Composite Resin Market Outlook:

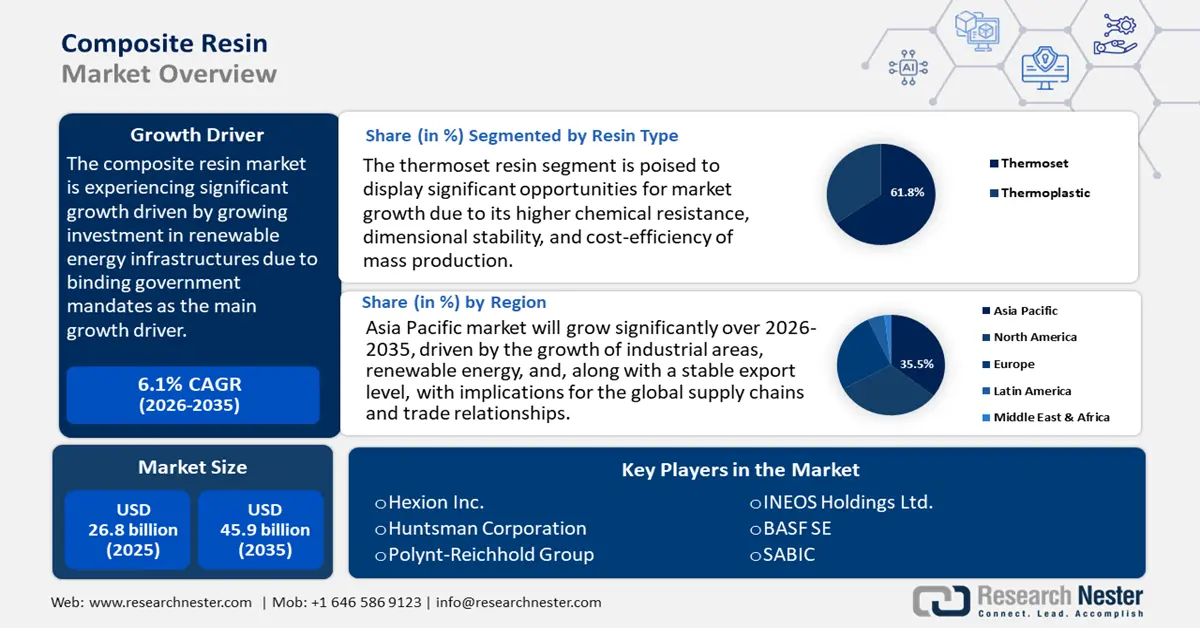

Composite Resin Market size was valued at USD 26.8 billion in 2025 and is projected to reach USD 45.9 billion by the end of 2035, rising at a CAGR of 6.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of composite resin is assessed at USD 29.1 billion.

The global composite resin market is anticipated to grow with an upward trend, primarily driven by the growing investment in renewable energy infrastructures due to binding government mandates as the main growth driver. The European Union has established a goal of at least 42.5% renewable energy in the energy mix of its member states by 2030, and it provides a direct demand boost in advanced composite materials that are utilized to design wind power turbine blades, solar panel structures and grids, and poles. The states of the EU target the rise of renewable electricity up to 66% by 2030, which supports even further the alignment of supply chains and production with the climate objectives of the EU.

India Government policies encourage growth in wind power capacity and industrial production. India aims to generate 50% of its electricity from non-fossil sources by 2030, supported by a government target of 500 GW renewable energy capacity, including 140 GW from wind power. As of March 2022, wind capacity stood at 40.358 GW, with strong growth potential estimated at 695.5 GW. The Ministry of New and Renewable Energy supports indigenous technology development and collaborates actively with IEA Wind TCP to drive innovation and industrial production. These efforts in legislation quicken the demand for composite resins for energy projects and grid hardware.

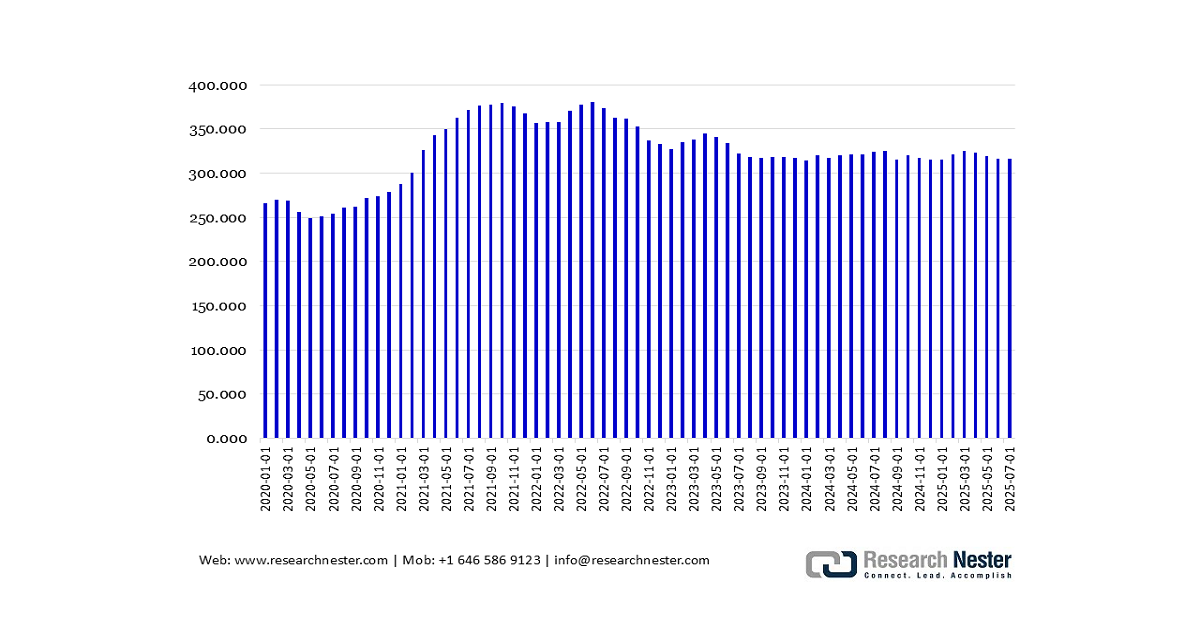

The material supply chain of composite resins globally is underpinned by rising levels of plastics and synthetic industrial feedstocks imports, with U.S. Customs data indicating steady growth in the past five years of import volumes of plastic materials, a major building block in resin manufacture and downstream assembly line configurations both in the U.S. and overseas. The expansion of the manufacturing capacity has been aligned with the region's trade policy, where more assembly lines and capacities are developed to keep up with the expectations of growth in the transportation, infrastructure, and energy domains. The graph below represents the Producer Price Index for Plastics Material and Resin Manufacturing.

PPI by Industry: Plastics Material and Resin Manufacturing

Source: U.S. Bureau of Labor Statistics via FRED

Globally, investments in research, development, and deployment (RD&D) are rising significantly. This growth is particularly strong in fields that enable renewable energy integration and industrial modernization, a trend clearly reflected in official national science funding reports and policy frameworks from key regions like the European Union and India. For example. The EU’s Fit for 55 agenda allocates significant funding, 30% of its 2021–2027 budget and 35% of Horizon Europe’s research funds to climate action and green innovation. Similarly, India aims to install 450 GW of renewables by 2030, supported by initiatives like the International Solar Alliance and LeadIT, fostering technology exchange and industrial transformation, highlighting a reinforced focus on advancing clean energy and sustainable industrial growth.

Key Composite Resin Market Insights Summary:

Regional Highlights:

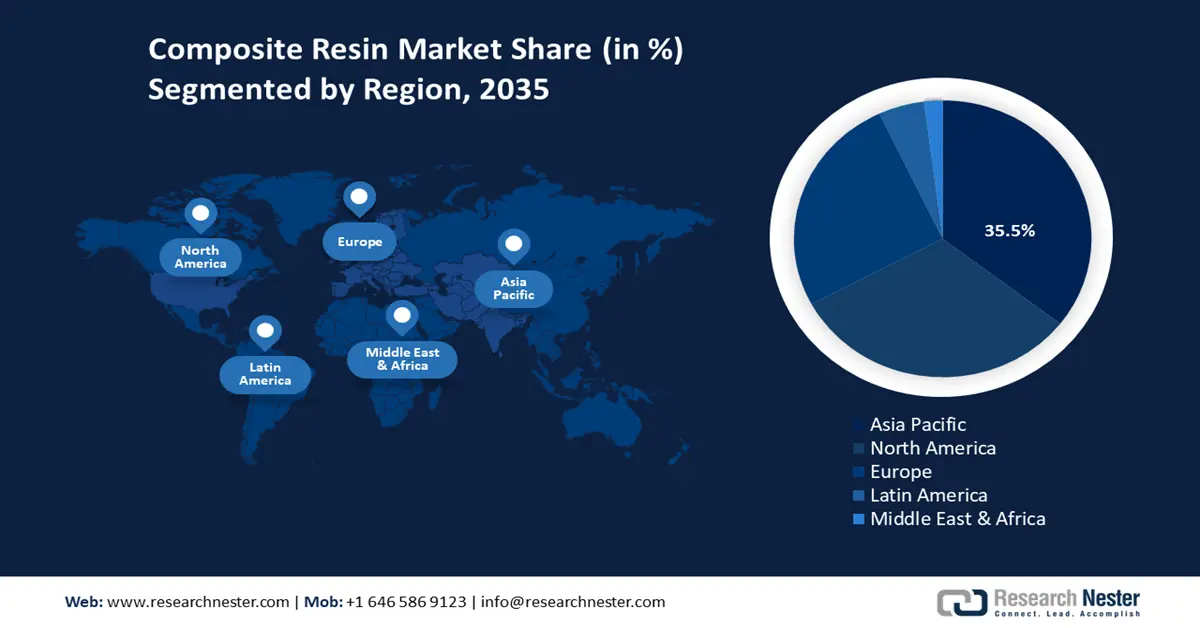

- By 2035, the Asia-Pacific region is projected to command a 35.5% share of the composite resin market, attributed to the expansion of industrial zones, renewable energy initiatives, and rising sustainability requirements.

- North America is anticipated to secure a 31.7% share by 2035, supported by strong momentum in automotive, construction, electronics, and renewable energy sectors.

Segment Insights:

- Thermoset resins are expected to capture a 61.8% share by 2035 in the composite resin market, propelled by their higher chemical resistance, dimensional stability, and cost-efficiency in mass production.

- Injection molding is set to hold a 39.7% share from 2026–2035, underpinned by its scalability, precision, and operational efficiency.

Key Growth Trends:

- Lightweight, high-performance materials demand

- ECHA PVC & additive regulations

Major Challenges:

- Increasing environmental compliance costs

- Barriers to market access

Key Players: Hexion Inc., Huntsman Corporation, Polynt-Reichhold Group, INEOS Holdings Ltd., BASF SE, SABIC, LyondellBasell Industries, Qenos, Crest Speciality Resins Pvt. Ltd., Polynt Composites Malaysia Sdn. Bhd., Allnex.

Global Composite Resin Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 26.8 billion

- 2026 Market Size: USD 29.1 billion

- Projected Market Size: USD 45.9 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia-Pacific (35.5% Share by 2035)

- Fastest Growing Region: Asia-Pacific

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Vietnam, Mexico, Indonesia

Last updated on : 29 August, 2025

Composite Resin Market - Growth Drivers and Challenges

Growth Drivers

- Lightweight, high-performance materials demand: Lightweight composite resins continue to be in high demand in the automotive and aerospace industries to allow significant weight savings in vehicles, driving fuel effectiveness and emissions reduction. For instance, a 10% decrease in the vehicle weight yields a 6% to 8% increase in the vehicle fuel economy, as per the U.S. Department of Energy (DOE). Work in aircraft indicates that composites in commercial jets can reduce structural weight by around 20%, leading to significant improvements in aircraft efficiency and performance. This weight reduction translates into significant lifetime fuel savings amounting to many tons for large aircraft, which substantially lowers operational costs and carbon emissions. Major models like the Boeing 787 achieve up to 20% fuel savings compared to traditional designs due to extensive composite use. These benefits drive widespread adoption of composites in modern aviation.

- ECHA PVC & additive regulations: A recent comprehensive study by the European Chemicals Agency (ECHA) has assessed the hazards associated with polyvinyl chloride (PVC) and its common additives, including plasticizers, heat stabilizers, and flame retardants. The report recommends implementing new regulatory measures to limit exposure to ortho-phthalate plasticizers and organotin stabilizers due to their identified risks. Furthermore, it underscores the urgent need to advance technological solutions addressing PVC microplastic pollution, which poses significant environmental and potential health threats. The findings from the European Chemicals Agency (ECHA) are creating significant regulatory pressure on the EU to move beyond substance-by-substance restrictions and adopt broader measures against entire groups of chemicals. This shift creates a legal obligation that compels manufacturers to invest in the redevelopment of resin chemistries and accelerate innovation toward safer, more sustainable alternatives.

- Green chemicals & sustainability initiatives: Regulatory pressures, with sustainability goals, are encouraging the transformation of the chemical industry toward green chemicals. The U.S. market for green chemicals was valued at $3.9 billion in 2024 and is projected to reach $7.5 billion by 2033, reflecting a trajectory toward maturity comparable to other established green product sectors. This growth is primarily catalyzed by evolving EPA mandates and strengthening consumer demand for bio-based and non-toxic ingredients. Life Cycle Assessments indicate that bio-based resin alternatives have lower overall environmental impacts of 11-16% in all areas relative to standard petrochemical-based resins, supporting the fact that switching to more bio-based inputs in composite resin products is poised to expand into its market rapidly and transition to renewable inputs.

Composite Resin Utilization in Industrial Manufacturing

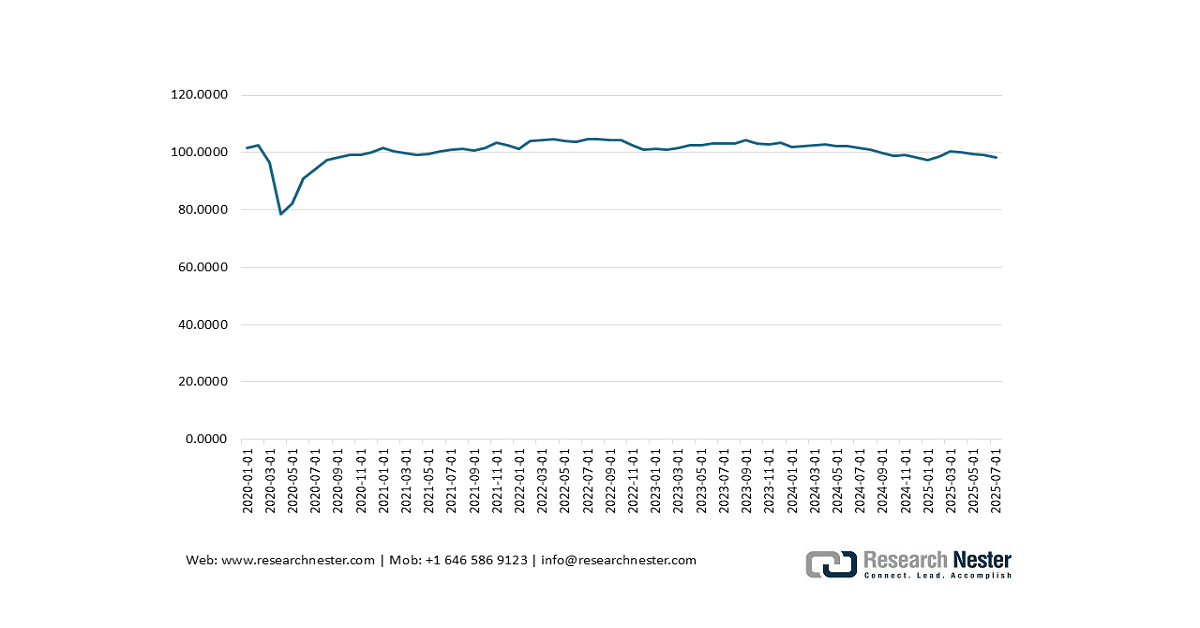

The plastics and rubber products manufacturing sector (NAICS 326) relies heavily on composite resins as critical raw materials for producing finished and intermediate goods. Composite resins such as epoxy, polyester, and vinyl ester serve as the matrix component in composite materials, where they bind reinforcing fibers like fiberglass or carbon to create lightweight, durable products. Establishments within NAICS 326 (e.g., manufacturers of automotive parts, aerospace components, or consumer goods) process these resins through molding, extrusion, or lamination to create final products. Thus, composite resins act as upstream inputs enabling innovation and value-added production within the downstream plastics and rubber manufacturing industry.

Industrial Production: Manufacturing Goods: Plastics and Rubber Products (NAICS = 326)

Source: Board of Governors of the Federal Reserve System (US) via FRED

Challenges

- Increasing environmental compliance costs: In the U.S., the costs of environmental compliance are rising among composite resin manufacturers due to strict EPA regulations regarding the emission of hazardous air pollutants into the environment caused by reinforced plastic composites manufacturing. NESHAP dictates that the facilities install state-of-the-art control technologies and have extensive monitoring of their emissions. The EPA reported that the final rule resulted in a nationwide annual decrease of 7,682 tons of hazardous air pollutants, a 43% decrease. Although this improves air quality and health outcomes, it also substantially causes a large increase in operating expenses, especially difficult for small and mid-sized manufacturers to remain competitive and drive industry association.

- Barriers to market access: The entry of composite resins suppliers into the global composite resin market is faced by stiff competition in terms of protecting domestic industries through the use of tariffs, importation quotas, licensing, and technical standards, which are currently in operation in many countries. The WTO recognizes that technical regulations, standards, testing, and certification requirements, key forms of non-tariff barriers, can hamper market access and create disproportionate challenges for small and medium exporters. Technical requirements (e.g., technical requirements on chemical composition or recycling requirements) also impose lead time and incur additional compliance costs in some regions. This has forced most composite resin suppliers to invest in legal, technical, and logistical capacities to overcome entrance complexities in the global markets to augment their operational expenses and economic losses towards universal dispensation of innovative chemical products.

Composite Resin Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2024 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 26.8 billion |

|

Forecast Year Market Size (2035) |

USD 45.9 billion |

|

Regional Scope |

|

Composite Resin Market Segmentation:

Resin Type Application Segment Analysis

Thermoset resins are anticipated to dominate the composite resin market share, capturing 61.8% by 2035. This dominance is attributed to their higher chemical resistance, dimensional stability, and cost-efficiency of the mass production. Unsaturated polyester resins have a great preference in their use in construction and automotive parts like panels and reinforcement, as they handle the harsh operating environments. These modified resins, vinyl ester resins, and phenolic resins have improved corrosion resistance over marine or industrial tanks, and phenolic resins are strong in high-temperature environments and fire-resistant in transport and building panels. The U.S. Department of Energy estimated that the durability and long life of thermosets enable them to be used in demanding infrastructure and transport projects. This flexibility and the ability to customise to specific needs keep them part of the wider innovation within the industry. The emerging pressure to operate spurring sustainability requirements is also forcing manufacturers to produce bio-based derivatives of thermoset resins that reduce carbon footprints to achieve properties required to meet specifications of green buildings.

The leading sub-segments contributing to expansion in the thermoset composites are epoxy resin and unsaturated polyester resins. Superior mechanical strength, adhesion, and chemical resistance are unique to Epoxy resins, making them indispensable even in the aerospace industry, wind energy generation, and automotive structural industries. The use of epoxy-based composites makes up a large part of the aircraft's primary structure, such as the Boeing 787, and the composites contribute to dramatic fuel burn reduction and also serve to help save operating costs. Unsaturated polyester resins prevail in the building, marine, and automobile body panel applications because they are completely manufacturable and versatile in their applications. These resin forms justify the market-dominant position of the thermoset segment and contribute to innovation in lasting, high-performance applications in changing industries.

Manufacturing Process Segment Analysis

Injection molding is estimated to expand its significant composite resin market share of 39.7% from 2026 to 2035, owing to its scalability, precision, and operational efficiency. This process allows manufacturers to make precise geometric shapes with close tolerances in a large production volume, which makes the production process essential in the fabrication of automotive interior trim components, electronic gadget housings, and appliances, as well as medical device casings. Department of Energy underlines injection molding as the most preferred technique of accelerating the trend of lightweight in mobility because the technique allows the manufacturing of highly designed plain resin materials, and the procedure produces occupants of a highly defined and patterned design in the lowest possible count of cycling them, and also has the capability of dealing with thermoset and thermoplastic product formulations. As the automotive and electronics industries face a need for fast prototyping and large volume manufacturing, the use of injection molding is necessitated by the compatibility with automation technologies to manage competitive supply chains. Its flexibility in numerous compositions and applications in the composition of its materials will remain a major pillar in its dominance in the composite resin market.

Injection molding is a foundational manufacturing procedure for composite resin parts, delivering accurate and durable products for high-impact applications such as automotive internal parts and electronic housings. Injection molding is also used in automotive interiors to manufacture dashboards, door boards, and problems in the console as these help to give a very lightweight solution to enhance the fuel economy. The U.S. EPA Automotive Trends Report adds that switching out conventional materials with plastics, such as injection-molded parts, allows manufacturers to boost car energy efficiency by 2% per 45kg switched, and plastics make up an approximate 20% share of total weight in a modern car. This weight loss is a direct contribution to the reduction of emissions, as well as smarter value addition of resources by automakers towards electric and hybrid platforms.

Injection molding is used to produce mass quantities of insulated and precision housings for consumer electronics and industrial controls in electronic housings, where this process allows housing to be produced in greater mass quantities by electrical safety and electromagnetic compatibility requirements, as well as environmental standards such as RoHS, VDE, and UL. Polyamide and polycarbonate are excellent mechanical and electrical materials that find wide usage as injection moldable materials by fabricators who have to meet the most demanding thermal and safety needs. Such advantages guarantee the maintenance of injection molding's dominant position in the automotive industry and advance the segment of electronics, enhancing the energy efficiency of a product and its conformity.

Application Segment Analysis

The automotive sector is anticipated to grow at a composite resin market share of 34.3% over the forecast years from 2026 to 2035, driven by essential sub-streams such as structural elements, battery covers in electric cars, interior part components, and bumpers. Government regulations on fuel economy and greenhouse gases, from agencies like the EPA, further accelerate the growth of the market. The U.S. EPA reports that the transportation sector accounted for the largest share 28% of total U.S. greenhouse gas emissions in 2022, making it the top source among all sectors, as per the annual Inventory of U.S. Greenhouse Gas Emissions and Sinks 1990–2022, with contributions from cars, trucks, commercial aircraft, railroads, and other transportation sources. To help automakers meet stricter emissions limits, the EPA has promoted advanced materials such as composite resins that enable significant vehicle weight reductions, improved fuel efficiency, and greater design flexibility, especially critical as manufacturers shift toward electric vehicles. The use of composite resins in crash safety, light construction, and advanced electrification platforms provides the guarantee of their long-term development in the automotive architecture in the period to be forecasted.

Our in-depth analysis of the composite resin market includes the following segments:

| Segment | Subsegments |

|

Resin Type |

|

|

Manufacturing Process

|

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Composite Resin Market - Regional Analysis

Asia Pacific Market Insights

The Asia-Pacific composite resin market is expected to dominate the global landscape with the largest revenue share of 35.5% over the forecast years, due to the growth of industrial areas, renewable energy, and the need to address sustainability. According to the United States International Trade Commission, Asia-Pacific countries like South Korea, Taiwan, Thailand, China, and India are significant exporters of epoxy resins. The countries have demonstrated a stable export level with implications for the global supply chains and trade relationships. The growing production of coal and electricity in the Asia Pacific is increasing the amount of CO2 emissions, thus contributing to the demand for composite resins. Since the region is also inclined towards sustainability, the composite resins stand out to enhance fuel efficiency and sustain clean energy, assuring market growth. For example, in 2022 Asia Pacific produced 17,465 Mt of CO2 through the combustion of fuel, contributing 51.2% of world emissions. Coal accounts for 69.5% of emissions, and electricity production is the biggest one at 54.1%. Emissions in the region have increased by 147% since 2000, and it is because of China and India.

By 2035, China’s composite resin market is expected to lead the Asia Pacific region due to significant industrialization within the country and robust automotive, wind power, and construction sectors, among others. China has spent more on clean energy technology than the other leading 10 nations combined in 2023, with greater than 60 per cent financing renewables-based energy and transport electrification. It hit its non-hydro energy storage aim of 2025 before schedule, standing at 31.4 GW, with more than 100 billion yuan (USD 13.9 billion) of investments. Over 30+ projects received 260 billion RMB (USD 35.9 billion) in the Chinese green hydrogen sector. Government policies on and R&D investments are 2.5 times as much as the rest of the world will enable the country to continue to lead in clean tech exports, which is projected to surpass USD 340 billion by 2035.

The mass use of bio-based resins in the composite resin market is stimulated by government initiatives like the initiative of China to make lightweight, recyclable, and low-emission materials, which are enhanced by the Made in China 2025. For instance, China presents a circular economy that helps it to execute its carbon ambitions by advancing lightweight, recyclable, and low-emission materials, such as bio-based resins. Such a strategy would limit emissions in difficult-to-decarbonise industries, such as plastics, ensure secure access to raw materials needed in renewable energy, and increase economic security. Policies promote product redesigning, reuse, and product material substitution, which promotes sustainable industrial development and market acceptance of eco-friendly materials. This makes China a global leader in composite resin development in the name of sustainability and high-end material technologies.

India’s composite resin market is estimated to grow at the fastest CAGR from 2026 to 2035, represented by increasing demand in major industries, including construction, transportation, and renewable energy. Constant growth in infrastructure development, coupled with the use of the industry, is expected to push the market into a value of over INR 24,000 crore (roughly USD 2.8 billion) by 2030. The market is expected to grow at a CAGR of 7.8%, supported by government initiatives like smart cities and renewable energy projects. Key manufacturing centres such as Gujarat, Maharashtra, and Tamil Nadu play an important role in expanding manufacturing capacity. The Indian epoxy resin market is projected to reach 186.1 kilotons in 2025 and is expected to grow at a CAGR of 8.0% to reach 271.3 kilotons by 2030, driven by the adoption of eco-friendly and bio-based resin solutions. Furthermore, initiatives by the government, such as the Make in India and Smart Cities Mission, are encouraging sustainable chemistry and innovations with advanced technologies.

North America Market Insights

North America composite resin market is expected to grow at a significant revenue share of 31.7%, during the projected years, by 2035. This growth is attributed to robust activity in automotive, building & construction, electronics, and renewable energy markets. In 2022, 125.5 billion pounds of resin were produced by the North American industry (an increase of 1.3% over 2021 or 123.9 billion pounds); sales and captive use hit 126.8billion pounds (an increase of 2.8 percent). In 2022, the production of plastic products was up by 4.1% on 2021, exports grew by 9.9 to 18.3 billion, and imports surged 6.5% to 49.6 billion, indicating high levels of regional trade and manufacture.

Output of the building and construction industry increased by 3.2%, and in the automotive industry, there was an average of 411pounds of plastics and composites per vehicle use- quantity, which indicates huge resin use and adaptation in advanced manufacturing. In the electronics market, resin consumption increased by 2.4% in 2022 to aid the innovation of both consumer and industrial products. Such statistics emphasize the diversification of composite resin market drivers in North America and the fact that North America leads the world in resin technology. The CAGR is expected to grow at a notable rate by 2035, sustained through continued investment in reducing the weight of materials, green innovation, and safety and sustainability-minded regulatory standards.

The composite resin market in the U.S. is expected to lead the North American region by 2035, attributed to the increasing demand for composite resin in the automotive, construction, aerospace, and clean energy industries. Resin manufacture in the U.S. makes up the majority of the total 125.5 billion pounds produced across North America, and projections have the output of plastics products increasing by 4.1% in 2022. Manufacturers in the U.S. consume 411 pounds of plastics and composites on average per vehicle, with tremendous market penetration in the transportation market. In 2023, the U.S. Department of Energy (DOE) announced USD 30 million in funding to advance composite materials, including composite resins, and additive manufacturing for large wind turbines, including offshore wind energy systems.

The initiative supports DOE’s Offshore Wind Supply Chain Road Map by focusing on additive manufacturing of large wind blades using polymer-based composite resins for rapid prototyping and tooling. It also aims to improve the cost and performance of non-blade turbine components through advanced materials and manufacturing techniques. Additionally, the program emphasizes automation, digitalization, sustainability, and modular construction to address manufacturing challenges. OSHA ensures high-level measures of resin management and production safety that enhance the safeguarding of the working processes and the protection of the employees. There are also several federal and private sustainability grants in the U.S., which encourage recyclable and bio-based composite resins to be developed.

Canada’s composite resin market is likely to expand at a steady pace, driven by the high investments in the country within the framework of clean technologies and sustainable materials. In 2023, the Department of Natural Resources Canada established the Clean Fuels Fund to drive acceleration of advanced materials-such as composites, in the energy industry with an outlay of USD 1.5 billion. The Environmental Protection Act requires high standards in the manufacture of chemicals and in their waste disposal, increasing the eco-friendly production of resins in Canada. The Canadian research projects emphasize innovation in bio-composites and recycling of resins, which places it in a good position in sustainability. Cross-sector partnerships with universities and industry organizations lead to better technological capability and resilience of supply chains. Canada, with its federal initiatives and world vision on clean manufacturing, is even gaining momentum in determining the future of the composite resin markets.

Europe Market Insights

The European composite resin market is witnessing rapid growth, owing to industrial innovation and sustainability regulations, as well as the European Union's strategic investment. By 2025, it is predicted that Europe will consume about 39.5% of the total composite resin around the world, followed by thermosetting resins, predominantly epoxy and polyester resin, dominating because of their robustness and capacity to resist high temperatures. The EU champion research and innovation program, aka Horizon Europe, has set aside 93.5 billion Euros covering 2021-2027, majorly focusing on green chemical innovation and innovative materials. These funds have already seen an increase in demand for composite resins in member states, especially in the sectors of wind energy, automotive industries, as well as the aerospace industries. The EU push on bio-based and recyclable resins is also bringing a faster innovation with production capacity on bioplastics set to increase by more than 2 times, from around 2.47 million tonnes in 2024 to approximately 5.73 million tonnes by 2029. This growth is fuelled by the development of biobased and biodegradable polymers such as PLA, PHA, biobased polyethylene (PE), and polypropylene (PP), reflecting strong diversification and expansion of sustainable resin materials. Europe, with its powerful policies and industry impetus, will continue reigning as the world leader in composite resin development up to 2035.

Key Composite Resin Market Players:

- Hexion Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Huntsman Corporation

- Polynt-Reichhold Group

- INEOS Holdings Ltd.

- BASF SE

- SABIC

- LyondellBasell Industries

- Qenos

- Crest Speciality Resins Pvt. Ltd.

- Polynt Composites Malaysia Sdn. Bhd.

- Allnex

The composite resin market is competitive globally, where the top players have associated themselves with vertical integration, expansion, as well as sustainable innovation to retain reliability in the market. Companies such as BASF, Hexion, and Mitsubishi Chemical are putting effort into bio-based resins and higher-end technologies of manufacturing that include RTM and 3D printing, in their efforts to reduce the cost and increase the efficiency of their production process. Global supply chains and R&D capabilities have been enhanced by strategic mergers, i.e., the consolidation between Polynt and Reichhold. Asian producers are increasing their competitive advantages because of their low costs and the emerging mass demand in their country. As more compounds are subjected to environmental legislation and form structures for lightweight products in the automotive and aerospace sectors, leading companies are focusing on their recyclable formulations and cyclical economy frameworks to gain market share in the long run.

Top Global Composite Resin Market

Recent Developments

- In May 2025, Huntsman introduced two new bio-based I-BOND resins that feed to composite woods at the LIGNA trade show in Germany. These resins, with a bio-based content of up to 25%, dramatically cut down on the carbon footprint of composite wood products by a margin of 30% over conventional fossil-based resins. This launch hits the increasing popularity of ecologically correct materials and emitting low materials in the sphere of construction and manufacturing in Europe. By this launch, Huntsman would be at the frontline of bio-based chemical solutions, and this comes in line with the stricter environmental policies as well as the growing demand of customers who prefer environmentally friendly products.

- In February 2025, Westlake Epoxy launched new products at JEC World 2025 (March 4-6, 2025- Paris), concentrating on state-of-the-art composite technologies regarding wind power, aero-space, automotive, hydrogen storage, and bicycle industries. Improvements in sustainability through key innovations include recyclable rotor blade technology in wind turbines, providing reuse of composites, and the EpoVIVE portfolio of more sustainable epoxies with higher bio-content, to decrease the product carbon footprint of aeronautical parts. The company devotes its attention to items of efficiency, safety, and sustainability across every new development and offers on-site technical presentations to industry specialists to know more about their solutions.

- Report ID: 8039

- Published Date: Aug 29, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.