Battery Manufacturing Equipment Market Outlook:

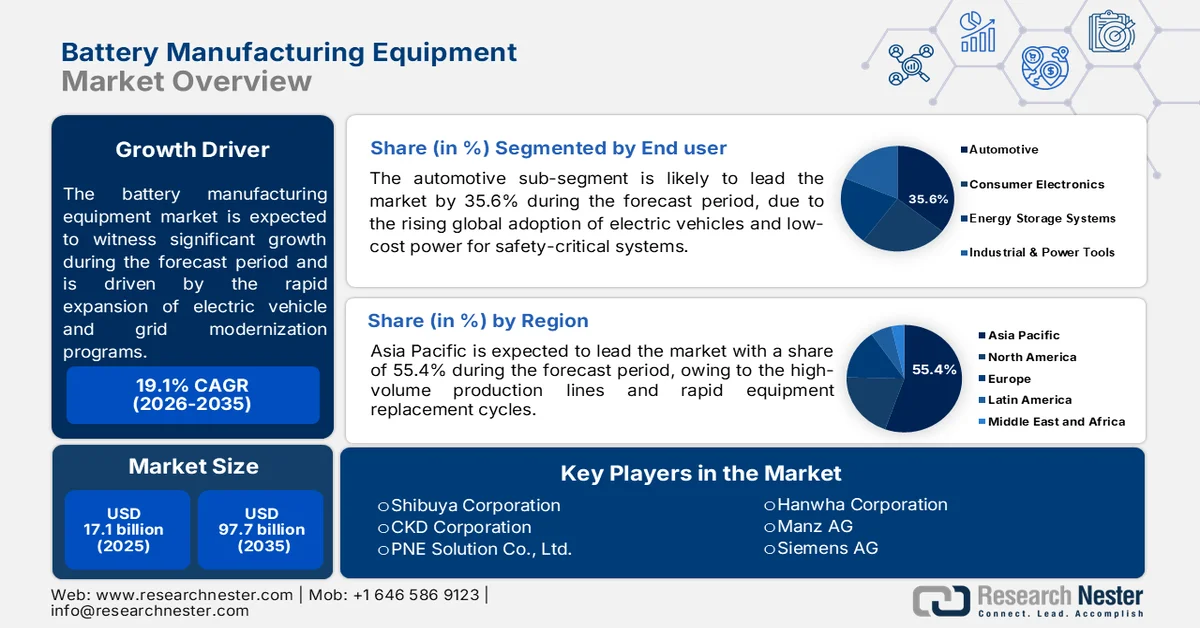

Battery Manufacturing Equipment Market size was valued at USD 17.1 billion in 2025 and is projected to reach USD 97.7 billion by the end of 2035, registering around 19.1% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of battery manufacturing equipment is estimated at USD 20.2 billion.

Battery manufacturing equipment market is driven by the rapid expansion of electric vehicle, stationary energy storage, and grid modernization programs across various regions. According to the International Energy Agency (IEA), April 2024 data, the global EV battery demand increased by about 40% in 2023, while announced battery manufacturing projects continue to expand production capacity well beyond current levels. This scale-up is increasing procurement of electrode coating systems, slurry mixing units, calendaring equipment, cell assembly lines, electrolyte filling systems, dry-room infrastructure, and formation and testing equipment. Public-sector funding is also strengthening capital expenditure pipelines for equipment suppliers. The U.S. Department of Energy (DOE) announced in February 2022 more than USD 3 billion in investments under the Bipartisan Infrastructure Law to support the domestic battery manufacturing and processing facilities, while the Loan Programs Office continues financing large-scale battery supply chain projects.

As battery plants move toward higher throughput and automation, manufacturers are prioritizing precision process control, yield optimization, and energy-efficient production systems to reduce operational costs and improve production consistency across giga-scale facilities. The battery manufacturing equipment market is also shaped by the supply chain diversification policies and stricter sustainability requirements from governments and energy agencies. The IEA February 2026 data estimates that China accounts for more than 80% of global battery cell production capacity, prompting the economies to increase domestic manufacturing incentives to reduce import dependency. This transition is creating sustained demand for advanced production equipment capable of supporting localized cell chemistries, including lithium iron phosphate (LFP) and nickel manganese cobalt (NMC) batteries.

Key Battery Manufacturing Equipment Market Insights Summary:

Regional Highlights:

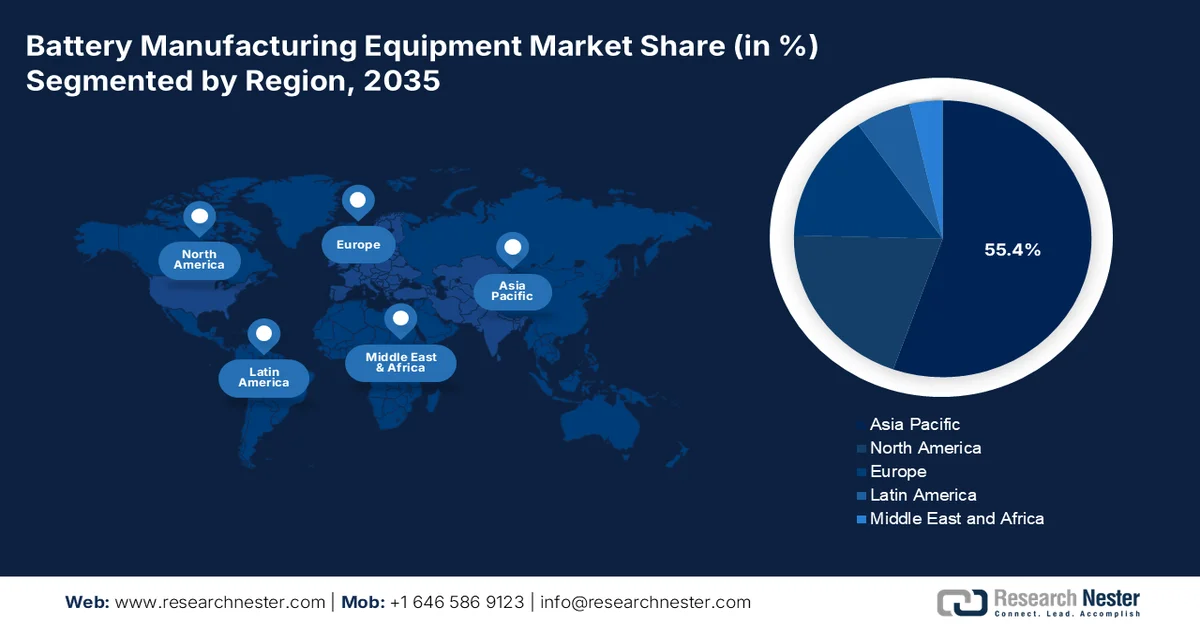

- Asia Pacific is anticipated to command 55.4% revenue share by 2035, impelled by high-volume gigafactory production and rapid equipment replacement cycles

- North America is likely to witness steady expansion in the battery manufacturing equipment market throughout 2026-2035 fueled by regional policy mandates and accelerated gigafactory construction timelines

Segment Insights:

- The automotive segment of the battery manufacturing equipment market is projected to capture 35.6% share by 2035, propelled by the global electric vehicle adoption

- Hardware is anticipated to retain a dominant position through 2035 owing to rising investments in gigafactory infrastructure and high demand for precision-driven production machinery

Key Growth Trends:

- Expansion of grid-scale energy storage projects

- Smart manufacturing adoption

Major Challenges:

- Technological complexity and precision requirements

- Supply chain disruptions

Key Players: Shibuya Corporation, CKD Corporation, PNE Solution Co., Ltd., Hanwha Corporation, Manz AG, Siemens AG, Mitsubishi Electric Corporation, Toray Engineering Co., Ltd., Dürr AG, Nordson Corporation, Applied Materials, Inc., Cognex Corporation, Ascent Solar Technologies, Inc., Intertek Group plc, Supernova Technologies Private Limited, Arrows Automation, Our Next Energy Inc., NEO Battery Materials Ltd, Kalmar, BOZHON.

Global Battery Manufacturing Equipment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 17.1 billion

- 2026 Market Size: USD 20.2 billion

- Projected Market Size: USD 97.7 billion by 2035

- Growth Forecasts: 19.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (55.4% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: China, United States, Germany, Japan, South Korea

- Emerging Countries: India, Indonesia, Vietnam, Mexico, Canada

Last updated on : 19 May, 2026

Battery Manufacturing Equipment Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of grid-scale energy storage projects: Growing deployment of renewable energy systems is increasing the demand for battery energy storage systems. This creates downstream requirements for the battery production equipment. According to the NLM March 2025 data, the global renewable power capacity reached more than 3,870 GW, requiring expanded storage infrastructure to manage grid reliability and intermittent power generation. Governments are investing heavily in the storage integration projects to support solar and wind deployment targets. Utility-scale storage projects require large-format lithium-ion batteries, increasing investment in battery cell and module manufacturing facilities. This trend is supporting the demand for electrode coating systems, laser welding tools, pack assembly equipment, and automated inspection technologies. Moreover, the energy storage modernization initiatives promote the domestic battery production capacity expansion.

- Smart manufacturing adoption: The expansion of smart manufacturing ecosystems is strengthening demand for advanced battery manufacturing equipment market by improving industrial automation capabilities, workforce readiness, and digital production infrastructure. As per the Ministry of Heavy Industries' November 2023 report over 9,800 individuals received Industry 4.0 awareness support nearly 800 professionals from 243 organizations were trained in smart manufacturing and digital transformation programs involving OEMs, PSUs, DRDO, start-ups, and academic institutions. IISc also developed 14 indigenous smart technologies across robotics, digital twins, inspection systems, additive manufacturing, and sustainability applications, with some already implemented in MSMEs. In addition, 5 industrial Industry 4.0 projects worth INR 3 crore are underway, while 16 projects worth INR 81 crore are under government review. These initiatives are supporting broader adoption of automation-intensive manufacturing systems applicable to high-volume battery production facilities.

Key Industry 4.0 and Smart Manufacturing Statistics

|

Organization / Initiative |

Statistical Data |

|

IISc Smart Factory – Industry 4.0 Awareness |

Over 9,800 individuals received awareness and training support in smart manufacturing and digital transformation |

|

IISc Smart Factory Training Programs |

Nearly 800 professionals and academics from 243 organizations trained |

|

IISc Research & Innovation Projects |

6 projects worth INR 5 crore completed with TCS, Yaskawa, Faurecia, and Toyota |

|

IISc Indigenous Technologies |

14 smart technologies developed in robotics, digital twin, additive manufacturing, inspection, and sustainability |

|

IISc Ongoing Industry 4.0 Projects |

5 industrial projects worth INR 3 crore underway |

|

IISc Projects Under Review |

16 projects worth INR 81 crore under review by DHI |

|

IISc Start-up Funding |

One Industry 4.0 start-up attracted INR 50 lakh in seed funding |

|

Siemens Virtual Prototyping Lab Donation |

Infrastructure support worth INR 45 lakh |

|

Siemens Fellowship Support |

3 MTech and 1 PhD fellowships funded worth INR 88 lakh |

|

STCI Advanced Computing Lab |

INR 30 lakh funded for smart factory training |

|

Siemens SmartX Hackathon Funding |

INR 60 lakh allocated for start-up mentoring and seed funding |

|

DST Hybrid Manufacturing Proposal |

INR 6.5 crore approved project |

|

IIT Delhi Robotics Demonstration at Robocon |

800–900 students from 50 colleges participated |

|

CMTI Awareness Initiatives |

4,050 participants attended Industry 4.0 awareness programs |

|

CMTI Internship Programs |

153 engineering students completed internships |

|

CMTI Executive Training Programs |

150 industry executives trained |

Source: Ministry of Heavy Industries' November 2023

Challenges

- Technological complexity and precision requirements: Battery manufacturing requires extreme precision across multiple stages, including electrode coating, stacking, electrolyte filling, and formation testing with minimal room for error. New entrants in the battery manufacturing equipment market lack the proprietary process knowledge that incumbents have developed over decades. The complexity intensifies as the industry shifts toward solid-state batteries, which demand entirely new equipment designs for dry electrode processing and lamination. Traditional manual intervention leads to inconsistencies, lower yields, and higher waste, directly impacting the product quality and profitability.

- Supply chain disruptions: The global trade tensions and the tariff policies are the key challenges in the battery manufacturing equipment market. Precision rollers and calendering equipment, essential for high-efficiency battery production, face import disruptions. These disruptions lead to higher setup costs, production delays, and uncertainty in the equipment pricing. Moreover, the fragmentation of the global supply chains forces new entrants to navigate the complex regulatory environments across the different regions while managing inventory risks and lead time uncertainties.

Battery Manufacturing Equipment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

19.1% |

|

Base Year Market Size (2025) |

USD 17.1 billion |

|

Forecast Year Market Size (2035) |

USD 97.7 billion |

|

Regional Scope |

|

Battery Manufacturing Equipment Market Segmentation:

End user Segment Analysis

Under the end user segment, the automotive is leading in the battery manufacturing equipment market and is poised to hold the share value of 35.6% by 2035. The segment is driven by the global electric vehicle adoption. As the world gradually transitions from internal combustion engines to EVs, lead batteries provide reliable, low-cost power for safety-critical systems such as lighting, door locks, infotainment, and emergency braking, even when the main lithium pack is discharged. Furthermore, lead batteries are the backbone of EV charging stations, acting as buffer storage to stabilize grid demand during peak charging events. According to the Battery Council 2026 data, 99% recycling rate of lead batteries, with the highest of any battery chemistry, lead batteries significantly boost the sustainability profile of EVs and lead-battery-supported charging stations. This circular economy advantage reduces the environmental footprint of EV ecosystems. Automotive OEMs and charging network operators continue to specify lead batteries alongside lithium systems, ensuring this legacy technology remains a relevant sub-segment driver through 2035.

Component Supplied Segment Analysis

The hardware is dominating the component segment in the battery manufacturing equipment market because it forms the physical backbone of any gigafactory. This includes robotic arms for electrode stacking, precision laser cutters for tab welding, dry room systems for moisture control, formation racks for cell activation, and conveyor networks for material handling. Battery manufacturers prioritize hardware investments because equipment uptime, throughput, speed, and mechanical precision directly determine production yield and cell quality. Furthermore, hardware components face wear and tear from continuous operation, necessitating periodic replacement and upgrades, which generate recurring revenue streams for suppliers. As gigafactories scale to multi-GWh capacities, the sheer volume of physical machinery required ensures hardware consistently captures nearly three-quarters of total component spending.

Automation Level Segment Analysis

Fully automated battery manufacturing equipment market dominates the automation segment because the sheer scale of capacity expansion requires minimal human intervention. According to the NETL February 2023 data, lithium-ion cell manufacturing capacity in U.S. was projected to grow from about 59 GWh in 2020 to 224 GWh by 2025, a 280% increase. Achieving this fourfold expansion within five years would be impossible with semi-automated or manual lines, which introduce variability and slower throughput. Fully automated systems enable 24/7 operation with defect rates directly supporting giga factory output targets. Moreover, the equipment suppliers are deploying robotic stacking, inline laser welding, and AI-driven vision inspection at unprecedented scale.

Our in-depth analysis of the battery manufacturing equipment market includes the following segments:

|

Segment |

Subsegments |

|

Equipment Type |

|

|

Battery Cell Format |

|

|

Automation Level |

|

|

Stage of Production |

|

|

End user |

|

|

Component Supplied |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Battery Manufacturing Equipment Market - Regional Analysis

APAC Market Insights

The Asia Pacific dominates the battery manufacturing equipment market and is expected to capture the regional revenue share of 55.4% by the end of 2035. The battery manufacturing equipment market is defined by high-volume production lines and rapid equipment replacement cycles. Equipment buyers in this region prioritize throughput speed and cost per unit over flexibility, given established cell chemistries and form factors. Fully automated assembly lines are standard, with suppliers offering turnkey integration from electrode mixing to formation. Competition among the equipment vendors is intense, compressing the margins but driving continuous innovation in the winding, stacking, and electrolyte filling speeds. Aftermarket services, including the spare parts retrofits and the predictive maintenance contracts, represent a significant revenue stream due to the installed base size. Moreover, the regional suppliers dominate, although local content policies in India and Indonesia are creating opportunities for domestic assembly of imported machinery.

The domestic advanced chemistry cell (ACC) production and electric mobility adoption are driving the battery manufacturing equipment market in India. According to the PIB March 2022 data, the government approved a Production Linked Incentive (PLI) scheme worth USD 2.17 billion to establish 50 GWh of ACC battery manufacturing capacity, increasing the demand for the coating cell assembly, electrolyte filling, and formation equipment. The IEA 2024 data reported that electric vehicle registrations in India surpassed 1.9 million units, reflecting a rising downstream battery demand. In addition, the PIB stated in July 2023 that India identified 5.9 million tons of inferred lithium resources in Jammu & Kashmir, strengthening long-term investment prospects for domestic battery manufacturing and processing infrastructure.

India ACC Battery Manufacturing Investments and Capacity Expansion

|

Category |

Statistical Data / Development |

|

ACC PLI Scheme Budget |

₹18,100 crore (approx. USD 2.17 billion) approved by Government of India |

|

Target Manufacturing Capacity |

50 GWh annual ACC battery manufacturing capacity planned |

|

Number of Selected Companies |

4 companies selected under ACC PLI scheme |

|

Companies Awarded Capacity |

Reliance New Energy Solar, Ola Electric, Hyundai Global Motors, Rajesh Exports |

|

Total Bids Submitted |

10 companies submitted bids under ACC Battery Storage Programme |

|

Technically Qualified Companies |

9 companies qualified after evaluation |

|

Ola Electric Capacity Allocation |

20 GWh awarded |

|

Hyundai Global Motors Capacity Allocation |

20 GWh awarded |

|

Rajesh Exports Capacity Allocation |

5 GWh awarded |

|

Reliance New Energy Capacity Allocation |

5 GWh awarded with 15 GWh waitlisted |

|

Manufacturing Timeline |

Facilities required to be operational within 2 years |

|

Incentive Disbursement Period |

Incentives provided over 5 years based on battery sales |

|

Expected Oil Import Savings |

₹2,00,000 crore to ₹2,50,000 crore projected savings |

|

Automotive PLI Scheme |

₹25,938 crore automotive PLI support |

|

FAME Scheme Support |

₹10,000 crore allocated under FAME program |

Source: PIB March 2022

The Japan battery manufacturing equipment market is expanding rapidly, and in 2025, the market size reached USD 862.20 million; in 2026, the market is estimated to reach USD 953.10 million. Moreover, the market is set to expand at a CAGR 17.8% during the forecast period. By 2035, the market is set to reach USD 5436.08 million. The nation is driven by the government-backed investments in storage batteries and EV supply chains. According to Japan's transition bonds February 2026 data, the nation approved support for battery production projects totaling more than USD 15.4 billion in private investment. IEA 2023 data also reported that the government allocated approximately USD 2.5 billion to strengthen domestic battery supply chains and storage capacity expansion. Additionally, the Japan Automobile Dealers Association stated that electrified vehicle sales, including hybrids and EVs, continued rising increasing demand for lithium-ion battery production infrastructure and automated manufacturing equipment across Japan’s industrial sector.

North America Market Insights

The North America is projected to expand steadily during the assessed period, 2026 to 2035. The battery manufacturing equipment market is driven by the regional policy mandates and gigafactory construction timelines. Equipment buyers prioritize suppliers capable of on-site commissioning, maintenance, and spare parts inventory. Formation and aging systems remain the most capital-intensive segment requiring specialized power electronics and thermal management integration. Fully automated assembly lines are the baseline requirement, as semi-automated solutions cannot achieve the uptime and defect rates demanded by the automotive customers. Suppliers in Canada and Mexico serve cross-border projects using USMCA trade provisions for local content qualification. Equipment lead times have extended significantly for specialized machinery such as laser welding stations and electrolyte filling systems. Further, the regional service networks have become a competitive differentiator.

The rapid domestic battery production growth supported by the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA) is expanding the battery manufacturing equipment market in the U.S. According to the CSIS April 2026 data, more than 180 battery component manufacturing facilities have been commissioned across 38 states, strengthening demand for electrode processing cell assembly formation and automation equipment. U.S. battery production increased by nearly 140%, reflecting large-scale investments in the domestic gigafactory infrastructure and supply chain localization. Battery sector employment also reached its highest level, with projections indicating up to 125,000 jobs by 2032. The expansion of downstream cell and module manufacturing capacity is increasing the procurement of advanced smart manufacturing systems, robotics, and integrated material handling equipment across the U.S. battery ecosystem.

The increasing federal investments in electric vehicle supply chains and critical mineral processing infrastructure are shaping the battery manufacturing equipment market in Canada. In July 2023, the Government of Canada announced up to USD 13 billion in support for the Volkswagen battery cell manufacturing facility in St. Thomas, Ontario, one of the country’s largest industrial investments linked to battery production expansion. The Government of Canada, in December 2022, also reported that the federal government committed nearly USD 3.8 billion under the Critical Minerals Strategy to strengthen domestic lithium, nickel, cobalt, and graphite supply chains. In addition, Statistics Canada stated that zero-emission vehicle registrations increased YoY, accelerating domestic battery demand and associated manufacturing equipment requirements for cell production, automation, and pack assembly operations.

Europe Market Insights

The battery manufacturing equipment market in Europe is expanding rapidly and is driven by the stringent environmental regulations. Equipment buyers prioritize energy efficiency, recyclability, and solvent-free processing capabilities to comply with the EU Battery Regulation. Formation and the aging systems must include the energy recovery features, and dry electrode processing equipment is gaining traction as manufacturers seek to reduce the use of toxic solvents. European buyers favor modular flexible lines capable of switching between cell chemistries and form factors without extended downtime. Cross-border projects require equipment suppliers to maintain service centers in multiple countries, favoring established players with regional footprints. Germany and Italy automation firms lead in precision stacking and laser welding. Partnerships with Fraunhofer, CEA, and other research institutes are common for pilot line development before the commercial scale-up.

The battery manufacturing equipment market in Germany is expanding due to the increasing investments in domestic battery cell production and the industrial decarbonization initiatives. In 2024, Germany’s Federal Ministry for Economic Affairs and Climate Action (BMWK) continued supporting European battery value chain projects under the Important Projects of Common European Interest (IPCEI), which mobilized billions of euros in battery-related industrial investments across Europe. The European Commission's May 2025 data reported that battery-electric vehicle registrations in Germany exceeded 45,535, a rise of 53.5% in April 2024, strengthening demand for localized battery production capacity. Additionally, EMBER May 2026 data stated that Germany hosts 25% of Europe’s total large-scale battery capacity, increasing requirements for the automated coating assembly, electrolyte filling, and formation equipment in domestic gigafactory operations.

Strong government support for the zero-emission vehicle adoption and the domestic battery production infrastructure is shaping the battery manufacturing equipment market in the UK. In January 2024, the UK government confirmed that 80% of new cars and 70% of new vans sold in Great Britain must be zero-emission by 2030, increasing to 100% by 2035 under the Zero Emission Vehicle mandate. The policy is supported by USD 2.66 billion in government investment for EV incentives and charging infrastructure expansion, as per the Global Ardour Recycling Limited, February 2026. Battery electric vehicles accounted for 16.5% of new UK car registrations in 2023, with over 314,000 units sold, increasing the demand for battery cell manufacturing capacity. Additionally, the government approved a USD 505 million grant for Tata Group’s battery gigafactory, supporting future investments in automated battery production equipment and assembly systems.

Key Battery Manufacturing Equipment Market Players:

- Shibuya Corporation (Japan)

- CKD Corporation (Japan)

- PNE Solution Co., Ltd. (South Korea)

- Hanwha Corporation (South Korea)

- Manz AG (Germany)

- Siemens AG (Germany)

- Mitsubishi Electric Corporation (Japan)

- Toray Engineering Co., Ltd. (Japan)

- Dürr AG (Germany)

- Nordson Corporation (U.S.)

- Applied Materials, Inc. (U.S.)

- Cognex Corporation (U.S.)

- Ascent Solar Technologies, Inc. (U.S.)

- Intertek Group plc (UK)

- Supernova Technologies Private Limited (India)

- Arrows Automation (India)

- Our Next Energy Inc. (U.S.)

- NEO Battery Materials Ltd (Canada)

- Kalmar (Finland)

- BOZHON (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Shibuya Corporation leverages its deep expertise in the battery manufacturing equipment market from the semiconductor and pharmaceutical automation sectors to deliver the high-precision filling, capping, and handling equipment for the lithium-ion battery assembly. The company has strategically focused on the modular cleanroom-compatible systems that enhance electrolyte filling accuracy and reduce contamination risks.

- CKD Corporation has established itself in the battery manufacturing equipment market via its advanced pneumatic control, fluid dispensing, and precision indexing systems used extensively in electrode stacking and cell packaging. The company adopts strategic initiatives such as developing servo-driven energy-efficient valve systems that reduce air consumption while maintaining micro-liter dispensing accuracy for electrolytes and sealants.

- PNE Solution Co., Ltd. specializes in formation and testing systems, the final, capital-intensive stage of battery production, where cells are electrically activated and sorted. The company has strategically advanced in the battery manufacturing equipment market and its multi-channel formation chargers and aging test chambers to handle high current densities for EV and energy storage system (ESS) batteries. In 2024, the company has made a total output of USD 373.4 million.

- Hanwha Corporation leverages its aerospace and defense automation heritage to compete in the battery manufacturing equipment market, primarily through its Hanwha Machinery division. The company focuses on the high-speed electrode notching, stacking, and tab welding equipment for the cylindrical and prismatic cells. Strategic initiatives include the development of laser patterning systems for dry electrode processing, reducing solvent use, and reducing drying energy.

- Manz AG is a key European innovator in the battery manufacturing equipment market, known for its laser cutting, winding, and assembly platforms for lithium-ion and solid-state batteries. The company has strategically shifted focus to equipment for the large format pouch cells and all solid-state batteries (ASSB), where its vacuum processing and roll-to-roll handling expertise are critical. In 2024, the company has made a revenue of USD 145.7 million.

Here is a list of key players operating in the global battery manufacturing equipment market:

The battery manufacturing equipment market is highly competitive and is characterized by a mix of established automation giants and specialized Asian leaders. China firms dominate large-scale production lines, while South Korea and Japan companies excel in high-precision winding, stacking, and assembly equipment. Europe and U.S. players focus on niche technologies such as dry electrode coating and laser structuring to support the next-generation batteries. Key strategic initiatives include the vertical integration partnerships with the gigafactory builders and heavy R&D investment in digitalization and energy-efficient dry rooms to lower production costs and carbon footprints. For example, in May 2025, Our Next Energy Inc. (ONE) announced a strategic partnership with Pomega Energy Storage Technologies

Corporate Landscape of the Battery Manufacturing Equipment Market:

Recent Developments

- In October 2025, NEO Battery Materials Ltd. announced the expansion of its site to establish battery cell manufacturing capabilities and scale up silicon battery material production and research operations. The company has announced an operational electrode manufacturing facility in South Korea with the buildings on 2.5 acres, with an additional 0.8 acres designated for future expansion.

- In July 2025, Kalmar unveiled its second-generation lithium-ion (Li-ion) battery solution for its range of electrically powered counterbalanced equipment, such as empty container handlers, reachstackers, and forklifts. The new battery system provides enhanced energy capacity, longer, more predictable performance curve, and improved thermal stability across a wide range of operating environments.

- In May 2025, BOZHON has announced the mass production line for lithium-ion batteries, which is a key energy carrier for electric vehicles and energy storage systems. By using its robust technical foundation and innovative capabilities, the company has launched a comprehensive production line solution tailored to deliver intelligent, high-efficiency, and flexible production systems.

- Report ID: 5355

- Published Date: May 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.