Advanced Persistent Threat Protection Market Outlook:

Advanced Persistent Threat Protection Market size was valued at USD 17.5 billion in 2025 and is projected to account for USD 50.5 billion by 2035, rising at a CAGR of 11.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of advanced persistent threat protection is assessed at USD 19.4 billion.

Government-backed cybersecurity assessments continue to indicate sustained state-aligned intrusion activity targeting critical infrastructure defense supply chains and public sector networks, driving the demand for advanced persistent threat protection market. The World Economic Forum January 2026 data indicates that the ransomware attack increased 54%, with many campaigns attributed to organized threat groups employing long-term persistence and lateral movement tactics. Similarly, the FBI's April 2024 data depicted that cybercrime recorded 880,418 complaints, reflecting a 22% YoY increase and underscoring the growing financial and operational risks to enterprises and government entities. Additionally, advanced persistent threat actors are increasingly exploiting vulnerabilities in legacy systems and third-party vendors, further intensifying enterprise demand for continuous monitoring and threat intelligence capabilities.

Besides, the adoption is further supported by the regulatory mandates and national cybersecurity strategies, highlighting the proactive threat intelligence and continuous monitoring. The U.S. has mandated Zero Trust architecture implementation across federal agencies, requiring agencies to deploy advanced detection and response mechanisms aligned with APT mitigation. In this context, the FDD 2026 data indicated that the proposed fiscal adjustments, such as a USD 707 million reduction to the cybersecurity and infrastructure security agency, lowering its budget to just over USD 2 billion from an anticipated USD 2.6 billion, have direct implications for procurement cycles and deployment timelines. As CISA functions as the central civilian cybersecurity authority, funding variability can influence federal contract volumes, prioritization of continuous monitoring programs, and support to critical infrastructure operators. Further, the statutory requirements and threat exposure levels continue to sustain baseline demand for persistent threat detection and response capabilities across government and regulated industries.

Key Advanced Persistent Threat Protection Market Insights Summary:

Regional Highlights:

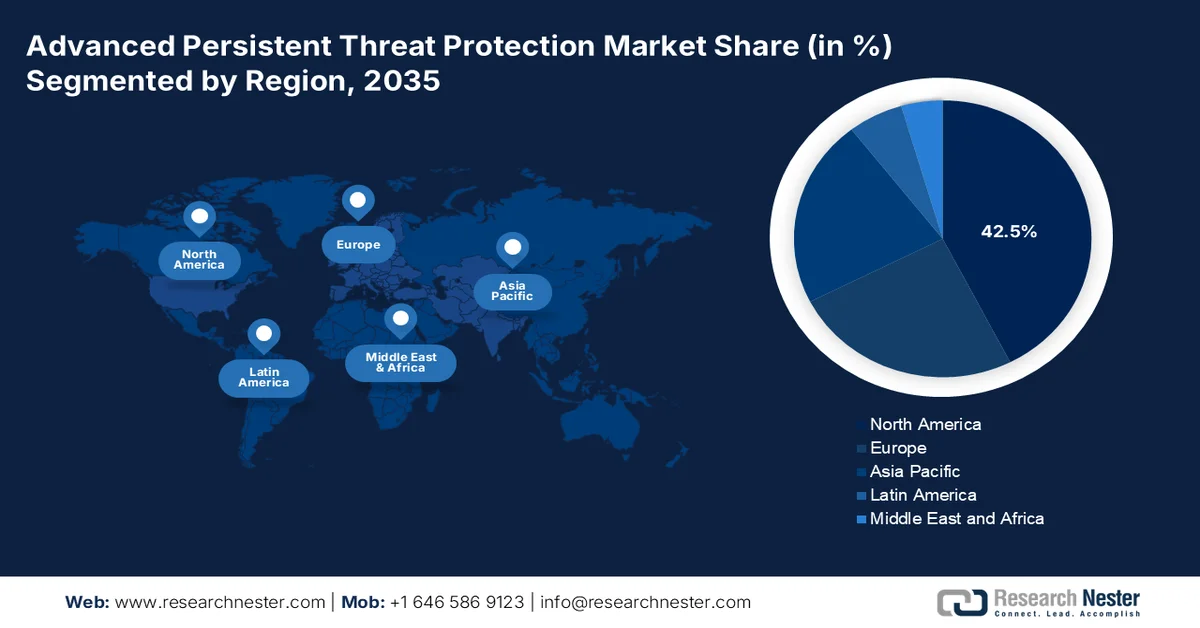

- The advanced persistent threat protection market in North America is projected to hold a 42.5% share by 2035, impelled by stringent regulatory frameworks and centralized government-led procurement systems

- Asia Pacific is anticipated to witness the fastest growth at a CAGR of 14.5% during 2026–2035, stimulated by rapid digital transformation across government and critical infrastructure sectors

Segment Insights:

- The advanced persistent threat protection market large enterprises segment is projected to account for 71.4% share by 2035, propelled by stringent regulatory mandates and increasing exposure to high-value cyber threats

- The cloud/SaaS subsegment within deployment mode is anticipated to dominate over 2026–2035, fueled by real-time threat intelligence updates and scalable protection across distributed workforces

Key Growth Trends:

- Expansion of federal cybersecurity budgets

- Increasing cyber incident costs

Major Challenges:

- Extreme technical complexity

- Intense pricing pressures and consumption-based commercial models

Key Players: CrowdStrike, Palo Alto Networks, Microsoft, Mandiant, FireEye, Symantec Broadcom, Trend Micro, Check Point Software Technologies, Fortinet, Cisco Systems, Kaspersky Lab, McAfee, Sophos, RSA Security, Varonis Systems, Rapid7, Cybereason, Blue Coat Symantec, Heligan Group, Seceon Inc.

Global Advanced Persistent Threat Protection Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 17.5 billion

- 2026 Market Size: USD 19.4 billion

- Projected Market Size: USD 50.5 billion by 2035

- Growth Forecasts: 11.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Singapore, Australia

Last updated on : 1 May, 2026

Advanced Persistent Threat Protection Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of federal cybersecurity budgets: Rising federal allocations are directly shaping the enterprise procurement cycles for persistent threat detection and response. According to the DHS 2026 data, nearly USD 10.9 billion is allocated for civilian cybersecurity spending, reinforcing the long-term investment in monitoring threat intelligence and Zero Trust architecture. Agencies are required to align spending with the continuous diagnostics and mitigation programs, creating a consistent demand across the contractors and infrastructure operators. Additionally, the federal modernization initiatives emphasize secure cloud adoption and endpoint visibility, pushing enterprises to deploy advanced detection layers. These funding flows cascade into private sector compliance requirements, mainly for defense healthcare and financial services vendors.

- Increasing cyber incident costs: The cyber losses are driving urgency in enterprise security investments. The FBI's April 2024 data indicated that the IC3 reported USD 12.5 billion in cybercrime losses in 2023, reflecting the financial impact of the persistent and targeted attacks. High loss values are pushing organizations to prioritize early detection and continuous monitoring solutions. Moreover, the mandatory reporting requirements for critical infrastructure operators are improving visibility into attack frequency, further influencing the budget allocations. Further rising financial exposure from ransomware and espionage campaigns has accelerated investments in automated detection and response systems, positioning cost mitigation as a key driver for advanced persistent threat protection adoption.

FBI IC3 2023 Internet Crime Report, 2023

|

Category |

2023 Data |

YoY Change (vs 2022) |

|

Total IC3 Complaints |

880,418 |

+10% |

|

Total Financial Losses |

USD 12.5 billion |

+22% |

|

Top State (California) |

80,000 complaints; >USD 2 billion losses |

— |

|

Highest Loss Crime Type |

Investment Scams: USD 4.57 billion |

+38% |

|

Crypto Investment Fraud |

USD 3.94 billion |

+53% |

|

Most Affected Age Group |

30-49 years |

— |

|

FBI San Francisco Division |

USD 400 million losses (investment scams) |

— |

|

Santa Clara County (Investment Fraud) |

446 victims; >USD 152 million losses |

— |

|

Most Reported Crime Type |

Phishing: 298,000+ complaints (34%) |

— |

|

FBI San Francisco (Phishing) |

364 complaints; USD 1.5 million losses |

— |

|

Alameda County (Phishing Losses) |

USD 500,000 losses |

— |

Source: FBI April 2024

- Growth in government led threat intelligence sharing: Public sector initiatives to enhance threat intelligence sharing are boosting the demand for integrated security platforms in the U.S. CISA’s Joint Cyber Defense Collaborative enables real-time information sharing between government and private sector entities. These programs improve visibility into advanced threat actor tactics, techniques, and procedures, driving the adoption of intelligence-enabled detection systems. Similarly, the international collaboration via NATO and allied cybersecurity partnerships is expanding the cross-border intelligence exchange. Enterprises are investing in platforms capable of integrating government-provided threat feeds into their security operations. Moreover, the enhanced intelligence-sharing frameworks are expected to significantly improve detection capabilities, further accelerating demand for advanced persistent threat protection technologies.

Challenges

- Extreme technical complexity: Modern advanced persistent threat attacks no longer confine themselves to single environments they move across identity systems, endpoints, and cloud infrastructure. New manufacturers struggle to develop platforms that can detect and block attacks spanning these domains. The enterprise evaluations demonstrated this challenge, explicitly testing participants against the China state-sponsored group MUSTANG PANDA and criminal group SCATTERED SPIDER in cross-domain scenarios.

- Intense pricing pressures and consumption-based commercial models: Enterprise APT protection pricing has become highly advanced, combining per endpoint fees, consumption-based components, and complex multi-year commitments that disadvantage new players in the advanced persistent threat protection market. Additional charges for data storage create unpredictable expenses that new vendors struggle to structure competitively. For manufacturers entering the market, establishing pricing models that balance affordability and profitability is a substantial roadblock.

Advanced Persistent Threat Protection Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.2% |

|

Base Year Market Size (2025) |

USD 17.5 billion |

|

Forecast Year Market Size (2035) |

USD 50.5 billion |

|

Regional Scope |

|

Advanced Persistent Threat Protection Market Segmentation:

Organization Size Segment Analysis

Under the organization size segment, the large enterprises are dominating and are poised to hold the share value of 71.4% by the end of 2035 in the advanced persistent threat protection market. According to the World Economic Forum, January 2026 data, nearly 45% of all CEOs from the private sector have the ability to respond to major cyber incidents targeting critical infrastructure. Large enterprises operate complex cross-border digital ecosystems and hold high-value intellectual property, making them prime APT targets. They also face binding operational directives that mandate continuous threat hunting and real-time incident response requirements rarely applied to small businesses. Large enterprises deploy full suite APT platforms that include network traffic analysis and deception technology. This regulatory and threat burden dominates the spending in the advanced persistent threat protection market.

Deployment Mode Segment Analysis

Within the deployment mode, the cloud/SaaS subsegment is dominating the advanced persistent threat protection market. The segment is driven by the instant threat intelligence updates and scales across distributed workforces. According to the Industrial Cyber February 2026 data, CSIA reported blocking 2.62 billion malicious connections across federal civilian networks and an additional 371 million across critical infrastructure networks in a single year. These billions of events, many representing APT command and control traffic, phishing callbacks, and data exfiltration attempts, require real-time inspection, behavioral correlation, and automated blocking that on-premises appliances simply cannot sustain. Moreover, the cloud platforms can replicate the federal government's success in blocking billions of malicious connections annually while countering sophisticated, nation-state-led persistent threats.

Component Segment Analysis

The solutions sub segment is leading in the component segment in the advanced persistent threat protection market. solutions encompass a range of technologies, including network traffic analysis, endpoint detection and response, email and web gateways, sandboxing, and deception technology. Among these, the converged platforms that combine XDR with NTA are emerging as the leading sub-segment due to their ability to correlate across multiple vectors, endpoints, cloud workloads, network flow, and email into a unified view of APT attack chains. As APT groups increasingly employ living off the land techniques and zero-day exploits, organizations favor comprehensive solution suites over standalone tools. Services, including professional and managed offerings, remain essential but hold a smaller revenue share compared to technology-driven solutions.

Our in-depth analysis of the advanced persistent threat protection market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Deployment Mode |

|

|

Organization Size |

|

|

Industrial Vertical |

|

|

Threat Type |

|

|

Technology |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Advanced Persistent Threat Protection Market - Regional Analysis

North America Market Insights

North America is dominating the advanced persistent threat protection market and is expected to hold the regional revenue share of 42.5% by the end of 2035. The region is driven by a mature regulatory environment where the government mandates and industry compliance frameworks jointly shape procurement decisions. The U.S. maintains binding operational directives requiring federal civilian agencies to deploy continuous monitoring and endpoint detection capabilities, and the Department of Defense imposes certification requirements on defense industrial base contractors before contract award. The advanced persistent threat protection market is characterized by centralized procurement through federal programs such as FedRAMP in the US and Shared Services Canada, which consolidate vendor qualification and security certification requirements before agencies can purchase solutions.

The rising incident frequency federal compliance mandates and expanding public sector cyber investments are driving the advanced persistent threat protection market in the U.S. According to the GAO's June 2024 data, the federal agencies reported over 30,659 cybersecurity incidents in 2022, reflecting continued system vulnerabilities. GAO January 2023 data shows 23 federal agencies with significant cybersecurity weaknesses, reinforcing the demand for continuous monitoring and threat detection investments. Moreover, the NLM July 2025 study indicated that more than 725 reportable incidents were recorded in 2023, exposing more than 133 million patient records, highlighting vulnerabilities in regulated sectors. These figures show increasing pressure on enterprises and governments to strengthen detection, response, and threat intelligence, which is driving advanced persistent threat protection market growth.

Cyber Incidents Reported from 2015 to 2021

|

Year |

Incident |

|

2015 |

3,880 |

|

2016 |

1,559 |

|

2017 |

2,004 |

|

2018 |

1,543 |

|

2019 |

1,331 |

|

2020 |

812 |

|

2021 |

948 |

Source: GAO January 2023

The rising incident volumes and increased federal cyber program funding are shaping the advanced persistent threat protection market in Canada. The Walrus March 2026 data reported over 2,000 cyber incidents impacting critical infrastructure organizations, indicating sustained targeting of essential services. The Government of Canada's November 2025 data depicted that USD 48.9 million is allocated over three years to enhance cybersecurity for small and medium-sized enterprises, expanding adoption beyond large enterprises. Additionally, the Government of Canada's October 2024 data noted that 16% of Canada businesses experienced cybersecurity incidents in 2023, with a higher incidence in the finance and healthcare sectors. These figures reflect growing enterprise-level risk exposure and policy-driven adoption of monitoring and threat intelligence systems. Government-led initiatives, regulatory compliance requirements, and increased attack frequency across digital infrastructure continue to support steady demand for advanced persistent threat detection and response capabilities.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the advanced persistent threat protection market and is projected to expand at a CAGR of 14.5% during the assessed period, 2026 to 2035. The region is driven by the rapid digital transformation across government financial services and critical infrastructure sectors. Japan leads with stringent cybersecurity requirements under the Basic Act on Cybersecurity and the Ministry of Economy, Trade, and Industry guidelines for critical infrastructure operators across energy, water, finance, healthcare, and transportation sectors. South Korea operates under the Act on Promotion of Information and Communications Network Utilization and the Personal Information Protection Act, mandating advanced persistent threat detection for telecommunications and financial services.

Rapid digital adoption and a sharp rise in cyber incidents is shaping the advanced persistent threat protection market in India. According to the PIB October 2025 data, over 86% of households are connected to the internet. The country’s expanding digital ecosystem has significantly increased the attack surface. Government data shows cybersecurity incidents rising from 10.29 lakh in 2022 to 22.68 lakh in 2024, indicating escalating threat complexity and frequency. Moreover, the Union Budget 2025 to 2026 allocated USD 95 million for cybersecurity initiatives, strengthening the national detection and response infrastructure. Enforcement actions, including blocking over 9.42 lakh SIM cards and 2.63 lakh IMEIs linked to cyber fraud, highlight active threat mitigation efforts. These developments are driving enterprise and government investment in continuous monitoring, threat intelligence, and advanced detection systems across India.

India Cybersecurity Landscape and Government Initiatives, 2025

|

Category |

Data / Statistics |

|

Internet Penetration |

86%+ households connected |

|

Cyber Incidents Growth |

10.29 lakh (2022) to 22.68 lakh (2024) |

|

Government Budget Allocation |

USD 95 million (2025–26) |

|

Financial Fraud Impact |

USD 45,000 reported (NCRP, Feb 2025) |

|

SIM & Device Blocking |

9.42 lakh SIMs; 2,63,348 IMEIs blocked |

|

Cyber Helpline |

1930 operational |

|

CERT-In Activities |

109 mock drills; 1,438 organizations |

|

Law Enforcement Training |

1,05,796 officers; 82,704 certifications |

|

I4C Actions |

3,962 Skype IDs; 83,668 WhatsApp accounts blocked |

|

Fraud Prevention Savings |

USD 670 million saved (17.82 lakh complaints) |

|

Cybercrime Labs (CCPWC) |

USD 16.2 million; 24,600 personnel trained |

|

Cyber Exercises |

600+ participants (Bharat Cyber Exercise 2025) |

|

Digital Ecosystem Scale |

970M internet users; 1.2B mobile subscribers |

Source: PIB October 2025

Rising cybercrime volumes and coordinated government response frameworks are driving the advanced persistent threat protection market in Singapore. According to the Singapore Police Force, February 2024 data, scam and cybercrime cases increased 49.6% from 33,669 in 2022 to 50,376 in 2023, indicating a rapid escalation in threat activity. Scams accounted for 92.4% of total cases (46,563 incidents), with phishing malware-enabled fraud and investment scams dominating attack vectors. Despite a slight decline in total losses to USD 651.8 million in 2023, the financial impact remains substantial, sustaining demand for advanced detection and response systems. These developments are driving enterprise adoption of continuous monitoring threat intelligence, and incident response solutions across financial services and digital infrastructure sectors.

Europe Market Insights

The advanced persistent threat protection market in Europe operates under harmonized regulatory requirements driven by the NIS2 Directive, which is enforceable across all 27 member states. National governments are transposing NIS2 into local law, with Germany, France, and the UK leading implementation. The healthcare sector faces heightened scrutiny following increased ransomware targeting of hospitals, prompting the European Commission to allocate a billion euros under the EU4Health program for cybersecurity upgrades. The European Union Agency for Cybersecurity publishes technical guidelines for threat detection, incident response, and supply chain security. Member states are establishing Computer Security Incident Response Teams with cross-border coordination mandated under the directive. These regulatory drivers create predictable demand for the APT protection solutions capable of meeting harmonized standards.

Rising federal cybersecurity spending, regulatory enforcement, and the increasing incident reporting are shaping the advanced persistent threat protection market in Germany. The Federal Office for Information Security 2023 data reported over 70 new software vulnerabilities identified daily, highlighting the expanding attack surface. Germany’s federal budget allocated USD 10 billion for cybersecurity and digital security programs as per ITA August 2025, reinforcing investments in threat detection and resilience. Moreover, the increase in malware variants observed reflects growing advancements in cyber threats. These trends are driving enterprise and public sector adoption of continuous monitoring, threat intelligence, and incident response systems, and thus boosting a long-term demand for advanced persistent threat protection solutions.

The rising incident frequency, regulatory enforcement, and public sector investment are fueling the advanced persistent threat protection market in the UK. According to the British Chambers of Commerce 2025 data, nearly 50% of businesses and 32% of charities experienced a cybersecurity breach or attack in the past year. Moreover, the National Cyber Security Centre in November 2023 reported managing 371 nationally significant incidents in 2023, reflecting persistent targeting of critical sectors. The UK government's January 2026 data also committed USD 3.3 billion under the National Cyber Strategy to strengthen the national cyber resilience. These data points indicate sustained demand for advanced monitoring threat intelligence and response capabilities across enterprises and public infrastructure, supported by compliance requirements and increasing attack advancements.

UK Cyber Security Breaches, 2024

|

Category |

Data / Statistic |

|

Businesses Experiencing Breaches |

50% |

|

Charities Experiencing Breaches |

32% |

|

Average Cost per Breach (All Businesses) |

USD 1,530 |

|

Average Cost (Medium & Large Businesses) |

USD 13,750 |

|

Post-Breach Action – Training |

23% |

|

Post-Breach Action – System Updates |

9% firewall; 8% antivirus updates |

|

No Action Taken After Breach |

39% |

Source: British Chambers of Commerce 2025

Key Advanced Persistent Threat Protection Market Players:

- CrowdStrike (U.S.)

- Palo Alto Networks (U.S.)

- Microsoft (U.S.)

- Mandiant (U.S.)

- FireEye (U.S.)

- Symantec (Broadcom) (U.S.)

- Trend Micro (Japan)

- Check Point Software Technologies (Israel)

- Fortinet (U.S.)

- Cisco Systems (U.S.)

- Kaspersky Lab (Russia)

- McAfee (U.S.)

- Sophos (UK)

- RSA Security (U.S.)

- Varonis Systems (U.S.)

- Rapid7 (U.S.)

- Cybereason (U.S.)

- Blue Coat (Symantec) (U.S.)

- Heligan Group (UK)

- Seceon Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- CrowsStrike is a dominant player in the advanced persistent threat protection market, leveraging its cloud native Falcon platform to deliver real-time endpoint detection and response against nation-state and advanced adversary attacks. By integrating AI-driven threat intelligence and behavioral analytics, the company enables proactive threat hunting and automated remediation.

- Palo Alto Networks has cemented its leadership in the advanced persistent threat protection market by embedding APT-focused capabilities into its Cortex XDR and Next Generation Firewall ecosystems. Through the strategic integration of machine learning, sandboxing, and network traffic analysis, the company enables real-time identification of command and control communication. In 2025, the total revenue reached USD 9.22 billion.

- Microsoft has rapidly ascended in the advanced persistent threat protection market by embedding APT detection natively into its Sentinel SIEM and Defender XDR platforms, leveraging Windows, Office 365, Azure, and LinkedIn. Using advanced behavioral modeling and threat intelligence, the company identifies advanced attacker tradecraft. In 2024, the company delivered USD 245 billion of annual revenue.

- Mandiant remains a premier authority in the advanced persistent threat protection market, renowned for its frontline threat intelligence and incident response expertise. The company’s Mandiant Advantage platform operationalizes attack lifecycle data into actionable insights for Google’s Chronicle SecOps suite and native XDR tools.

- FireEye revolutionized the advanced persistent threat protection market with its multi-vector virtual execution engine for real-time signatureless threat detection. By integrating network email endpoint and cloud security with proprietary threat intelligence from Mandiant, the company provides ambulatory zero-day aware protection.

Here is a list of key players operating in the global advanced persistent threat protection market:

The advanced persistent threat protection market is highly competitive, dominated by the U.S.-based cybersecurity giants alongside strong regional players from Europe, Asia Pacific, and the Middle East. The key strategies include integrating AI-driven threat intelligence, zero-trust architectures, and extended detection and response capabilities. Major vendors are actively pursuing mergers and acquisitions to broaden their security portfolios and cloud native offerings. For example, in February 2025, Sophos announced the acquisition of Secureworks. Moreover, the niche firms focus on deception technology and network traffic analysis to detect stealthy nation-state sponsored threats. Strategic partnerships with managed security service providers are also stimulating the global advanced persistent threat protection market penetration, mainly across APAC and Europe.

Corporate Landscape of the Advanced Persistent Threat Protection Market:

Recent Developments

- In April 2026, Heligan Group launched Heligan Strategic Advisory, a specialist risk intelligence and investigations unit that expands the firm's advisory and intelligence services. The new business will provide strategic intelligence and advisory services for companies and investors, alongside due diligence, sanctions analysis, cross-border investigations, dispute support, and digital intelligence.

- In January 2026, Seceon Inc. announced the general availability of aiBAS360™, its innovative Breach Attack Simulation (BAS) platform. Now integrated within the OTM Platform as well as in aiSIEM-CGuard 2.0, aiBAS360 empowers organizations to proactively test their security defenses against Advanced Persistent Threats (APTs) and real-world threat actors through comprehensive attack simulations mapped to the MITRE ATT&CK framework.

- In July 2025, Palo Alto Networks® announced it has completed its acquisition of Protect AI, an innovative leader in securing Artificial Intelligence (AI) applications and models. The acquisition accelerates Palo Alto Networks' commitment to securing the next generation of technology infrastructure, a landscape increasingly defined by the rapid proliferation of AI.

- Report ID: 8550

- Published Date: May 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.