Automotive Intercooler Market Outlook:

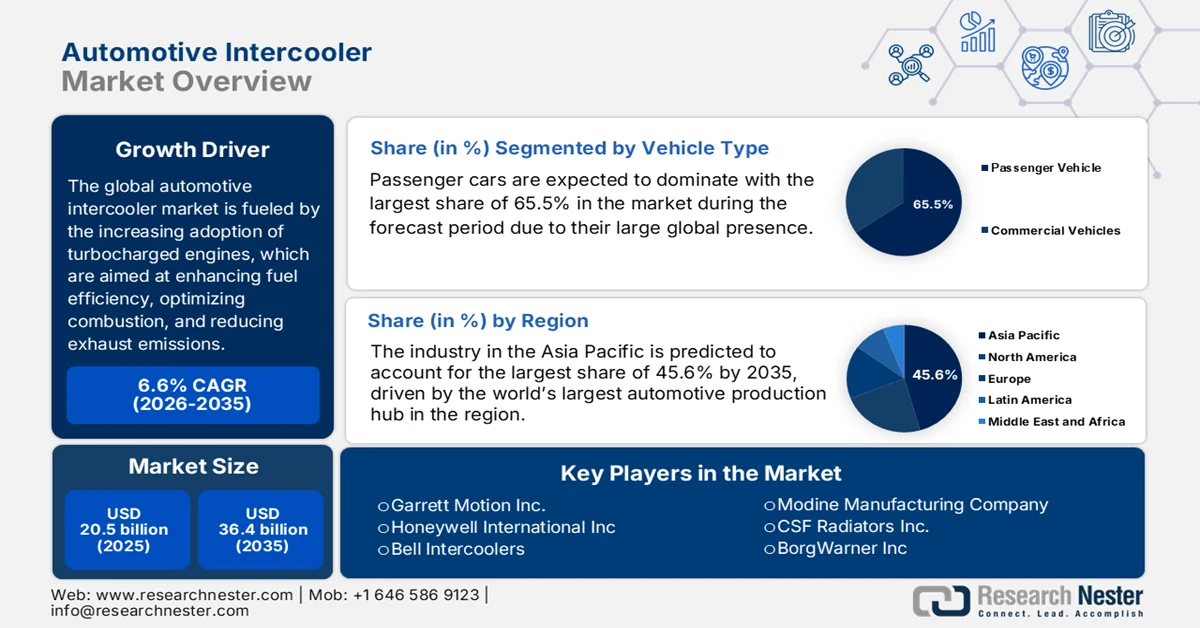

Automotive Intercooler Market size was valued at USD 20.5 billion in 2025 and is projected to reach USD 36.4 billion by the end of 2035, rising at a CAGR of 6.6% during the forecast period from 2026 to 2035. In 2026, the industry size of automotive intercooler is assessed at USD 21.8 billion.

The increasing adoption of turbocharged engines, which enhance fuel efficiency, optimize combustion, and reduce exhaust emissions, is the main factor responsible for the upliftment of the automotive intercooler market. As per an article published by the U.S. Environmental Protection Agency (EPA) in February 2026, turbochargers increase engine power by forcing more air and fuel into the engine, allowing a 4-cylinder turbocharged engine to produce the power of a larger naturally aspirated engine. Besides, the report underscored that most of the gasoline turbocharged engines in 2024 used GDI and VVT, thereby improving efficiency, reducing engine knock, and cutting turbo lag. Moreover, gasoline turbocharged engines, which include HEVs and PHEVs, accounted for almost 44% of all vehicle production in model year 2024, thus denoting a lucrative growth opportunity for automotive intercoolers.

Furthermore, with the increasing demand for vehicles, the shift toward hybrid powertrains continues to create demand for specialized, efficient cooling solutions. At the same time, expanding vehicle production and the growing popularity of performance-oriented aftermarket upgrades are deliberately driving the automotive intercooler market demand. In February 2026, the article published by the U.S. Energy Information Administration stated that about 22% of U.S. light-duty vehicle sales were hybrid, battery electric, or plug-in hybrid vehicles in 2025, which is up from 20% in 2024. The hybrid electric vehicles gained market share, whereas battery electric and plug-in hybrid sales declined after federal tax credits expired in September. Hybrid vehicles, which do not require plugs, were unaffected by tax credit expiration and do not directly impact grid electricity demand, thus denoting a huge opportunity for the automotive intercooler market in the upcoming years.

Key Automotive Intercooler Market Insights Summary:

Regional Highlights:

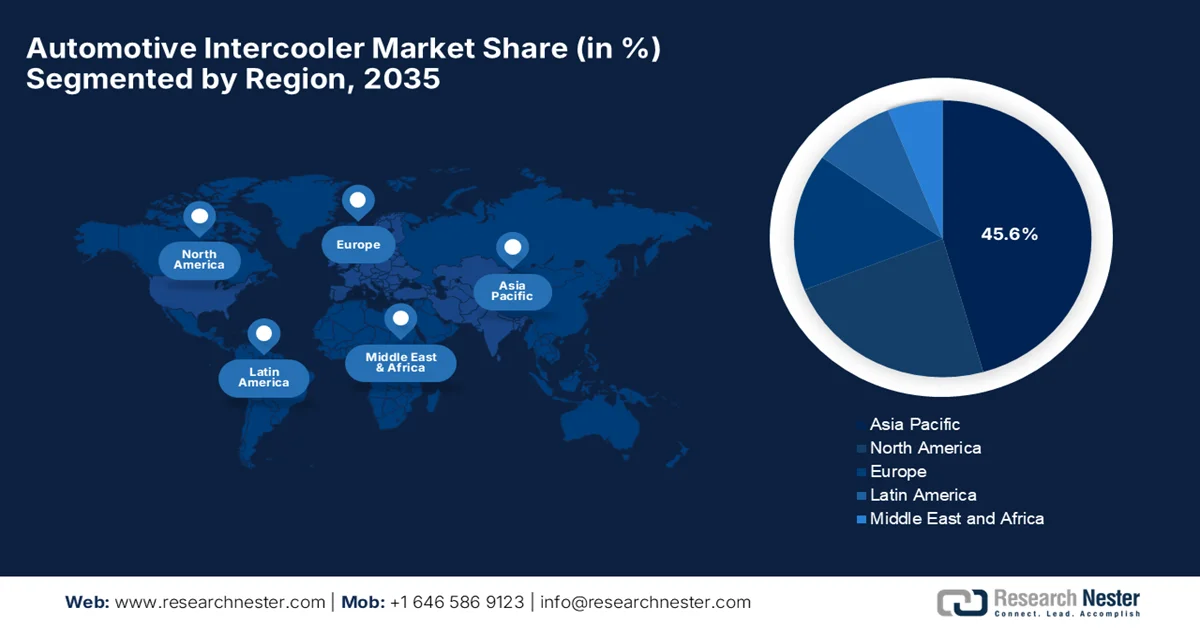

- Asia Pacific region is projected to command a 45.6% share of the automotive intercooler market by 2035, propelled by its dominance in global vehicle production and expanding electrification trends

- North America is anticipated to witness notable growth in the forecast period 2026-2035, stimulated by the increasing shift toward turbocharged SUVs and performance-oriented vehicles

Segment Insights:

- In the automotive intercooler market, the passenger cars segment is expected to hold a 65.5% share by 2035, driven by rising consumer inclination toward personal mobility and performance optimization

- The air-to-liquid intercooler segment is projected to secure a significant revenue share by 2035, fueled by its superior cooling efficiency and enhanced engine performance capabilities

Key Growth Trends:

- Stringent emission regulations

- Growth in passenger & commercial vehicle production

Major Challenges:

- Integration with electrified and hybrid powertrains

- Competition from alternative cooling technologies

Key Players: Garrett Motion Inc. (U.S.), Honeywell International Inc. (U.S.), Bell Intercoolers (U.S.), Modine Manufacturing Company (U.S.), CSF Radiators Inc. (U.S.), BorgWarner Inc. (U.S.), Mishimoto Automotive (Japan), Denso Corporation (Japan), HKS Co., Ltd. (Japan), GReddy (Japan), Valeo SA (France), MAHLE GmbH (Germany), Nissens A/S (Denmark), Pro Alloy Motorsport Ltd (UK).

Global Automotive Intercooler Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 20.5 billion

- 2026 Market Size: USD 21.8 billion

- Projected Market Size: USD 36.4 billion by 2035

- Growth Forecasts: 6.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, India

- Emerging Countries: Brazil, Mexico, Indonesia, Vietnam, Thailand

Last updated on : 7 April, 2026

Automotive Intercooler Market - Growth Drivers and Challenges

Growth Drivers

- Stringent emission regulations: The globally implemented regulatory standards are encouraging lower CO₂ and pollutant emissions, which are accelerating the shift to smaller, forced‑induction engines that require intercooling for reduced environmental impact. In March 2024, the U.S. EPA finalized stricter greenhouse gas emission standards for light- and medium-duty vehicles, which will begin with model year 2027, phasing in through 2032. These rules build on earlier standards for 2023 to 2026 and leverage clean car technologies to reduce climate pollution, improve public health, and lower driver costs. On the other hand, annual reports track manufacturer performance and long-term fuel economy trends for several decades, hence positively impacting the automotive intercooler market’s expansion and exposure.

- Growth in passenger & commercial vehicle production: The aspect of increased automotive production volumes across different economies, especially in emerging markets, supports greater intercooler deployment as standard equipment in the newest vehicles. In September 2025, the article published by India Brand Equity Foundation (IBEF) stated that India’s automotive sector contributes around 7.1% to GDP and is emerging as a global passenger vehicle export hub with 15 international manufacturers operating across the country. At the same time, OEMs such as Hyundai, Maruti Suzuki, Tata Motors, and Kia are exporting to 100 countries. Compact cars and drive growth, supported by initiatives such as Make in India and the PLI scheme, thus driving demand in the automotive intercooler market.

- Technological advancements & material innovation: Global leaders are focused on developing lighter intercooler designs, such as advanced air‑to‑air and air‑to‑water systems, and the use of aluminum and composite materials. This readily enhances performance, thereby contributing to the growth of the automotive intercooler market. In April 2025, Garrett Motion showcased its latest innovations at Auto Shanghai 2025, which include the introduction of its 3-in-1 e-powertrain and e-cooling compressor technologies in China, which are aimed at advancing zero-emission vehicle performance. The E-Cooling compressor in this delivers high-performance, oil-free thermal management for electric trucks, buses, and passenger cars, supporting efficient battery and cabin cooling, thus prompting a profitable business environment for pioneers in this field.

Challenges

- Integration with electrified and hybrid powertrains: The major shift towards electric vehicles is a big obstacle hindering the growth of the automotive intercooler market. The traditional intercoolers primarily manage air intake temperatures in internal combustion engines, but hybrid and range-extended electric vehicles demand thermal management across batteries, power electronics, and motors. In this context, designing intercoolers that can integrate properly into these complex powertrains is difficult. At the same time, space constraints, thermal load variations, and differing cooling requirements for multiple components complicate the engineering attributes. In addition, systems need to maintain durability and performance under high-voltage and fluctuating operational conditions. Therefore, this integration challenge imposes limitations on the direct transfer of existing intercooler designs to electrified platforms, forcing manufacturers to make heavy investments in R&D for effective solutions.

- Competition from alternative cooling technologies: Emerging cooling technologies, such as liquid-cooled charge air systems, phase-change materials, and advanced heat exchangers, are adding competitive pressure on the traditional way of air-to-air intercoolers. These alternatives can offer better efficiency, reduced weight, making it challenging for conventional intercooler adoption. Manufacturers in the automotive intercooler market face the dilemma of investing in established intercooler designs or adopting newer, less-proven technologies that might deliver superior performance. Therefore, this uncertainty can delay procurement decisions and slow the commercialization of traditional solutions. In addition, automakers in this sector need to consider reliability, cost-effectiveness, and manufacturability when comparing alternatives, thus creating a constant pressure point for intercooler manufacturers, affecting automotive intercooler market growth.

Automotive Intercooler Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.6% |

|

Base Year Market Size (2025) |

USD 20.5 billion |

|

Forecast Year Market Size (2035) |

USD 36.4 billion |

|

Regional Scope |

|

Automotive Intercooler Market Segmentation:

Vehicle Type Segment Analysis

In the vehicle type segment, passenger cars are expected to dominate with the largest share of 65.5% in the automotive intercooler market during the forecast period. Their large global presence and rising consumer interest in performance optimization are the key factors behind this dominance. At the same time, there has been an increasing demand for personal mobility, coupled with the growing popularity of sports and custom-built cars, which has significantly driven the adoption of intercoolers in this category. In September 2025, Nissan introduced its all-new 1.0-liter turbocharged engine in the Middle East. It will deliver 99 hp, 152 Nm of torque, and fuel efficiency of up to 17.3 km/l; the powertrain blends spirited performance with smooth drivability. Therefore, the consistent innovations from the pioneering companies, coupled with significant trade of passenger cars, position the segment at the forefront of revenue generation in this sector.

Technology Type Segment Analysis

Air-to-liquid intercooler, which is under the technology segment, is anticipated to grow with a considerable revenue share in the automotive intercooler market by the end of 2035. The growth of the segment is largely attributable to its superior efficiency and advanced performance capabilities. These systems provide better cooling when compared to traditional air-to-air intercoolers, enabling higher engine pressure and increased horsepower without altering engine size. In September 2025, BMW reported that its B58 3.0-liter straight-six has become a cornerstone engine since its debut, powering 41 models across BMW and even brands such as Toyota and Morgan. It consists of a twin-scroll turbo and an integrated intercooler; it blends strength, efficiency, and refinement. Thus, such instances solidify the segment’s position in the upcoming years.

Sales Channel Segment Analysis

The aftermarket segment leads the sales channel category in the automotive intercooler market during the discussed timeframe. The segment’s growth is largely driven by its affordability and flexibility for consumers. As the global vehicle parc continues to expand and vehicles remain in use for longer periods, this in turn raises the need for replacement and performance-enhancing components such as intercoolers. Besides, the aftermarket provides a wide range of options for customization and upgrading, especially among motorsports enthusiasts and performance vehicle owners. In addition, the relatively lower installation costs and compatibility with various vehicle types make aftermarket intercoolers highly attractive among consumers. Furthermore, this segment is expected to maintain its prominent position due to continuous demand for upgrades, replacements, and performance modifications.

Our in-depth analysis of the automotive intercooler market includes the following segments:

|

Segment |

Subsegments |

|

Vehicle Type |

|

|

Technology |

|

|

Sales Channel |

|

|

Design Type |

|

|

Engine Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Intercooler Market - Regional Analysis

APAC Market Insights

The Asia Pacific automotive intercooler market is anticipated to garner the largest revenue share of 45.6% during the discussed timeframe. The region’s dominance is largely propelled by the world’s largest automotive production hub, and it plays a prominent role in overall vehicle manufacturing and electrification. According to the official statistics published by the International Trade Administration in November 2025, Japan is considered to be the world’s fourth-largest automotive market, with almost 4.4 million new passenger vehicles sold in 2024. It also mentioned that domestic brands dominate with a 95% market share and are led by Toyota at 41%, whereas imports account for just 5%. Kei cars continue to thrive, making up over one-third of sales thanks to affordability and tax incentives. Thus, this large production footprint supports intercooler demand tied to both internal combustion and electrified vehicles.

The high vehicle production volumes and the widespread adoption of turbocharged engines are rearranging the growth dynamics of the automotive intercooler market in China. Manufacturers in the country are highly focused on technological innovations, such as liquid-cooled charge air systems and the development of lightweight materials, to enhance efficiency in remaining ICE and hybrid platforms. Based on the government data published in January 2026, the country’s auto industry has grown tremendously in 2025, with production reaching 34.5 million units and sales totaling 34.4 million, which is up over 9 percent year-on-year. This marks the 17th consecutive year China has led the world in both output and sales, maintaining volumes above 30 million for three straight years. It also stated that new energy vehicles drove much of the growth, with over 16.6 million produced and 16.49 million sold, reflecting nearly 30 percent annual increases, thus suitable for bolstering the market’s growth.

In India, the automotive intercooler market is growing on account of vehicle emission regulations. This regulatory shift has mandated a remarkable increase in the adoption of turbocharged engines across both passenger and commercial vehicle segments, with the main goal to improve fuel efficiency and reduce nitrogen oxide and particulate matter emissions. As per the article published by Press Information Bureau (PIB) in July 2022, the country’s auto fuel policy, by leapfrogging directly from BS-IV to BS-VI emission norms, has reduced permissible Sulphur content from 50 ppm to just 10 ppm. Besides, this improvement enabled the adoption of advanced emission control technologies such as diesel particulate filters and selective catalytic reduction systems to reduce particulate matter and nitrogen oxide emissions. Oil India Limited has strengthened safety and environmental management with over 1,000 SOPs under its HSSE framework, regularly reviewed by top management, thus positively impacting the market’s expansion.

North America Market Insights

The leadership in technological innovation, stringent federal fuel economy standards, and a regional shift toward turbocharged light trucks and SUVs are certain drivers that are responsible for driving the automotive intercooler market in North America. Simultaneously, the increasing popularity of large performance-oriented vehicles sustains demand for high-capacity air-to-air and air-to-water cooling systems. As per the article published by the U.S. EPA in February 2026, the country’s automotive industry is making a shift toward SUVs, with 66% of new vehicles classified as trucks in model year 2024. The report highlights a long-term transition away from sedans/wagons toward both truck SUVs and car SUVs, with truck SUVs alone accounting for nearly half of total vehicle production. In addition, the manufacturers are applying advanced technologies such as turbocharged engines and gasoline direct injection to improve efficiency and performance.

The U.S. automotive intercooler market is solidifying its position in the regional landscape, which is effectively propelled by the presence of pioneering companies and their focus on developing lightweight materials and integrated thermal management solutions. These solutions are for both traditional internal combustion engines and next-generation hybrid powertrains. As per the article published by the U.S. EPA in July 2025, conventional gasoline and diesel vehicles are also benefiting from advanced technologies that improve efficiency and performance. Attributes such as multi-speed and continuously variable transmissions, cylinder deactivation, and start-stop systems help reduce fuel consumption. Also, the turbocharging allows smaller engines to deliver big power, ensuring that even traditional vehicles remain competitive, cost-effective, and environmentally friendlier in today’s automotive landscape, thus driving demand for intercoolers.

Canada automotive intercooler market has gained immense exposure, largely driven by the increasing adoption of turbocharged engines as manufacturers are looking to meet stricter federal standards. The long-term outlook for the country’s market is reshaped by an aggressive shift toward zero-emission vehicles and a robust aftermarket sector. Based on the government data published in February 2026, the country introduced an automotive strategy to transform its industry and reduce reliance on the U.S. market. It is efficiently backed by huge funding and tax incentives, and the plan prioritizes stronger emissions standards and expanded consumer affordability programs. Investments in charging infrastructure, trade diversification with partners such as Korea and China, and workforce reskilling aim to secure Canada’s leadership in clean mobility, thus making it suitable for bolstering the country’s market growth.

Europe Market Insights

The presence of top-tier automakers and dense concentration of vehicle manufacturing is responsible for uplifting the automotive intercooler market in Europe. The region is seeing rapid expansion through focused investments in innovative automotive technologies. The European Union is proactively advancing the decarbonisation of its transport sector to meet the Paris Agreement goals, aiming for at least a 55% reduction in greenhouse gas emissions by 2030 and climate neutrality by 2050. Despite improvements in engine efficiency, transport emissions have risen, prompting policies to boost low- and zero-emission vehicles and associated infrastructure. Regulations such as the EU Emissions Trading System, the Effort-Sharing Regulation 2023/857, and the Net-Zero Industry Act (2023) set binding emission targets and support the adoption of cleaner vehicle technologies. These measures make sure that conventional and advanced combustion vehicles, including turbocharged and intercooler-equipped engines, comply with these stricter environmental standards.

A world-class manufacturing base and the presence of major domestic automakers that heavily utilize turbocharged engines to balance performance with fuel efficiency are the main factors responsible for boosting the overall automotive intercooler market in Germany. The country is positioning itself as a global hub for high-performance and tuning aftermarket solutions, wherein the high-efficiency intercoolers are in steady demand by enthusiasts seeking to maximize engine power and durability. As per the Germany Trade & Invest reports, Germany’s automotive industry is Europe’s leader, which has generated almost USD 614.2 billion in revenue in 2024, with 70% from exports. It produced 4.07 million passenger cars and registered 2.8 million new vehicles, employing 773,000 people, including 158,000 in R&D. In addition, the country presents remarkable opportunities that lie in e-mobility, battery technology, autonomous driving, fuel cells, and software-defined vehicles, hence driving demand in the automotive intercoolers industry.

The UK automotive intercooler market is undergoing a period of rapid growth, largely driven by the regulatory environment, which has made intercoolers essential for enhancing fuel efficiency and reducing greenhouse gas emissions across both passenger and commercial vehicle segments. The long-term landscape in the country is being reshaped by the country’s aggressive transition toward zero-emission vehicles, as battery electric vehicles, which do not require traditional intake cooling, gain market share. Domestic manufacturers are pivoting toward integrated thermal management solutions for hybrid platforms to be competitive in the global dynamics. Based on the February 2026 government data, domestic transport remained the largest greenhouse gas emitting sector, accounting for around 30% of total emissions in 2024, which is encouraging automotives to opt for sustainable options, such as intercoolers.

Key Automotive Intercooler Market Players:

- Garrett Motion Inc. (U.S.)

- Honeywell International Inc. (U.S.)

- Bell Intercoolers (U.S.)

- Modine Manufacturing Company (U.S.)

- CSF Radiators Inc. (U.S.)

- BorgWarner Inc. (U.S.)

- Mishimoto Automotive (Japan)

- Denso Corporation (Japan)

- HKS Co., Ltd. (Japan)

- GReddy (Japan)

- Valeo SA (France)

- MAHLE GmbH (Germany)

- Nissens A/S (Denmark)

- Pro Alloy Motorsport Ltd (UK)

- Forge Motorsport Ltd. (UK)

- MANN+HUMMEL Group (Germany)

- HELLA (Germany)

- Marelli (Japan)

- Amazon Web Services (U.S.)

- PWR Advanced Cooling Technology (Australia)

- Hanon Systems Co., Ltd. (South Korea)

- Tata AutoComp Systems Ltd. (India)

- REX Heat Exchanger (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Garrett Motion Inc. is identified as one of the leading automotive technology companies specializing in turbochargers, thermal management, and related systems. The company’s advanced intercoolers and thermal solutions are especially designed to optimize charge‑air cooling and enhance engine performance.

- BorgWarner Inc. is a major automotive supplier that has a strong focus on thermal management systems, including Intercell eCoolers. The firm’s systems improve fuel economy and reduce emissions by efficiently managing thermal loads, which is a key component in supporting intercooler and overall vehicle cooling architectures.

- Honeywell reorganized its automotive turbo business under the Honeywell Garrett brand. The company is deeply involved in turbocharging technologies that complement intercooler systems. Besides its automotive turbo innovations, which optimize engine performance and emissions, are driving intercooler demand as part of the forced induction and thermal management ecosystem.

- Denso Corporation is one of the world’s largest automotive parts manufacturers, which has an expanded portfolio of thermal management products that includes OEM‑quality intercoolers and charge air coolers for turbocharged engines. The firm’s intercoolers help improve engine efficiency and reduce emissions.

- MANN+HUMMEL Group is a global filtration and thermal management specialist whose intercoolers and related components are extensively used by OEMs in passenger and commercial vehicles. The firm’s thermal systems are mainly focused on efficient air and coolant flow, thereby contributing to improved engine performance and reduced emissions.

Below is the list of some prominent players operating in the global automotive intercooler market:

The automotive intercooler market hosts both established global suppliers and specialized regional manufacturers. Major players such as Garrett Motion, Honeywell, Valeo, MAHLE, and Denso lead in terms of advanced thermal management solutions and strong OEM partnerships. At the same time, the regional innovators from Japan and Europe are highly focused on high‑precision engineering and integration with turbo and hybrid systems, whereas companies in India and Australia emphasize cost‑effective, adaptable products for emerging markets. In May 2025, HELLA announced its return to the thermal management segment in the aftermarket, launching an initial range of 1,200 spare parts, which also includes intercoolers, with plans to expand to 6,000 components by the end of 2027. The company aims to consolidate its role as a full-range supplier in the independent aftermarket by leveraging its two decades of experience in engine cooling and air conditioning.

Corporate Landscape of the Automotive Intercooler Market:

Recent Developments

- In March 2026, Marelli, in collaboration with AWS, introduced an AI-powered system test generation agent to automate the creation of system test cases from engineering requirements in validating software-defined vehicle systems.

- In February 2026, Garrett reported that its intercooler core technology, validated in high-load testing on a 900 hp Audi RS6, demonstrated superior thermal stability and consistent performance under repeated acceleration cycles.

- Report ID: 4401

- Published Date: Apr 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Automotive Intercooler Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.