Cell Culture Market Outlook:

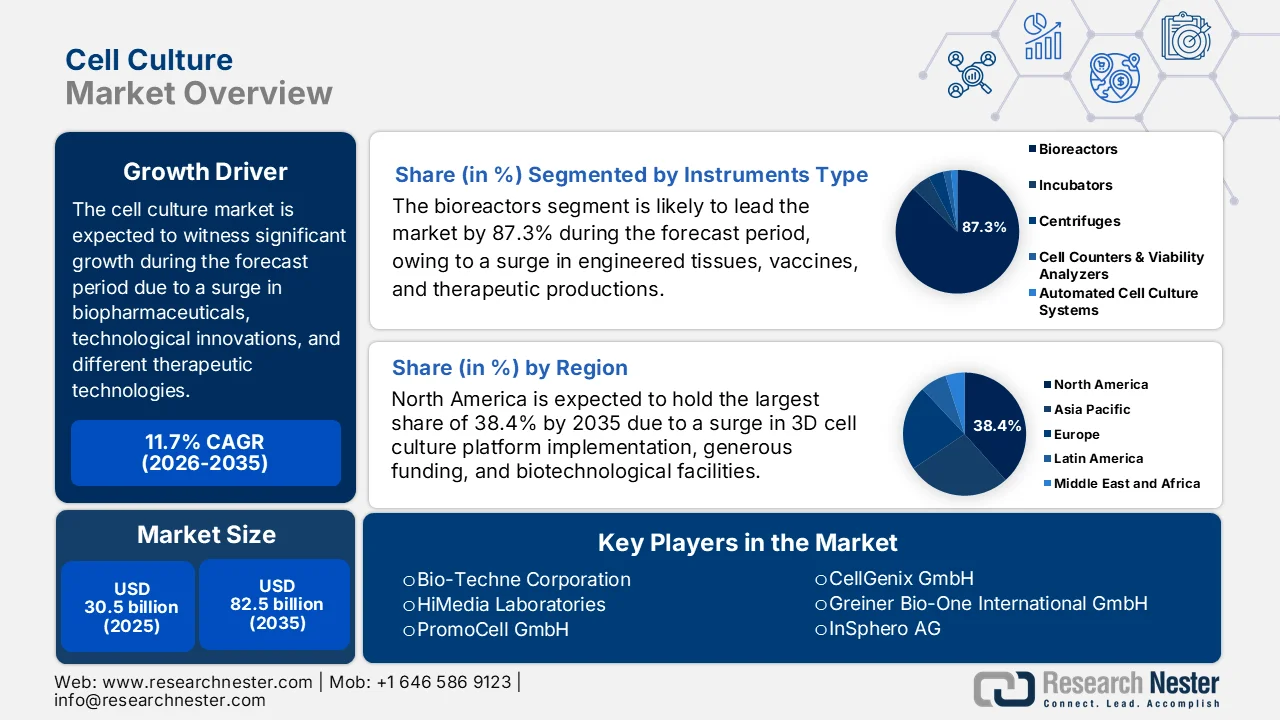

Cell Culture Market size was valued at over USD 30.5 billion in 2025 and is expected to reach USD 82.5 billion by the end of 2035, growing at a CAGR of 11.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of cell culture is assessed at USD 34 billion.

The global cell culture market’s foundational upliftment is highly shaped by technological advancement, biopharmaceutical expansion, along with in-depth evaluation that has revealed distinctive forces to operate at different levels of the ecosystem. According to official statistics published by NIH in February 2024, the U.S. Food and Drug Administration (FDA) has significantly accepted 32 cell gene therapies, with an increased in approvals. Besides, there has been an increase in the number of regenerative medicine therapy product developers from 900 to almost 2,700 worldwide. Likewise, there has also been a surge in the number of gene and cell therapy clinical trials from 1,000 to 1,600, as well as a surge in patients aided with chimeric antigen receptor T cell (CAR-T) therapies from 180 to 20,000, thus positively impacting the cell culture market growth.

Furthermore, the decentralized cell culture manufacturing, the integration of microphysiological systems into regulatory frameworks, and the reshoring of biopharmaceutical manufacturing supply chains, are a few trends that are responsible for bolstering the cell culture market globally. In terms of biopharmaceutical manufacturing, the April 2025 MedRxiv Organization article indicated that pharmaceutical organizations demonstrate that manufacturing expenses tend to account for nearly 20% to 30% of overall expenses, which is inclusive of direct material expenses for patent protected drugs and almost 52% for generic medications. Besides, the total U.S.-based biologics product constitute the highest total CAPEX, amounting to USD 2,280,000, while India-specific costs are USD 677,000, corresponding to a reduction of 70.3% in comparison to U.S.-driven products, thereby making it suitable for boosting the market exposure.

Key Cell Culture Market Insights Summary:

Regional Highlights:

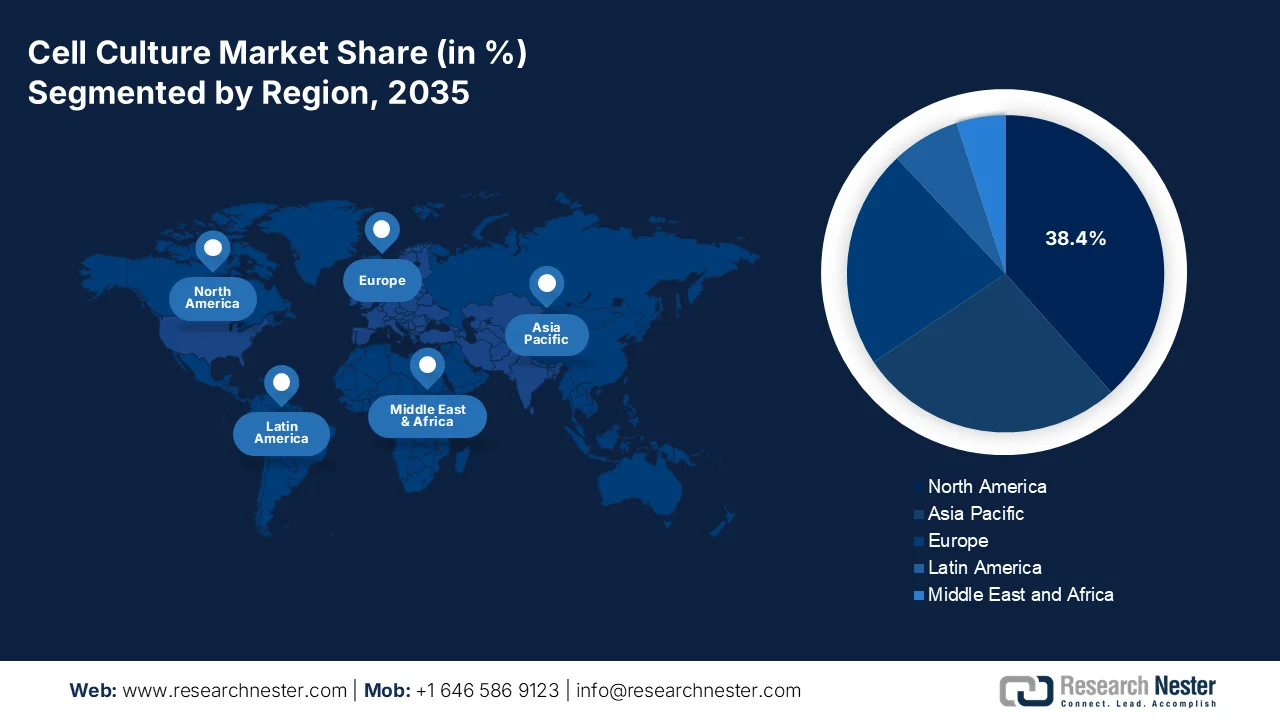

- North America in the cell culture market is projected to command a leading 38.4% share by 2035, driven by strong adoption of advanced 3D cell culture platforms, substantial federal R&D funding, and robust biotechnology infrastructure

- Europe is anticipated to register the fastest growth during the 2026–2035 period, impelled by increasing government funding for biopharmaceutical innovation and rising emphasis on non-animal testing methodologies

Segment Insights:

- The bioreactors segment of the cell culture market is projected to account for a dominant 87.3% share by 2035, propelled by rising demand for engineered tissues, vaccines, and automated high-density therapeutic production

- The consumables sub-segment is expected to secure the second-largest share during the 2026–2035 period, fueled by the recurring need for replenishment across continuous research, development, and manufacturing cycles

Key Growth Trends:

- Surge in the aging demographic imperative

- Expansion in the therapeutic modality pipeline

Major Challenges:

- Stringent regulatory compliance and quality assurance

- Skilled labor shortage and knowledge gap

Key Players:Thermo Fisher Scientific, Danaher Corporation, Merck KGaA, Sartorius AG, Corning Incorporated, Lonza Group, Becton Dickinson and Company BD, FUJIFILM Diosynth Biotechnologies, Takara Bio Inc., Bio-Techne Corporation, HiMedia Laboratories, PromoCell GmbH, CellGenix GmbH, Greiner Bio-One International GmbH, InSphero AG, Emulate Inc., Mimetas BV, STEMCELL Technologies, Esco Lifesciences Group, SmithBio BIOTOP, Novo Holdings AS, REPROCELL, Evonik, Mitsui Chemicals Inc.

Global Cell Culture Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size:USD 30.5 billion

- 2026 Market Size: USD 34 billion

- Projected Market Size: USD 82.5 billion by 2035

- Growth Forecasts: 11.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.4% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Singapore, Australia

Last updated on : 31 March, 2026

Cell Culture Market - Growth Drivers and Challenges

Growth Drivers

- Surge in the aging demographic imperative: The unprecedented worldwide demographic shift toward the aging population serves as one of the drivers for the cell culture market. According to official statistics published by the World Health Organization (WHO) in February 2025, the suitable life expectancy at birth reached 73.3 years as of 2024, denoting an increase of 8.4 years. Besides, there has been an increase in the number of 60 years-aged people from 1.1 billion as of 2023 to 1.4 billion by the end of 2030. This particular rise in the aging population is particularly rapid and evident across developing economies. Therefore, there has been a rise in significant implications for public health and increased focus on maintaining proper health, especially for old-aged people, thus fueling the cell culture market growth.

- Expansion in the therapeutic modality pipeline: This particular driver emerges from the expanded diversity of therapeutic modalities, demanding cell culture platforms as non-negotiable manufacturing facilities, which is positively driving the cell culture market. As per an article published by NIH in January 2024, the percentage of individuals utilizing health approaches gradually increased from 19.2% to 36.7% as of 2022. Besides, there has been a surge in yoga therapy from 5% to 15.8%, which assists in stem cell, cellular regeneration, and gene expression. Moreover, meditation has emerged as the most utilized approach, with an upsurge from 7.5% to 17.3% in the same duration that readily impacts molecular biology, aging, and cellular health, thus making it suitable for uplifting the market exposure.

- Focus on cellular agriculture and food security: This is yet another structural driver for the cell culture market, which is eventually emerging at the intersection of food security and environmental sustainability. Based on a data report published by the USDA Government in December 2024, the cumulative capitalized investment in cell-cultured seafood and meat reached USD 3.1 billion as of 2023. Likewise, during the same timeline, the capital investment in precision fermentation also reached USD 2.1 billion. These particular increases have occurred, owing to a surge in interests in the animal and environmental welfare aspects of traditional livestock production and concerns. These are based on disease transmission between animals and humans, along with worldwide accessibility to protein, thus fueling the market expansion.

Challenges

- Stringent regulatory compliance and quality assurance: The aspect of navigating the complex and evolving regulatory landscape represents a formidable barrier across the cell culture market. Regulatory bodies including the FDA, EMA, and PMDA readily enforce increasingly rigorous standards for cell culture-derived products, particularly for cell and gene therapies where manufacturing processes directly impact patient safety. Besides, each change in raw material source, equipment, or process requires extensive validation and often triggers supplemental regulatory filings, creating friction for innovation adoption. The transition to serum-free and chemically-defined media, while scientifically advantageous, demands comprehensive stability testing and comparability studies that can delay product launches by 12 to 24 months.

- Skilled labor shortage and knowledge gap: The rapid technological evolution within the cell culture market has outpaced the available talent pool, creating a critical skills gap that threatens operational scalability. Besides, bioprocessing at present requires expertise spanning traditional cell biology, advanced automation, data analytics, and regulatory compliance, a multidisciplinary skillset rarely cultivated in conventional academic programs. The shortage of experienced bioprocess engineers, quality assurance specialists, and cell culture technicians is most acute in emerging biotech hubs and contract manufacturing organizations racing to meet surging demand for cell and gene therapy production. Moreover, the turnover rates in high-demand technical roles have escalated, driving up labor costs and compromising institutional knowledge retention.

Cell Culture Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.7% |

|

Base Year Market Size (2025) |

USD 30.5 billion |

|

Forecast Year Market Size (2035) |

USD 82.5 billion |

|

Regional Scope |

|

Cell Culture Market Segmentation:

Instruments Type Segment Analysis

Based on the instruments type, the bioreactors segment in the cell culture market is anticipated to garner the highest share of 87.3% by the end of 2035. The segment’s upliftment is primarily attributed to the increased demand for engineered tissues, vaccines, along with automated and high-density production of therapeutics. According to official statistics published by NLM in December 2022, the suitable cultivation of tumor infiltrating lymphocytes in polyolefin bags resulted in the reduction by 9.8% in comparison to regular plates. Besides, the utilization of periodic pumping eventually increased T cell numbers, and meanwhile, the continuous pumping led to a 75% decrease in resting control T-flasks. Therefore, all these developments are extremely suitable for creating bioreactors, which in turn, is extremely suitable for bolstering the cell culture market exposure.

Product Segment Analysis

During the forecast period, the consumables sub-segment, part of the product segment, is projected to grab the second-highest share in the cell culture market. The sub-segment’s growth is highly driven by a recurring revenue model, as these products require continuous replenishment throughout ongoing research, development, and manufacturing cycles, unlike capital equipment which involves one-time purchases. Within this sub-segment, cell culture media formulations reflect their critical role in maintaining optimal cell growth conditions and supporting diverse cell line requirements. The expansion of single-use bioprocessing systems has further intensified consumables demand, as disposable bioreactor bags and tubing assemblies are replaced after each production run.

Application Segment Analysis

The biopharmaceutical manufacturing sub-segment, which is part of the application segment, is expected to account for the third-highest share in the cell culture market by the end of the stipulated duration. The sub-segment’s development is highly propelled by its indispensable role in producing monoclonal antibodies, vaccines, and recombinant proteins. Within this sub-segment, monoclonal antibody manufacturing is driven by expanding therapeutic applications in oncology, immunology, and autoimmune diseases. Additionally, the growth is reinforced by structural shifts in global manufacturing capacity, representing a continuous year-over-year increase (YoY). The industry’s decisive pivot toward flexible production architectures is evidenced by the adoption rate of single-use systems, enabling faster turnaround times and reduced contamination risks in comparison to traditional stainless-steel bioreactors.

Our in-depth analysis of the cell culture market includes the following segments:

|

Segment |

Subsegments |

|

Instruments Type |

|

|

Product |

|

|

Application |

|

|

Consumables Type |

|

|

End user |

|

|

Cell Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cell Culture Market - Regional Analysis

North America Market Insights

North America in the cell culture market is anticipated to garner the largest share of 38.4% by the end of 2035. The market’s upliftment in the region is primarily fueled by the robust adoption of advanced 3D cell culture platforms, generous federal-based funding for in-depth research and development, strong biotechnological infrastructure, concentrated biotech facilities, suitable reimbursement policies, and industry-academic collaboration. According to official statistics published by the U.S. Senate Government in April 2025, invasive pests, especially in the U.S., alone costs over USD 1.2 trillion in the past 60 years. Therefore, with the utilization of biotechnology, farmers in the country are focused on growing crops that are resistant to pests. Therefore, this increased biotechnology integration has resulted in an increase in the market growth in the overall region.

The cell culture market in the U.S. is growing significantly, owing to suitable funding opportunities, an escalation in implementing organoids, organ-on-a-chip platforms, and primary cells, the aspect of CMS reimbursement restructuring for gene and cell therapies, and reduction in clinical trial expenses. As stated in an article published by NLM in November 2023, by the end of the first quarter of 2023, there has been more than 100 different accepted cell, RNA, and gene therapies, with more than 3,700 in preclinical and clinical development. Besides, onasemnogene abeparvovec is considered an adeno-associated virus vector-based gene therapy for successfully delivering the SMN gene encoding SMN protein and demonstrate clinical advantages for almost 7.5 years, thereby making it extremely suitable for expanding the market growth in the overall country.

The strategic federal investment in domestic biomanufacturing capacity, an increase in government funding, the production of crucial cell culture inputs for therapeutics and vaccines, coordination with natural strategy for diminishing reliance on imported cell culture materials, and the focus on stem cell research, are certain factors fueling the cell culture market in Canada. Based on government estimates published by the Government of Canada in March 2025, more than USD 2.3 billion has been readily invested for rebuilding the country’s biomanufacturing capacity, therapeutics, and vaccines. Besides, OmniaBio’s extended facility in Hamilton is focused on seeking to drive an increase in manufacturing efficiency by 5 times, while diminishing supply and production expenses by almost 50%. This is suitable facilitating patient accessibility to life-saving treatments for rare diseases, such as cancer, thereby positively impacting the market growth.

Europe Market Insights

Europe in the cell culture market is expected to emerge as the fastest-growing region during the forecast duration. The market’s development is highly propelled by the presence of different cell culture technologies, generous governmental funding for biopharmaceutical innovation, robust regulatory push for non-animal testing methodologies, expansion in cell culture capacity, and investments in vaccine production autonomy. According to official statistics published by the Europe Commission in 2025, the administrative body significantly financed a part of upfront expenses from the USD 3.1 billion emergency support instrument as a down-payment fund on vaccines. Besides, vaccine delivery to regional countries have increased, accounting for a total of 84.8% of the adult population in August 2023, thereby enhancing the market exposure in the region.

2024 Vaccines Export and Import in Europe

|

Countries |

Export (USD) |

Import (USD) |

|

Belgium |

13.6 billion |

6.8 billion |

|

Ireland |

12.4 billion |

556 million |

|

France |

4.1 billion |

1.4 billion |

|

Italy |

3.2 billion |

1.6 billion |

|

Germany |

2 billion |

3.4 billion |

|

Spain |

1.5 billion |

1.2 billion |

|

Netherlands |

1.1 billion |

1.15 billion |

|

UK |

457 million |

1.5 billion |

|

Poland |

484 million |

909 million |

Source: OEC

The cell culture market in Germany is gaining increased traction, owing to a surge in investments for biologics manufacturing capacity, pharmaceutical production strategy, therapeutic manufacturing infrastructure, and focus on stem cell research. As per an article published by the BIQ Deutschland Organization in January 2025, the financing of domestic biotechnology organizations increased by 78% as of 2024 in comparison to 2023. Additionally, the total venture capital, amounting to USD 1.0 billion, along with USD 1.1 billion increase in capital through stock exchange, and USD 22.9 million in public offering, led to an overall USD 2.2 billion, compared to USD 1.2 billion in 2023. This particular increase is suitable for both 68% of private and more than 82% of public organizations, thereby making it suitable for boosting the market growth in the country.

The government’s focus on advanced cell therapies through sustained funding approaches, the provision of generous research and innovation budget, enhancement in bioprocessing and technological infrastructure, and an upsurge in manufacturing facilities are trends that are developing the cell culture market in the UK. As stated in an article published by the OHE Organization in October 2025, the comprehensive accessibility to cell and gene therapies in four indications tend to develop healthcare benefits with a suitable valuation surpassing USD 22.9 billion in more than 10 years, for the domestic economy, systems, and individuals. Besides, the payer’s pricing of such therapies for individuals with acute myeloid leukemia (AML) amounts to USD 668 million, which is primarily driven by health benefits. Simultaneously, the most significant valuation created in beta-thalassemia effectively related to healthcare expense savings at nearly USD 85 million. Moreover, the additional value of wide access to these therapies creates suitable cost savings for different diseases, thus creating a huge growth opportunity for the cell culture market in the country.

Cell and Gene Therapy Valuation for Different Diseases in the UK (2025)

|

Disease Indications |

Population Size |

Individuals |

Systems |

Economy |

Driver |

|

All diseases |

310 |

USD 12.6 million |

USD 114,956.5 |

USD 689,739 |

Long survival rate in a small cohort. |

|

Acute Myeloid Leukemia (AML) |

23,970 |

USD 670.1 million |

USD 532.1 million |

USD 6.3 million |

Durable remission to lower care demands. |

|

Beta-Thalassemia |

426 |

USD 59.7 million |

USD 85 million |

USD 58.6 million |

Transfusion independence. |

|

Alzheimer’s disease |

973,160 |

USD 45.5 billion |

USD 22.8 billion |

USD 24.7 billion |

Limited progression and diminished care burden. |

Source: OHE Organization

APAC Market Insights

The Asia Pacific in the cell culture market is projected to witness considerable growth by the end of the forecast duration. The market’s growth in the region is highly driven by substantial government investment, expansion in biotechnology industries, effectively prioritizing self-sufficiency in biologics manufacturing, and focus on technological innovation with innovative regenerative medicines. According to official statistics published by NLM in March 2024, the active pharmaceutical ingredients (API) industry across low and middle-income economies were valued at USD 193.1 billion as of 2023, which is further projected to increase to USD 285.2 billion by the end of 2028. In addition, 60.5% of API in produced in Asia Far East, with India and China deliberately considered leading suppliers of pharmaceutical excipients and raw materials globally, thus proliferating the market growth in the region.

The cell culture market in China is gaining increased exposure, owing to strong governmental investment, regulatory modernization, the Healthy China 2030 strategy, an increase in biologics manufacturing facilities, rise in aging population, and an increase in chronic and oncology diseases demanding biologic therapies. As stated in an article published by NLM in December 2025, the country deliberately recorded 4.8 million new cancer cases, which is 341.7 per 100,000 population, along with 2.5 million deaths, accounting for 182.3 per 100,000 as of 2022. Besides, female breast, stomach, liver, lung, thyroid, and colorectal cancers catered to 67.5% of deaths. Moreover, the age-standardized mortality rate for all cancer types reduced by roughly 1.3% yearly, while the 5-year relative survival optimized from 30.9% to 43.7%, thus denoting an optimistic outlook for the market growth.

The aspects of national strategic technologies, enhanced tax credit benefits, an escalation in approval pathways for regenerative medicines, reduction in time-to-market for cell culture-based therapeutics, increased biologics export, and governmental funding are deliberately responsible for uplifting the cell culture market in South Korea. As per an article published by Invest Korea in March 2025, the biopharmaceutical industry in steadily growing, with an increase in domestic pharmaceutical industry by 5.3% YoY and reached USD 23 billion as of 2023. Additionally, over the past 5 years, the bio industry in the country grew at an average yearly growth rate of 8.2%, which is more than double the growth rate of the country’s GDP, which is 3.8% during the same timeline. Moreover, the present industrial size in the nation is only 1.5% of the global sector, demonstrating a huge potential for the market growth in the overall country.

Key Cell Culture Market Players:

- Thermo Fisher Scientific (U.S.)

- Danaher Corporation (U.S.)

- Merck KGaA (Germany)

- Sartorius AG (Germany)

- Corning Incorporated (U.S.)

- Lonza Group (Switzerland)

- Becton, Dickinson and Company (BD) (U.S.)

- FUJIFILM Diosynth Biotechnologies (Japan/UK)

- Takara Bio Inc. (Japan)

- Bio-Techne Corporation (U.S.)

- HiMedia Laboratories (India)

- PromoCell GmbH (Germany)

- CellGenix GmbH (Germany)

- Greiner Bio-One International GmbH (Austria)

- InSphero AG (Switzerland)

- Emulate, Inc. (U.S.)

- Mimetas B.V. (Netherlands)

- STEMCELL Technologies (Canada)

- Esco Lifesciences Group (Singapore)

- SmithBio (BIOTOP) (Malaysia)

- Novo Holdings A/S (Denmark)

- REPROCELL (Japan)

- Evonik (Germany

- Mitsui Chemicals, Inc. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Thermo Fisher Scientific operates as a fully integrated solutions provider, offering an extensive portfolio spanning cell culture media, sera, bioreactors, and single-use technologies across the entire research-to-manufacturing continuum. The company leverages its unparalleled global distribution network and deep customer relationships to serve as a one-stop partner for academic institutions, biotech startups, and large-scale biopharmaceutical manufacturers alike.

- Danaher Corporation commands a dominant position in bioprocessing, specializing in single-use technologies, downstream purification, and digital manufacturing solutions. The company’s business model emphasizes continuous innovation through its Danaher Business System, enabling rapid integration of acquired technologies and consistent operational excellence across its cell culture portfolio.

- Merck KGaA distinguishes itself through deep expertise in high-quality cell culture media formulations and critical raw materials, particularly in chemically-defined and serum-free platforms. The company maintains a strong focus on enabling advanced therapy manufacturing, providing specialized solutions for cell and gene therapy developers navigating complex regulatory pathways.

- Sartorius AG concentrates on precision bioprocessing equipment and single-use bioreactor systems, positioning itself as a critical partner for scale-up and commercial manufacturing operations. The company’s strategy centers on delivering integrated hardware and software platforms that enhance process control, reproducibility, and operational efficiency for biologics producers.

- Corning Incorporated leverages its materials science heritage to specialize in advanced cell culture vessels, surface-treated consumables, and scalable cell culture systems. The company differentiates itself through proprietary surface technologies that optimize cell attachment, expansion, and differentiation across research, drug discovery, and bioprocessing applications.

Here is a list of key players operating in the global cell culture market:

The global cell culture market is consolidated, with the top five manufacturers holding the majority of the market share, dominated by U.S. and Europe-based multinationals. The competitive landscape is characterized by vertical integration, where leaders, such as Thermo Fisher Scientific and Danaher (Cytiva) offer end-to-end solutions from consumables to advanced bioreactors. Besides, to secure their positions, key players are pursuing expansion through strategic acquisitions and geographic diversification. For instance, in December 2024, Novo Holdings A/S successfully acquired Catalent in an all-cash transaction with an overall enterprise valuation of an estimated USD 16.5 billion. Moreover, Novo Holdings sold 3 of Catalent’s almost 50 worldwide facilities, with the objective of developing sustainable value creation within life sciences through its strategic ownership model, thus driving the cell culture industry globally.

Corporate Landscape of the Cell Culture Market:

Recent Developments

- In March 2026, REPROCELL expanded its product catalogue by deliberately making the addition of the BioThrust ComfyCell Incu bioreactor platform, for effectively strengthening its provision of stem cell research and advanced human cell culture.

- In October 2024, Evonik has successfully established the newest worldwide network for developing system solutions that tend to address upstream risks in cell culture, in association with the Global Competence Network for Cell Culture Solutions for forming a team of research development, application technology, and business experts.

- In April 2024, Mitsui Chemicals, Inc. made investments in FullStem Co. Ltd. through the 321FORCE Global Innovation Fund L.P. for expanding its business in the cell culture industry by standard capitalization on outstanding materials.

- Report ID: 8488

- Published Date: Mar 31, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Cell Culture Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.