Automotive Aluminum Market Outlook:

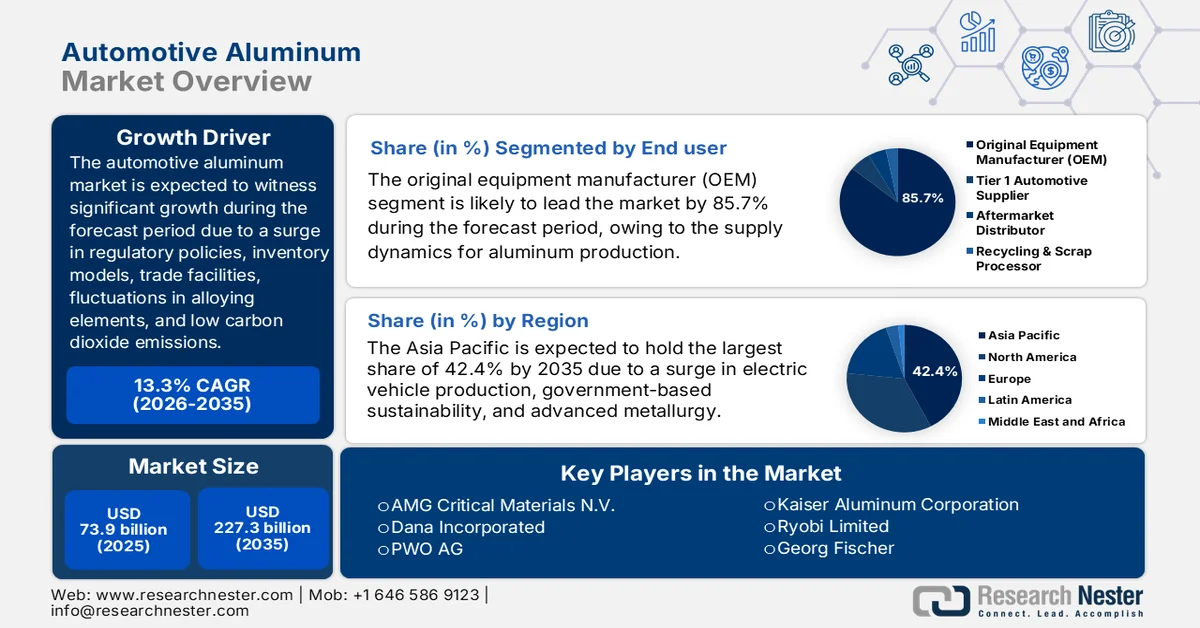

Automotive Aluminum Market size was valued at USD 73.9 billion in 2025 and is expected to reach USD 227.3 billion by the end of 2035, growing at a 13.3% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of automotive aluminum is evaluated at USD 83.7 billion.

The worldwide automotive aluminum market is significantly shaped by different foundational factors, including regulatory frameworks for mandating low carbon dioxide emissions, trade dynamics for aluminum and steel, inventory models by manufacturers, fluctuation in alloying elements, such as copper and magnesium, and the push for circular economy principles. According to official statistics published by International Aluminum in 2026, there will be an increase in the aluminum demand by nearly 40% by 2030, while the overall industry is expected to produce an additional 33.3 million tons to cater to the growing demand across all industrial sectors, from 86.2 million tons as of 2020 to 119.5 million tons in 2030. Besides, the electrical, packaging, construction, and packaging industries are driving the market demand, accounting for 75% of the overall metal requirement.

2024 Metal Import and Export Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

China |

286 billion |

138 billion |

|

Germany |

118 billion |

105 billion |

|

U.S. |

87.1 billion |

172 billion |

|

Global Trade Valuation |

1.5 trillion |

|

|

Global Trade Share |

6.8% |

|

|

Product Complexity |

0.2 |

|

Source: OEC

Furthermore, the digital twin integration in aluminum die casting, low-altitude economy and eVTOL as a new aluminum demand frontier, geopolitical supply chain reconfiguration, and material substitutions pressures from advanced composites, are a few trends that are responsible for driving the automotive aluminum market globally. As per an article published by Intelligent Systems with Applications in June 2025, the method of combining digital twins with a long and short-term memory algorithm has achieved a 91.8% accuracy for predicting the production line capacity of aluminum, which is further verified on a commemorative disk production line. In addition, this particular approach enhances production control as well as evaluates delivery dates and capacity. Therefore, based on this benefit, the digital twin is extremely suitable to uplift the aluminum capacity production globally.

Key Automotive Aluminum Market Insights Summary:

Regional Highlights:

- Asia Pacific is projected to lead the automotive aluminum market with a 42.4% share by 2035, driven by rapid industrialization and surging electric vehicle production

- Europe is anticipated to be the fastest-growing region over the forecast period, propelled by stringent emission regulations and rising adoption of advanced aluminum alloys

Segment Insights:

- In the automotive aluminum market, the original equipment manufacturer (OEM) segment is projected to account for an 85.7% share by 2035, propelled by mounting regulatory pressure to reduce fleet-wide emissions while maintaining vehicle safety and performance

- The passenger car sub-segment is anticipated to capture a considerable share by 2035, fueled by rising demand for lightweighting to improve fuel efficiency and extend electric vehicle range

Key Growth Trends:

- AI facility buildout for non-cyclical aluminum demand

- Regulatory push for recycled content in vehicle production

Major Challenges:

- Competing lightweight materials and joining complexities

- Recycling quality and closed-loop supply chain gaps

Key Players: Constellium, Norsk Hydro, Arconic, Novelis, UACJ, Alcoa Corporation, Rio Tinto Group, Hindalco Industries Limited, China Hongqiao, Nanshan Aluminum, Aluminum Corporation of China Chalco, Nemak, Speira, AMG Critical Materials N.V., Dana Incorporated, PWO AG, Kaiser Aluminum Corporation, Ryobi Limited, Georg Fischer, Ahresty Corporation, Emirates Global Aluminium, AISIN Corporation, ALUnited, Rio Tinto.

Global Automotive Aluminum Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 73.9 billion

- 2026 Market Size: USD 83.7 billion

- Projected Market Size: USD 227.3 billion by 2035

- Growth Forecasts: 13.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.4% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 28 April, 2026

Automotive Aluminum Market - Growth Drivers and Challenges

Growth Drivers

- AI facility buildout for non-cyclical aluminum demand: This is one of the emerging growth drivers for the massive automotive aluminum market demand, which is effectively generated by an artificial intelligence (AI) data center facility. According to official statistics published by the Brookings Education in November 2025, hyperscale data centers usually comprise over 5,000 file servers within their infrastructures. Besides, the generative AI industry escalated almost 40% per year and increased by USD 43.9 billion as of 2023, and is further projected to reach USD 1 trillion by the end of 2032. Therefore, this projected growth is based on the requirement of huge amounts of aluminum for power distribution systems, structural components, and cooling facilities, thus fueling the automotive aluminum market growth.

- Regulatory push for recycled content in vehicle production: The aspect of strict environmental regulations targeting automotive emissions is currently expanding to material production emissions, which is uplifting the unprecedented demand for the automotive aluminum market. As stated in an article published by the International Aluminum Organization in 2026, aluminum is considered one of the most recycled materials on earth, with nearly 75% of the 1.5 billion tons effectively produced and utilized. In addition, every year, more than 30 million tons of aluminum scrap are recycled worldwide, which ensures its status as the ultimate recycled material on the overall planet. Therefore, with such recognition, it is increasingly implemented and utilized by the automotive sector globally.

- Energy cost volatility favoring vertical integration: The sharp increase in worldwide energy prices is effectively driving a competitive transition to vertically integrated aluminum producers with access to low-cost and stabilized energy sources. As per an article published by End Fuel Poverty Coalition in April 2026, an increase has been estimated for energy bills by USD 265.4 from July. Additionally, the price will amount to USD 2,488.7 for a particular dual fuel household, demonstrating an upsurge by 12% from April. Therefore, this increase in energy pricing has created a two-tier economy for automotive buyers, including aluminum from renewable-based smelters and fossil-fuel-dependent sources witnessing production disruptions and price volatility, thus creating a growth opportunity for the automotive aluminum market.

Challenges

- Competing lightweight materials and joining complexities: Aluminum does not exist in a vacuum; instead, it competes directly with advanced high-strength steel, carbon fiber composites, and magnesium alloys. Each material offers distinct advantages in specific vehicle applications. For structural components, steel remains cheaper and easier to weld, while carbon fiber provides superior weight reduction albeit at a higher cost. More critically, aluminum introduces significant manufacturing challenges since it is difficult to weld to dissimilar metals like steel or copper without galvanic corrosion, which compromises vehicle longevity. Joining aluminum to battery enclosures, chassis frames, or powertrain mounts requires specialized riveting, adhesive bonding, or laser welding technologies, all of which negatively impact the automotive aluminum market growth.

- Recycling quality and closed-loop supply chain gaps: While aluminum is infinitely recyclable, the automotive sector struggles to maintain closed-loop recycling systems without degrading material properties. Besides, vehicle aluminum comes in multiple alloy series, with each formulated for specific functions such as heat exchangers, body panels, or crash management systems. Mixing these alloys during conventional shredding and melting results in lower-grade cast aluminum unsuitable for high-performance structural applications. Therefore, achieving true circularity demands sophisticated scrap sorting technologies, including laser-induced breakdown spectroscopy and X-ray sorting, which remain expensive and not widely deployed across dismantling centers, thus causing a hindrance in the automotive aluminum market.

Automotive Aluminum Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

13.3% |

|

Base Year Market Size (2025) |

USD 73.9 billion |

|

Forecast Year Market Size (2035) |

USD 227.3 billion |

|

Regional Scope |

|

Automotive Aluminum Market Segmentation:

End user Segment Analysis

Based on the end user, the original equipment manufacturer (OEM) segment is anticipated to garner the largest share of 85.7% in the automotive aluminum market by the end of 2035. The segment’s upliftment is highly driven by integrating aluminum at the platform level, making strategic decisions that cascade through the entire supply chain. The primary driver for OEM dominance is the growing regulatory pressure to reduce fleet-wide emissions while maintaining vehicle safety and performance. Automakers are increasingly replacing traditional steel with aluminum alloys in structural components, body panels, and chassis systems to achieve lightweighting targets without compromising crashworthiness. Besides, OEMs must retool existing stamping plants, invest in new joining technologies such as self-piercing rivets and laser welding, and retrain production staff-all significant capital expenditures.

Vehicle Type Segment Analysis

The passenger car sub-segment, part of the vehicle type segment, is projected to account for the second-largest share in the automotive aluminum market. The sub-segment’s growth is effectively fueled by offering lightweighting that bolsters fuel economy, enhances electric vehicle range, and diminishes emissions. According to official statistics published by the MDPI in April 2025, there has been an increase in the worldwide electric vehicle sales by 25% as of 2024, in comparison to 2023, and successfully reached an estimated 11 million vehicles globally. Besides, as per the 2025 IEA Organization article, the electric car fleet significantly reached nearly 58 million, which is almost 4% of the overall passenger car fleet by the end of 2024. This growth is also equivalent to a surge in the total electric car fleet, thereby making it suitable for boosting the sub-segment’s growth.

Application Segment Analysis

By the end of the stipulated timeline, the body structure and closures sub-segment, which is part of the application segment, is expected to grab the third-largest share in the automotive aluminum market. The sub-segment’s development is highly propelled by its importance in the automotive industry, wherein it serves as the ultimate method for lightweighting to optimize vehicle performance and cater to stringent environmental regulations. As stated in a data report published by the Aluminum Association in December 2022, the worldwide aluminum industry is expected to reach USD 242 billion by the end of 2027, with yearly growth rates from 3.2% to 5.7%. Therefore, this has led to the largest predicted surge in battery electric vehicles (BEVs) in the past 2 decades, which is a robust catalyst for automotive aluminum, which is driving the sub-segment’s upliftment.

Our in-depth analysis of the automotive aluminum market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Vehicle Type |

|

|

Application |

|

|

Manufacturing Process |

|

|

Product Form |

|

|

Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Aluminum Market - Regional Analysis

APAC Market Insights

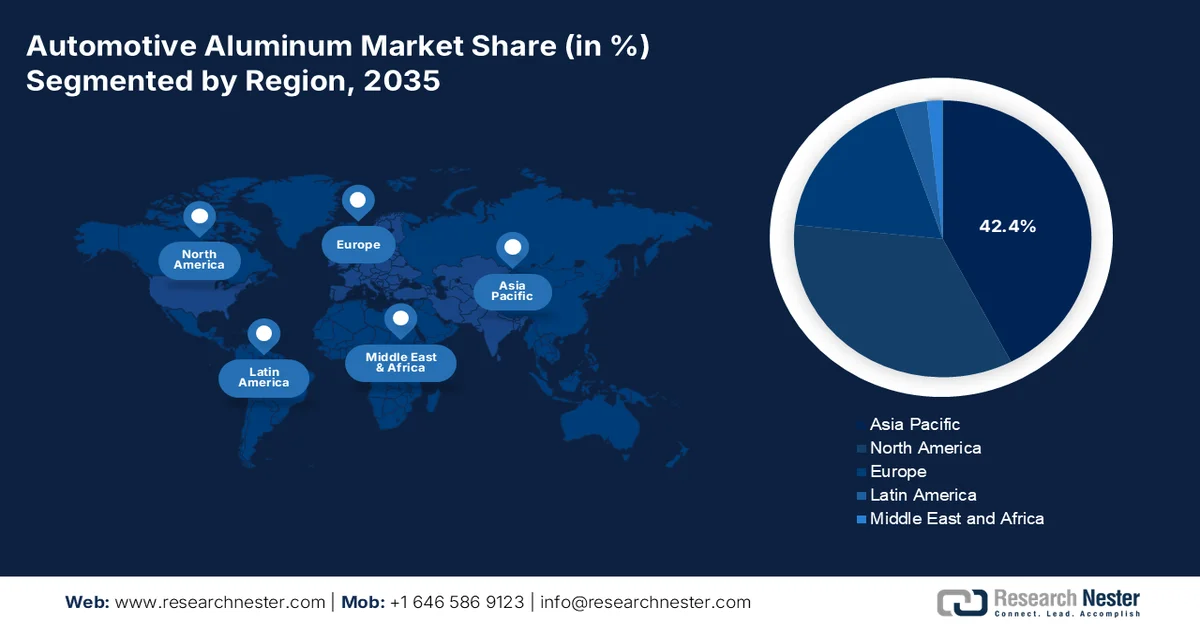

The Asia Pacific in the automotive aluminum market is anticipated to garner the highest share of 42.4% by the end of 2035. The market’s growth in the region is highly attributed to rapid industrialization, a surge in electric vehicle production, government-led sustainability, strong electric vehicle policies, regional aluminum production capacity, and innovative metallurgy and premium vehicle production. According to official statistics published by the Silver Institute Organization in December 2025, the electric vehicle industry penetration is expected to continue over the long-lasting forecast horizon, with worldwide production to grow at a 13% growth rate by the end of 2031. Besides, the shift from internal combustion engine vehicles, particularly battery electric vehicles, is leading to an average consumption of 67% to 79% of silver, thus enhancing the market demand.

The automotive aluminum market in China is growing significantly, owing to the largest automotive production, strong electric vehicle adoption, lightweighting targets, generous investment in low-carbon aluminum smelting and recycling facilities, and an expansion in charging infrastructure. As stated in an article published by the State Council Information Office in January 2026, there has been an increase in both automotive production and sales by 34 million units. In addition, the overall auto output reached 34.5 million units in 2025, demonstrating a 10.4% increase from 2024, and meanwhile, there has been a surge in sales by 9.4% year on year (YoY) to 34.4 million units. Moreover, the domestic output and sales remained stable for 17 years, thereby proliferating the market’s growth.

The aspects of an increase in strategic manufacturing facilities, supply chain diversification approaches, abundant bauxite reserves, raw material security, an increase in electronics and automotive industries, foreign direct investment plans, and participation in different free trade agreements are a few factors for bolstering the automotive aluminum market in Vietnam. Based on government estimates published by the USGS in October 2024, the country is regarded as the 11th largest producer of bauxite, effectively accounting for 1% of the global production, as well as 19% of worldwide reserves. Besides, the output valuation of the construction and manufacturing industries accounted for 6.2% and 25% of the gross domestic production (GDP) as of 2022, which indicated an increase in the overall industry’s output by 30%, thereby making it suitable for bolstering the market in the country.

Europe Market Insights

Europe in the automotive aluminum market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by strict emission-based regulations, the consumption of automotive aluminum extrusion, the rapid incorporation of aluminum alloys, tactical logistics positioning, and leveraging hydrogen-based production and advanced alloy technologies. According to official statistics published by Energy Policy in June 2026, the region launched the Delegated Act on renewable hydrogen, aiming to enable 70% reduction in emissions, in comparison to steam-methane reforming, by defining requirements for renewable hydrogen production. Besides, the region is highly dependent on domestic renewable hydrogen by the end of 2050, eventually enhancing annual expenses by almost 3%, and further requires 518 GW of electrolysis capacity, thus proliferating the market’s development.

2024 Hydrogen Export/Import Analysis in Europe

|

Countries |

Export (USD) |

Import (USD) |

|

Belgium |

36.7 million |

4.0 million |

|

Netherlands |

25.5 million |

36.3 million |

|

Germany |

17.6 million |

8.6 million |

|

France |

6.5 million |

17.9 million |

|

Poland |

3.6 million |

2.5 million |

|

Slovakia |

3.1 million |

1.8 million |

|

Hungary |

2.2 million |

- |

|

Spain |

1.9 million |

839,000 |

Source: OEC

The automotive aluminum market in Germany is gaining increased traction, owing to the concentration of premium automotive manufacturers, the sustained demand for high-performance aluminum extrusions, substantial commitments to electric vehicle production, sustainability programs, manufacturing capabilities, and government support for electric vehicle manufacturing. As stated in an article published by the ITA in August 2025, the country’s manufacturing exports surged from USD 955 billion as of 2022 to more than USD 1 trillion in 2023, and further to nearly USD 991 billion in 2024. Besides, the 2024 U.S. advanced manufacturing exports to the country amounted to USD 37 billion. In addition, the valuation of U.S.-based exports to the country accounted for an estimated USD 43 billion, thus relatively fueling the market’s exposure.

The government-based industrial decarbonization, 2030 investment strategy, an expansion in the electric vehicle industry, along with aerospace and aluminum synergy, are a few trends that are responsible for driving the automotive aluminum market in France. As per an article published by the Clean Energy Wire Organization in March 2026, based on the country’s 2030 investment plan, the domestic government effectively ramped up generous funding to combine worldwide competitiveness with climate objectives, with USD 528.4 million earmarked for the development and research of advanced low-carbon technologies. Besides, the country’s plans for decarbonizing industry, such as carbon capture and storage, with an initial aim of sequestering 4 to 8 million tons of carbon dioxide from industrial facilities every year by the end of 2030, thereby making it suitable for boosting the automotive aluminum market.

North America Market Insights

North America in the automotive aluminum market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by an increasing shift to electric vehicles, the adoption of closed-loop aluminum recycling systems, and automotive manufacturing partnering with suppliers for collecting manufacturing scrap and returning it as a usable sheet material. According to official statistics published by the Bureau of Labor Statistics in February 2023, there has been an increase in electric car sales, especially in the U.S., from a mere 0.2% of overall car sales to 4.6%, which is gradually increasing the demand for aluminum in the region. Moreover, electric vehicle sales in the country are expected to reach 40% of total passenger car sales by the end of 2030, along with 50% surge for foresee electric vehicle sales by the end of the same year.

2024 Electric Motor Vehicle Export/Import Analysis in North America

|

Countries |

Export (USD) |

Import (USD) |

|

Mexico |

10.2 billion |

1.3 billion |

|

U.S. |

6.0 billion |

22.4 billion |

|

Canada |

- |

7.2 billion |

|

Costa Rica |

- |

331 million |

|

Panama |

- |

31.8 million |

|

Barbados |

- |

31.7 million |

|

Guatemala |

- |

22.3 million |

Source: OEC

The automotive aluminum market in the U.S. is growing significantly, owing to the presence of strict fuel economy regulations, a boom in the electric vehicle production, lightweighting as a tactical imperative, and technological advancements in alloy development. As stated in an article published by the Department of Energy (DOE) in March 2026, the Office of Critical Minerals and Energy Innovation (CMEI) and Hydrocarbons and Geothermal Energy Office (HGEO) jointly declared a generous funding opportunity of almost USD 69 million for processes or technologies for advancing the domestic production and refining of critical materials. Besides, the Notice of Funding Opportunity (NOFO) is a significant part of the USD 1 billion in critical materials, and this is followed by the USD 500 million announcement by the Manufacturing Deployment Office for developing commercial and demonstration facilities to increase the supply of critical materials, which is positively uplifting the automotive aluminum market growth in the country.

The low-carbon hydroelectric power advantage, an increase in the demand for automotive sector lightweighting, the government support for electric vehicle supply chains, and the export integration with the U.S.-based automotive sector are certain factors that are boosting the automotive aluminum market in Canada. As per an article published by the Government of Canada in November 2023, the total population utilizes increased electricity from low-carbon resources, based on which the demand is poised to grow by 47% by the end of 2050, in terms of the evolving policy scenario. In this regard, the country’s electricity system is emerging as greener and is predicted to increase from 82% to 95% by the same year. Therefore, with all this expected growth, the market is gradually expanding in the country, which is enhancing the utilization of aluminum.

Key Automotive Aluminum Market Players:

- Constellium (Netherlands)

- Norsk Hydro (Norway)

- Arconic (U.S.)

- Novelis (U.S.)

- UACJ (Japan)

- Alcoa Corporation (U.S.)

- Rio Tinto Group (UK)

- Hindalco Industries Limited (India)

- China Hongqiao (China)

- Nanshan Aluminum (China)

- Aluminum Corporation of China (Chalco) (China)

- Nemak (Mexico)

- Speira (Germany)

- AMG Critical Materials N.V. (Netherlands)

- Dana Incorporated (U.S.)

- PWO AG (Germany)

- Kaiser Aluminum Corporation (U.S.)

- Ryobi Limited (Japan)

- Georg Fischer (Switzerland)

- Ahresty Corporation (Japan)

- Emirates Global Aluminium (United Arab Emirates)

- AISIN Corporation (Japan)

- ALUnited (France and Denmark)

- Rio Tinto (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Constellium is a major supplier of advanced aluminum sheet and structural components for the automotive industry, specializing in lightweight body-in-white and battery enclosure solutions. The company works closely with Europe and North America automakers to develop high-strength alloys that improve vehicle safety while reducing overall mass.

- Norsk Hydro leverages its vertically integrated operations to supply low-carbon aluminum extrusions and rolled products to global automotive manufacturers. The company focuses heavily on sustainable production methods, offering dedicated low-emission aluminum grades that help automakers meet tightening environmental regulations.

- Arconic provides high-performance aluminum sheet, plate, and forged products for critical automotive applications such as suspension systems and crash management components. The company maintains strong engineering collaboration with original equipment manufacturers to develop next-generation alloys tailored for electric vehicle architectures.

- Novelis is the world's largest producer of rolled aluminum products for the automotive sector, supplying closure panels, structural parts, and battery housings to nearly every major automaker. The company leads the industry in closed-loop recycling partnerships, collecting manufacturing scrap directly from stamping plants and returning it as usable sheet material.

- UACJ is a leading Japanese supplier of rolled and extruded aluminum for automotive heat exchangers, body panels, and battery components. The company serves major Asian automakers with advanced flat-rolled products designed to meet the precise dimensional and surface quality requirements of high-volume vehicle assembly lines.

Here is a list of key players operating in the global automotive aluminum market:

The automotive aluminum market is highly competitive, dominated by global giants, such as Novelis, Constellium, and Norsk Hydro, alongside strong regional players from China and Japan. Moreover, key strategic initiatives include heavy investment in recycled and low-carbon aluminum to meet OEM sustainability goals, with Novelis achieving significant recycled content and Norsk Hydro leading on zero-carbon products. Besides, in May 2025, Emirates Global Aluminium initiated an agreement to expand its CelestiAL solar aluminium supply to Hyundai Mobis. Under this agreement, the CelestiAL volume is expected to be increased from 8,000 to almost 15,000 tons per year by the end of 2026, and both EGA and Mobis are poised to explore a long-lasting agreement for supplying value-added aluminum products, thus proliferating the automotive aluminum market globally.

Corporate Landscape of the Automotive Aluminum Market:

Recent Developments

- In February 2026, AISIN Corporation, Minth Group Limited, and Toyota Tsusho Corporation agreed to establish ATM Automotive Parts Inc., based on a joint venture, for producing aluminum body frame parts, particularly in Canada, with the intention of strengthening the supply system for aluminum parts for vehicles in North America.

- In October 2025, ALUnited partnered with Jiangsu Asia-Pacific Light Alloy Technology Co., Ltd. (APALT), demonstrating a major and crucial player in the overall aluminum industry, and comprises two production facilities, including ALUnited Denmark in Tønder and ALUnited France in Louviers.

- In April 2025, Rio Tinto and AMG Metals & Materials signed a Memorandum of Understanding (MOU) to jointly address the feasibility of developing an integrated low-carbon aluminum project, which is powered by renewable energy in India.

- Report ID: 8539

- Published Date: Apr 28, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.