C5 Resin Market Outlook:

C5 Resin Market was valued at USD 952.5 million in 2025 and is projected to reach a value of USD 1.52 billion by the end of 2035, rising at a CAGR of 5.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of C5 resin is assessed at USD 1 billion.

The global C5 resin market is growing steadily on account of rising demand from adhesives, coatings, and rubber compounding industries. The booming packaging sector, influenced by rising e-commerce and expansion in the automotive industry, is also propelling a profitable business environment for pioneers in this field. According to the official statistics that were published by the International Organization of Motor Vehicle Manufacturers (OICA), the global motor vehicle production has shown a strong growth trajectory between 2023 and 2025, reflecting expansion in major automotive hubs worldwide. It states that Asia-Oceania leads in production, with the output increasing from 38.57 million units in 2023 to 41.22 million units in 2025, a rise of 7 %. China remains the largest single contributor, growing from 21.07 million to 24.33 million units (+13 %). Hence, this data indicates there is a huge demand for industrial resins such as C5, used in adhesives, coatings, and composite parts in vehicle manufacturing.

Global Motor Vehicle Production: Official Government Figures, Regional Output & Trade Analysis Q1 to Q3 (2023-2025)

|

Region/Country |

2023 Units |

2025 Units |

% Change 2025/2023 |

|

Asia-Oceania |

38,575,638 |

41,223,939 |

+7% |

|

China |

21,074,705 |

24,332,696 |

+13% |

|

India |

4,459,894 |

4,802,843 |

+8% |

|

Europe |

13,059,383 |

12,416,589 |

-5% |

|

U.S. |

8,112,283 |

7,780,247 |

-4% |

|

South America |

2,245,581 |

2,389,366 |

+7% |

Source: OICA

Furthermore, the aspects of urbanization and infrastructure development in the emerging nations also stimulate consistent demand in the C5 resin market. According to the article published by the United Nations Environment Programme (UNEP) in March 2024, the buildings and construction sector accounted for 34 % of global energy demand and 37 % of energy-related CO₂ emissions in 2022, which underscores its scale as well as impact worldwide. The report also stated that, along with the ongoing policy and technology efforts, the sector needs to increase the decarbonization efforts, which requires an annual increase of ten points to meet 2030 climate targets, wherein the C5 resin utilization can support this goal. In addition, the report emphasizes that the adoption of resilient construction methods and nature-based solutions is highly essential for sustainable growth. Thus, these insights indicate that the global construction industry continues to expand, with substantial demand for materials and technologies.

Key C5 Resin Market Insights Summary:

Regional Highlights:

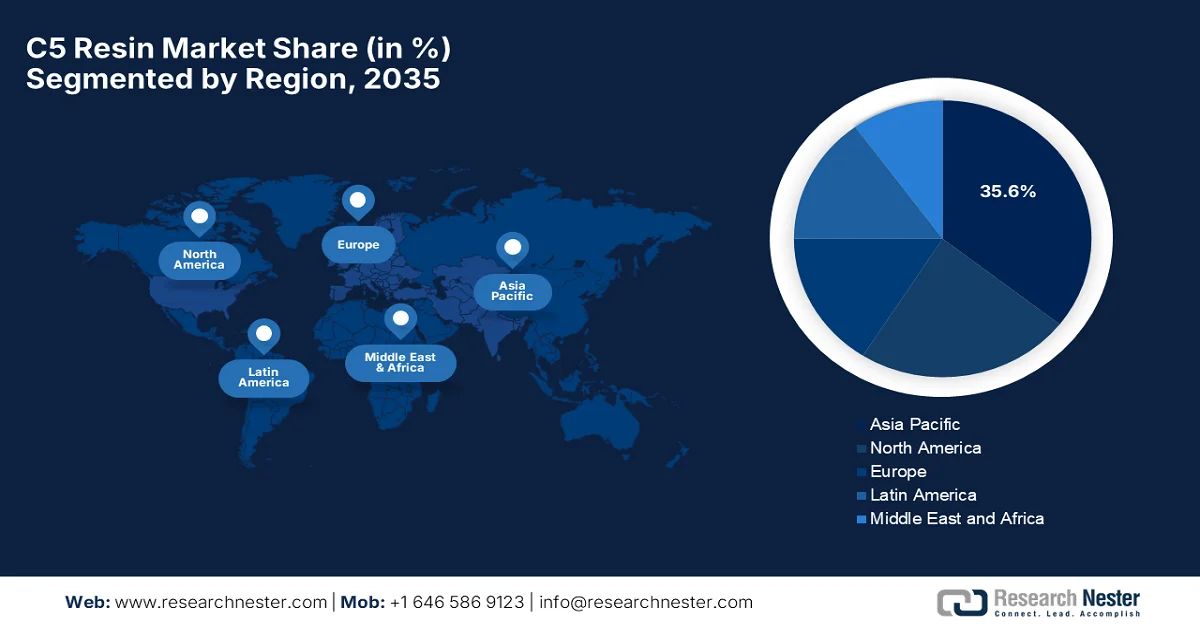

- Asia Pacific C5 resin market is anticipated to command a 35.6% share by 2035, attributed to expanding manufacturing activities, rising construction demand, and increasing automotive production

- North America is projected to witness the fastest growth during 2026–2035, fueled by strong demand from paints, coatings, tire manufacturing, and adhesive applications

Segment Insights:

- Adhesives & sealants segment in the C5 resin market is projected to account for 45.6% share by 2035, propelled by rising demand across packaging, hygiene products, and industrial bonding applications

- Aliphatic C5 hydrocarbon resin segment is expected to secure a considerable share by 2035, impelled by its superior compatibility with natural and synthetic rubber in adhesive and rubber compounding applications

Key Growth Trends:

- Rising demand from adhesives & sealants

- Growth in packaging sector

Major Challenges:

- Volatility in crude oil prices

- Environmental and regulatory pressure

Key Players: ExxonMobil Chemical Company (U.S.), Eastman Chemical Company (U.S.), Kolon Industries, Inc. (South Korea), Zeon Corporation (Japan), Arakawa Chemical Industries, Ltd. (Japan), Idemitsu Kosan Co., Ltd. (Japan), Neville Chemical Company (U.S.), Resinall Corporation (U.S.), Cray Valley (TotalEnergies Group) (France), Formosan Union Chemical Corporation (Taiwan), Lesco Chemical Limited (China), Zhejiang Henghe Petrochemical Co., Ltd. (China), Zibo Luhua Hongjin New Material Group Co., Ltd. (China), Puyang Changyu Petroleum Resins Co., Ltd. (China), Puyang Tiancheng Chemical Co., Ltd. (China), Shanghai Jinsen Hydrocarbon Resins Co., Ltd. (China), Qingdao Bater Chemical Co., Ltd. (China), Shandong Landun Petroleum Resin Co., Ltd. (China), Henan Anglxxon Chemical Products Co., Ltd. (China), Seacon Corporation (India), Braskem S.A. (Brazil).

Global C5 Resin Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 952.5 million

- 2026 Market Size: USD 1 billion

- Projected Market Size: USD 1.52 billion by 2035

- Growth Forecasts: 5.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (35.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, India

- Emerging Countries: South Korea, Brazil, Mexico, Vietnam, Indonesia

Last updated on : 18 March, 2026

C5 Resin Market - Growth Drivers and Challenges

Growth Drivers

- Rising demand from adhesives & sealants: C5 resins are considered to be highly essential tackifiers in hot melt adhesives, pressure-sensitive adhesives, and other sealants due to strong tack, peel strength, and adhesion properties. In June 2025, the Adhesive and Sealant Council (ASC) reported that it had partnered with Smart EPD to update the product category rules for adhesives and sealants used in construction, thereby establishing a standardized methodology for developing life cycle assessments and environmental product declarations. This particular update will cover single- and multi-component building sealants based on various polymers and align with EPA and ACLCA PCR standards. Hence, such initiatives are expected to accelerate the adoption of sustainable adhesives and sealants, driving the overall C5 resin market.

- Growth in packaging sector: Flexible and specialty packaging is growing, which is spurred by food & beverage and e-commerce, thereby increasing demand for adhesives based on C5 resins. The packaging industry requires reliable and cost-effective adhesive systems, which C5 resins provide. In December 2025, the U.S. Census Bureau reported that retail e-commerce sales for the third quarter of 2025 reached a total value of USD 310.3 billion, which is up 1.9 % from the previous quarter and 5.1 % higher than the same quarter in 2024. On the other hand, the total retail sales for the quarter were USD 1,893.6 billion, wherein e-commerce accounted for almost 16.4 % of all retail sales. The consistent growth of online shopping is driving demand for packaging and related materials, supporting overall C5 resin market growth.

- Shift towards eco-friendly products: There has been a rising adoption of bio-based and sustainable resins, which is the fundamental growth driver for the C5 resin market. In this context, Henkel Adhesive Technologies in February 2026 announced that it entered into a tactical collaboration with a chemical company called Sekab with a prime focus to accelerate the shift from fossil-based to bio-based raw materials in adhesive production. The partnership is mainly focused on replacing conventional ethyl acetate with a sustainable, bio-based alternative, supporting Henkel’s sustainability and innovation goals. Therefore, from a strategic perspective, such initiatives enable high-performance adhesives that reduce environmental impact by efficiently helping customers achieve their climate targets.

Challenges

- Volatility in crude oil prices: C5 resins are derived from petroleum feedstocks such as piperylene and isoprene, which makes production costs highly sensitive to crude oil price fluctuations. Also, the aspect of sudden increases in crude prices raises raw material costs, which are often considered to be difficult to pass on to end-users due to competitive pricing pressures. Besides, these price drops can cause disruptions in terms of supply-demand economics for producers who have invested in fixed-capacity plants. This volatility impacts profitability and makes long-term planning highly complex, particularly for small and mid-sized producers in the C5 resin market who are lacking vertical integration. In this context, companies need to opt for hedging strategies and long-term supply contracts to address the financial and operational risks which are associated with crude oil price instability.

- Environmental and regulatory pressure: Governments, along with regulatory bodies across the globe, are imposing stricter environmental standards for chemical manufacturing, which also includes hydrocarbon resins. These regulations are mainly targeted at VOC emissions, air quality, and waste management, thereby compelling manufacturers to make investments in cleaner production technologies. Meanwhile, the aspect of non-compliance can lead to penalties and restricted market access. In addition, adapting to these standards increases operational costs and may require research into hydrogenated or bio-attributed C5 resins to meet environmental compliance. Therefore, companies need to balance sustainability initiatives with profitability by maintaining product performance in the C5 resin market.

C5 Resin Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.4% |

|

Base Year Market Size (2025) |

USD 952.5 million |

|

Forecast Year Market Size (2035) |

USD 1.52 billion |

|

Regional Scope |

|

C5 Resin Market Segmentation:

Application Segment Analysis

The adhesives & sealants subtype is expected to dominate the application segment of the C5 resin market, capturing 45.6% share during the forecast period. The segment’s dominance is highly driven by a strong growth in packaging, hygiene products, and industrial bonding applications. In addition, the rising adoption of solvent-free adhesives efficiently drives demand for hydrocarbon resins used as tackifiers. In July 2025, Henkel Adhesive Technologies announced the launch of Loctite Liofol LA 7837/LA 6265, which is a solvent-free, high-performance adhesive system especially designed for demanding flexible packaging applications, including retort packaging for pet food and ready meals. The system improves sustainability by eliminating energy-intensive drying steps, reducing material consumption, and lowering CO₂ emissions. Hence, such innovations highlight the shift toward efficient, eco-friendly adhesives that meet stringent safety requirements.

Type Segment Analysis

By the conclusion of 2035, the aliphatic C5 hydrocarbon resin, which is a part of the type segment, is anticipated to garner a considerable share in the C5 resin market. They provide excellent compatibility with natural rubber, synthetic rubber, and elastomers used in adhesives and rubber compounding, which is the main factor driving the sub-segment’s leadership. As per an article which was published by the National Institute of Health (NIH) in January 2026, it demonstrated the production and optimization of petroleum resins, which include hybrid aliphatic-aromatic resins (C5), by using cationic polymerization with AlCl3 catalysts. In this context, the report stated that the synthesized C5 resins showed excellent compatibility with natural rubber, synthetic rubber, and elastomers, making them suitable for adhesives, coatings, and rubber compounding. Hence, this work provides a proper framework for producing high-performance resins that support C5 resin market demand in adhesives and elastomer applications.

Top Petroleum Resin Exporting Countries Based on Official Trade Data (2024)

|

Country |

Export Value (USD) |

|

China |

1.31 billion |

|

U.S. |

1.15 billion |

|

Germany |

1.08 billion |

|

South Korea |

714 million |

|

Japan |

701 million |

|

France |

374 million |

|

Netherlands |

324 million |

|

Belgium |

241 million |

|

Italy |

188 million |

|

China - Taipei |

172 million |

Source: OEC

End use Industry Segment Analysis

Construction is projected to be the leading end user industry segment, which is propelled by the burgeoning infrastructure and building activities across the world. The C5 resins are extensively utilized in coatings, waterproofing materials, and road-marking paints, due to their excellent adhesion, chemical resistance, and durability, which enhance product performance as well as longevity. These resins improve the mechanical and thermal stability of construction materials by ensuring that they withstand harsh environmental conditions and heavy usage. In addition, their compatibility with various polymers allows formulators to develop suitable solutions for different sorts of applications, from protective coatings to elastomer-modified waterproofing compounds. Meanwhile, there has been a growing focus on sustainable, high-performance construction materials, which in turn supports the adoption of C5 resins in both residential and commercial building projects, thus solidifying their critical role in the C5 resin market’s expansion.

Our in-depth analysis of the C5 resin market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Type |

|

|

End use Industry |

|

|

Physical Form |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

C5 Resin Market - Regional Analysis

APAC Market Insights

The Asia Pacific c5 resin market is projected to hold the largest market share of 35.6% by the conclusion of 2035. The region’s leadership is mainly driven by strong manufacturing growth, rising construction activities, and expanding automotive production in China, India, Japan, and South Korea. In addition, the rapid growth in the packaging and adhesive industries also supports regional demand for C5 resins. According to the article published by Adhesives Organization in February 2025, Sika has expanded its presence in the region with two new plants in Singapore and Xi’an, China, thereby boosting the availability of adhesives, sealants, and construction solutions. The Singapore facility focuses on mortars for the dense metropolitan sector, whereas the Xi’an plant produces a wide range of products, including tile adhesives, waterproofing, and flooring solutions, making it suitable for bolstering the regional C5 resin market growth.

The robust expansion efficiently fueled by the surging demand for hot-melt adhesives within the packaging and hygiene sectors is the main factor responsible for the C5 resin market in China. The country is witnessing a structural shift towards the production of hydrogenated grades, which offer superior thermal stability and transparency for high-end applications such as medical supplies and food-grade sealants. Based on the government data, which was published in September 2025, the country has set a target to achieve an average annual growth of over 5 % in the added value of its petrochemical and chemical industries for 2025-2026. The crucial measures that were mentioned include the expansion of high-end chemical supply, accelerating breakthroughs in critical products such as electronic chemicals and high-end polyolefins, and developing high-quality chemical parks and industrial clusters, thus benefiting the overall C5 resin market growth in the country.

The C5 resin market in India is witnessing a transformative phase of growth, which is driven by the surging automotive and e-commerce sectors. The domestic companies are focused on expanding manufacturing plants to meet the demand arising from pavement markings and industrial coatings. In July 2024, Henkel India reported that it had completed Phase III of its Kurkumbh manufacturing facility near Pune, thereby expanding production of high-performance adhesives, sealants, and surface treatment products under the Loctite brand. Besides, this plant is equipped with Industry 4.0 technologies and an automated storage and retrieval system, which aims to localize production, meet growing domestic demand, and reduce import dependence. Furthermore, the transition toward low-odor applications is encouraging local suppliers to enhance their production technologies and supply chain capabilities.

North America Market Insights

The North America C5 resin market is forecasted to be the fastest growing landscapes during the stipulated time frame. The region’s prominence in this field is mainly driven by the presence of numerous paint and coating industries. On the other hand, the higher consumption in the tire manufacturing, adhesives, and infrastructure coatings also fuels the regional market growth. In May 2025, Neville Chemical notified that it had expanded its partnership with IMCD to increase U.S. availability of its hydrocarbon and specialty resins for adhesives and coatings manufacturers. The company’s key products, such as the NEVTAC series, consist of C5 and aromatic-modified aliphatic resins that enhance tack, peel strength, and versatility across adhesive, rubber, and coating applications. Hence, based on such consistent efforts from players, there is a huge growth opportunity for the C5 resin market in the region.

The increasing adoption of C5 resins in printing inks, the construction, and footwear sectors is the main fueling factor behind the robust growth of the U.S. C5 resin market. Growth is also supported by rising demand from formulators who are looking for low-viscosity, easily processable resins for advanced adhesive systems, as well as by initiatives to enhance domestic production capacities and supply chain efficiencies to meet evolving industry requirements. In April 2025, the U.S. Census Bureau reported that total construction spending reached annual rate of USD 2,195.8 billion (seasonally adjusted), which reflects almost 2.9% increase when compared to February 2024. The report also notes that private construction accounted for a total of USD 1,686.4 billion, wherein the residential and nonresidential projects both showed growth, whereas the public construction spending totaled USD 509.3 billion, supported by educational and highway projects, hence increasing demand for building materials, coatings, sealants, and associated industrial applications.

The booming logistics sectors, which utilize C5 resins extensively in hot-melt adhesives for cold-resistant shipping materials, drive the C5 resin market in Canada. The country’s market also benefits from government backing and rising environmental awareness, which increases the transition toward high-purity hydrogenated grades that offer better stability and lower emissions for indoor applications. Based on the government data, which was published in April 2024, Environment and Climate Change Canada and Health Canada assessed petroleum resins, hydrocarbon resin, and polymerized C5-12 distillates by concluding that these substances present low risk to human health and the environment. The report highlights that these resins are used in hot melt glues, tackifiers, and construction adhesives, with concentrations ranging from 10% to 60%, and are considered to be safe due to their high molecular weight and low volatility, hence positively impacting the market’s growth and exposure in the country.

Europe Market Insights

The Europe C5 resin market is growing significantly on account of strong emphasis on sustainability and regulatory compliance. The stricter standards are shifting the industry toward low-VOC and bio-based alternatives. Meanwhile, the major industrial hubs such as Germany, France, the UK, and Italy are leading the adoption of these advanced resins, particularly for energy-efficient construction and lightweight vehicle manufacturing. In this context, the Council of the region and Parliament in December 2023 reached a provisional agreement by updating the CLP regulation for the classification, labelling, and packaging of chemical substances. This particular revision improves clarity of hazard information, introduces digital and circular economy measures, and applies to all trade forms, including online and refillable products. In addition, this regulatory update efficiently strengthens consumer safety, ensures better environmental protection, and directly affects chemical producers in the region, including hydrocarbon resin and C5 resin manufacturers.

The C5 resin market in Germany is considered to be a central hub for high-tech chemical applications, driven largely by the automotive and industrial manufacturing sectors. Manufacturers in the country are at the forefront of integrating bio-based feedstocks and sustainable production processes to align with rigorous national energy efficiency goals. In November 2024, the Fraunhofer WKI reported the development of bio-based adhesives, which are made from renewable raw materials and biogenic residues. These adhesives are especially designed for applications in lightweight and hybrid construction, thereby enabling material-efficient bonding and easier recyclability, including switchable adhesives that allow wood and metal components to be separated at end-of-life. In addition, the research is also exploring formaldehyde-free lignin-sugar adhesives, humin-based wood bonding, and fungal mycelium binders, thereby supporting a bio-based circular economy in the construction and mobility sectors.

The rising demand across the packaging and construction sectors is responsible for uplifting the C5 resin market in the UK. Growth is largely propelled by the rapid expansion of e-commerce, which has increased the need for high-performance hot-melt adhesives and sustainable packaging solutions, particularly in the food and beverage industry. The clear movement toward specialty grades, such as low-odor and low-VOC hydrogenated formulations, is the main trend reshaping the growth trajectory of the country’s market. In September 2025, the country’s government reported that Eastern Shires Purchasing Organisation (ESPO), operated by Leicestershire County Council, issued a government tender for the supply of glues, adhesives, and adhesive tapes across the UK. The framework is valued at approximately USD 24 million and covers bulk delivery of adhesive products to ESPO’s distribution centre in Leicester, hence denoting a positive outlook for the market’s growth and exposure.

Key C5 Resin Market Players:

- ExxonMobil Chemical Company (U.S.)

- Eastman Chemical Company (U.S.)

- Kolon Industries, Inc. (South Korea)

- Zeon Corporation (Japan)

- Arakawa Chemical Industries, Ltd. (Japan)

- Idemitsu Kosan Co., Ltd. (Japan)

- Neville Chemical Company (U.S.)

- Resinall Corporation (U.S.)

- Cray Valley (TotalEnergies Group) (France)

- Formosan Union Chemical Corporation (Taiwan)

- Lesco Chemical Limited (China)

- Zhejiang Henghe Petrochemical Co., Ltd. (China)

- Zibo Luhua Hongjin New Material Group Co., Ltd. (China)

- Puyang Changyu Petroleum Resins Co., Ltd. (China)

- Puyang Tiancheng Chemical Co., Ltd. (China)

- Shanghai Jinsen Hydrocarbon Resins Co., Ltd. (China)

- Qingdao Bater Chemical Co., Ltd. (China)

- Shandong Landun Petroleum Resin Co., Ltd. (China)

- Henan Anglxxon Chemical Products Co., Ltd. (China)

- Seacon Corporation (India)

- Braskem S.A. (Brazil)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ExxonMobil Chemical Company is identified as the leading global producer of hydrocarbon resins, which also includes C5-based resins. The company is focused on producing high-performance resins for adhesives, coatings, and rubber compounding. In addition, ExxonMobil benefits from a strong global supply chain, R&D capabilities, and an extensive portfolio, which makes it a dominant player in the market.

- Eastman Chemical Company is a central player in this field, which is a major supplier of hydrocarbons and C5 resins, offering both standard and hydrogenated grades. The company serves adhesives, coatings, and industrial applications worldwide.

- Kolon Industries, Inc. is a prominent specialty chemicals manufacturer that produces C5 and C5/C9 copolymer resins for adhesives, paints, and rubber applications. Besides, the company is also focused on high-quality, low-color, and environmentally friendly resin grades.

- Zeon Corporation is a key producer of C5 hydrocarbon resins and other specialty polymers. The firm emphasizes innovation and sustainability, and it serves adhesives, coatings, rubber compounding, and specialty industrial applications, with a focus on hydrogenated resins, low-VOC formulations, and high-purity grades.

- Arakawa Chemical Industries, Ltd. is a specialist in petroleum resins, which include C5 resins, suitable for adhesives, paints, and the rubber industries. In addition, the company emphasizes high-quality, low-color, and tackifier resins optimized for hot-melt and pressure-sensitive adhesives.

Below is the list of some prominent players operating in the global C5 resin market:

The C5 resin market hosts several multinational petrochemical companies and regional specialty resin producers who are intensely competing on a global scale. Major pioneers such as ExxonMobil Chemical Company, Eastman Chemical Company, Kolon Industries, and Zeon Corporation maintain strong positions through integrated petrochemical supply chains, highly improved hydrogenation technologies, and extensive product portfolios. Most of the manufacturers in this field are focused on developing high-performance and low-VOC hydrocarbon resins to meet growing environmental regulations and demand from the adhesives and coatings industries. In February 2026, Zeon Corporation, through its venture arm Zeon Ventures, Inc., reported that it made a total investment of USD 50 million in Chemify Ltd. with the main goal to accelerate digital chemistry innovation. The partnership will leverage Chemify’s Chemputation technology to automate molecular design, synthesis, and testing for advanced materials.

Corporate Landscape of the C5 Resin Market:

Recent Developments

- In September 2025, Braskem announced that it would be participating in ABRAFATI 2025, where it showcased its portfolio of raw materials for the paint industry. The company highlighted its Unilene hydrocarbon resins, which enhance gloss and drying performance in paints and coatings.

- In July, 2025, Neville Chemical Company announced that it entered into a strategic partnership with Azelis Canada, appointing the company as its distributor in Canada for hydrocarbon and specialty resins used in coatings and adhesives.

- Report ID: 4058

- Published Date: Mar 18, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

C5 Resin Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.