Bio Polyols Market Outlook:

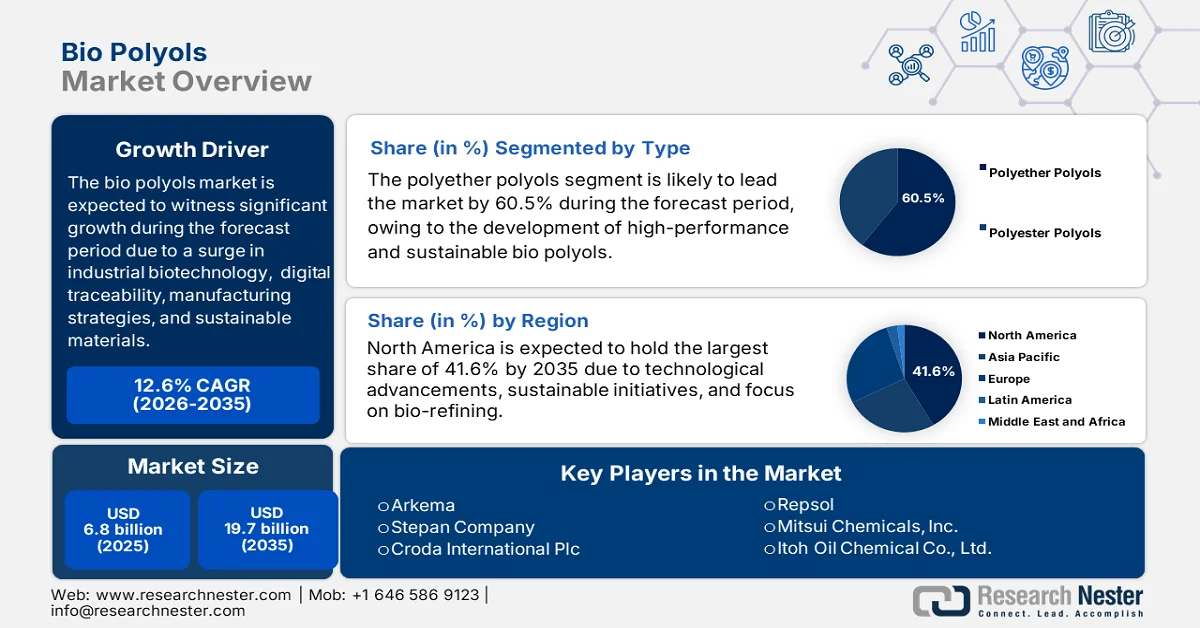

Bio Polyols Market size was over USD 6.8 billion in 2025 and is expected to reach USD 19.7 billion by the end of 2035, growing at a CAGR of 12.6% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of bio polyols is estimated at USD 7.6 billion.

The global bio polyols market is effectively shaped by a complex interplay of social, economic, and technological factors, including innovations in industrial biotechnology, digitalized traceability, and manufacturing efforts to produce high-quality materials with sustainable credentials. According to official statistics published by OECD in November 2025, biosolutions, as part of biotechnology, have the ability to save almost 2.5 billion tons of carbon dioxide. This is equivalent to every year by the end of 2030, by effectively substituting fossil-based products with other technical and environmental improvements. Besides, the Europe Circular Bioeconomy fund, amounting to USD 349 million as a public and private investment fund, is suitable for financing biosolutions. Therefore, with such a provision, there is a huge growth opportunity for the market internationally.

Furthermore, the strategic consolidation through vertical integration, the emergence of second-generation feedstock technologies, functional parity through innovative catalysis, certification infrastructure, digitalized traceability, and circular economy integration are trends that are boosting the market globally. As stated in a data report published by the IATA Organization in September 2025, nearly 400 million tons of sustainable aviation fuel are expected to be produced by the end of 2050. Besides, the worldwide biomass feedstock is predicted to reach more than 12,000 million tons by the same year, owing to increased accessibility to wastes and population growth. This is deliberately less than 35% of the amount that is realistically available for biofuels and bioenergy due to competing utilizations, thereby denoting an optimistic outlook for the market.

Key Bio Polyols Market Insights Summary:

Regional Highlights:

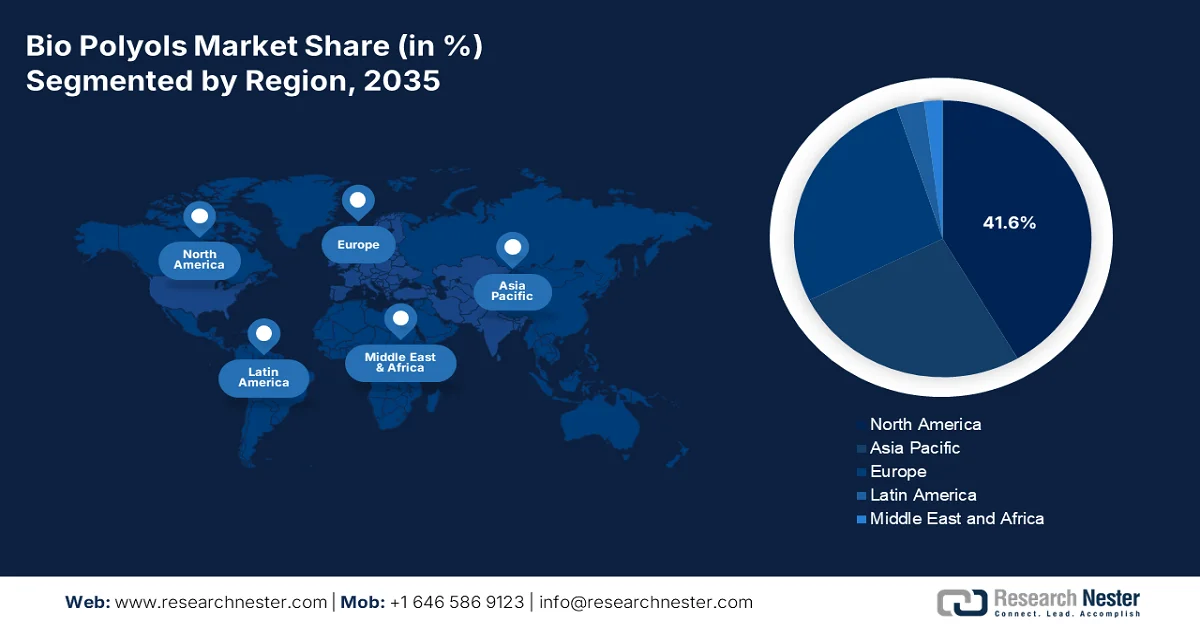

- North America bio polyols market is projected to command a 41.6% share by 2035, supported by strong corporate sustainability initiatives, advanced bio-refining technologies, and favorable regulatory frameworks stimulating renewable chemical adoption

- Asia Pacific is anticipated to emerge as the fastest-growing region in the market during 2026–2035, propelled by accelerating industrialization, expanding urbanization, and increasing availability of bio-based feedstocks

Segment Insights:

- The polyether polyols segment in the bio polyols market is projected to account for a 60.5% share by 2035, stimulated by the growing development of sustainable and high-performance bio-based polyols replacing petroleum-derived alternatives

- The rigid polyurethane (PU) foams segment is anticipated to capture the second-largest share throughout 2026–2035, reinforced by rising demand for high-performance and environmentally sustainable thermal insulation materials

Key Growth Trends:

- Increase of electrification imperatives

- Focus on green building certification

Major Challenges:

- Higher production expenses and economies of scale

- Greenwashing skepticism and certification complexity

Key Players: BASF (Germany), DuPont (U.S.), Dow (U.S.), Huntsman Corporation (U.S.), Cargill, Incorporated (U.S.), Emery Oleochemicals (Malaysia/U.S.), Arkema (France), Stepan Company (U.S.), Croda International Plc (UK), Repsol (Spain), Mitsui Chemicals, Inc. (Japan), Itoh Oil Chemical Co., Ltd. (Japan), Jayant Agro-Organics Limited (India), Covestro AG (Germany), Oleon NV (Belgium), BioBased Technologies (U.S.), Vertellus (U.S.), Stahl Holdings B.V. (Netherlands), Polioles (Mexico), Daicel Corporation (Japan).

Global Bio Polyols Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.8 billion

- 2026 Market Size: USD 7.6 billion

- Projected Market Size: USD 19.7 billion by 2035

- Growth Forecasts: 12.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (41.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: South Korea, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 9 March, 2026

Bio Polyols Market - Growth Drivers and Challenges

Growth Drivers

- Increase of electrification imperatives: The sudden transition towards electric vehicles has significantly intensified the focus on light-weighting to expand battery range and polyurethane components, which is positively impacting the bio polyols market globally. According to official statistics published by the World Resources Institute in December 2025, globally, 22% of passenger vehicles have been sold as electric as of 2024, which is 8 times higher than the previous 5 years. Besides, in terms of overall passenger electric vehicle sales, China has significantly emerged as the ultimate leader, with 11.3 million in 2024. This is deliberately followed by 1.4 million in the U.S., 570,000 in Germany, 550,000 in the UK, and 450,000 in France, thereby positively impacting the market expansion.

- Focus on green building certification: The embracing of green building certificate systems in the construction industry has created a measurable economic premium for bio-based materials in the market. As per an article published by The World Economic Forum in June 2024, BCG has successfully identified 11 tactical transition levers across the overall buildings value chain, intended to unlock more than 80% of the industry’s abatement potential and significantly unveil USD 1.8 trillion economic opportunity. Besides, buildings are responsible for 37% of international carbon dioxide emissions, along with 34% of Earth’s species. Moreover, with increased urbanization, particularly across emerging economies, it is predicted to continue in the upcoming decades, thus fueling the market growth.

- Surge in consumer brand sustainability commitments: A fundamental transition in consumer goods branding is driving the need for supply chain aspects, which is driving the bio polyols market worldwide. Major consumer-facing companies, from furniture retailers, such as IKEA, to footwear manufacturers and mattress brands, have made public commitments to incorporating sustainable materials in their products. These commitments create contractual pull through the supply chain, as brand owners require their suppliers to provide materials with verified bio-content. Unlike regulatory drivers that establish minimum standards, brand commitments often create targets exceeding regulatory requirements, driving premium demand for higher-performance bio-polyols.

Challenges

- Higher production expenses and economies of scale: The economic reality of the production process of the bio polyol market remains a formidable barrier to widespread adoption. Despite the volatility of petroleum prices, bio-based polyols consistently command a price premium compared to conventional alternatives. This cost differential stems from multiple factors inherent to the production process. First, the extraction and refining of natural oils into suitable feedstocks for polyol synthesis involves multiple processing steps, including epoxidation, hydroxylation, and transesterification, that are often more complex and less energy-efficient than the simple alkoxylation processes used to manufacture conventional polyether polyols from propylene oxide. These additional steps require specialized equipment, higher energy inputs, and more intensive quality control, all of which contribute to elevated manufacturing costs.

- Greenwashing skepticism and certification complexity: An increasingly sophisticated challenge facing the bio polyols market is the growing skepticism surrounding sustainability claims and the complex, costly landscape of certification and verification. As consumers, regulators, and corporate procurement officers become more attuned to the nuances of sustainability, simple claims of bio-based content are no longer sufficient. End users are demanding comprehensive lifecycle assessments, proof of sustainable sourcing, verification of carbon footprint reductions, and assurances that bio-based products do not compete with food systems or contribute to deforestation. This heightened scrutiny creates a significant compliance burden for bio polyol manufacturers, who must navigate a patchwork of certification schemes, including USDA BioPreferred, Europe DIN CERTCO, ISCC Plus, and various forestry and palm oil sustainability certifications.

Bio Polyols Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.6% |

|

Base Year Market Size (2025) |

USD 6.8 billion |

|

Forecast Year Market Size (2035) |

USD 19.7 billion |

|

Regional Scope |

|

Bio Polyols Market Segmentation:

Type Segment Analysis

The polyether polyols sub-segment, which is part of the type segment, is anticipated to garner the largest share of 60.5% in the market by the end of 2035. The sub-segment’s upliftment is highly driven by the aspect of developing sustainable and high-performance bio polyols, which act as renewable alternatives to petroleum-specific counterparts. According to official statistics published by the EPA Government in December 2024, the U.S. EPA has estimated that the proposed amendments to the polyether polyols (PEPO), which exclude the ethylene oxide emission standard, constitute the capability of diminishing HAP emissions by roughly 157 tons every year. In addition, the proposed ethylene oxide emission standards are predicted to be lowered by an estimated 14 tons per year, thereby making it suitable for expanding the sub-segment’s exposure.

Application Segment Analysis

The rigid polyurethane (PU) foams segment in the bio polyols market is projected to hold the second-largest share during the forecast period. The segment’s growth is highly fueled by its importance in creating high-performance and sustainable thermal insulation with lowered environmental impact. As per an article published by NLM in March 2024, polyols readily achieved an overall renewable material content that is more than 74%, with a suberinic acid content of 37%. Besides, this particular foam comprises an apparent density of an estimated 40 to 44 kg/m3, along with almost 95% of closed cell content, more than 0.2 MPa compression strength, and roughly 0.019 W/(m·K) of thermal conductivity. Moreover, the bio-based rigid PUR foams consist of nearly 29% renewable materials, thus creating an optimistic outlook for the segment growth.

End user Segment Analysis

By the end of the stipulated timeline, the construction and insulation segment, part of the end user, is expected to account for the third-largest share in the market. The segment’s development is highly propelled by the global building industry's seismic shift toward sustainability and energy efficiency. This segment encompasses the use of bio-based polyurethane systems in rigid foam insulation, spray foam, sandwich panels, sealants, and construction adhesives applications, where polyurethanes have long dominated due to their superior thermal performance and versatility. The growth dynamics in this segment are fundamentally reshaping the construction materials landscape. Bio-based polyurethanes are increasingly specified in building envelopes to meet stringent energy codes and green building certifications such as Leadership in Energy and Environmental Design (LEED) and Building Research Establishment Environmental Assessment Method (BREEAM).

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Application |

|

|

End user |

|

|

Feedstock Source |

|

|

Manufacturing Process |

|

|

End use Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Bio Polyols Market - Regional Analysis

North America Market Insights

North America in the bio polyols market is anticipated to garner the highest share of 41.6% by the end of 2035. The market’s upliftment in the region is highly fueled by the presence of corporate sustainability commitments, technological leadership in advanced catalysts and bio-refining, and regulatory tailwinds at both state and federal levels. Based on government estimates published by the EIA in October 2025, the capacity additions for biofuel production, especially in the U.S., slowed as of 2024, with a modest increase in the production capacity by 3% between 2024 and 2025. Besides, renewable diesel and other biofuels production capacity also increased by only 391 million gallons every year as in 2024, which is less than 1/3rd of the growth witnessed in 2022 and 2023. Moreover, the Rodeo facility comprises a capacity of 767 million gallons per year, denoting a surge from 180 million gallons per year, thus boosting the market growth in the region.

The bio polyols market in the U.S. is growing significantly, owing to federal incentives, a supportive regulatory landscape, the dominance of construction and automotive industries, as well as corporate sustainability innovation and leadership. Based on government estimates published by the EPA in February 2026, there has been an increase in vehicle fuel economy by 0.1 mpg to a record high of 27.2 mpg as of 2024. In addition, the average new vehicle fuel economy has readily optimized 16 out of the previous 20 years and has upsurged by 41%. Besides, the National Highway Traffic Safety Administration’s Corporate Average Fuel Economy regulations offer suitable reforms for light-duty vehicles, with 34% of all new vehicles categorized as cars and 66% as trucks. Moreover, the technological share for large-scale manufacturers is making it suitable for bolstering the market growth and expansion in the overall country.

Technological Share for U.S.-Based Large-Scale Manufacturers (2024)

|

Automotive Segment/ Manufacturers |

Stellantis |

GM |

Ford |

Mercedes |

VW |

Mazda |

|

Turbo |

39% |

64% |

80% |

81% |

92% |

24% |

|

GDI |

39% |

91% |

58% |

89% |

92% |

100% |

|

GDPI |

0% |

- |

28% |

- |

0% |

- |

|

Cylinder Deactivation |

11% |

49% |

15% |

7% |

3% |

46% |

|

CVT |

2% |

8% |

8% |

- |

- |

- |

|

7+ Gears |

94% |

67% |

87% |

89% |

90% |

18% |

Source: EPA

The aspects of environmental policy, robust government strategies, rise in green consumerism, corporate responsibility, along with investment in advanced technology and manufacturing, are responsible for boosting the market in Canada. According to an article published by the Government of Canada in July 2025, the government in the country provided USD 600 million to support therapy clinical trials, which are led by the private industry and domestic biomanufacturing opportunities. Additionally, this investment opportunity has been part of the USD 1 billion Plan to Mobilize Science within the overall nation. Besides, USD 175.6 million has also been provided for supporting AbCellera, particularly in its antibody therapy research, along with the construction of an antibody production infrastructure, thus positively impacting the market growth.

APAC Market Insights

The Asia Pacific in the bio polyols market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by an increase in urbanization and industrialization, governmental sustainability mandates, feedstock abundance, and the presence of a manufacturing hub for worldwide markets. According to official statistics published by the IEA Organization in 2023, India generously imports 60% of its vegetable oils, which feedstock growth is based on utilized animal fats and cooking oils. Besides, to align biofuel production with the Net Zero Scenario, it is essential to enter new economies, enhance feedstock supplies, diminish greenhouse gas emissions intensity, and escalate technological deployment, thus making it suitable for the market development in the region.

The market in China is gaining increased traction, owing to the existence of a tactical emerging industry, channeling suitable funding through green manufacturing strategies, chemical technologies, and readily adopting sustainable process advancements. As stated in an article published by the State Council Information Office in November 2022, the industrial added value of enterprises in the country’s chemical industry rose by 3.9% year-on-year (YoY). In addition, the main business revenue of these firms also went up by 8.2% YoY to USD 14.1 trillion. Besides, the overall profit of these firms topped USD 904 billion, significantly edging down by 2.3% in comparison to the previous year. Therefore, based on all these developments in the domestic chemical industry, the market is gradually gaining increased importance.

The aspects of the largest castor oil production, different research strategies, chemical technologies, green chemical processes, and organizational contributions are readily responsible for bolstering the bio polyols market in India. Based on government estimates published by the PIB Government in December 2025, the National Mission on Edible Oils (NMEO) has aimed to provide 650,000 hectares under the oil palm cultivation between 2025 and 2026, and is also projected to denote an increase in the crude palm oil production to 2.8 million tons by the end of 2030. Besides, in November 2025, 250,000 hectares have been successfully covered, bringing the overall oil palm coverage to 620,000 hectares, while the crude palm oil production has also increased from 191,000 tons to 380,000 by the end of 2025, this propelling the market demand in the overall country.

Europe Market Insights

Europe market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by the pioneering role in the worldwide transition towards sustainable chemistry, the presence of a sophisticated regulatory framework, and ambitious climate targets. According to official statistics published by the ITA in January 2022, authorities in the region registered more than 21,000 substances under the regional registration, evaluation, authorization, and restriction of chemicals (REACH) system. Additionally, over 200 chemical substances have been readily classified as substances of very great concern for utilizing them in regional stringent circumstances. Besides, different substances have been significantly classified to initiate suitable communication with hazardous properties, thus driving the market expansion in the overall region.

The bio polyols market in Germany is gaining increased exposure, owing to the presence of a robust industrial base, unwavering commitment towards sustainability, the automotive industry, and light-weighting objectives. As per an article published by Green Carbon in March 2024, 373 million tons of plastic have been produced from raw materials in the country. Besides, the Plastics Europe industrial association estimated the production of plastics to account for 391 million tons, along with the OECD Global Plastics Outlook of the Organization of Economic Cooperation and Development, projected to be roughly 600 million tons of plastics to be produced by the end of 2060. Moreover, an estimated 60% of polymers, such as packaging materials and shopping bags, are significantly produced for single utilization, thus fueling the market demand.

The existence of robust government leadership in bioeconomy, national strategies prioritizing chemicals, and suitable transition towards renewable feedstocks are certain factors that are responsible for driving the market in France. According to a data report published by the IEA Bioenergy in 2024, renewables make up 12% of the overall energy supply in the country as of 2022. In addition, the renewable energy share in finalized energy consumption is 17.1%, with nearly 60% of renewable energy, of which 10% stems from final energy consumption, significantly derived from biomass. Besides, the bioenergy carriers' import reliance is less than 10% in the country. Meanwhile, the role of liquid biofuels is steadily growing to an average level of 7.5% of total transport energy consumption, which is suitable for uplifting the market development in the overall country.

Key Bio Polyols Market Players:

- BASF (Germany)

- DuPont (U.S.)

- Dow (U.S.)

- Huntsman Corporation (U.S.)

- Cargill, Incorporated (U.S.)

- Emery Oleochemicals (Malaysia/U.S.)

- Arkema (France)

- Stepan Company (U.S.)

- Croda International Plc (UK)

- Repsol (Spain)

- Mitsui Chemicals, Inc. (Japan)

- Itoh Oil Chemical Co., Ltd. (Japan)

- Jayant Agro-Organics Limited (India)

- Covestro AG (Germany)

- Oleon NV (Belgium)

- BioBased Technologies (U.S.)

- Vertellus (U.S.)

- Stahl Holdings B.V. (Netherlands)

- Polioles (Mexico)

- Daicel Corporation (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- BASF is a dominant force in the market, leveraging its extensive R&D capabilities to pioneer bio-based polyol solutions for polyurethanes used in construction and automotive applications. The company is actively expanding its production capacity for its bio-based polyol production in Germany to meet surging demand, particularly from European automotive manufacturers.

- DuPont is a major contender in the market, concentrating on developing high-performance, sustainable polyols derived from renewable feedstocks such as castor oil and soy. The company is investing heavily in R&D to improve production efficiency and broaden the application scope of its bio-based materials beyond traditional sectors.

- Dow is a key manufacturer of bio-based polyols, offering sustainable alternatives that cater to the growing demand for green chemistry in various industries. The company focuses on integrating bio-based products into its extensive polyurethane portfolio, serving applications from furniture and bedding to automotive interiors.

- Huntsman Corporation is a leading player in the polyols sector, particularly noted for its significant share in the aromatic polyester polyols market, where it holds a substantial market position. The company is strategically pivoting its polyurethanes division toward high-value applications in aerospace, power infrastructure, and automotive battery components to offset legacy market volatility.

- Cargill Incorporated leverages its strong position in bio-based raw materials to produce a range of green polyols, effectively competing by targeting specific applications such as flexible foams and coatings. The company is actively investing in R&D to scale up production and improve the cost-competitiveness of its bio-based offerings for a global customer base.

Here is a list of key players operating in the global market:

The global bio polyols market is characterized by a mix of established chemical multinationals and specialized oleochemical companies, creating a dynamic competitive landscape. BASF, Dow, and Huntsman lead as diversified chemical giants leveraging their extensive R&D capabilities and global distribution networks to integrate bio-based offerings into their existing polyurethane portfolios. Simultaneously, specialized players, such as Emery Oleochemicals in Malaysia, Cargill in the U.S., and Croda in the UK, differentiate themselves through deep expertise in renewable feedstocks and targeted innovation in bio-refining technologies. Besides, in May 2025, Huntsman introduced the newest intumescent polyurethane coating system that has been created for automotive applications. This tends to offer passive fire protection to metal and composite substrates utilized in electric vehicles without compromising design flexibility, thus making it suitable for boosting the bio polyols industry.

Corporate Landscape of the Bio Polyols Market:

Recent Developments

- In August 2025, Algenesis Labs declared the commissioning of the Bio-Iso pilot plant, wherein the company is focused on developing the world’s first-ever 100% biogenic carbon isocyanate that is made from plants, which is a disruptive advancement in polyurethane chemistry.

- In March 2025, BASF successfully expanded the production capacity of its Coatings division for polyurethane and polyester resin. This particular division constitutes a yearly capacity of 8,000 metric tons of polyurethane and polyester resin, which has further increased to 18,800 metric tons per year.

- In September 2022, Emery Oleochemicals proclaimed the newest website for its eco-friendly polyols product portfolio that provides an optimized online experience and expanded technical data.

- Report ID: 8421

- Published Date: Mar 09, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.