Automotive Air Fuel Module Market Outlook:

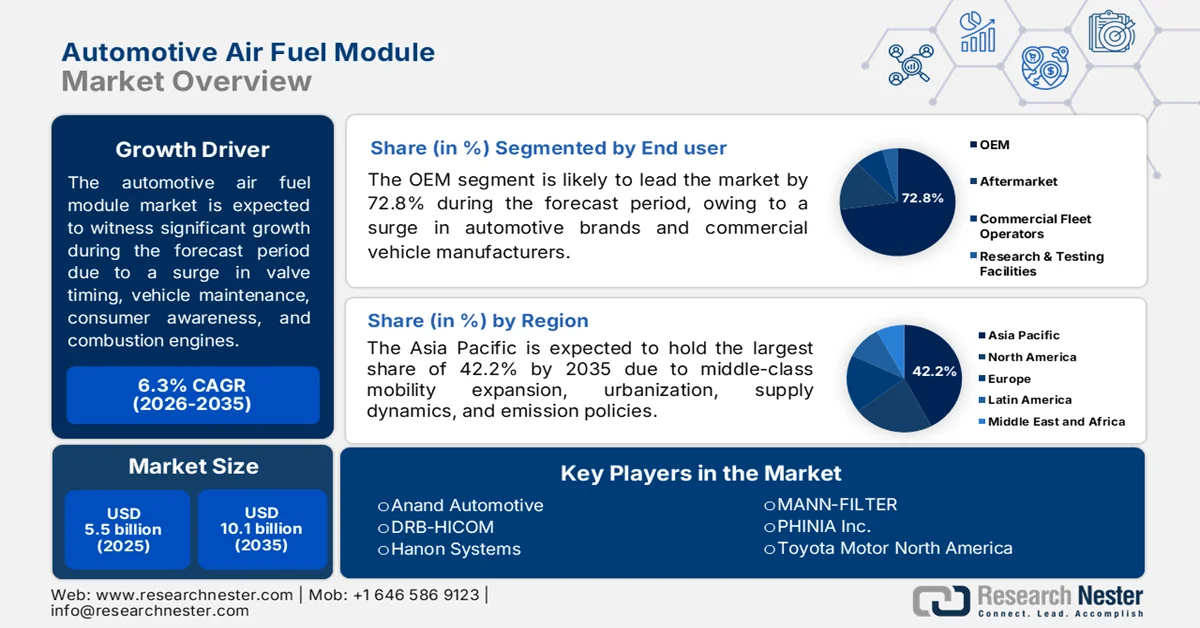

Automotive Air Fuel Module Market size was over USD 5.5 billion in 2025 and is projected to cross USD 10.1 billion by the end of 2035, growing at more than 6.3% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of automotive air fuel module is assessed at USD 5.8 billion.

The worldwide automotive air fuel module market is gradually shaping owing to an increase in the adoption of variable valve timing, turbocharging technologies, the demand for internal combustion engines, consumer awareness regarding vehicle maintenance, and a surge in fuel economy. According to official statistics published by the Engine Technology Forum Organization in July 2024, internal combustion engines are in huge demand across different economies. The demand is further expected to grow at an annual rate of 9% by 2030. In addition, this technology is poised to power 1/3rd of the latest vehicle fleet by 2032, emerging as the ultimate power source for 75% of large commercial vehicles, as per the projections. Moreover, combustion engines are highly utilized in heavy-duty off-road applications, in rail, marine, and power generation, thereby enhancing their supply dynamics globally.

2024 Combustion Engines Global Export and Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

U.S. |

8.6 billion |

6.2 billion |

|

Germany |

5.7 billion |

3.6 billion |

|

UK |

4.1 billion |

- |

|

Mexico |

- |

5.3 billion |

|

Global Trade Valuation |

47.4 billion |

|

|

Global Trade Share |

0.2% |

|

|

Product Complexity |

1.1 |

|

Source: OEC

Furthermore, the integration of predictive calibration algorithms, modular platform architecture across engine families, and embedded diagnostics with cloud connectivity are a few trends responsible for driving the automotive air fuel module market globally. Rising consumer demand is a key factor boosting the surge in the incorporation of artificial intelligence (AI) in automobiles. According to an article published by the TechRxiv Organization in July 2025, 77% of consumers are actively adopting AI-based features, including predictive maintenance services and personalized in-car experiences. Moreover, 52% are willing to pay an additional USD 5,000 for implementing these AI functionalities in their vehicles, thereby denoting a massive opportunity for expansion of the market across different regions.

Key Automotive Air Fuel Module Market Insights Summary:

Regional Highlights:

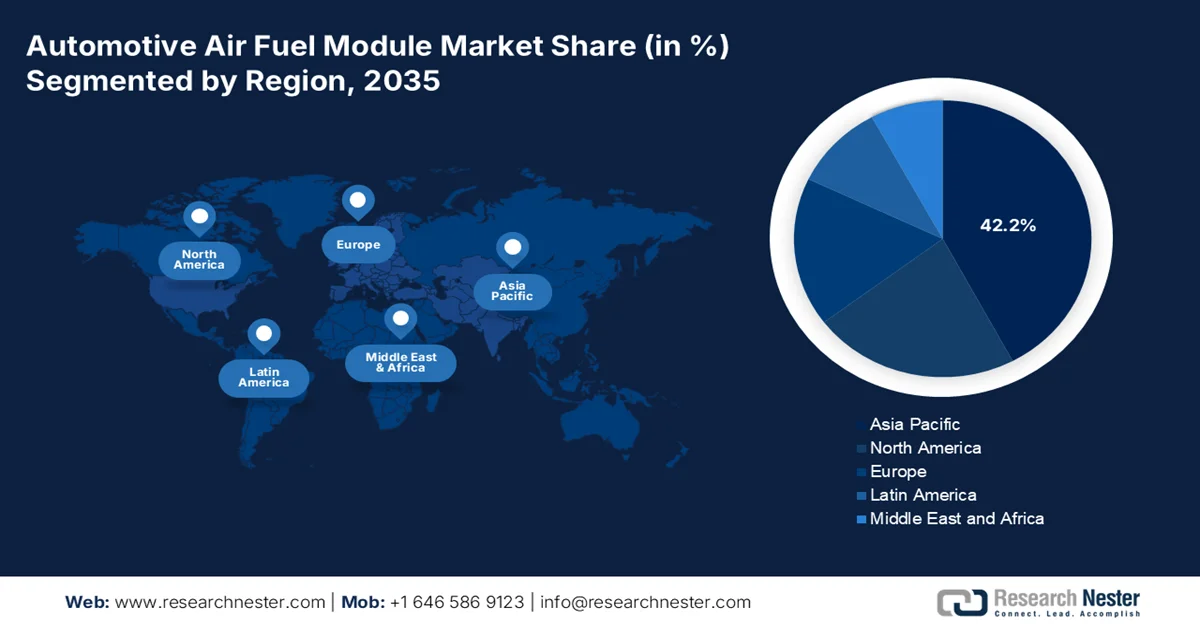

- The asia pacific region is projected to dominate the automotive air fuel module market with a 42.2% share by 2035, driven by expanding vehicle ownership, rapid urbanization, rising middle-class mobility, and stringent localized emission regulations

- Europe is anticipated to witness the fastest growth in the market throughout 2026–2035, impelled by stringent emission standards, increasing adoption of oxygen sensors, and growing collaboration between automakers and Tier-1 suppliers

Segment Insights:

- The OEM sub-segment is expected to capture a 72.8% share of the automotive air fuel module market by 2035, propelled by the integration of air fuel modules across high-volume vehicle production lines by leading global automakers and commercial vehicle manufacturers

- By 2035, the passenger cars sub-segment is poised to secure the second-largest share in the market, stimulated by rising global passenger vehicle ownership and the increasing reliance on personal mobility solutions

Key Growth Trends:

- Increase in hybrid electric vehicle models

- Expansion in ethanol-based industries

Major Challenges:

- Rising complexity of hybrid powertrains

- tringent and divergent emission regulations

Key Players: Bosch, Continental AG, Mahle, MANN+HUMMEL, Roechling, Valeo, HUTCHINSON, Magneti Marelli, Sogefi, Denso Corporation, Aisan Industry, Keihin, Hitachi Automotive Systems, Mikuni, Delphi Technologies, Donaldson Company, Visteon Corporation, Hyundai Kefico, Anand Automotive, DRB-HICOM, Hanon Systems, MANN-FILTER, PHINIA Inc., Toyota Motor North America, Rehlko.

Global Automotive Air Fuel Module Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.5 billion

- 2026 Market Size: USD 5.8 billion

- Projected Market Size: USD 10.1 billion by 2035

- Growth Forecasts: 6.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.2% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 26 May, 2026

Automotive Air Fuel Module Market - Growth Drivers and Challenges

Growth Drivers

- Increase in hybrid electric vehicle models: The rapid extension of these vehicles has readily created a distinctive growth driver for the automotive air fuel module market globally. According to official statistics published by the EIA Government in February 2026, almost 22% of light-duty vehicle models sold as of 2025, majorly in the U.S., were battery electric, hybrid, or plug-in hybrid vehicles, demonstrating an increase from 20% in 2024. Besides, the battery electric vehicle industry share reached a new high, accounting for 12% of overall light-duty vehicle purchases in September. Likewise, luxury vehicles catered to 14% of light-duty vehicles, along with the luxury sector, resulting in 23% of sales. Therefore, with this continuous growth in the hybrid vehicles category, the automotive air fuel module market is expanding uninterruptedly.

- Expansion in ethanol-based industries: Economies, such as Thailand, India, and Brazil, have generously incentivized the utilization of ethanol-based gasoline, based on which the automotive air fuel module market is gaining increased exposure. As stated in an article published by the USDA Government in June 2023, almost 37% of U.S.-based corn production went into producing ethanol, which is directly blended with motor gasoline across major economies. Besides, the expanded fuel ethanol consumption grew from 10.7 million to 5.3 billion gallons in the U.S., along with a recovery in Canada and Europe Union, with exceeded consumption. Moreover, the comprehensive availability of such a fuel has enforced vehicle manufacturers in developing recalibrated control logic, alcohol-compatible diaphragms, and corrosion-resistant seals.

Challenges

- Rising complexity of hybrid powertrains: The aspect of complete electrification readily threatens the conventional automotive air fuel module market, while hybrid vehicles experience a different challenge. These vehicles demand suitable air fuel modules, which operate seamlessly across both electric-based modes and engine-specific modes, requiring increased variable operating temperatures, precise fuel delivery, and frequent start and stop cycles under modified conditions. Besides, engineering a module that effectively maintains emission compliance, durability, and reliability across diversified duty cycles is extremely complex. As a result, this increases testing requirements, the risk of field failures, and development time. Moreover, small-scale suppliers without in-depth research and development resources struggle to meet specifications, thus limiting the market growth.

- Stringent and divergent emission regulations: The automotive air fuel module market needs to comply with a network of worldwide emission standards, including Europe 7, China 7, and EPA Tier 4. Each of these regulatory bodies enforces various evaluation protocols, restrictions, and compliance deadlines. Therefore, designing a single module that satisfies different economies requires expensive calibration work and redundant validation. Furthermore, regulations are becoming stringent on particulate matter from direct injection engines and cold-start emissions. Hence, keeping pace with this regulatory drift pressure ongoing engineering investment without corresponding volume growth, squeezing profitability. Meanwhile, small-scale players without global regulatory expertise face difficulty, thereby causing a hindrance to the automotive air fuel module market.

Automotive Air Fuel Module Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.3% |

|

Base Year Market Size (2025) |

USD 5.5 billion |

|

Forecast Year Market Size (2035) |

USD 10.1 billion |

|

Regional Scope |

|

Automotive Air Fuel Module Market Segmentation:

End user Segment Analysis

Based on the end user segment, the OEM sub-segment is anticipated to garner the largest share of 72.8% in the automotive air fuel module market by the end of 2035. This growth is primarily attributed to the presence of global automotive brands such as Toyota, Volkswagen, Ford, General Motors, Hyundai, Stellantis, and BMW, as well as commercial vehicle manufacturers, including Daimler Truck and Volvo. These organizations tend to integrate air fuel modules directly into new vehicles, particularly during assembly on production lines. Moreover, the dominance of the sub-segment originates from volume and compliance requirements. Meanwhile, each new internal combustion engine or hybrid vehicle manufactured requires a precisely calibrated air fuel module, thereby denoting a huge growth opportunity for the market globally.

Vehicle Type Segment Analysis

During the forecast period, the passenger cars sub-segment in vehicle type is projected to register the second-largest share in the automotive air fuel module market. The sub-segment’s growth is effectively driven by its role as the ultimate backbone of modernized personal mobility, freedom and economic empowerment, and offering unparalleled flexibility. According to official statistics published by the Center for Sustainable Systems in 2026, light trucks and automobiles remained the dominant mode of travel, especially in the U.S., significantly accounting for 86% of passenger miles traveled in 2023. Moreover, despite housing over 4% of the total global population, the represents nearly 11% of global car ownership. Comparatively, Russia owns 5%, followed by 4% in Germany, 6% in Japan, and 20% in China, reflecting the steadily rising demand for passenger cars worldwide.

Fuel Type Segment Analysis

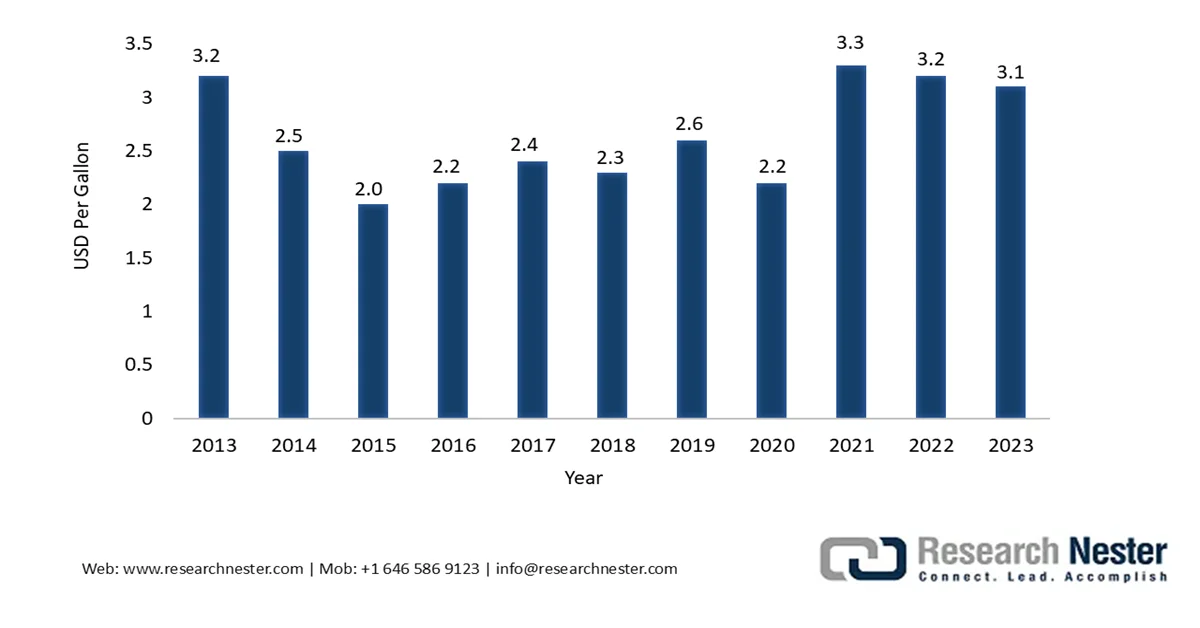

The gasoline segment in fuel type is expected to account for the third-largest share in the automotive air fuel module market by the end of the stipulated duration. The segment’s development is highly propelled by its necessity as an energy-dense liquid, which is utilized to power spark-based internal combustion engines. As stated in an article published by the EIA Government in September 2024, the monthly consumption of gasoline in the U.S. in terms of demand ranged from 358 million gallons per day in January 2023 to 375 million gallons per day in December 2023. Simultaneously, the gasoline price also fluctuated within this duration from USD .6 per gallon to USD 2.7 per gallon. Meanwhile, the fluctuation of regular-grade gasoline in the country is also impacting the segment’s growth, which in turn is boosting the market demand globally.

Source: EIA Government

Our in-depth analysis of the automotive air fuel module market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Vehicle Type |

|

|

Fuel Type |

|

|

Module Type |

|

|

Functionality |

|

|

Technology Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Air Fuel Module Market - Regional Analysis

APAC Market Insights

The Asia Pacific automotive air fuel module market is anticipated to grab the highest share of 42.2% by the end of 2035. The regional market’s growth is primarily driven by an increase in vehicle ownership, rapid urbanization, an expansion in the middle-class mobility, strict localized emission enforcement, domestic supply ecosystems, and competitive pricing for airflow components. For instance, as per the June 2025 CEEW Organization data report, the overall number of vehicles in India reached 226 million in 2023 and 494 million by the end of 2050. Based on this projection, two-wheelers are projected to dominate the country’s vehicle stock, with 350 million units by 2050, which is more than 175 million as of 2023. Likewise, private cars are also anticipated to surge by more than 2.7 times from 32 million to 90 million units in 2050, thereby proliferating the market growth in the region.

The automotive air fuel module market is growing significantly in China, owing to the largest automotive manufacturing facility, government approaches, the adoption of wide-ranging sensors, a robust push towards electric vehicles, and the rapid localization of suppliers. As stated in an article published by the State Council Information Office in January 2026, the country’s automotive sales and production witnessed an increase of 34 million units in 2025. Furthermore, the overall automotive output effectively reached 34.5 million units, demonstrating a 10.4% from 2024, while sales upsurged by 9.4% year-on-year (YoY) to 34.4 million units. In addition, an escalation in the newest energy vehicles has been noted, with sales and production totaling 16.4 million and 16.6 million units, making it suitable for effectively driving the market’s expansion in the country.

The aspects of expanding alternative fuel facilities, robust domestic automotive production, technological innovations in sensors, the growing demand for fuel-efficient vehicles, strict government standards, and an increase in hybrid electric vehicles are certain factors that are responsible for bolstering the automotive air fuel module market in Japan. The country’s market growth accounted for USD 1.3 billion in 2025, which is projected to reach USD 1.4 billion by 2026, and eventually expand up to 2.2 billion by the end of 2035. Based on government estimates published by the ITA in June 2023, the collaboration between the Japan Mini Vehicles Association and the Japan Automobile Dealers Association (JADA), 58,813 battery electric vehicles were sold in the country as of 2022, indicating a 2.7 times rise from 2021. In addition, this particular vehicle ratio surged to 1.7% and surpassed the 1% threshold, thus driving the automotive air fuel module market growth in the country.

Europe Market Insights

Europe in the automotive air fuel module market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is propelled by precise air and fuel ratios, stringent emission standards, the production of combustion engines, the adoption of oxygen sensors, and suitable collaborations between automotive manufacturers and Tier-1 suppliers. According to official statistics published by the European Union Aviation Safety Agency in 2026, in terms of sustainable aviation fuels, the ReFuelEU Aviation Regulation has successfully set a supply policy, which commenced with 2% as of 2025, and is further projected to increase to 70% by the end of 2050. Moreover, a sub-mandate for synthetic electric fuels is projected to start at 0.7% by 2030 and further surge to 35% by the end of 2050, thereby creating a huge growth opportunity for the automotive air fuel module market in the region.

The automotive air fuel module market is gaining increased traction in France, owing to the increased emphasis on hybrid vehicles, the demand for air fuel modules for start-stop operations, focus on premium electric vehicles, generous investment in hybrid powertrains, strong manufacturing industry, and different research programs. As stated in an article published by the Institute for Climate Economics in December 2025, as of 2023, domestic car manufacturers readily produced 23% of their respective light vehicles, in comparison to 53% in past years. The purpose of this production was to continuously remain competitive in the low-cost small-scale vehicle industry, along with offshoring a massive part of domestic production. Therefore, with such initiative, the market is gradually expanding and developing in the overall country.

The notable destination for automotive manufacturing investment, vehicle ownership rate, a rise in income and vehicle penetration, suitable modernization in the manufacturing sector, funding opportunities in precision component manufacturing, and government-based tax incentives are a few trends that are fueling the automotive air fuel module market in Poland. As per an article published by the Europe Commission in February 2026, battery electric vehicles (BEVs) accounted for 6.7% of new passenger car registrations as of 2025, while plug-in hybrid electric vehicles (PHEVs) constituted for 5.3% registrations. Additionally, a total of 28,143 PHEVs and 37,917 BHEVs were significantly registered throughout the same year, indicating an upsurge by 102% for BEVs and 88% for PHEVs, in comparison to 2024, thereby positively driving the market development.

North America Market Insights

The automotive air fuel module market in North America is projected to witness suitable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively attributed to sustained vehicle production, strict emission regulations, the implementation of hybrid electric vehicles, and the adoption of oxygen sensors for providing measurement accuracy. According to official statistics published by the U.S. International Trade Commission in February 2024, Michigan readily accounts for 19.0% of vehicle production in the region, followed by 42.2% in Upper Midwest states. Besides, vehicle manufacturing in the region is solely based onthe U.S.production of internationally owned manufacturers. In this regard, Alabama comprises the largest share of 22.9%, which is followed by Ohio, Kentucky, and Indiana, thus elevating the market exposure in the overall region.

Vehicle Production Levels and Shares Analysis in the U.S., 2022

|

States |

Vehicle Number |

Vehicle Production Share (%) |

Transplant Production Share (%) |

|

Michigan |

1,465,854 |

19.3 |

- |

|

Indiana |

866,775 |

11.8 |

20.4 |

|

Kentucky |

880,854 |

11.6 |

12.6 |

|

Alabama |

731,662 |

9.9 |

22.9 |

|

Ohio |

655,866 |

8.6 |

10.0 |

|

Texas |

388,817 |

5.1 |

0.2 |

|

California |

456,100 |

6.0 |

- |

|

Tennessee |

374,515 |

4.9 |

8.3 |

|

South Carolina |

267,846 |

3.5 |

8.2 |

|

Missouri |

445,498 |

5.9 |

- |

Source: U.S. International Trade Commission

The automotive air fuel module market is gaining increased exposure in the U.S., owing to the presence of strict Tier 3 and ongoing Tier 4 emission standards, an increase in SUV and pickup truck production volumes, the demand for aftermarket replacement from aging vehicle parc, as well as supply chain localization and domestic manufacturing consolidation. As stated in an article published by the Congress Government in March 2026, the automotive manufacturing industry in the country significantly accounts for 4.8% of gross domestic product (GDP), and also employs 10.1 million people through both direct and indirect employment opportunities. Besides, international automotive manufacturers generously invested USD 124 billion in domestic operations as of 2025 and successfully produced 4.9 million vehicles in 2024, thereby boosting the market demand.

U.S. Automotive Industry Share by Vehicle Sales (%), 2019-2024

|

Brand |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

|

Stellantis |

12.7 |

12.3 |

11.6 |

10.9 |

9.6 |

8.0 |

|

GM |

16.5 |

17.1 |

14.4 |

16.0 |

16.2 |

16.6 |

|

Ford |

13.8 |

13.7 |

12.4 |

13.1 |

12.5 |

12.7 |

|

BMW |

2.1 |

2.1 |

2.4 |

2.5 |

2.5 |

2.4 |

|

Honda |

9.2 |

9.1 |

9.5 |

6.9 |

8.2 |

8.7 |

|

Hyundai |

4.1 |

4.3 |

5.1 |

5.5 |

5.4 |

5.6 |

|

Kia |

3.5 |

3.9 |

4.5 |

4.9 |

4.9 |

4.9 |

|

Mazda |

1.6 |

1.9 |

2.2 |

2.1 |

2.3 |

2.6 |

Source: Congress Government

The integrated auto supply chain participation, vehicle export and assembly orientation, suitable trade agreement stability, cold-climate performance requirements, currency dynamics, and energy export linkage are certain trends that are bolstering the automotive air fuel module market in Canada. As per an article published by the ITA in April 2026, the automotive aftermarket yearly retail valuation in the country is predicted to reach USD 19 billion by the end of 2030. This has been possible with a surge in passenger vehicle imports to an estimated 15.6% to USD 38.6 billion as of 2023. Simultaneously, domestic imports of automotive components and parts were worth USD 18.5 billion, indicating an increase by roughly 19.7%. Therefore, with all these yearly growth in the overall automotive sector, there is a huge growth opportunity for the market in the overall country.

Key Automotive Air Fuel Module Market Players:

- Bosch (Germany)

- Continental AG (Germany)

- Mahle (Germany)

- MANN+HUMMEL (Germany)

- Roechling (Germany)

- Valeo (France)

- HUTCHINSON (France)

- Magneti Marelli (Italy)

- Sogefi (Italy)

- Denso Corporation (Japan)

- Aisan Industry (Japan)

- Keihin (Japan)

- Hitachi Automotive Systems (Japan)

- Mikuni (Japan)

- Delphi Technologies (UK)

- Donaldson Company (U.S.)

- Visteon Corporation (U.S.)

- Hyundai Kefico (South Korea)

- Anand Automotive (India)

- DRB-HICOM (Malaysia)

- Hanon Systems (South Korea)

- MANN-FILTER (Germany)

- PHINIA Inc. (U.S.)

- Toyota Motor North America (U.S.)

- Rehlko (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Bosch significantly constitutes a foundational position in the automotive air fuel module market through its strengthened expertise in engine management systems and fuel delivery technologies. The company is focused on refining its air-fuel ratio modules to support both traditional internal combustion engines and next-generation hybrid powertrains.

- Continental AG has leveraged its comprehensive portfolio in powertrain electronics and sensor integration to develop innovative air fuel modules that improve combustion efficiency. The company focuses on engineering solutions that assist automakers in meeting progressively stringent emission standards across global economies.

- Mahle applies its deep knowledge of air intake and filtration systems to manufacture integrated air fuel modules that optimize engine breathing and fuel mixing. The company has emphasized durability and thermal management to ensure module reliability under diverse operating conditions.

- MANN+HUMMEL readily specializes in clean air delivery systems that form a critical upstream component of the automotive air fuel module assembly. The company innovates in filter media and housing design to maintain consistent air quality entering the engine's combustion chamber.

- Roechling contributes to the market through its precision-engineered plastic components used in air intake manifolds and module housings. The company focuses on lightweight material solutions that reduce overall module weight without compromising structural integrity or sealing performance.

Here is a list of key players operating in the global automotive air fuel module market:

The global automotive air fuel module market is highly characterized by a consolidated competitive landscape, which is significantly dominated by established tier-1 automotive suppliers with in-depth engineering expertise in fuel delivery and engine management systems. Moreover, notable players such as Bosch, Denso, and Continental account for the majority of market share through their extensive R&D capabilities and long-standing OEM relationships. Likewise, tactical approaches among key players focus on developing advanced air-fuel ratio control technologies that are compatible with hybrid powertrains. Besides, in November 2025, Hanon Systems collaborated with Hankook & Company Group and introduced suitable solutions for sustainable and electrified mobility. The purpose was to extend technological leadership and advancement, especially into the aftermarket, and further expand worldwide competitiveness, thus fueling the automotive air fuel module industry.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, MANN-FILTER expanded its filters portfolio with lignin-specific media in the aftermarket, demonstrating an increase in the transition to continued sustainable production, with additional oil and air filters for different vehicles.

- In April 2026, PHINIA Inc. introduced its newest innovations by making progress in 500bar+ peak injection pressures for its very own cutting-edge gasoline direct injection (GDi) system, which is engineered for supporting the automotive sector’s shift to emission regulations.

- In April 2025, Toyota Motor North America and Rehlko declared their supplier agreement, wherein Toyota offered its very own hydrogen-driven fuel cell modules to Rehlko for its utilization in stationary power generator products.

- Report ID: 8581

- Published Date: May 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.