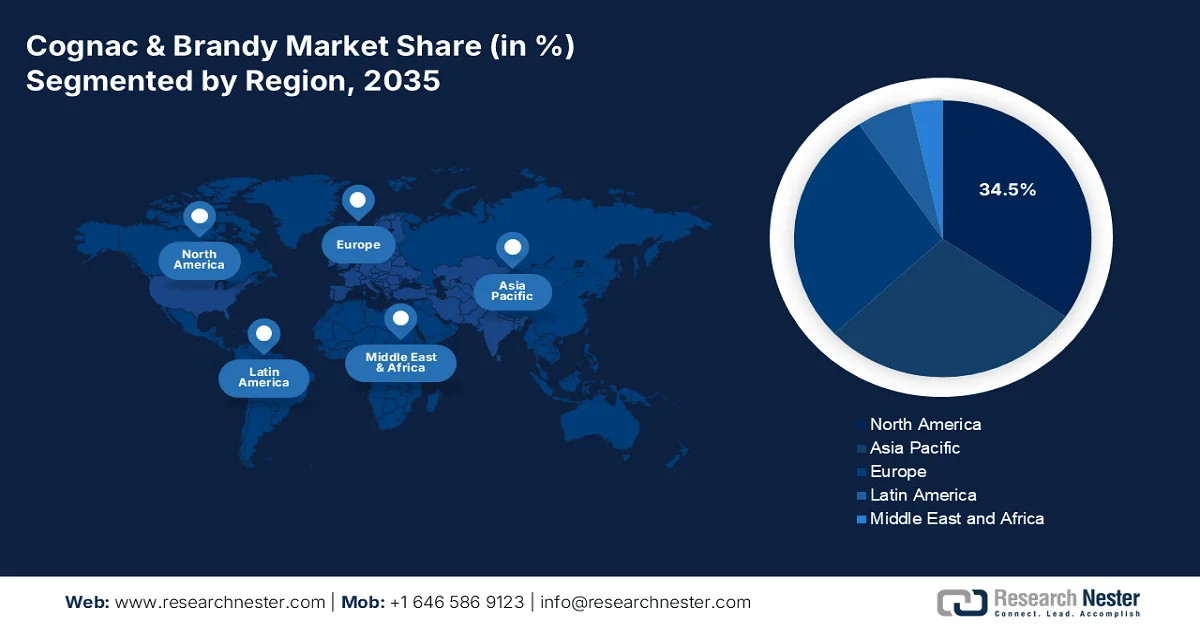

- North America in the cognac & brandy market is projected to secure a 34.5% share by 2035, attributed to the resurgence of on-premise consumption alongside expanding premium spirits distribution and rising social media-driven brand awareness

- Europe is poised to witness the fastest growth in the forecast period, fueled by strong heritage branding, evolving cocktail culture, and increasing premiumization trends

Segment Insights:

- The VS (Very Special- minimum 2 years) sub-segment in the cognac & brandy market is expected to account for a dominant 62.6% share by 2035, driven by its affordability, mixability, and growing appeal among new and casual consumers

- The off-trade retail segment is projected to capture the second-largest share over 2026-2035, owing to rising at-home consumption, premium gifting demand, and expanding retail distribution across key regions

Key Growth Trends:

- Expansion in the craft beverage ecosystem

- Increase in ultra-premium spirits

Major Challenges:

- Geopolitical trade barriers and tariff volatility

- Shifting consumer preferences toward low-ABV and no-alcohol alternatives

Key Players: ThaiBev (Thailand), Brown‑Forman (U.S.), Pernod Ricard (France), William Grant & Sons (UK), Diageo (UK), Rémy Cointreau (France), Bacardi (Bermuda), Edrington Group (UK), Cognac Camus (France), Constellation Brands (U.S.), LVMH (France), Hennessy (France), Martell (France), Rémy Martin (France), Courvoisier (France), Suntory (Japan), Radico Khaitan (India), Campari Group (Italy), Alliance Global Group (Philippines), Hine/EDV SAS (France), D'USSÉ cognac (France).

Global Cognac & Brandy Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 14.1 billion

- 2026 Market Size: USD 14.9 billion

- Projected Market Size: USD 24.2 billion by 2035

- Growth Forecasts: 6.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (34.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, France, China, United Kingdom, Germany

- Emerging Countries: India, Brazil, South Korea, Mexico, Vietnam

Last updated on : 15 April, 2026

Cognac & Brandy Market - Growth Drivers and Challenges

Growth Drivers

- Expansion in the craft beverage ecosystem: The explosive growth of the wide-ranging craft beverage movement is one of the significant drivers for the cognac & brandy market globally. According to official statistics published by Invest India in January 2025, India has successfully placed itself in the global single malt industry and significantly captured 53% sales as of 2023. Besides, the alcobev industry readily employs an astounding 8 million people, both directly and indirectly, and also accounts for 1.5% of the country’s overall workforce. This particular industry offers employment opportunities in retail, supply chain, and production, and supports localized economies. Besides, Extra Neutral Alcohol, which is a crucial raw material utilized in alcoholic beverages, offers suitable job opportunities for farmers for almost 724,611 farms and 3,623,057 farmers for grain production, thus suitable for uplifting the market demand.

- Increase in ultra-premium spirits: This is yet another specific driver for the market, which is rapidly expanding across secondary cities. As stated in an article published by the MDPI in January 2024, spirit beverages effectively account for 36.5% of the worldwide alcoholic drinks industry, and are considered the largest segment, with a valuation worth USD 408.8 billion as of 2023. In addition, this particular industry is expected to grow at 23% by the end of 2028 and reach USD 1,373.9 billion. Besides, as per the December 2024 European Research on Management and Business Economics article, the global luxury goods industry is valued at USD 346.1 billion as of 2023. This industry has also encompassed expensive, status-oriented, and high-quality products, which include cognac & brandy alcoholic products, thus fueling the market demand globally.

- Surge in tourism hotspots: Unlike general off-trade retail, a specific driver for the market is the resurgence of the on-trade channel within luxury travel retail and hospitality. As foreign tourism rebounds, airport duty-free stores and high-end hotels in regions such as the Middle East (Dubai) and Europe are reporting strong sales of premium aged brandies. These particular channels are crucial for driving trial and brand prestige, as consumers are more willing to purchase expensive XO or Hors d'Age bottles when in a vacation mindset. In addition, this recovery is particularly strong in Macau and Singapore, where integrated resorts are expanding their luxury spirit offerings to cater to high-net-worth travelers, thereby making it suitable for expanding the market exposure globally.

Challenges

- Geopolitical trade barriers and tariff volatility: The cognac & brandy market is among the most trade-sensitive industries in the consumer goods and food sector, deliberately creating extreme vulnerability to bilateral trade disputes. For instance, China, which is the fastest-growing market for French spirits, initiated an anti-dumping investigation on Europe-based brandies following regional tariffs on China-specific electric vehicles. Provisional duties were proposed, and a similar precedent occurred when the U.S. imposed tariffs on single-malt scotch and Cognac during the Airbus-Boeing dispute, causing a drop in U.S. Cognac imports within six months. These tariffs cannot be quickly mitigated because brandy production requires multi-year aging; producers cannot reroute inventory intended for China to Europe without disrupting long-term distributor relationships.

- Shifting consumer preferences toward low-ABV and no-alcohol alternatives: A generational shift in drinking habits poses a long-term demand-side roadblock for the market. Among consumers aged from 21 to 35 years in North America and Western Europe, per-capita spirits consumption has declined. This cohort increasingly prioritizes health and wellness, opting for no-alcohol spirits, low-ABV aperitifs, and functional beverages over high-proof brandy. The rise of sober curiosity and Dry January campaigns, currently formalized in UK government health guidelines, has normalized zero-proof alternatives. Furthermore, brandy lacks the cultural mixability of vodka or whiskey, while younger drinkers perceive cognac as an older generation’s status symbol rather than a daily cocktail ingredient.

Cognac & Brandy Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.2% |

|

Base Year Market Size (2025) |

USD 14.1 billion |

|

Forecast Year Market Size (2035) |

USD 24.2 billion |

|

Regional Scope |

|

Cognac & Brandy Market Segmentation:

Grade/Age Segment Analysis

The VS (very special- minimum 2 years) sub-segment, part of the grade/age segment, is anticipated to garner the highest share of 62.6% in the cognac & brandy market by the end of 2035. The sub-segment’s upliftment is primarily attributed to appealing to new consumers, casual drinkers, and the bar trade due to its affordability, vibrant fruit-forward profile, and mixability in classic cocktails such as the Sidecar and French Connection. According to BNIC regulations, VS cognacs must use eaux-de-vie where the youngest component is at least two years old, though many houses extend aging to three or four years for smoother blends. Key players, including Hennessy VS, Courvoisier VS, and Rémy Martin VS, dominate this space through aggressive marketing campaigns targeting younger demographics in North America and Europe, thus proliferating the sub-segment’s growth.

Distribution Channel Segment Analysis

Based on the distribution channel, the off-trade retail segment is projected to grab the second-highest share in the market during the forecast period. The segment’s growth is highly driven by enabling at-home consumption, serving as a suitable channel for premium gifting, and driving volume in the Asia Pacific and North America. According to official statistics published by OECD in November 2025, the per capita yearly alcohol consumption averaged 8.5 liters of pure alcohol across different countries as of 2023. For instance, Portugal and Latvia constitute the highest consumption, along with Romania, reaching more than 11.5 liters yearly. Therefore, retail shops in these locations are readily focused on distributing hard liquor, such as brandy, based on rigorous import and export, which is positively uplifting the market expansion and development globally.

Global Hard Liquor Export and Import Analysis (2024)

|

Countries/Component |

Export (USD) |

Import (USD) |

|

UK |

9.2 billion |

- |

|

Mexico |

6.1 billion |

- |

|

France |

5.4 billion |

- |

|

U.S. |

- |

11.1 billion |

|

China |

- |

2.0 billion |

|

Germany |

- |

1.8 billion |

|

Global Trade Valuation |

41.3 billion |

|

|

Global Trade Share |

0.18% |

|

Source: OEC

Price Tier Segment Analysis

By the end of the stipulated timeline, the premium segment, which is part of the price tier, is expected to account for the third-highest share in the cognac & brandy market. The segment’s development is highly propelled by a combination of strict production constraints, quality and rarity of the finalized product, and lengthy aging processes. As per a data report published by the Distilled Spirits Council of the U.S. in June 2022, the total alcohol promotional sales accounted for a 32.4%, with more than 20% changes. Besides, this particular segment is significantly responsible for almost 69% of spirits valuation, based on which the price tier caters to 34.3% in the U.S. Besides, the premium pricing is further categorized into super-premium and ultra-premium, which positively impacts the spirits industry, thereby making it suitable for the segment to expand globally.

U.S. Spirits Industry Analysis by Premium Price Category (2022)

|

Price Category |

Range |

Growth |

|

Premium |

USD 22.5 to USD 29.9 |

7% |

|

Super Premium |

USD 30.0 to USD 44.9 |

8.3% |

|

Ultra-Premium |

USD 45.0 to USD 99.9 |

12.4% |

Source: Distilled Spirits Council of the U.S.

Our in-depth analysis of the cognac & brandy market includes the following segments:

|

Segment |

Subsegments |

|

Grade/Age |

|

|

Distribution Channel |

|

|

Price Tier |

|

|

Product Type |

|

|

Flavor Profile |

|

|

Packaging Type |

|

|

Alcohol Content |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cognac & Brandy Market - Regional Analysis

North America Market Insights

North America in the cognac & brandy market is anticipated to garner the largest share of 34.5% by the end of 2035. The market’s upliftment in the region is primarily attributed to the sustained recovery of on-premise consumption at hotels, restaurants, and bars, along with an increase in multicultural demographics, and expansion in premium spirits distribution through provincial liquor brands. Besides, the continuous increase in bars and cafes in the region is making the population aware of the newest launches through social media, which readily supports the market growth. According to a data report published by Georgia Southern Commons in 2025, the U.S. comprises 169.6 million Instagram users, making it the second-largest audience in the world. In addition, Instagram has more than 500 million daily active users, and it has emerged as an essential marketing tool to receive updates on luxury brands and services as well as new bars and restaurants, which in turn is denoting a positive impact on the market growth.

The cognac & brandy market in the U.S. is growing significantly, owing to the strong premiumization trend, an increase in cocktail culture, stabilization and recovery, celebrity partnerships and tactical marketing strategies, social media engagement and digital influence, notable metro economy focus, and modest bright spots amid category decline. As stated in a data report published by the Tales of the Cocktail Foundation Organization in May 2024, the organization successfully generated an overall economic impact of USD 24 million as of 2023, demonstrating an 8.7% increase from 2022. In addition, it has effectively recycled 3,675 pounds of glass bottles through suitable partnerships, which positively impacts the market growth in the country. Besides, the continuous spirits import values and volumes are also positively impacting the cocktail consumption, which is also responsible for bolstering the market expansion in the country.

Spirits Import by Values and Volume in the U.S. (2019-2023)

|

Year |

Values (USD Million) |

Volume |

|

2019 |

10.8 |

0.8 |

|

2020 |

3.1 |

0.4 |

|

2021 |

4.3 |

0.5 |

|

2022 |

3.3 |

0.6 |

|

2023 |

5.8 |

0.8 |

Source: USDA

The aspect of the fastest economy, an increase in disposable income of consumers, the growing popularity of premium and craft spirits, changing consumer preferences for innovative and unique flavors, and the expansion in the demand for the lucrative spirit segment are certain factors that are uplifting the market in Canada. As per an article published by the CCBC Organization in September 2024, there has been an increase in spirits consumption by the population, with sales worth USD 3 billion as of 2022. In addition, there is a growing trend in the consumption, owing to a reduction in beer sales volume, denoting a decline by 10%. Besides, spirits represent 35% of the overall alcoholic beverages industry in the country, which effectively boosts the sales of ready-to-drink beverages and spirits. Both these spirit types presently occupy 8% and 26% of the industry, thereby significantly proliferating the market growth in the country.

Europe Market Insights

Europe in the cognac & brandy market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is highly propelled by a robust heritage branding, an expansion in the cocktail culture, premiumization trends, a shift in consumer preferences, and regulatory policies. According to a data report published by Spirits Europe in November 2024, the region is the ultimate center of excellence and producer of spirits, especially in the premium segment, indicating an 11% of worldwide spirits production in value. Based on this production, the region accounts for 39% of grape-based spirits, as well as 17% of liqueurs and cordials. Moreover, based on the exports and consumer preference for premium spirits, the region is significantly predicted to account for a 13% growth in the global spirits consumption by the end of 2028, thus positively fueling the market development.

The regulatory and historic heart of cognac production, limitations in releasing targeting collectors, heritage-based brands for emphasizing century-old craftsmanship, and the presence of modernized strategies to ensure traceability technologies to develop consumer trust and authenticate origin are a few trends that are developing the market in France. As stated in an article published by NLM in August 2023, the overall alcohol consumption in the country accounts for 11.4 liters per year per capita, which constitutes the potential to register 41,000 alcohol-based deaths every year. Besides the increased consumption, the country does not have any kind of national program on alcohol control and lacks evidence-specific measures on alcohol taxation. Therefore, based on these limitations, the market has both developing and limited growth opportunity in the country.

The cognac & brandy market in Germany is gaining increased traction, owing to a rise in the demand for artisanal and authentic spirits, innovation in sustainability and packaging for production processes, cost-effective premium choices for consumers requiring quality at competitive prices, and an escalation in the sale of imported hard drinks products. According to official statistics published by the Distilled Spirits Council of the U.S. in May 2023, the spirits industry in the country is highly dominated by imported spirits, which effectively account for almost 65% of the industry's value. Based on this, the country provides a combination of wealth, size, and a robust interest in premium imported distilled spirits. Additionally, premium spirits are extremely strong due to which the market is gradually developing in the country.

APAC Market Insights

The Asia Pacific in the cognac & brandy market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by an increase in disposable incomes, an expansion in luxury hospitality channels, growth in the cocktail culture across major economies, and the presence of digital-first marketing campaigns, along with tactical travel retail activations. According to official statistics published by the Hospitality Net Organization in March 2026, the region demonstrates a robust luxury hotel potential with Almaty readily leading at 69.5% occupancy, while ADR successfully reaching USD 1 to USD 400. In addition, this city provides an estimated 2,567 chain-based rooms, which include 659 luxury chain rooms. Therefore, with the availability of such hospitality, there is a huge demand for market exposure in the overall region.

The cognac & brandy market in China is gaining increased exposure, owing to international brands investing in digital-first marketing campaigns, an increase in immersive tasting experiences, the development of brandy variants with local flavor profiles for capturing young customers, and expansion in duty-free retail spaces across commercial and airport facilities. As stated in an article published by NLM in July 2022, the overall alcohol industry in the country is rapidly growing, with the most popular distilled spirit, baijiu, accounting for an increased output from 7 million tons, which is 5.7 liters per capita, to 13.5 million tons, which is 9.7 liters per capita. This particular spirit has experienced growth in the country owing to an increase in its consumption, which is positively uplifting the market growth.

The aspects of a surge in the need for aspirational spirits among millennials, an expansion of premium hospitality chains across metropolitan cities, the introduction of blended brandy products, modernized trade channels, and strategic partnerships are a few trends that are responsible for boosting the market in India. Based on government estimates published by the ITA in September 2022, the alcoholic beverage industry in the country is regarded as the world’s 3rd largest, which is significantly valued at USD 35 billion. In regard to this valuation, there has been an increase in importing distilled spirits to USD 319 million, demonstrating an outstanding 40% year-on-year (YoY) increase. Additionally, the U.S.-based exports of distilled spirits to the country surged by 114% on a YoY basis to USD 7 million, which is positively driving the market growth.

Key Cognac & Brandy Market Players:

- ThaiBev (Thailand)

- Brown‑Forman (U.S.)

- Pernod Ricard (France)

- William Grant & Sons (UK)

- Diageo (UK)

- Rémy Cointreau (France)

- Bacardi (Bermuda)

- Edrington Group (UK)

- Cognac Camus (France)

- Constellation Brands (U.S.)

- LVMH (France)

- Hennessy (France)

- Martell (France)

- Rémy Martin (France)

- Courvoisier (France)

- Suntory (Japan)

- Radico Khaitan (India)

- Campari Group (Italy)

- Alliance Global Group (Philippines)

- Hine/EDV SAS (France)

- D'USSÉ cognac (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- ThaiBev has strategically expanded its spirits portfolio beyond its core Southeast Asian markets by introducing brandy expressions tailored to local taste preferences. The company leverages its extensive distribution network across Thailand, Vietnam, and Cambodia to position brandy as an accessible premium option for emerging middle-class consumers.

- Brown‑Forman readily competes in the brandy segment primarily through its older heritage brands, focusing on aged expressions that appeal to traditional American consumers. The company emphasizes craft distillation methods and limited-batch releases to differentiate its brandy offerings from mass-market competitors.

- Pernod Ricard effectively maintains a strong foothold in the cognac category through its Martell brand, which is positioned as the oldest of the major cognac houses. The company focuses on storytelling around its heritage crus and invests heavily in experiential marketing across Asia's luxury gifting channels.

- William Grant & Sons has selectively entered the premium brandy space through acquisitions and limited-edition releases aimed at connoisseurs. The company leverages its family-owned independence to craft small-batch brandies that emphasize artisanal production values over volume sales.

- Diageo participates in the cognac and brandy market through a curated portfolio of premium and ultra-premium labels, distributed via its unparalleled global logistics network. The company focuses on cocktail culture marketing, positioning brandy as a versatile base spirit for modern mixology alongside its whiskey and vodka brands.

Here is a list of key players operating in the global market:

The global cognac & brandy market is highly consolidated, with French producers dominating the premium and ultra‑premium segments due to strict appellation laws and centuries‑old brand heritage. Moreover, notable players such as LVMH, Pernod Ricard, and Rémy Cointreau control the majority of the market, while Diageo and Bacardi maintain strong portfolios through global distribution networks. In response to trade tariffs in China and the U.S., leaders are diversifying into the Asia Pacific by launching limited‑edition aged expressions and expanding cocktail‑friendly offerings to attract younger consumers. Besides, in July 2025, D'USSÉ cognac successfully initiated a partnership-based deal with Ravyn Lenae, a Grammy-nominated rapper, singer, and songwriter, for introducing the latest D'USSÉ VSOP Magnum Edition bottle. This particular VSOP-driven cognac is aged almost 4.5 years, and was launched in Chicago, as well as at other consumer events in standard hotspots across the region, thereby making it suitable for bolstering the market.

Corporate Landscape of the Cognac & Brandy Market:

Recent Developments

- In October 2025, Hennessy (LVMH) effectively partnered with LeBron James, a global icon, to unveil the Hennessy V.S.O.P Limited Edition, thereby deliberately focusing on and ensuring excellence, sharing, and authenticity.

- In December 2023, Campari Group successfully acquired Courvoisier cognac from Beam Suntory and strengthened its very own portfolio of global brand priorities, especially in aged spirits, along with supporting long-lasting premiumization ambition across notable strategic segments.

- Report ID: 8514

- Published Date: Apr 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.