Ransomware Protection Market Outlook:

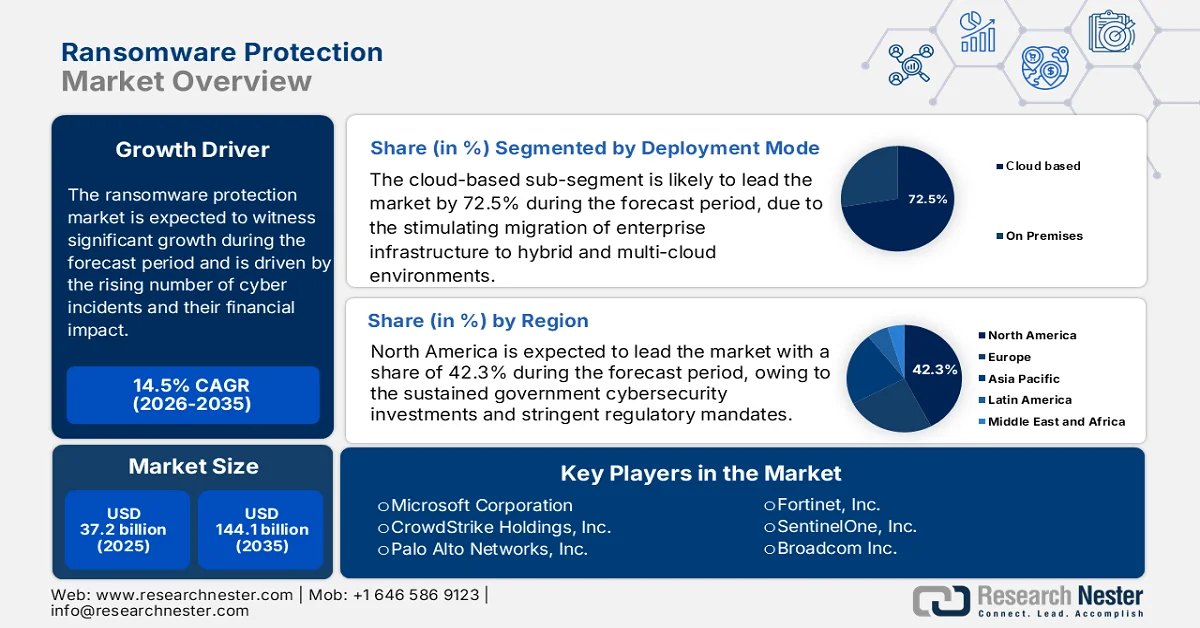

Ransomware Protection Market size was valued at USD 37.2 billion in 2025 and is projected to reach USD 144.1 billion by the end of 2035, rising at a CAGR of 14.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of ransomware protection is estimated at USD 42.6 billion.

The ransomware protection market is driven by the rising number of cyber incidents and their financial impact. The ransomware incidents target the critical infrastructure sector, including healthcare, energy, and government services, disrupting operations and driving mandatory reporting and resilience programs. According to the MEITY July 2023 data, nearly 50% of the global ransomware attacks are targeted at the U.S. Further, the GAO January 2024 data depicts that 14 of 16 critical infrastructure sectors have experienced ransomware attacks in recent years, reinforcing the demand for enterprise-grade protection frameworks. Moreover, the National Institute of Standards and Technology continues to promote the structured cybersecurity frameworks, with adoption increasing across regulated industries to reduce the exposure and ensure compliance. These factors drive the procurement of integrated ransomware protection solutions across large enterprises and public agencies.

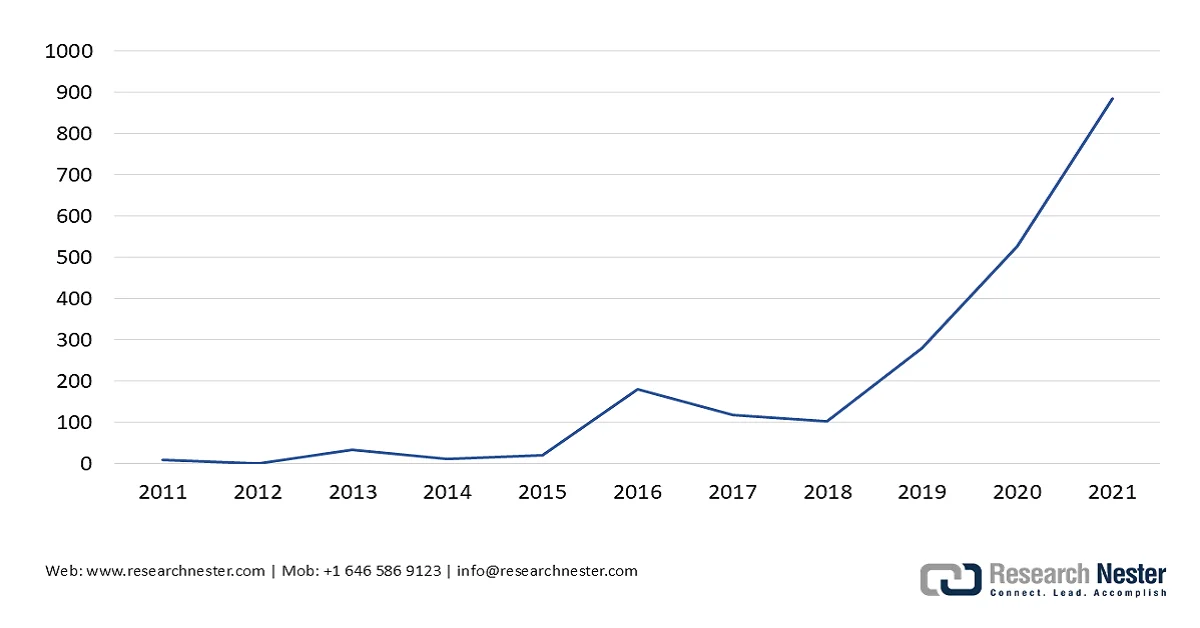

Besides, the intergovernmental and public health organizations underscore the operational risk posed by ransomware to essential services. The WHO reported a fivefold increase in cyberattacks during COVID, with ransomware being a primary vector affecting the healthcare delivery systems. Similarly, the EU also identifies ransomware as one of the top cyber threats, accounting for a significant share of major cybersecurity incidents across the member states, with attack volumes increasing YoY. The GAO January 2024 data depicts that in 2021, reports indicate that the total value of ransomware incidents reached USD 886 million, promoting a higher allocation of IT security budgets toward detection, backup, and incident response capabilities. Additionally, as the regulatory enforcement tightens and reporting requirements expand, organizations are prioritizing long-term investments in ransomware protection to mitigate operational, financial, and compliance risks.

U.S. Dollar Value of Ransomware Incidents (2024)

Source: GAO January 2024

Key Ransomware Protection Market Insights Summary:

Regional Highlights:

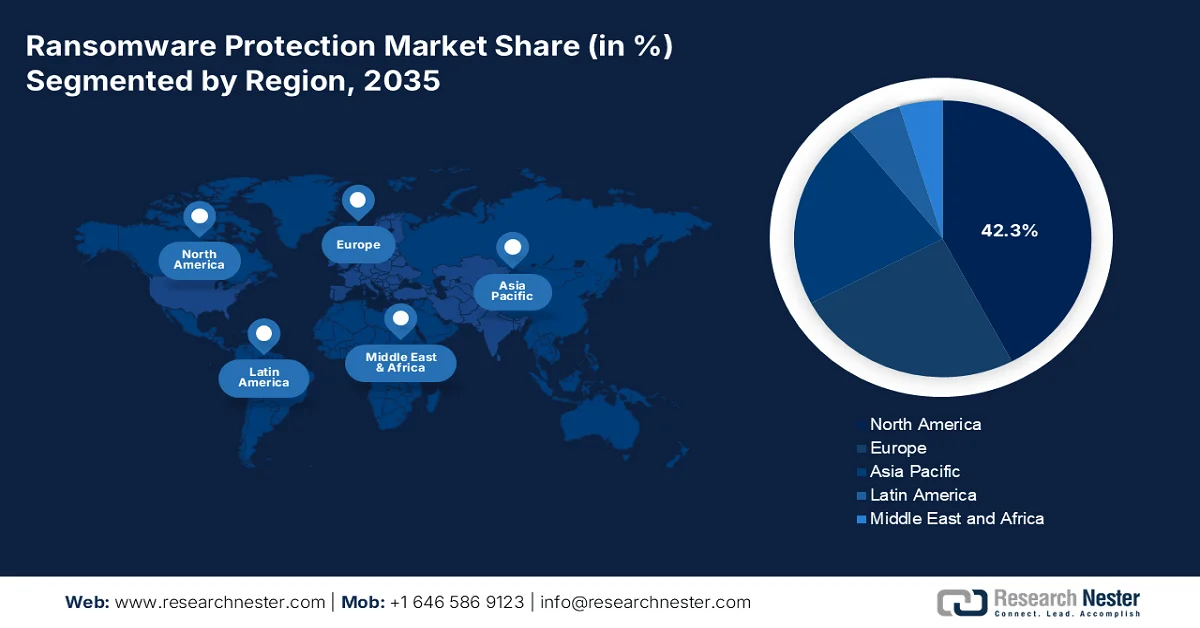

- North America is projected to secure a 42.3% share of the ransomware protection market by 2035, underpinned by sustained government cybersecurity investments and stringent regulatory mandates

- Asia Pacific is anticipated to witness the fastest expansion at a CAGR of 13.5% during 2026–2035, fueled by rapid digital transformation and escalating ransomware attack volumes

Segment Insights:

- In the ransomware protection market, the cloud-based sub-segment under deployment mode is expected to account for a 72.5% share by 2035, propelled by the accelerating migration toward hybrid and multi-cloud environments

- Within the component segment, the solutions sub-segment is poised to dominate by 2035, impelled by rising ransomware incidents driving demand for advanced automated threat detection and response technologies

Key Growth Trends:

- Expansion of federal cybersecurity budgets

- National cybersecurity strategies

Major Challenges:

- Advancements in cyber-attacks

- High technology barrier

Key Players: Microsoft Corporation (U.S.), CrowdStrike Holdings, Inc. (U.S.), Palo Alto Networks, Inc. (U.S.), Fortinet, Inc. (U.S.), SentinelOne, Inc. (U.S.), Broadcom Inc. (Symantec) (U.S.), Cisco Systems, Inc. (U.S.), Trend Micro Incorporated (Japan), Sophos Group plc (UK), Check Point Software Technologies Ltd. (Israel), Acronis International GmbH (Switzerland), Bitdefender (Romania), ESET, spol. s r.o. (Slovakia), Kaspersky Lab (Russia), CyberArk Software Ltd. (Israel), ColorTokens (U.S.), PureID (U.S.), Halcyon (U.S.), Arctic Wolf (U.S.), Veeam Software (U.S.).

Global Ransomware Protection Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 37.2 billion

- 2026 Market Size: USD 42.6 billion

- Projected Market Size: USD 144.1 billion by 2035

- Growth Forecasts: 14.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 1 April, 2026

Ransomware Protection Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of federal cybersecurity budgets: Government budget allocation remains a primary demand driver for the ransomware protection market across enterprise vendors and service providers. According to the White House 2025 data, the U.S. federal cybersecurity budget exceeded USD 13 billion in 2025, reflecting a sustained prioritization of threat detection, zero-trust architecture, and ransomware resilience programs across civilian and defense agencies. The Cybersecurity and Infrastructure Security Agency continues to channel investments into ransomware readiness initiatives, including incident response capabilities and infrastructure protection. This level of spending directly influences the enterprise procurement standards, as federal frameworks often cascade into private sector compliance requirements, mainly in regulated industries such as finance and healthcare.

- National cybersecurity strategies: Government-led cybersecurity strategies are shaping the enterprise investment priorities and stimulating the ransomware protection adoption. The National Cybersecurity Strategies mandate stronger accountability for organizations handling critical data and promote the adoption of secure-by-design systems. Similarly, countries across Europe and Asia are implementing national frameworks requiring organizations to enhance their cyber resilience. These strategies are not only regulatory but also backed by public funding and incentives for implementation. Enterprises are responding by increasing cybersecurity budgets to align with national standards, mainly in sectors subject to audits and compliance checks.

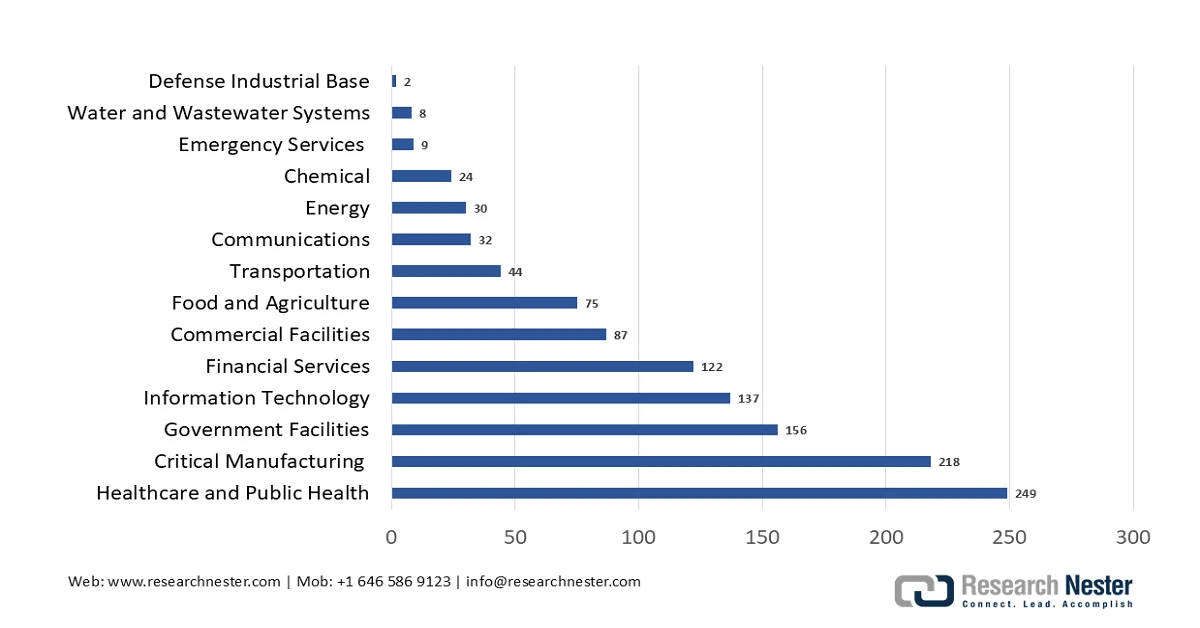

- Growth in cybercrime reporting: Rising ransomware incidents and associated financial losses are promoting governments to expand law enforcement funding and cybercrime response capabilities. The FBI’s Internet Crime Complaint Center 2023 data reported USD 59.6 million in ransomware-related losses, registered with broader economic impacts significantly higher due to downtime and recovery costs. This has led to increased funding for cybercrime investigation units and international cooperation programs. Moreover, healthcare is leading with major ransomware-affected cases. Governments are investing in awareness campaigns and incident reporting systems, boosting the organizations to strengthen their internal defenses. These measures are driving the market.

Sectors Affected Ransomware (2023)

Source: FBI’s Internet Crime Complaint Center 2023

Challenges

- Advancements in cyber-attacks: Cybercriminals continuously develop more advanced technique pushing the vendors into a perpetual cycle of innovation. The emergence of ransomware as a service has lowered the barrier to entry for attackers while increasing the complexity of defense. The entrants must defend against polymorphic malware fileless attacks and malware designed to terminate or blind endpoint security solutions. New vendors in the ransomware protection market must invest heavily in behavioral analysis and AI-driven detection to counter such rapidly advancing threats.

- High technology barrier: Developing a proprietary, effective cybersecurity engine requires extraordinary technical expertise and resources. A functional solution demands a high-performance scan engine with real-time signature-based and behavioral analysis capabilities, plus decloaking functions and minimal false positives. Further, the vendors in the market must build a scalable management console and a threat lab to analyze new cyberthreats registered daily. Very few companies have successfully developed their own scan engine from scratch.

Ransomware Protection Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

14.5% |

|

Base Year Market Size (2025) |

USD 37.2 billion |

|

Forecast Year Market Size (2035) |

USD 144.1 billion |

|

Regional Scope |

|

Ransomware Protection Market Segmentation:

Deployment Mode Segment Analysis

Under the deployment mode segment, the cloud-based sub-segment is leading and is expected to hold the share value of 72.5% by the end of 2035 in the ransomware protection market. The segment is driven by the stimulating migration of enterprise infrastructure to hybrid and multi-cloud environments. Organizations prefer cloud-delivered security for its inherent scalability, reduced capital expenditure, and the ability to provide consistent protection across distributed workforces without the complexity of managing on-premises hardware. According to the Government of the UK, January 2026 data shows that nearly 65% of businesses are using cloud computing, which correlates with the increased adoption of cloud-based security solutions, as organizations nowadays prioritize agile, centrally managed defenses against ransomware.

Component Segment Analysis

Within the component segment, the solutions sub-segment is leading in the ransomware protection market, reflecting the organizational preference for acquiring dedicated software and hardware assets over outsourced service management. This segment encompasses critical technologies such as endpoint detection and response, extended detection and response, email security gateways, and network sandboxing, all of which provide automated, real-time prevention and remediation capabilities. Enterprises favor these solutions because they offer granular control, deep integration with existing IT infrastructure, and the ability to autonomously contain threats at machine speed, significantly reducing the reliance on manual intervention. The NLM June 2022 study indicated that ransomware incidents increased by 72%, compelling organizations to invest heavily in advanced solution-based defenses as a primary line of protection against escalating threats.

Organization Size Segment Analysis

The large enterprises segment represents the largest share within the ransomware protection market, attributable to these organizations' extensive attack surfaces, stringent regulatory compliance requirements, and substantial security budgets. Further, the large enterprises operate across multiple geographies with thousands of endpoints, cloud instances, and legacy systems, making them prime targets for advanced ransomware campaigns. Further, they invest heavily in comprehensive security platforms that unify endpoint detection, zero-trust architecture, and automated incident response across their digital ecosystem. According to the World Economic Forum January 2026 data, 45% of the CEO in large organizations reported the ability to respond to cyber incidents, underscoring the strong cybersecurity solution toward advanced ransomware protection solutions.

Our in-depth analysis of the ransomware protection market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Deployment Mode |

|

|

Organization Size |

|

|

Endpoint Type |

|

|

Industry Vertical |

|

|

Technology |

|

|

Security Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Ransomware Protection Market - Regional Analysis

North America Market Insights

North America is dominating and commands the largest ransomware protection market share of 42.3% by the end of 2035. The market is driven by the sustained government cybersecurity investments and stringent regulatory mandates. The region benefits from the concentrated vendor presence, mature cybersecurity infrastructure, and the elevated threat awareness across public and private sectors. The U.S. has allocated significant funding for federal cybersecurity with mandatory zero-trust implementation across federal agencies, driving endpoint detection and response adoption. Key drivers include the mandatory incident reporting frameworks, critical infrastructure protection regulations, and cyber insurance requirements mandating specific security controls. The region continues to prioritize preemptive threat hunting and recovery capabilities over reactive approaches.

The rising scale and financial impact of cyber-enabled crimes reported by federal agencies is driving the ransomware protection market in the U.S. According to the FBI’s Internet Crime Complaint Center 2023 data, investment fraud losses reached USD 4.57 billion in 2023, up 38% from USD 3.31 billion in 2022, with cryptocurrency-related scams increasing by 53% to USD 3.96 billion. Moreover, 21,489 Business Email Compromise (BEC) incidents resulted in losses exceeding USD 2.9 billion, highlighting the growing advancements of email-based intrusion techniques. Over five years, IC3 has received an average of 758,000 complaints annually, underscoring the persistent and widespread nature of cyber threats. These data show that enterprises are increasing their investments in endpoint protection, thus reinforcing demand for integrated ransomware protection solutions.

The increasing cyber incident frequency, rising recovery costs, and proactive government intervention are driving the ransomware protection market in Canada. According to the Government of Canada, January 2026 data, the Canadian Centre for Cyber Security issued 336 pre-ransomware notifications to over 300 organizations, preventing potential attacks and generating estimated savings of up to USD 18 million, demonstrating the tangible value of early threat detection. Moreover, the Government of Canada's January 2026 data depicts that 13% of businesses affected by cybersecurity incidents identified ransomware as the attack vector, indicating a growing share of ransomware-related threats. At the same time, 22% of businesses are investing in cybersecurity training for non-IT staff, reflecting a shift toward organization-wide risk mitigation. These data are driving the sustained demand for outsourced and automated ransomware protection solutions across Canadian enterprises.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the ransomware protection market and is expected to expand at a CAGR of 13.5% during the assessed period, 2026 to 2035. The region is driven by the rapid digital transformation, rising attack volumes, and increasing government intervention across major economies. Governments across the region are implementing mandatory cybersecurity frameworks as digital infrastructure expands and the ransomware incidents targeting critical sectors intensify. On the other hand, India has allocated USD 93.8 million for cybersecurity projects as per the PIB October 2025 data, with the specific allocations for ransomware defense across municipal government and industrial control systems. South Korea’s cybersecurity breaches surged to 26% based on the Yonhap News Agency, with the financial and healthcare sectors being the primary targets. The region’s diverse regulatory landscape, combined with the rapid adoption of cloud, continues to drive the expansion.

The rising cyber incidents and cybersecurity initiatives are driving the ransomware protection market in India. According to the MEITY 2023 data, 53% increase in ransomware incidents in 2022 underscores the growing threat landscape, pushing enterprises to prioritize advanced protection and recovery solutions. The PIB January 2026 data depicts that the nation has handled over 2.94 million cybersecurity incidents in 2025 while issuing 1,530 alerts, 390 vulnerability notes, and 65 advisories, reflecting large-scale national monitoring and response capabilities. Further preventive initiatives, such as the Cyber Swachhta Kendra, have achieved 98% coverage of the digital population, onboarding 1,427 organizations and enabling 8.95 million malware removal tool downloads, indicating widespread adoption of basic cybersecurity hygiene measures. These developments are driving enterprise demand for ransomware protection solutions, thus boosting the market growth.

The ransomware protection market in Japan is driven by a rise in cyber incidents and increasing advancements of attack vectors in the various sectors. According to the National Police Agency 2022 data, nearly 230 ransomware cases were reported, marking a 57.5% YoY increase in incidents. This affects organizations across all sizes and industries. Moreover, the phishing-driven financial fraud is intensifying, with 1,136 online banking fraud cases recorded, resulting in JPY 1.5 billion in losses. Additionally, the NPA has also detected an average of 7,707.9 vulnerability scanning attempts per IP address per day, with a portion targeting IoT devices, which is originating from overseas sources, highlighting persistent external threats. These data are pushing the enterprises to increase the investments in ransomware protection solutions to mitigate operational disruptions and financial losses associated with evolving cyber threats.

Europe Market Insights

The ransomware protection market in Europe is shaped by the stringent regulatory frameworks, rising attack volumes targeting critical infrastructure, and coordinated government investments across member states. The European Union Agency for Cybersecurity reported that ransomware remains the most significant cyber threat to the EU, with attacks increasingly targeting healthcare, energy, and public administration sectors. The government spending across Europe has been stimulated with the European Commission's March 2025 data indicating that the government allocated USD 1.40 billion under the Digital Europe Programme for cybersecurity deployment. Further, the Cyber Resilience Act imposes mandatory security requirements on hardware and software products throughout their lifecycle, creating non-discretionary demand for compliant ransomware protection solutions.

The rising cybercrime incidence, increasing economic losses, and stronger federal cybersecurity investments are shaping the ransomware protection market in Germany. According to Germany’s Federal Ministry of the Interior, June 2025 data, cybercrime cases reached over 131,391 in 2024, reflecting sustained pressure on enterprises to strengthen digital defenses. Moreover, the ransomware remains a dominant threat, with over 70% of organizations experiencing cyberattacks or attempted attacks in recent years, according to the Federal Office of Information Security across the manufacturing and public administration sectors. Further government-backed spending and policy frameworks are expanding as Germany’s federal budget continues to allocate increased funding toward IT security and critical infrastructure protection under national cybersecurity strategies. These developments are driving the enterprise demand for ransomware protection solutions.

The increasing cyberattack frequency, regulatory compliance requirements, and underreporting challenges are driving the ransomware protection market in the UK. According to the UK Government’s January 2025 data, Cyber Security Breaches Survey 2024, 50% of businesses reported experiencing at least one cyberattack, with 6% identifying ransomware as the attack method, indicating a consistent threat presence across the sectors. Further, the ransomware incidents reported to the Information Commissioner’s Office have risen steadily, with 511 incidents recorded in a single quarter, reflecting growing exposure among organizations handling sensitive data. Similarly, 7% of computer misuse incidents were reported in the year ending March 2024, suggesting a substantially larger unaddressed threat landscape. These factors are driving UK enterprises to increase investments in ransomware protection solutions, therefore driving the market growth.

Key Ransomware Protection Market Players:

- Microsoft Corporation (U.S.)

- CrowdStrike Holdings, Inc. (U.S.)

- Palo Alto Networks, Inc. (U.S.)

- Fortinet, Inc. (U.S.)

- SentinelOne, Inc. (U.S.)

- Broadcom Inc. (Symantec) (U.S.)

- Cisco Systems, Inc. (U.S.)

- Trend Micro Incorporated (Japan)

- Sophos Group plc (UK)

- Check Point Software Technologies Ltd. (Israel)

- Acronis International GmbH (Switzerland)

- Bitdefender (Romania)

- ESET, spol. s r.o. (Slovakia)

- Kaspersky Lab (Russia)

- CyberArk Software Ltd. (Israel)

- ColorTokens (U.S.)

- PureID (U.S.)

- Halcyon (U.S.)

- Arctic Wolf (U.S.)

- Veeam Software (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Microsoft Corporation is a dominant player in the ransomware protection market, embedding the advanced security natively into its Windows ecosystem and Microsoft 365 Defender platform. By using vast telemetry AI and automated incident response, the company delivers comprehensive protection that extends across endpoints, identities, and cloud environments.

- CrowdStrike Holdings, Inc. has redefined the ransomware protection market via its cloud native Falcon platform, which unifies next-generation antivirus endpoint detection and response and threat intelligence. By utilizing lightweight agents and AI-driven analytics, the company delivers real-time visibility and proactive threat hunting across enterprise environments. In 2024, the company made a total revenue of USD 3.06 billion.

- Palo Alto Networks, Inc. strengthens the ransomware protection market by integrating security across endpoints, networks, and cloud via its Cortex and Prisma platforms. Using AI and behavioral analytics, the company provides proactive threat prevention, automated investigation, and zero-trust enforcement. This ensures that the organization can detect and block ransomware.

- Fortinet, Inc. advances the ransomware protection market with its security fabric architecture, which delivers deep integration across network endpoint and cloud security. powered by custom security processing units and AI-driven threat intelligence, the company enables real-time inline prevention and automated response to ransomware attacks. In 2024, the company made a revenue of USD 5,955.8 million.

- SentinelOne, Inc transforms the ransomware protection market via its autonomous AI-powered Singularity platform, which unifies endpoint, cloud, and identity protection. By automating threat detection, investigation, and response in real time, the company eliminates the need for manual intervention and delivers unparalleled speed in stopping ransomware attacks.

Here is a list of key players operating in the global ransomware protection market:

The ransomware protection market is intensely competitive and is defined by a shift from standalone antivirus to integrated platforms combining endpoint detection and response, extended detection and response, and zero-trust architecture. The key players are pursuing strategic initiatives such as AI-driven threat intelligence, aggressive mergers and acquisitions to consolidate capabilities, and deep integration with cloud ecosystems. For example, in September 2024, ColorTokens Inc. announced that it had acquired PureID, an innovative startup providing secure identity and access management. Further, the players such as Microsoft and CrowdStrike lead with native platform plays, while specialized vendors such as Sophos and Malwarebytes focus on ease of use and resilience, creating a dynamic landscape where consolidation and innovation occur simultaneously.

Corporate Landscape of the Ransomware Protection Market:

Recent Developments

- In February 2026, Halcyon announced the launch of its Incident Response (IR) Partner Program with Beazley Security and Booz Allen Hamilton. This program integrates Halcyon’s dedicated anti-ransomware platform with the proven expertise of leading IR providers to deliver end-to-end protection against ransomware and data extortion attacks.

- In November 2025, Arctic Wolf announced plans to enhance AuroraTM Endpoint Security with upcoming AI-powered ransomware prevention and rollback capabilities. Through the acquisition of UpSight Security, Arctic Wolf will accelerate the development and future delivery of these features, expanding its ability to protect organizations against ransomware, credential theft, and other advanced endpoint attacks.

- In January 2024, Veeam Software announced the availability of the new Veeam Cyber Secure Program, which combines Veeam’s purpose-built technology with a team of experts to help enterprises prepare for, protect, and recover from ransomware.

- Report ID: 8498

- Published Date: Apr 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Ransomware Protection Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.