Automotive Pumps Market Outlook:

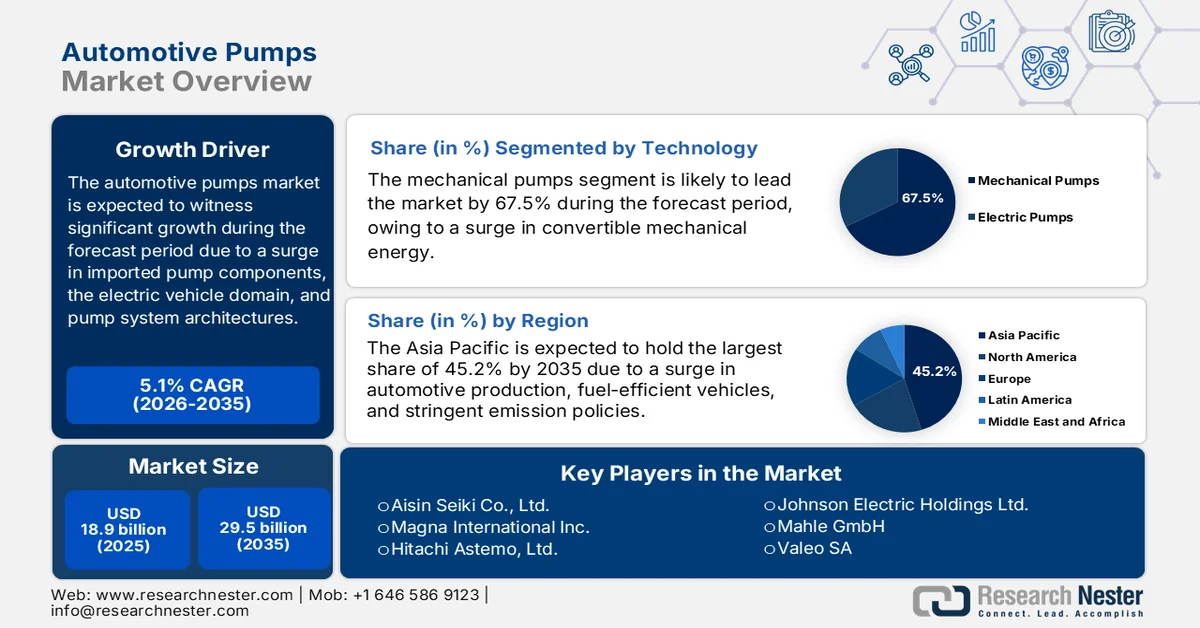

Automotive Pumps Market size was valued at USD 18.9 billion in 2025 and is projected to reach USD 29.5 billion by the end of 2035, growing at a 5.1% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of automotive pumps is evaluated at USD 19.8 billion.

The worldwide automotive pumps market is positively influenced by different foundational factors that create a wide-ranging operating landscape. These include trade policies, tariff adjustments, and cost pressures on imported pump components, such as electronic controllers, impellers, housings, and electric motors. According to official statistics published by the OEC in April 2026, the U.S. is considered the top exporter of pumps, with a valuation of USD 746 million as of 2024. Likewise, the country is also the greatest importer of pumps, worth USD 443 million in the same year. Besides, the global trade is valued at USD 4.6 billion, along with a global trade share of 0.02%, and 0.7 as product complexity. Moreover, the continuous supply dynamics of electric motors are also positively impacting the operation of pumps, thus bolstering the automotive pumps market exposure globally.

2024 Electric Motors Export and Import Analysis

|

Countries/Component |

Export (USD) |

Import (USD) |

|

China |

18 billion |

3.8 billion |

|

Germany |

8.4 billion |

7.5 billion |

|

U.S. |

5.1 billion |

13.4 billion |

|

Global Trade Valuation |

73.6 billion |

|

|

Global Trade Share |

0.3% |

|

|

Product Complexity |

0.9 |

|

|

Export Growth |

0.5% |

|

Source: OEC

Furthermore, the integration of smart pump controls with vehicle domain controllers, the aftermarket evolution toward diagnostic-based and remanufactured pump solutions, and the presence of modular and multi-circuit pump system architectures are certain trends that are responsible for fueling the automotive pumps market globally. As stated in an article published by Energy Strategy Reviews in July 2025, electric vehicle sales effectively reached 14.6 million units as of 2023, demonstrating a 35% growth in comparison to 2022. Besides, two-wheelers accounted for 13% of overall electric vehicle sales in the same year, with South Asia and India indicating significant growth. Simultaneously, there has been an increase in three-wheelers by 30%, with China and India significantly controlling 95% of the worldwide industrial share, thus proliferating the market demand and expansion.

Region-Wise Electric Vehicle Share, 2023

Source: Energy Strategy Reviews

Key Automotive Pumps Market Insights Summary:

Regional Highlights:

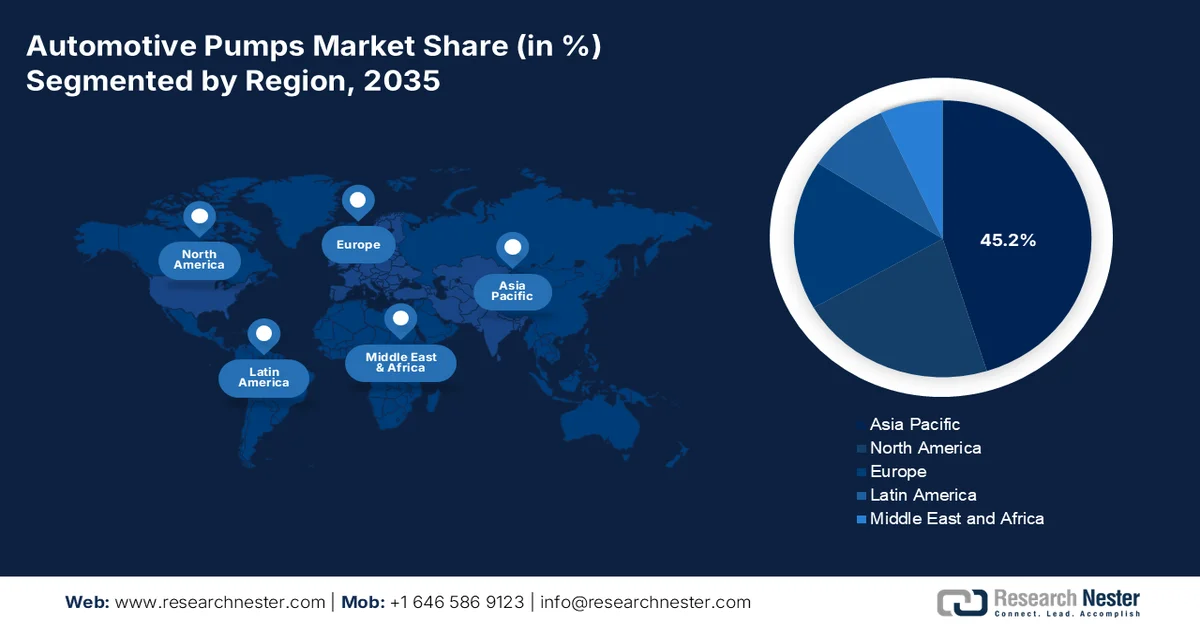

- Asia Pacific is projected to account for a 45.2% share by 2035, propelled by expanding automotive production, rising demand for fuel-efficient vehicles, stringent emission norms, rapid electrification, and advancements in hydrogen fuel cell pump technologies

- Europe automotive pumps market is set to witness the fastest growth during 2026-2035, impelled by stringent environmental regulations, increasing hybrid and electric vehicle adoption, and advancements in smart pump and thermal management technologies

Segment Insights:

- Mechanical pumps segment is anticipated to hold a dominant 67.5% share by 2035, driven by its critical function in efficiently transferring and compressing fluids through mechanical-to-hydraulic or pneumatic energy conversion

- Passenger cars segment in the automotive pumps market is expected to secure the second-largest share over 2026-2035, owing to the transition toward electrified mobility, demand for advanced thermal management systems, and increasing adoption of modular vehicle platforms

Key Growth Trends:

- Expansion in the emerging economy automotive industry

- Advancements in hydrocarbon emission control systems

Major Challenges:

- Intense price competition from low-cost regional manufacturers

- Standardization and compatibility issues across vehicle platforms

Key Players: Robert Bosch GmbH (Germany), Denso Corporation (Japan), Continental AG (Germany), ZF Friedrichshafen AG (Germany), Aisin Seiki Co., Ltd. (Japan), Magna International Inc. (Canada), Hitachi Astemo, Ltd. (Japan), Johnson Electric Holdings Ltd. (Hong Kong), Mahle GmbH (Germany), Valeo SA (France), Rheinmetall Automotive AG (Germany), SHW AG (Germany), Hanon Systems (South Korea), Nidec Corporation (Japan), Mikuni Corporation (Japan), Gates Corporation (U.S.), ACDelco (U.S.), Jung Woo Auto Co., Ltd. (South Korea), Daewha Fuel Pump Industries Ltd. (South Korea), Fuxin Dare Automotive Parts Co., Ltd. (China), ABC Technologies (Canada), TI Fluid Systems plc (UK), Alfa Laval (Sweden), ArianeGroup (France), Setco Automotive Limited (India).

Global Automotive Pumps Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 18.9 billion

- 2026 Market Size: USD 19.8 billion

- Projected Market Size: USD 29.5 billion by 2035

- Growth Forecasts: 5.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.2% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 30 April, 2026

Automotive Pumps Market - Growth Drivers and Challenges

Growth Drivers

- Expansion in the emerging economy automotive industry: The rapid enhancement of automotive industries across emerging nations serves as one of the fundamental growth drivers for the automotive pumps market globally. According to an article published by the Europe Research on Management and Business Economics in April 2024, the sales of electric vehicles surpassed 10 million units as of 2022, indicating a 3-fold surge within 2 years. In addition, more than 26 million electric cars were on the road in the same year, which was over 5-times the overall number in 2018. Besides, even though electric vehicles significantly account for just 2.1% of the worldwide vehicle stock, the electrification process has been robustly escalating, thus boosting the automotive pumps market growth and development.

- Advancements in hydrocarbon emission control systems: This particular advancement represents a significant growth opportunity for the automotive pumps market, which reflects the industry’s in-depth commitment to reducing environmental impact. As stated in an article published by the IEA Organization in 2025, the overall energy-based carbon dioxide emissions surged by 0.8% as of 2024, denoting an increase in the all-time high of 37.8 Gt carbon dioxide. This rise effectively contributed to a record atmospheric carbon dioxide concentration of 422.5 ppm in the same year, which is almost 3 ppm higher than 2023, and also 50% higher than pre-industrial levels. Besides, there has been a growth in carbon dioxide emissions from fuel combustion by almost 1% or 357 Mt carbon dioxide, thereby making it suitable for driving the market expansion.

- Extension of hydrogen fuel cell vehicle commercialization: The escalating commercialization of hydrogen fuel cell vehicles also serves as a strong growth driver for the automotive pumps market. As per an article published by the International Journal of Hydrogen Energy in June 2025, these particular vehicle types have the ability to diminish greenhouse gas emissions by 50% to 90% in comparison to internal combustion engine vehicles, with the reduction aspect relying on the hydrogen production pathway. Besides, these fuel cell systems demand a specialized array of pumps to effectively manage hydrogen recirculation, air compression, and coolant flow for stack thermal regulation, thus uplifting the market growth and development.

Challenges

- Intense price competition from low-cost regional manufacturers: The automotive pumps market faces persistent margin erosion from aggressive pricing strategies employed by manufacturers operating in low-cost production regions. These competitors benefit from substantially lower labor costs, reduced regulatory compliance expenses, and government subsidies that insulate them from global trade pressures. Established global brands like Bosch, Continental, and Denso must maintain rigorous quality standards, invest heavily in research and development, and comply with emissions and safety regulations across multiple jurisdictions, all of which add significant overhead, thus negatively impacting the market growth and expansion globally.

- Standardization and compatibility issues across vehicle platforms: Modernized vehicle manufacturers produce dozens of distinct models across multiple brands, each with unique thermal management requirements, packaging constraints, and electronic architectures. Therefore, suppliers in the automotive pumps market must engineer dozens of variant configurations rather than benefiting from mass production efficiencies offered by standardized components. A water pump designed for a compact electric city car cannot simply be scaled up for an electric sports utility vehicle without extensive redesign of mounting brackets, flow rates, control algorithms, and communication protocols. This lack of cross-platform compatibility forces suppliers to maintain sprawling product portfolios and complex inventory management systems, increasing operational costs.

Automotive Pumps Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.1% |

|

Base Year Market Size (2025) |

USD 18.9 billion |

|

Forecast Year Market Size (2035) |

USD 29.5 billion |

|

Regional Scope |

|

Automotive Pumps Market Segmentation:

Technology Segment Analysis

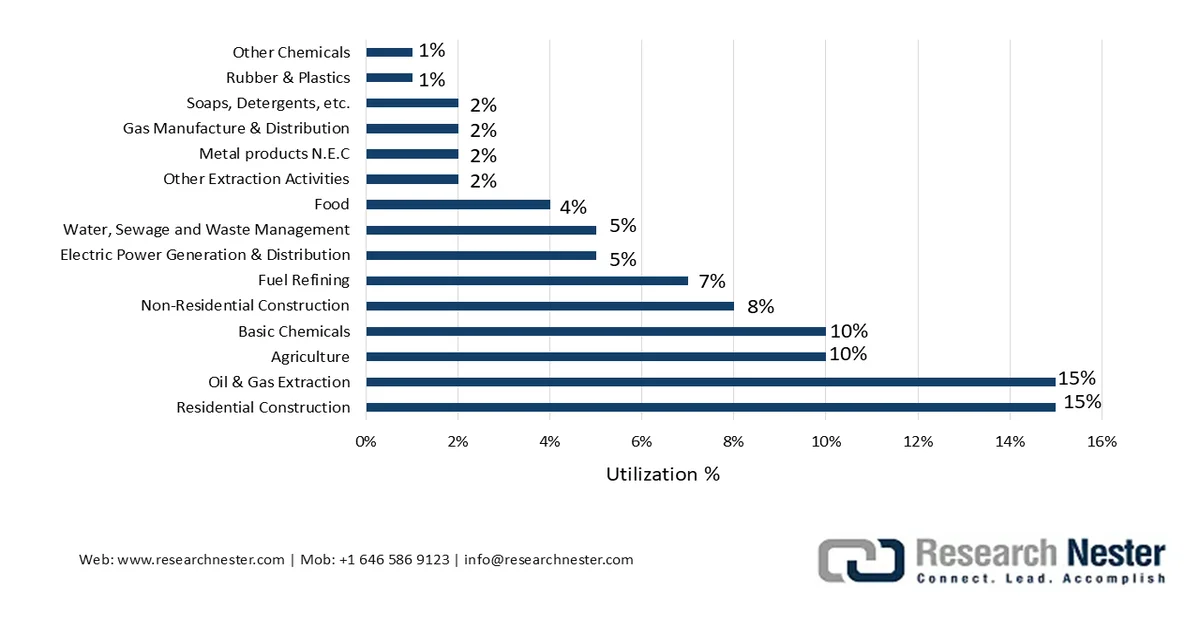

The mechanical pumps segment is anticipated to garner the highest share of 67.5% in the automotive pumps market by the end of 2035. The segment’s upliftment is primarily fueled by its role as a crucial device that moves, transfers, and compresses fluids, such as slurries, gases, and liquids, by effectively converting mechanical energy into pneumatic or hydraulic energy. According to official statistics published by the Pumps Organization in 2026, the pump industry in the U.S. is predicted to comprise more than 450 manufacturers of different sizes, significantly operating across 38 states. Besides, pump sales in the country are estimated at 10 billion annually, reflecting the use of motorized pumps across various industries. Moreover, the Hydraulic Institute in the nation represents more than 85% of domestic manufacturers and is deliberately leading Pump Manufacturers, Suppliers and System Integrators, thus driving the segment’s growth.

Motorized Pump Utilization Across Different Industries in the U.S., 2026

Source: Pumps Organization

Vehicle Type Segment Analysis

The passenger cars segment, part of the vehicle type, is projected to grab the second-highest share in the automotive pumps market during the forecast duration. The segment’s growth is highly driven by the shift toward electrified and shared mobility. This evolution opens new opportunities as electric powertrains create robust demand for advanced thermal management and coolant pumps, positioning suppliers to capture value in next-generation vehicle architectures. The move toward modular vehicle platforms encourages standardization, which simplifies manufacturing processes and reduces production costs, enabling pump manufacturers to achieve greater economies of scale. Besides, mobility-as-a-service and subscription models emphasize long-term durability, prompting automakers to seek higher-quality, longer-lasting pump solutions, thereby strengthening relationships between OEMs and tier-one suppliers.

Pump Type Segment Analysis

By the end of the stipulated timeline, the fuel injection pumps sub-segment, which is part of the pump type segment, is expected to account for the third-highest share in the automotive pumps market. The sub-segment’s development is highly propelled by its importance for optimizing emissions compliance, fuel efficiency, and performance. Besides, from an energy and power perspective, these pumps are critical for optimizing the conversion of chemical energy from fuel into mechanical motion. Their primary roadblock lies in the intensifying pressure to reduce engine-out emissions while maintaining power density. Moreover, modernized high-pressure common-rail systems demand extreme mechanical precision to atomize fuel effectively, yet this complexity increases parasitic load on the engine.

Our in-depth analysis of the automotive pumps market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Vehicle Type |

|

|

Pump type |

|

|

Sales Channel |

|

|

Displacement Type |

|

|

Application |

|

|

EV Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Pumps Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the automotive pumps market is anticipated to grab the largest share of 45.2% by the end of 2035. The market’s upliftment in the region is highly propelled by an expansion in the automotive production landscape, the growing preference for fuel-efficient vehicles, strict emission regulations enforced across countries, rapid electrification adoption, and the development of pumps for hydrogen fuel cells. According to official statistics published by the UNCTAD Organization in October 2024, China effectively manufactured 58% of global electric vehicles as of 2023, which cemented its position as the most dominant player in the overall industry. Besides, Thailand consumes almost 776,000 vehicles every year, especially light commercial vehicles, and has emerged as one of the major vehicle exporters, thus bolstering the automotive pumps market growth in the overall region.

Car Manufacturing in the Asia Pacific, 2023

|

Countries |

Number of Cars |

|

China |

30,160,966 |

|

Japan |

8,997,440 |

|

India |

5,851,507 |

|

Korea |

4,243,597 |

|

Thailand |

1,841,663 |

Source: UNCTAD Organization

The automotive pumps market in China is growing significantly, owing to the largest automotive producer, an expansion in the vehicle manufacturing capacity for creating substantial pump demand, a strong push to new energy vehicles, an upsurge in the fuel cell commercial vehicle production, and the government’s focus on hydrogen infrastructure development. As stated in an article published by the State Council Information Office in January 2026, there has been an expansion in domestic automobile production and sales by 34 million units. Additionally, the country’s overall output reached 34.5 million units, indicating a 10.4% in comparison to 2024. Besides, there has been a rise in sales by 9.4% year-on-year (YoY) to 34.4 million units, which is also responsible for driving the market in the overall country.

The aspects of a sure in automobile production and sales, the existence of supportive government initiatives, technological innovation in pump design, a rise in the demand for low-emission and fuel-efficient vehicles, extension of the automotive aftermarket, and transition to hybrid vehicle and electrification are a few trends for fueling the automotive pumps market in India. Based on government estimates published by the PIB in August 2025, the country registered 5.6 million electric vehicles in February 2025, which reflected the rapid adoption of clean mobility. Likewise, the country’s electric vehicle industry has already charged ahead between 2024 and 2025, with electric two-wheeler sales hit 1.4 million units. This demonstrated a 21% increase from the previous year’s 948,000 units, which increasingly accelerated the shift to sustainable and clean mobility on domestic roads.

Europe Market Insights

Europe in the automotive pumps market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly attributed to the presence of strict environmental regulations, a decisive transition toward hybrid and electric vehicles, innovative pump technologies, an escalation in electric water pump adoption for battery thermal management, and the incorporation of smart pump controls. According to official statistics published by the Heat Pumping Technologies in March 2026, there has been continuous growth in heat pump sales in the region, with an average surge of 10.3% across 16 nations, with an overall residential sales reaching 2.6 million units as of 2025. This particular growth is highly driven by the Warm Homes Plan and the Boiler Upgrade Scheme, both of which assisted in the sales jump by 27% to 125,000 units, thus denoting an optimistic outlook for the automotive pumps market.

Installed Heat Pumps Across Europe Yearly Stock Analysis, 2012-2025

|

Year |

Heat Pump Installation (In Units) |

|

2012 |

6.3 |

|

2013 |

7.1 |

|

2014 |

7.9 |

|

2015 |

8.8 |

|

2016 |

9.9 |

|

2017 |

11.0 |

|

2018 |

12.3 |

|

2019 |

13.9 |

|

2020 |

15.6 |

|

2021 |

17.8 |

|

2022 |

20.9 |

|

2023 |

23.8 |

|

2024 |

26.0 |

|

2025 |

28.2 |

Source: Heat Pumping Technologies

The automotive pumps market in Germany is gaining increased traction, owing to the largest vehicle producer, the increased concentration of original equipment manufacturers, focus on technological innovation capacity, and the strong electric vehicle adoption targets. As stated in an article published by the ITA in November 2024, the automotive industry is one of the largest industrial sectors, catering to nearly a quarter of overall industry revenues and supporting almost 780,000 employment opportunities. Additionally, the domestic auto industry significantly generated more than USD 611 billion in overall sales, demonstrating an 11% growth from 2022, which comprises USD 496.3 million motor vehicles, USD 15.7 million trailers, and USD 99.8 million for parts and accessories. Besides, automotive suppliers effectively account for 16.3% of the industry’s turnover, thus positively fueling the market development.

The regulatory framework, government legislations, the urgency for automakers to shift their product portfolios towards complete electrification, an increase in the demand for electric oil pumps, electric water pumps, and innovative thermal management solutions, and growth in the electric vehicle charging facility are responsible for fueling the automotive pumps market in the UK. As per an article published by the IIR Organization in March 2026, the heat pump sales in the country successfully reached the latest high of 125,037 units, indicating more than 27% increase as of 2025, in comparison to 2024. Based on this growth, there has been a rise in air-to-water monobloc systems by 26%, along with a surge in ground-and-water source heat pumps by 32.05, and domestic hot water heat pumps by 36%, thereby making it extremely suitable for fueling the market development.

Heat Pump Sales Analysis in the UK, 2019-2025

|

Year |

Sales |

Manufactured in the UK |

% UK Made |

|

2019 |

25,727 |

- |

- |

|

2020 |

29,226 |

- |

- |

|

2021 |

47,699 |

- |

- |

|

2022 |

61,061 |

16,968 |

27.8 |

|

2023 |

62,906 |

23,864 |

37.9 |

|

2024 |

98,345 |

32,920 |

33.5 |

|

2025 |

125,037 |

45,398 |

36.3 |

Source: IIR Organization

North America Market Insights

North America in the automotive pumps market is projected to experience considerable growth by the end of the stipulated duration. The market’s growth in the region is effectively driven by the strong demand for fuel delivery systems, innovative thermal management solutions, a well-established automotive manufacturing base, strict fuel economy, and an escalating shift to electrified powertrains. Based on government estimates published by the EIA in April 2026, in terms of on-highway diesel fuel prices ranged from USD 5.6 per gallon to USD 5.4 per gallon within April, demonstrating a rise by 1.4% from 2 years and 1.8% from a year ago in the U.S. Besides, as of January 2026, crude oil in the country accounted for 51% for regular gasoline and 41% for diesel. This was followed by 20% of refining for regular gasoline and 18% for diesel, thereby denoting a huge growth opportunity for the market exposure.

Regular Gasoline Pricing Impacting the Fuel Delivery System in the U.S., 2026

|

Timeline |

Pricing and Change % |

|

April 6 |

USD 4.1 per gallon |

|

April 13 |

USD 4.1 per gallon |

|

April 20 |

USD 4.0 per gallon |

|

2 years ago |

0.3% |

|

1 year ago |

0.9% |

Source: EIA

The automotive pumps market in the U.S. is gaining increased exposure, owing to strict emission and fuel economy regulations, growth in the electric vehicle penetration, the huge demand for vehicle parc supporting aftermarket, the shift to automated and electric pumps, and focus on consolidation and acquisition activities. As stated in an article published by the International Federation of Robotics in May 2025, automakers in the country have generously invested in automation, with overall installations of industrial robots in the car industry gradually increased by 10.7% and successfully reached 13,700 units as of 2024. Besides, the total automotive industry is readily considered the ultimate pillar of domestic robotic demand, along with increased exposure across metal and machinery, as well as electronics, plastic and chemical products, and food industries, thus driving the market growth.

Yearly Industrial Robotic Installation by U.S. Customer Industry, 2022-2024

|

Industry Type |

2022 (Units) |

2023 (Units) |

2024 (Units) |

|

Automotive |

14,657 |

12,421 |

13,747 |

|

Metal and Machinery |

3,859 |

4,171 |

3,765 |

|

Electrical/Electronics |

3,875 |

3,900 |

2,932 |

|

Plastic and Chemical Products |

3,040 |

2,972 |

2,727 |

|

Food |

2,403 |

1,860 |

2,277 |

Source: International Federation of Robotics

The increase in the need for fuel-efficient vehicles, strict emission regulations, the growth in the automotive manufacturing base, the robust electric vehicle adoption, suitable investments in automotive research and development, and cross-border supply chain integration are certain factors driving the automotive pumps market in Canada. As per an article published by the Government of Canada in August 2025, there has been an increase in zero-emission vehicles, such as battery-electric vehicles and plug-in hybrid electric vehicles, which reached 15% of overall new motor vehicle registrations as of 2024. In addition, there has also been an upsurge in total vehicle sales by 8% as of 2024 in comparison to 2023. Besides, zero-emission vehicles were deliberately responsible for 60% of the net increase in overall vehicle registrations in the country, which is positively impacting the market.

Key Automotive Pumps Market Players:

- Robert Bosch GmbH (Germany)

- Denso Corporation (Japan)

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Aisin Seiki Co., Ltd. (Japan)

- Magna International Inc. (Canada)

- Hitachi Astemo, Ltd. (Japan)

- Johnson Electric Holdings Ltd. (Hong Kong)

- Mahle GmbH (Germany)

- Valeo SA (France)

- Rheinmetall Automotive AG (Germany)

- SHW AG (Germany)

- Hanon Systems (South Korea)

- Nidec Corporation (Japan)

- Mikuni Corporation (Japan)

- Gates Corporation (U.S.)

- ACDelco (U.S.)

- Jung Woo Auto Co., Ltd. (South Korea)

- Daewha Fuel Pump Industries Ltd. (South Korea)

- Fuxin Dare Automotive Parts Co., Ltd. (China)

- ABC Technologies (Canada)

- TI Fluid Systems plc (UK)

- Alfa Laval (Sweden)

- ArianeGroup (France)

- Setco Automotive Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Robert Bosch GmbH leads the automotive pumps market with its comprehensive portfolio spanning fuel injection, electric water, and electric oil pumps for conventional and electrified vehicles. The company focuses heavily on developing high-efficiency pump solutions that support thermal management in battery electric and hybrid powertrains.

- Denso Corporation leverages its deep expertise in thermal systems to supply advanced electric water pumps and fuel pumps optimized for both internal combustion and electric vehicles. The Japanese giant prioritizes miniaturization and energy efficiency in its pump designs to meet evolving powertrain requirements.

- Continental AG delivers a wide range of automotive pumps, including fuel delivery modules, coolant pumps, and active oil management systems for passenger cars and commercial vehicles. The company emphasizes smart, electronically controlled pump technologies that reduce parasitic energy losses and improve overall vehicle efficiency.

- ZF Friedrichshafen AG integrates pump solutions primarily within its transmission and driveline systems, focusing on electric oil pumps for automated transmissions and hybrid drivetrains. The company's pump strategy aligns closely with its broader commitment to emissions reduction and electrification across vehicle platforms.

- Aisin Seiki Co., Ltd. manufactures mechanical and electric water pumps, oil pumps, and fuel pumps, supplying a significant portion of its output to affiliated Toyota Group vehicle manufacturers. The company actively develops next-generation electric pump technologies to support hybrid, plug-in hybrid, and battery electric vehicle architectures.

Here is a list of key players operating in the global automotive pumps market:

The global automotive pumps market is highly competitive, characterized by the presence of established Tier-1 suppliers and specialized regional manufacturers. Leading players such as Robert Bosch GmbH, Denso Corporation, and Continental AG dominate through extensive R&D capabilities and global production networks. Moreover, strategic initiatives across the industry focus on electrification and thermal management solutions for hybrid and battery electric vehicles. Key players are investing heavily in electric oil pumps and electric water pumps to align with the shift away from internal combustion engines. Besides, in April 2025, ABC Technologies completely acquired TI Fluid Systems plc for an enterprise valuation of more than USD 2.4 billion. The purpose was to rebrand TI Automotive based on its distinguished heritage that reflects the shared focus on customer services, people, and outstanding engineering, thus fueling the automotive pumps industry.

Corporate Landscape of the Automotive Pumps Market:

Recent Developments

- In January 2026, Alfa Laval and ArianeGroup initiated the signature of a co-development agreement for a liquid hydrogen trailer pump, followed by the Memorandum of Understanding as of December 2024.

- In June 2025, Setco Automotive Limited launched its newest advanced product, which is known as the automotive water pump, marking a tactical extension of the organization’s product portfolio into the critical engine cooling industry, and further reinforcing its commitment to reliability, efficient, and innovative engineering.

- In June 2024, Bosch expanded its portfolio to include the powerful PDE coolant pump, which is suitable for cooling electronic components, electric motors, e-axles, batteries, along with different eating applications, including auxiliary and interior heating.

- Report ID: 8542

- Published Date: Apr 30, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.