Cyber Threat Intelligence Market Outlook:

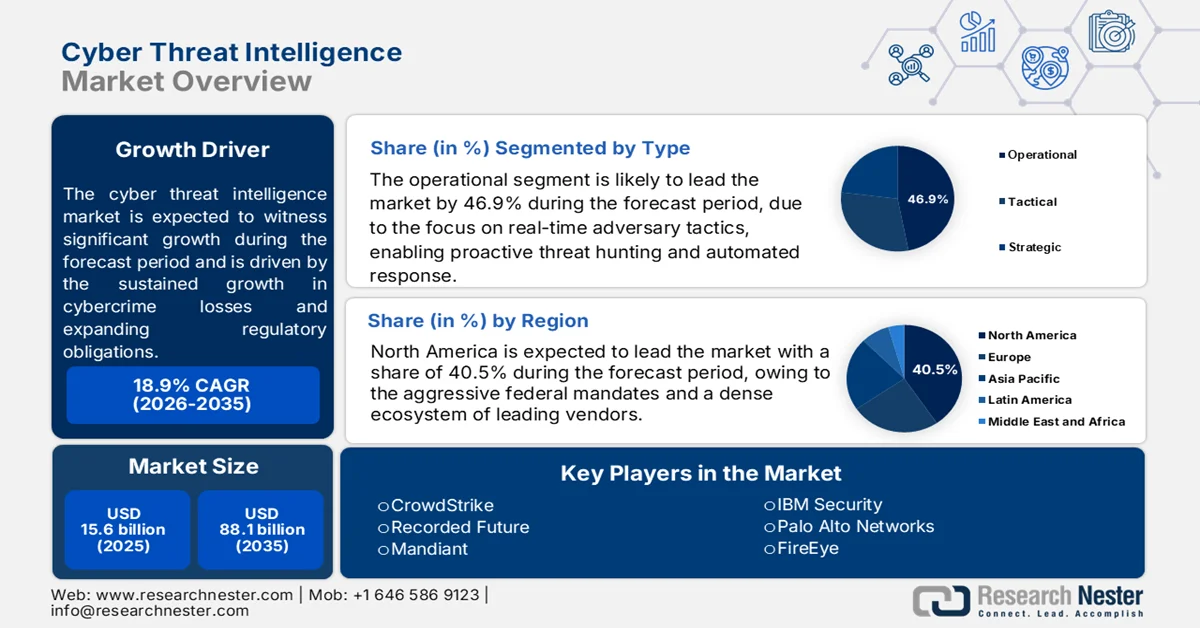

Cyber Threat Intelligence Market size was valued at USD 15.6 billion in 2025 and is expected to reach USD 88.1 billion by the end of 2035, growing at around 18.9% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of cyber threat intelligence is evaluated at USD 18.5 billion.

The cyber threat intelligence market is shaped by sustained growth in cybercrime losses, expanding regulatory obligations, and increased investment in public-private security coordination. Organizations are allocating larger portions of security budgets toward intelligence-led monitoring and risk assessment as attack volumes continue to rise across critical infrastructure, financial services, healthcare, manufacturing, and government networks. According to the IC3 2023 data, the agency received more than 880,418 cybercrime complaints in 2023, with reported losses exceeding USD 12.5 billion, highlighting the growing financial exposure faced by enterprises and public institutions. Government agencies are also strengthening intelligence-sharing frameworks to improve resilience.

Key Cyber Threat Intelligence Market Insights Summary:

Regional Highlights:

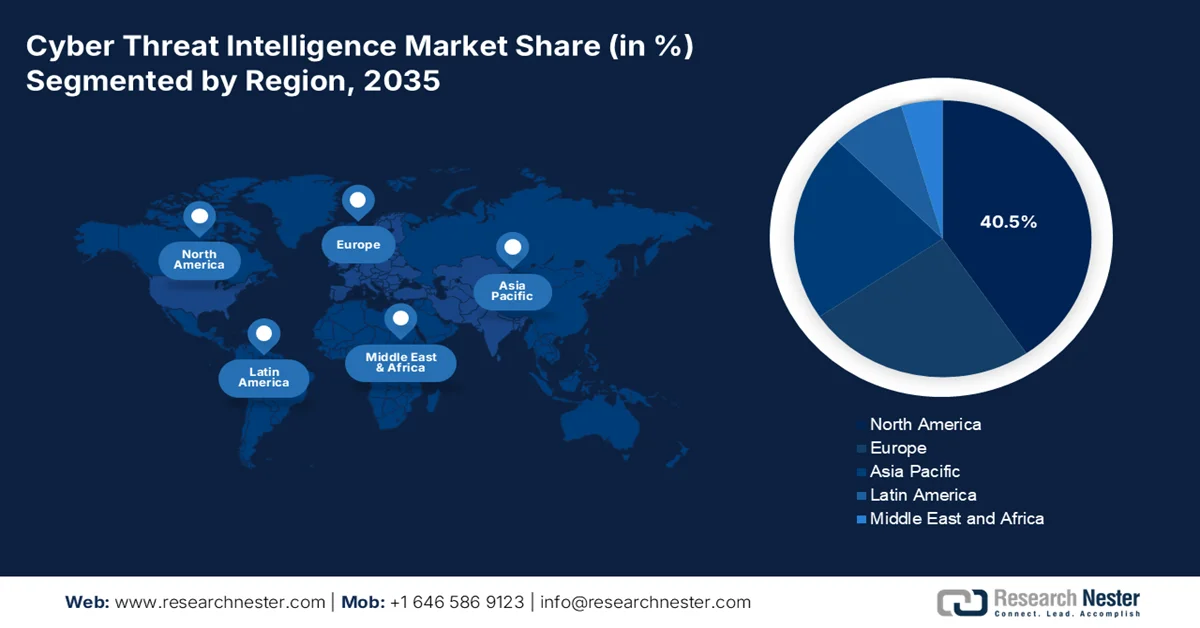

- North America is projected to command 40.5% of the cyber threat intelligence market by 2035, underpinned by aggressive federal mandates, widespread private-sector adoption, and a dense ecosystem of leading vendors

- Asia Pacific is anticipated to witness the fastest expansion in the market during 2026-2035, fueled by rapid digitalization, escalating nation-state cyber activities, and aggressive government mandates across key economies

Segment Insights:

- The Operational segment is expected to account for 46.9% of the cyber threat intelligence market by 2035, supported by real-time adversary tactics, techniques, and procedures that enable proactive threat hunting and automated response

- The Cloud-based segment is poised to maintain its leadership position throughout 2026-2035, catalyzed by growing cloud adoption and increasing demand for scalable, real-time threat detection integrated within cloud environments

Key Growth Trends:

- Rising government cybersecurity budget

- Expansion of critical infrastructure protection programs

Major Challenges:

- Regulatory & compliance hurdles

- High cost of skilled threat analysts

Key Players: CrowdStrike (U.S.), Recorded Future (U.S.), Mandiant (U.S.), IBM Security (U.S.), Palo Alto Networks (U.S.), FireEye (U.S.), Microsoft (U.S.), Rapid7 (U.S.), Anomali (U.S.), LookingGlass Cyber Solutions (U.S.), Kaspersky (Russia), Siemens (Germany), BAE Systems (UK), Orange Cyberdefense (France), NTT Security (Japan), Cyber Security Cloud (Japan), Kordia (Australia), Cisco (U.S.), QuDef (U.S.), Dataminr (U.S.).

Global Cyber Threat Intelligence Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 15.6 billion

- 2026 Market Size: USD 18.5 billion

- Projected Market Size: USD 88.1 billion by 2035

- Growth Forecasts: 18.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, United Kingdom, Germany, Japan

- Emerging Countries: India, South Korea, Singapore, Australia, Indonesia

Last updated on : 8 June, 2026

Cyber Threat Intelligence Market - Growth Drivers and Challenges

Growth Drivers

- Rising government cybersecurity budget: Government cybersecurity expenditure is a major demand driver for cyber threat intelligence platforms and services. Public-sector agencies are increasing investments in threat monitoring, intelligence sharing, and national cyber defense programs as cyberattacks against critical infrastructure intensify. The White House March 2024 data depicted that the budget requested USD 13 billion for civilian cybersecurity investments, including funding for federal network security modernization and threat detection capabilities. As public agencies expand threat intelligence programs, solution providers gain opportunities in intelligence feeds, managed services, and threat analysis platforms supporting national security objectives.

- Expansion of critical infrastructure protection programs: Critical infrastructure protection initiatives are increasing demand for CTI solutions across energy, transportation, healthcare, water, and communications sectors. Governments increasingly require operators of essential services to improve cyber resilience through proactive threat monitoring and intelligence sharing. In the United States, CISA February 2023 oversees 16 critical infrastructure sectors and continues to expand cybersecurity support programs for operators facing escalating threats from nation-state and criminal groups. Organizations must continuously monitor evolving threats and report significant incidents, increasing the need for actionable intelligence. Vendors that integrate operational technology (OT) intelligence with traditional IT threat intelligence are particularly well-positioned to benefit as governments focus on protecting industrial systems and national infrastructure assets.

- Growing public investment in digital government programs: Digital transformation initiatives across governments are expanding attack surfaces and increasing demand for CTI solutions. Governments worldwide are digitizing public services, citizen platforms, taxation systems, healthcare records, and administrative operations. The Open Forum Europe August 2025 data depicts that the Digital Europe Programme allocates approximately €7.5 billion to accelerate digital technologies, including cybersecurity capabilities and cyber resilience projects. CTI solutions support these modernization programs by identifying emerging threats targeting digital services and helping agencies prioritize defensive measures. Vendors that provide intelligence integrated with cloud security, identity management, and government security operations centers are likely to benefit from sustained public-sector digital investment.

Challenges

- Regulatory & compliance hurdles: GDPR, CCPA, and India’s DPDP Act restrict how threat data can be collected and shared across borders. Non-compliance risks fines of a million. Though the global cyber threat intelligence market is expected to grow despite government pricing constraints in the EU public sector. Top companies faced EU-wide restrictions over data localization concerns, forcing it to relocate threat data processing to Switzerland.

- High cost of skilled threat analysts: Entry requires hiring expert threat hunters, malware reverse engineers, and intelligence analysts with salaries. Small suppliers cannot compete. Top company automates analyst workflows using deep learning, reducing human analyst dependency. The global shortage of cybersecurity professionals drives up talent costs, blocking new market entrants.

Cyber Threat Intelligence Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

18.9% |

|

Base Year Market Size (2025) |

USD 15.6 billion |

|

Forecast Year Market Size (2035) |

USD 88.1 billion |

|

Regional Scope |

|

Cyber Threat Intelligence Market Segmentation:

Type Segment Analysis

Under the type segment, operational is leading in the cyber threat intelligence market and is expected to capture the share value of 46.9% by the end of 2035. This sub-segment focuses on real-time adversary tactics, techniques, and procedures, enabling proactive threat hunting and automated response. A multi-layered AI approach allows platforms to develop refined understanding of normal operations while rapidly flagging potential threats. According to the World Journal of Advanced Research and Reviews, May 2025 data, organizations implementing these advanced AI security platforms report a 43% reduction in mean time to detect (MTTD) and a 68% reduction in mean time to respond (MTTR) compared to industry averages. These improvements directly validate operational intelligence's value, as faster detection and response minimize breach impact.

Deployment Mode Segment Analysis

Within the deployment mode, the cloud-based is leading in the cyber threat intelligence market. The shift toward cloud-native CTI platforms mirrors broader cloud adoption trends across industries. As per the NCSES August 2022 data, cloud computing showed an intermediate adoption level, with 54% of non-imputed firms demonstrating digitalization of minimum one business function and the obtaining of minimum one cloud computing service. The 54% adoption baseline creates a ready market for cloud-delivered threat intelligence, as organizations prefer integrating security tools into existing cloud environments. According to NIST's 2024 cloud security study, 68% of federal agencies migrated threat intelligence to the cloud, seeking real-time updates and reduced latency. As more firms digitize functions, cloud-based CTI becomes the natural deployment choice for scalable, real-time threat detection.

Organization Size Segment Analysis

Large enterprises' sub-segment in the organization size leads the cyber threat intelligence market. These organizations operate complex IT infrastructures and face high-volume, targeted attacks requiring dedicated threat intelligence. National-level response capabilities, such as those demonstrated by CERT-In, highlight the scale of threats targeting large enterprises. As per the PIB January 2026 data CERT-In handled over 29.44 lakh cyber incidents, issuing 1,530 alerts, 390 vulnerability notes, and 65 advisories, reflecting large-scale national cyber response capability. This volume of incidents—averaging over 8,000 daily—directly correlates with enterprise attack surfaces. According to DHS's 2022 infrastructure report, 81% of large enterprises maintain dedicated threat intelligence functions, as they face nation-state and ransomware campaigns requiring proactive operational intelligence to achieve rapid detection and response outcomes.

Our in-depth analysis of the cyber threat intelligence market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Deployment Mode |

|

|

Organization Size |

|

|

Application |

|

|

Industry Vertical |

|

|

Threat Source |

|

|

Solution |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cyber Threat Intelligence Market - Regional Analysis

North America Market Insights

North America is dominating the cyber threat intelligence market and is expected to hold the regional revenue share value of 40.5% by the end of 2035. The region is driven by aggressive federal mandates, widespread private sector adoption, and a dense ecosystem of leading vendors. The U.S. leads through binding directives requiring real-time threat intelligence integration across civilian agencies and critical infrastructure, while Canada prioritizes public-private intelligence sharing under its national cyber strategy. Both countries benefit from advanced security operations centers, high cybersecurity spending, and cross-border collaboration through Five Eyes partnerships. Key trends include migration to cloud-based threat intelligence platforms, AI-driven operational intelligence for faster detection, and vertical-specific feeds for healthcare, finance, and energy sectors, reinforcing North America’s dominant position.

The cyber-enabled fraud and advanced digital threats continue to increase across public and private sectors are driving the cyber threat intelligence market in the U.S. According to the FBI April 2026 data, the IC3 received 1,008,597 complaints, up from 859,532 complaints in 2024, with reported losses reaching nearly USD 21 billion. Cryptocurrency-related crimes accounted for more than USD 11 billion in losses across 181,565 complaints, while artificial intelligence-enabled scams generated approximately 22,364 complaints and USD 893 million in losses. These escalating threat levels are encouraging federal agencies, financial institutions, healthcare providers, and enterprises to invest in cyber threat intelligence solutions that improve threat detection, fraud prevention, and incident response capabilities.

The increasing cyber incidents affecting businesses, government agencies, and critical infrastructure operators is shaping the cyber threat intelligence market in Canada. According to the Get Gigs January 2026 data, cybercrime remained the top cyber threat to Canadians, with ransomware continuing to be one of the most disruptive threats to organizations. In addition, the budget 2024 allocated USD 917.4 million over five years to strengthen cybersecurity capabilities and protect critical government systems and essential services. The Government of Canada October 2024 data also reported that 18% of Canadian businesses experienced cybersecurity incidents in 2023, highlighting the need for enhanced threat monitoring and intelligence-driven security measures. These trends are driving adoption of threat intelligence platforms, intelligence-sharing services, and advanced cyber risk management solutions across the Canadian market.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the cyber threat intelligence market. The region is driven by rapid digitalization, escalating nation-state cyber activities, and aggressive government mandates across key economies. Japan, India, South Korea, and Australia lead with active cyber defense laws and compulsory threat intelligence reporting for critical infrastructure. China and Southeast Asian nations (Indonesia, Malaysia, Singapore) are expanding intelligence-sharing frameworks and regional ISACs. Primary trends include cloud-native CTI deployments, localized threat feeds addressing regional language and attack patterns, and public-private partnerships to protect manufacturing, finance, and telecommunications sectors. The region also sees rising demand for managed threat intelligence services due to acute cybersecurity talent shortages.

The digital adoption and cyber risks increase across government, financial services, telecommunications, and enterprise sectors is driving the cyber threat intelligence market in India. According to the PIB October 2025 data, over 86% of households are connected to the internet, significantly expanding the country's digital footprint and security requirements. Cybersecurity incidents increased from 10.29 lakh cases in 2022 to 22.68 lakh cases in 2024, reflecting the growing scale and advancements of cyber threats. To strengthen national cyber resilience, the Union Budget 2025–26 allocated ₹782 crore for cybersecurity projects. Rising cyber fraud activity, combined with government-led cybersecurity initiatives, is accelerating demand for cyber threat intelligence solutions that support threat detection, incident response, fraud prevention, and security operations.

The growing number of cyber incidents and increasingly advanced attack methods are shaping the cyber threat intelligence market in Japan. According to the National Police Agency 2022 data, around 230 ransomware cases were reported in 2022, reflecting a 57.5% increase from the previous year and affecting businesses across a wide range of sectors. Financial cybercrime is also intensifying, with 1,136 online banking fraud incidents resulting in losses of approximately JPY 1.5 billion. Furthermore, the NPA recorded an average of 7,707.9 vulnerability scanning attempts per IP address per day, including attacks targeting connected devices from overseas sources. These developments are driving enterprises to invest in stronger cyber threat intelligence and cybersecurity measures to minimize operational disruptions and financial losses.

Reported Ransomware Cases, 2022

|

Year |

No. of Cases |

|

2020 |

21 |

|

2021 (H1) |

61 |

|

2021 (H2) |

85 |

|

2022 (H1) |

114 |

|

2022 (H2) |

116 |

Source: NPA 2022

Europe Market Insights

The stringent regulatory mandates and cross-border intelligence collaboration is driving the cyber threat intelligence market in Europe. The Digital Operational Resilience Act (DORA) and the NIS2 Directive require financial and critical infrastructure entities to deploy continuous threat intelligence and share incident data within hours. Major economies including Germany, France, Italy, and the UK lead adoption, while Nordic countries emphasize public-private intelligence sharing through sector-specific ISACs. Key trends include demand for compliance-ready CTI platforms with automated reporting, integration with governance frameworks, and growing preference for sovereign cloud-based intelligence solutions to meet EU data residency requirements. Additionally, managed threat intelligence services are gaining traction as organizations address internal skill shortages.

The rising volume of cyber threats and software vulnerabilities is shaping the cyber threat intelligence market in Germany. According to the Federal Office for Information Security October 2024 data, an average of 78 new vulnerabilities were identified every day in 2023, while the agency received approximately 18 zero-day vulnerability reports per month involving IT products from German vendors. The growing threat environment has increased the importance of proactive intelligence and vulnerability monitoring. In addition, a ransomware attack on an IT service provider during the reporting period disrupted approximately 20,000 workplaces across 72 municipalities, affecting services for around 1.7 million people. These developments are driving investment in threat intelligence platforms, cyber monitoring, and incident response capabilities.

The cyber threat intelligence market in UK continues to develop as organizations strengthen cybersecurity capabilities in response to persistent digital threats. According to the Government of UK April 2026 data, 63% of businesses reported experiencing a cyber breach or attack during the year, indicating that cyber risks remain widespread across the economy. At the same time, the information and communication sector demonstrated notable progress, with the proportion of businesses experiencing a cybercrime declining from 43% in 2024/25 to 22% in 2025, suggesting improvements in cyber resilience and defensive measures. Despite these gains, the continued prevalence of cyber incidents is driving organizations to invest in threat intelligence platforms, security monitoring, and proactive risk management solutions to identify emerging threats and protect critical operations.

Key Cybersecurity Indicators, 2025

|

Metric |

Businesses |

|

Organizations experiencing a cyber breach or attack in the last 12 months |

43% (≈612,000 businesses) |

|

Medium businesses experiencing a breach or attack |

65% |

|

Large businesses experiencing a breach or attack |

69% |

|

Phishing attacks experienced |

38% |

|

Phishing identified as most disruptive attack |

69% of affected businesses |

|

Businesses experiencing phishing only (no other attack type) |

51% |

|

Ransomware attacks experienced |

1% |

|

Impersonation attacks experienced |

12% |

|

Organizations reporting negative outcomes after a breach |

19% |

|

Businesses reporting revenue/share value loss from attacks |

5% |

|

Businesses reporting reputational damage from attacks |

3% |

|

Use of updated malware protection |

81% |

|

Secure cloud data backups |

74% |

|

Two-factor authentication deployment |

47% |

|

Businesses using external cybersecurity providers |

44% of micro businesses |

|

Formal cybersecurity strategy in place |

57% of medium businesses; 70% of large businesses |

|

Organizations protecting personal data through encryption/anonymization |

77% |

Source: Government of UK April 2026

Key Cyber Threat Intelligence Market Players:

- CrowdStrike (U.S.)

- Recorded Future (U.S.)

- Mandiant (U.S.)

- IBM Security (U.S.)

- Palo Alto Networks (U.S.)

- FireEye (U.S.)

- Microsoft (U.S.)

- Rapid7 (U.S.)

- Anomali (U.S.)

- LookingGlass Cyber Solutions (U.S.)

- Kaspersky (Russia)

- Siemens (Germany)

- BAE Systems (UK)

- Orange Cyberdefense (France)

- NTT Security (Japan)

- Cyber Security Cloud (Japan)

- Kordia (Australia)

- Cisco (U.S.)

- QuDef (U.S.)

- Dataminr (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- CrowdStrike leverages the cyber threat intelligence market by embedding its Falcon platform with real-time indicators of attack (IoAs) and adversary tradecraft data collected from billions of telemetry events. This intelligence enables proactive threat hunting and automated prevention across endpoints, cloud workloads, and identities. In 2024, the company has made a total revenue of USD 45.3 million.

- Recorded Future dominates the cyber threat intelligence market through its real-time, AI-powered intelligence platform that ingests and analyzes data from the open, dark, and technical web. Its solutions provide predictive threat intelligence, vulnerability prioritization, and security orchestration across SIEMs and SOARs.

- Mandiant brings frontline incident response expertise to the cyber threat intelligence market, transforming years of breach investigations into actionable threat intelligence feeds and verified adversary profiles. Its Intelligence Center delivers strategic, operational, and tactical intelligence, helping organizations understand threat actor motivations, tactics, techniques, and procedures (TTPs).

- IBM Security integrates threat intelligence into its QRadar SIEM and managed security services, leveraging the cyber threat intelligence market to aggregate and correlate data from over 100 global sources, including X-Force Threat Intelligence. IBM’s platform uses cognitive analytics and threat prioritization to reduce alert fatigue and accelerate incident investigation. In 2025, the company has made a revenue growth by 6%.

- Palo Alto Networks embeds threat intelligence from its Unit 42 research team into the Cortex XSOAR and XDR platforms, driving innovation in the cyber threat intelligence market. The company aggregates global threat data, including malware signatures, C2 infrastructure, and phishing indicators, to deliver real-time prevention across the network, cloud, and endpoint.

Here is a list of key players operating in the global cyber threat intelligence market:

The cyber threat intelligence market is highly competitive, driven by demand for real-time, actionable data and AI-driven automation. Key players are adopting strategic initiatives such as integrating threat intelligence with Security Orchestration, Automation, and Response (SOAR) platforms, expanding cloud-native solutions, and leveraging machine learning for predictive analytics. Mergers and acquisitions are common to broaden data sources and geographic reach. For example, in March 2024, Cisco completed the USD 28 billion acquisition of Splunk. Partnerships with MSSPs and government agencies are also intensifying, alongside a push toward open-source intelligence (OSINT) and dark web monitoring. Regional champions are emerging, challenging US dominance by offering localized, industry-specific threat feeds.

Corporate Landscape of the Cyber Threat Intelligence Market:

Recent Developments

- In June 2026, QuDef has announced the launch of SQOUT, a platform which is designed to assess, model, and monitor security risks in Quantum Key Distribution (QKD) and other quantum communication systems as deployments expand across government and enterprise networks.

- In March 2026, Dataminr announced the launch of Dataminr for Cyber Defense, a suite of preemptive threat and exposure solutions that assembles and operationalizes real-time, client-tailored intelligence from first signal to risk-prioritized action.

- In December 2025, NTT DATA announced the launch of 4 next-gen autonomous Cyber Defense Centers powered by AI technologies in Bengaluru, Hyderabad, Noida and Mumbai, with two additional centers set to open in Birmingham (UK) and Dallas (USA).

- Report ID: 8131

- Published Date: Jun 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.