Coating Resins Market Outlook:

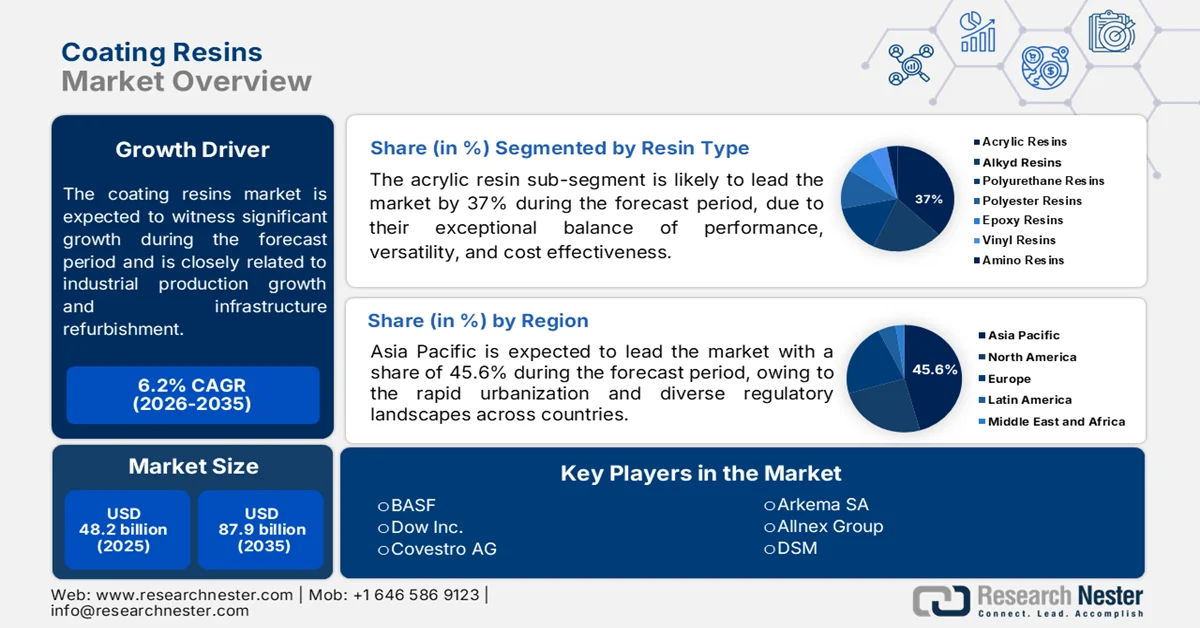

Coating Resins Market size was valued at USD 48.2 billion in 2025 and is projected to cross USD 87.9 billion by the end of 2035, rising at a CAGR of 6.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of coating resins is estimated at USD 51.1 billion.

The coating resins market is being shaped by industrial production growth, infrastructure refurbishment, automotive manufacturing recovery, and tightening environmental compliance requirements across North America, Europe, and the Asia Pacific. According to the U.S. Census Bureau, May 2026 data, the total U.S. construction spending for the month of March 2026 reached USD 2,185.5 billion, reflecting sustained investment across residential, commercial, and public infrastructure projects that directly support the demand for architectural and industrial coatings. The NIST March 2025 data indicated that manufacturing contributed more than USD 2.93 trillion to U.S. GDP, while the ACEA September 2024 data recorded global vehicle production above 93.9 million units in 2023, supporting coatings demand across OEM and refinish applications.

Environmental compliance continues to influence procurement strategies and resin selection. The U.S. Environmental Protection Agency maintains national volatile organic compound emission standards for architectural and industrial coatings, promoting the adoption of waterborne powder UV curable and high-solid resin systems. Similar regulatory direction in Europe via environmental sustainability frameworks is stimulating the transition toward lower-emission resin technologies for industrial users seeking compliance stability and lifecycle durability improvements. Moreover, the London South East August 2021 data indicates that titanium dioxide, which is the key pigment, used in volumes, rose by 45% YoY, with price volatility affecting resin-based coating formulation costs. Additionally, the European Environment Agency has reported continued policy emphasis on industrial emission reduction and circular manufacturing practices, pushing the coating manufacturers to prioritize low-VOC and resource-efficient resin systems across construction, transportation, and industrial applications.

Key Coating Resins Market Insights Summary:

Regional Highlights:

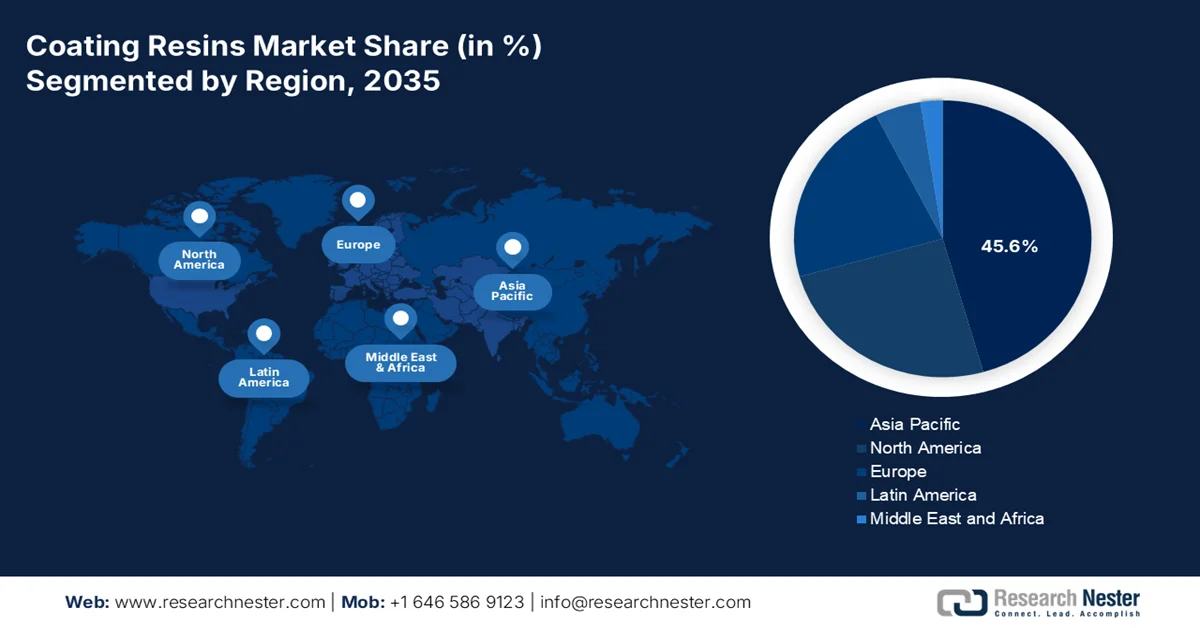

- The Asia Pacific coating resins market is anticipated to capture 45.6% revenue share by 2035, propelled by rapid urbanization, expanding manufacturing activity, and increasing infrastructure and automotive production across China and India

- North America market is forecast to witness substantial growth during 2026-2035, stimulated by stringent VOC emission regulations, infrastructure rehabilitation projects, and rising adoption of waterborne and high solids resin systems

Segment Insights:

- Acrylic resins are projected to account for 37% of the coating resins market by 2035, attributed to their superior weatherability, UV resistance, versatility, and growing utilization in sustainable architectural and industrial coating applications

- Waterborne coating technology is expected to maintain a dominant position in the technology segment throughout 2026-2035, fueled by global VOC reduction mandates and increasing preference for environmentally compliant coating systems

Key Growth Trends:

- Rising adoption of epoxy systems

- Automotive production accelerating the resin consumption

Major Challenges:

- Time-consuming regulations

- High R&D costs for sustainable formulations

Key Players: BASF (Germany), Dow Inc. (U.S.), Covestro AG (Germany), Arkema SA (France), Allnex Group (Germany), DSM (Netherlands), Mitsubishi Chemical Corporation (Japan), DIC Corporation (Japan), Evonik Industries (Germany), Mitsui Chemicals (Japan), Kansai Paint (Japan), Nan Ya Plastics Corporation (Taiwan), Cortec Corporation (U.S.), Orica (Australia), PTT Global Chemical (Thailand).

Global Coating Resins Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 48.2 billion

- 2026 Market Size: USD 51.1 billion

- Projected Market Size: USD 87.9 billion by 2035

- Growth Forecasts: 6.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Germany, India, Japan

- Emerging Countries: Vietnam, Indonesia, Brazil, Mexico, Thailand

Last updated on : 20 May, 2026

Coating Resins Market - Growth Drivers and Challenges

Growth Drivers

- Rising adoption of epoxy systems: The increasing adoption of epoxy technologies in industrial and commercial infrastructure is contributing to the growth of bio-based epoxy resins. Manufacturers are focusing on low-emission and high-durability resin systems that comply with tightening environmental regulations and long lifecycle performance requirements in factories, storage facilities, assembly halls, and parking structures. In March 2025, BASF and Sika jointly developed a new amine building block for curing epoxy resins, commercialized under BASF’s Baxxodur® EC 151 brand for industrial flooring applications. The development highlights the rising industry investment in the advanced curing technologies that support improved chemical resistance, durability, and lower environmental impact. Demand for such systems is increasing alongside infrastructure modernization and the industrial construction activities globally.

- Automotive production accelerating the resin consumption: The rising production of SUVs and pickup trucks is contributing to growth in the coating resins market due to higher coating requirements for larger vehicle platforms. Coating resins are used in automotive primers, clear coats, underbody protection, and corrosion-resistant finishes applied across vehicle bodies and structural components. According to the EPA, February 2026 data, the trucks accounted for 66% of all new vehicles sold in the U.S. in model year 2024, while passenger cars represented 34%. The growing preference for truck SUVs and pickup vehicles is increasing the demand for durable epoxy, polyurethane, acrylic, and polyester resin systems capable of withstanding harsh environmental and operational conditions.

Challenges

- Time-consuming regulations: Regulatory compliance is a significant barrier to entry in the coating resins market. Manufacturers must navigate the complex frameworks governing the volatile organic compound emissions, hazardous air pollutants, and chemical safety standards. In North America and Europe, regulations such as the Clean Air Act and REACH impose rigorous testing, documentation, and reformulation requirements that can delay market entry. Small and medium-sized enterprises struggle with the financial burden of compliance, which requires regulatory affairs teams and continuous monitoring of the evolving standards.

- High R&D costs for sustainable formulations: The industry-wide transition from the solvent-borne to environmentally friendly coating systems demands a substantial research and development investment. Developing waterborne powder high solids and UV/EB curable resins requires specialized expertise, advanced testing facilities, and extended development timelines. Biobased resin systems derived from renewable feedstocks represent a particularly capital-intensive frontier as they require novel monomer synthesis and performance validation. For new entrants, the R&D cost burden can be prohibitive.

Coating Resins Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.2% |

|

Base Year Market Size (2025) |

USD 48.2 billion |

|

Forecast Year Market Size (2035) |

USD 87.9 billion |

|

Regional Scope |

|

Coating Resins Market Segmentation:

Resin Type Segment Analysis

Acrylic resins dominate the coating resins market and is poised to hold the share value of 37% by 2035. The segment is driven due to their exceptional balance of performance, versatility, and cost effectiveness. These resins offer weatherability, UV resistance, and non-yellowing properties, making them ideal for exterior architectural paints and automotive clearcoats. Acrylic emulsions provide adhesion to various substrates, including wood, metal, and masonry, delivering superior gloss retention and dirt pick-up resistance. Moreover, acrylic polyol hybrids are replacing traditional polyurethanes in industrial maintenance coatings, providing comparable durability at lower raw material costs. The ongoing development of bio-based acrylic monomers from renewable feedstocks is expanding their appeal in green building projects. Their versatility ensures continued coating resins market leadership across the decorative, industrial, and protective coating applications.

Technology Segment Analysis

Waterborne coating is the largest sub-segment in the technology segment and is driven by global VOC reduction mandates. According to the American Coating Association, October 2021 data, nearly 85% of the interior coatings use waterborne technology. This growth is attributed to stricter air quality standards enforced under the Clean Air Act, pushing the manufacturers to phase out solvent-borne systems. Waterborne acrylics and polyurethanes now deliver comparable performance in gloss, hardness, and chemical resistance. Major economies, including the EU, China, and India, have also adopted similar regulations, creating a global shift. The technology benefits from lower fire risk, reduced hazardous waste disposal costs, and easier application. As green building certifications like LEED v5 gain traction, waterborne coatings are becoming the industry standard for both interior and exterior applications.

End use Industry Segment Analysis

The building and construction industry is the leading sub-segment in the coating resins market. The segment is driven by massive infrastructure spending worldwide. In India, the construction sector contributes 8% to the nation's GDP with a valuation of USD 126 billion as per the India Investment Grid October 2025, underscoring the scale of demand for architectural and protective coatings. Every new residential tower, bridge, or industrial facility requires significant volumes of acrylic, epoxy, and polyurethane resins for wall paints, anti-corrosion primers, and floor coatings. Government initiatives such as Housing for All and the National Infrastructure Pipeline further accelerate resin consumption. As urbanization continues across Asia and Africa, the building segment's dominance in the coating resins market is assured.

Our in-depth analysis of the coating resins market includes the following segments:

|

Segment |

Subsegments |

|

Resin Type |

|

|

Technology |

|

|

Application |

|

|

End use Industry |

|

|

Chemistry |

|

|

Substrate |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Coating Resins Market - Regional Analysis

APAC Market Insights

Asia Pacific is dominating the coating resins market and is expected to hold the regional revenue share of 45.6% by 2035. The coating resins market is driven by rapid urbanization, expanding manufacturing activity, and diverse regulatory landscapes across countries. China and India remain the largest consumers, driven by massive infrastructure projects, affordable housing programs, and automotive production growth. Architectural coatings dominate the region, with acrylic and vinyl resins widely used for interior and exterior applications. Moreover, the industrial coatings for consumer electronics, marine vessels, and packaging also contribute significantly in various nations. Environmental regulations are tightening gradually, with China leading stricter VOC limits and promoting the waterborne and powder coating adoption. However, solventborne systems are dominant due to the cost considerations and varied enforcement across emerging economies.

Government support for domestic manufacturing reduced import costs for the resin raw materials, and the development of the advanced coating technologies for industrial and strategic applications is shaping the coating resins market in India. According to May 2026, the Government of India issued Notification No. 12/2026 Customs, granting temporary zero-duty imports on key materials, including epoxy resins, alkyd resins, polyurethanes, vinyl acetate, styrene, and packaging-related polymers used in coatings, adhesives, and lamination applications. The measure is expected to reduce input costs for domestic packaging and printing manufacturers amid rising global prices. Moreover, DRDO December 2025 data shows India’s Centre of Excellence (CoE) on Polymer Coatings is supporting MSMEs and startups through pilot-scale manufacturing, testing, and development of high-performance coatings, including thermal-resistant silicone epoxy hybrid coatings for marine and defense applications capable of sustaining temperatures up to 300°C and reducing heat transfer by 50°C. These data show an active upliftment in the coating resins market growth and expansion.

Comparative Performance of Commercial Coating vs. NMRL, 2025

|

Properties |

Commercial Coating |

NMRL Coating |

|

Thermal conductivity, W/m.K |

0.086 |

0.90 |

|

Adhesion strength, MPa |

2 |

4 |

|

Tensile strength, MPa |

2 |

3 |

|

Resistance to salt spray test, 500 h (Corrosion rating: 0-No protection, 10-Highest protection) |

1 |

9 |

|

Heat build-up in sample, C |

37 |

25 |

Source: DRDO December 2025

The Japan coating resins market is set to grow from USD 1.9 billion in 2025 to USD 3.1 billion by the end of 2035 at a CAGR of 4.9% during the forecast period. In 2026, the market is projected to reach USD 2.42 billion. The nation is driven by the rising industrial production expansion in electronics and automotive manufacturing, and increasing investment in sustainable infrastructure materials. According to the JAMA September 2025 data, Japan’s automobile production reached 8.23 million units in 2024, supporting strong demand for coating resins used in automotive surface finishing and corrosion protection applications. Moreover, the METI June 2024 data indicates that 30% of bridges and 22% of tunnels had been in service for over 50 years, with nearly 75% of bridges expected to exceed 50 years of service by 2033. This is increasing demand for protective and maintenance coating systems across public infrastructure projects.

Percentage of Old Infrastructure, 2024

|

Type |

2023 |

2033 |

2040 |

|

Road bridges |

30 |

55 |

75 |

|

Tunnels |

22 |

36 |

53 |

|

Sewer pipe culverts |

5 |

16 |

35 |

|

Port facilities |

21 |

43 |

66 |

|

River management facilities |

10 |

23 |

38 |

|

Industrial water pipelines |

49 |

62 |

71 |

Source: METI June 2024

North America Market Insights

North America is projected to expand significantly during the assessed period, 2026 to 2035. The coating resins market is driven by the stringent environmental regulations and aging infrastructure renewal. Manufacturers are shifting from solventborne to waterborne and high solids resin systems to comply with the federal and state-level VOC emission limits. The architectural coatings segment is the largest consumer, supported by the steady residential and commercial construction activity. Protective coatings for bridges, highways, and industrial facilities represent a growing application area as public agencies prioritize corrosion control to extend the asset life. Acrylic and epoxy resins dominate due to their versatility, durability, and compatibility with low VOC formulations. Further, the emerging trends include bio-based resin adoption for federal procurement and powder coating expansion in the industrial segments. Supply chain regionalization continues as manufacturers seek to reduce their dependency on overseas raw material sources.

The increasing regulatory oversight and innovation in specialty resin technologies across industrial and healthcare applications are driving the coating resins market in the U.S. The U.S. Environmental Protection Agency's March 2026 data indicated that the proposed rulemaking affecting epoxy resin manufacturers is expected to reduce hazardous air pollutant emissions, primarily epichlorohydrin, by 105 tons annually, pushing the adoption of cleaner and lower-emission coating resin technologies. This is driving investment in environmentally compliant epoxy and polyamide resin production used in coatings, adhesives, and industrial applications. In addition, advanced resin coating developments in healthcare materials are supporting specialty market expansion. The NLM study published in July 2024 shows that experimental resin coatings containing bioactive additives demonstrated monomer conversion rates of 60% to 69%, exceeding the 55% conversion rate of commercial coating products while maintaining comparable flexural strength performance of 35 to 40 MPa, highlighting ongoing innovation in functional coating materials across the U.S., therefore surging the coating resins market growth.

Strict VOC emission regulations and rising investments in the domestic epoxy coating production are driving the coating resins market in Canada. According to the Government of Canada, October 2022 data, the VOC emissions for the architectural coating sector declined to 11.7 kilotons following the implementation of VOC regulations, despite coating production volumes remaining stable at 283 million liters. This regulatory shift is accelerating the demand for low-VOC and solvent-free resin technologies across architectural and industrial coating applications. In addition, the Government of Canada February 2025 data announced over USD 6.2 million in funding support for Chemtec Epoxy Coatings to expand the production capacity and automate manufacturing operations in Quebec. The company currently offers more than 200 solvent-free epoxy resin coating products reflecting growing domestic demand for sustainable coating solutions.

Europe Market Insights

The Europe coating resins market is heavily influenced by stringent environmental regulations and ambitious climate targets. The region leads the global shift away from solvent-borne systems, with the waterborne powder and high solids resins capturing the majority of the architectural and industrial coating applications. Renovation and retrofitting of the aging buildings drive steady demand for decorative coatings, while protective coatings for the bridges, highways, and public infrastructure consume significant volumes of the epoxy and polyurethane resins. Germany, France, Italy, and the UK are key national markets, each with distinct enforcement priorities. Bio-based and recycled content resins are gaining traction due to green public procurement policies. Manufacturers increasingly focus on the circular economy principles, including resin systems designed for easy coating removal and substrate recoating. Supply chains emphasize local production to reduce carbon footprints and comply with the REACH chemical safety requirements.

The increasing industrial modernization, construction renovation activity, and rising investment in sustainable manufacturing are shaping the coating resins market in Germany. The building permits for residential and non-residential construction have continued to support large-scale renovation and infrastructure projects, increasing the demand for architectural and protective coating resins. Moreover, the GTAI 2025 data reported that the country remained Europe’s largest chemical producer, with the chemical and pharmaceutical industry generating annual revenues exceeding USD 245 billion in recent years, supporting domestic production of coating raw materials and specialty resins. Further, Germany’s Federal Ministry for Digital and Transport allocated multi-billion euro investments toward railway modernization and bridge rehabilitation projects, increasing demand for corrosion-resistant epoxy polyurethane and polyester coating systems used in transportation and public infrastructure applications.

The growth in construction activity and stable vehicle manufacturing output is shaping the coating resins market in the UK and increasing demand for architectural, automotive, and protective coatings. According to the UK Parliament April 2026 data, the construction sector output increased by 1%, reflecting a continued infrastructure development and the renovation activity requiring coating resins for paints, sealants, and corrosion-resistant applications. In addition, nearly 905,000 vehicles were manufactured in the UK as per the UK Parliament May 2025 data, including passenger cars, vans, trucks, taxis, and buses. This sustained automotive production is supporting demand for epoxy, acrylic, polyurethane, and polyester coating resins used in OEM coatings, refinishing, and component protection systems. Moreover, the increasing adoption of low-VOC and high-durability resin technologies aligns with evolving environmental and industrial performance standards across the UK market.

UK Automotive Industry, 2022-2024

|

Indicator |

Data |

Year |

|

Total Vehicles Produced in the UK |

905,000 units |

2024 |

|

Total Cars Produced in the UK |

780,000 units |

2024 |

|

Cars Produced in the UK |

905,000 units |

2023 |

|

Cars Produced in the UK |

775,000 units |

2022 |

|

UK Share of Global Car Production |

1.0% of 76 million global cars |

2024 |

|

Germany Car Production |

3.9 million units |

2024 |

|

Spain Car Production |

1.9 million units |

2024 |

|

France Car Production |

850,000 units |

2024 |

|

Share of UK Cars Exported |

77% (~600,000 vehicles) |

2024 |

|

UK Car Export Value |

GBP 28 billion |

2024 |

|

UK Car Exports to the U.S. |

GBP 7.7 billion (27% of exports) |

2024 |

|

Employees in UK Motor Vehicle Manufacturing |

139,000 employees |

2023 |

|

Share of Total UK Employment |

0.4% |

2023 |

|

Employees in Motor Vehicle Sales & Repair Sector |

548,000 employees |

2023 |

|

Share of Total UK Employment in Vehicle Sales & Repair |

1.7% |

2023 |

Source: UK Parliament, May 2025

Key Coating Resins Market Players:

- BASF (Germany)

- Dow Inc. (U.S.)

- Covestro AG (Germany)

- Arkema SA (France)

- Allnex Group (Germany)

- DSM (Netherlands)

- Mitsubishi Chemical Corporation (Japan)

- DIC Corporation (Japan)

- Evonik Industries (Germany)

- Mitsui Chemicals (Japan)

- Kansai Paint (Japan)

- Nan Ya Plastics Corporation (Taiwan)

- Cortec Corporation (U.S.)

- Orica (Australia)

- PTT Global Chemical (Thailand)

- Samhwa Paints Industrial Co., Ltd. (South Korea)

- KCC Corporation (South Korea)

- Asian Paints (India)

- Berger Paints India (India)

- U-POL (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BASF is one of the world’s leading suppliers of raw materials for the coating resins market, offering a comprehensive portfolio that includes acrylics, alkyds, polyurethanes, and epoxies. The company has strategically shifted toward high-solid waterborne and bio-based resin systems to meet tightening environmental regulations.

- Dow Inc. is a top player in the coating resins market known for its advanced acrylic and styrene acrylic emulsion technologies. The company focuses on developing low-VOC APE-free and formaldehyde-free resins for architectural and industrial applications. In 2025, the company made net sales of USD 40 billion.

- Covestro AG specializes in high-performance polyurethane resins and raw materials for the coating resins market, particularly waterborne polyurethane dispersions and polyisocyanates. The company’s strategic focus lies in replacing solvent-borne systems with more sustainable alternatives for automotive OEM, wood, and protective coatings.

- Arkema SA is a major player in the coating resins market via its coating solutions division, which includes acrylic, polyamide, and specialty resin technologies. The company has aggressively expanded its bio-based offerings, waterborne acrylics derived from renewable sources. In 2024, the company made a net sale of USD 10.36 billion.

- Allnex Group is a pure play leader in the coating resins market, offering one of the widest portfolios of liquid resins, powder coating resins, and crosslinkers. The company’s strategic initiatives center on developing next-generation technologies, including energy-curable resins, waterborne alkyds, and high-temperature stable powder resins.

Here is a list of key players operating in the global coating resins market:

The global coating resins market is highly competitive, characterized by the presence of both multinational chemical giants and specialized regional players. Key strategic initiatives include capacity expansions, mergers, and acquisitions to broaden product portfolios and heavy investment in bio-based and high-solid resin technologies to meet the stringent environmental regulations. For example, in September 2025, KANSAI HELIOS acquired German Powder Coatings and Resins producer CWS Lackfabrik GmbH. Companies are focusing on developing waterborne and powder coating resins to reduce volatile organic compound emissions. Regional leaders use local supply chains and raw material access, while global players emphasize R&D for advanced applications in automotive, architectural, and industrial coatings.

Corporate Landscape of the Coating Resins Market:

Recent Developments

- In April 2026, allnex announced the launch of Solvent-Borne Alkyd and Polyester rPET liquid resins. This launch advances the sustainability in the coatings industry, empowers customers to reduce their carbon footprint to address global plastic pollution.

- In January 2025, Cortec® announced the development of biobased anticorrosion coatings for metal with the release of EcoLine® 3860. EcoLine® 3860 contains 27% USDA certified biobased content and is specifically designed for industrial users to increase the use of renewable content.

- In March 2024, DIC Corporation announced that its subsidiaries in India such as DIC South Asia Private Limited in Mumbai and IDEAL CHEMI PLAST PRIVATE LTD. in Badlapur, have established the DIC South Asia Private Limited Application Lab that is dedicated to evaluating coating resins for automotive coatings and infrastructure applications.

- Report ID: 4245

- Published Date: May 20, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.