Wearable Skin Patch Market Outlook:

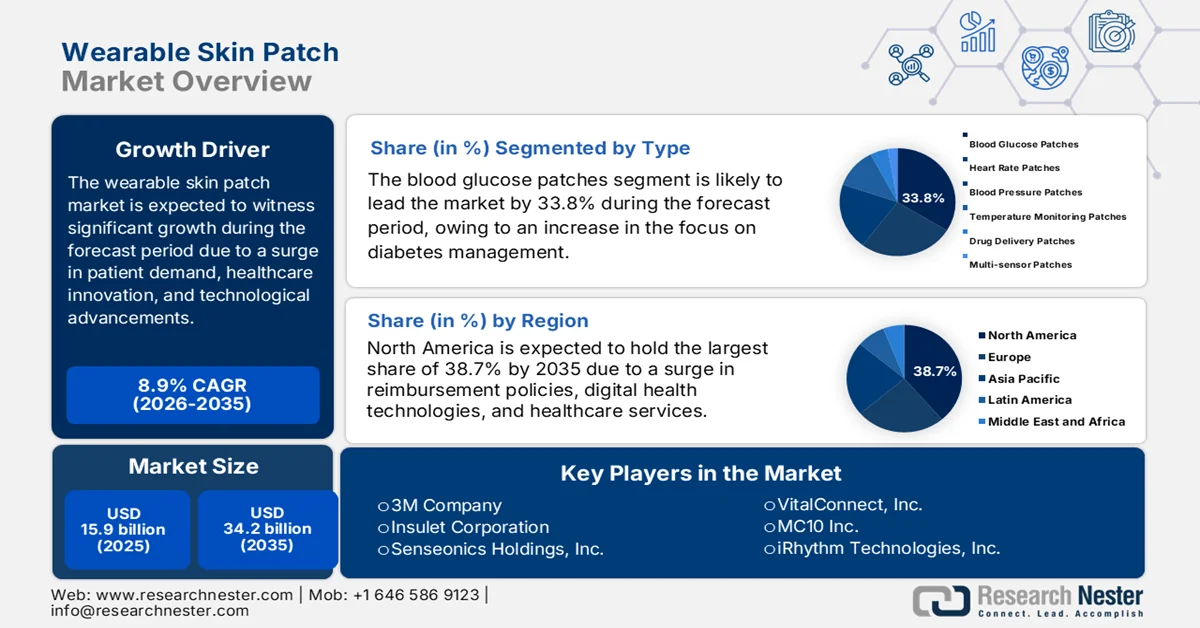

Wearable Skin Patch Market size was over USD 15.9 billion in 2025 and is estimated to reach USD 34.2 billion by the end of 2035, expanding at a CAGR of 8.9% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of wearable skin patch is evaluated at USD 17.3 billion.

The worldwide wearable skin patch market is rapidly evolving, readily shaped by a sudden transition in patient demands, healthcare digitalization, and technological advancements. According to official statistics published by the World Health Organization (WHO) in September 2023, nearly 1 in every 10 patients is significantly harmed in healthcare, and over 3 million deaths occur every year, owing to unsafe care. Additionally, across low-to middle-income nations, as many as 4 in 100 people die from unsafe care. Besides, more than 50% of harm, accounting for 1 in every 20 patients, is preventable, while it has been estimated that as many as 4 in 10 patients are effectively harmed in ambulatory and primary settings. Moreover, up to 80%, which is 23.6% to 85% of this harm, can be avoided by deliberately enhancing the market’s exposure across different nations.

Furthermore, the integration with consumer electronics, miniaturization and ultra-thin designs, expansion into lifestyle and wellness industries, and the presence of subscription-based business models are certain trends that are bolstering the wearable skin patch market globally. As stated in a data report published by the UK Parliament Organization in April 2025, the aspect of physical activity has been associated with 1 in 6 deaths, especially in the UK, amounting to £7.4 billion in expenses. Additionally, increased physical activity tends to persist for at least 6 months, while 32% of the population globally stopped wearing devices after 6 months and 50% after a year. Besides, the Department of Health and Social Care (DHSC) significantly piloted a suitable scheme in Wolverhampton and also engaged over 10% of Singapore’s adult population through wearables, thereby enhancing the market’s demand internationally.

Key Wearable Skin Patch Market Insights Summary:

Regional Highlights:

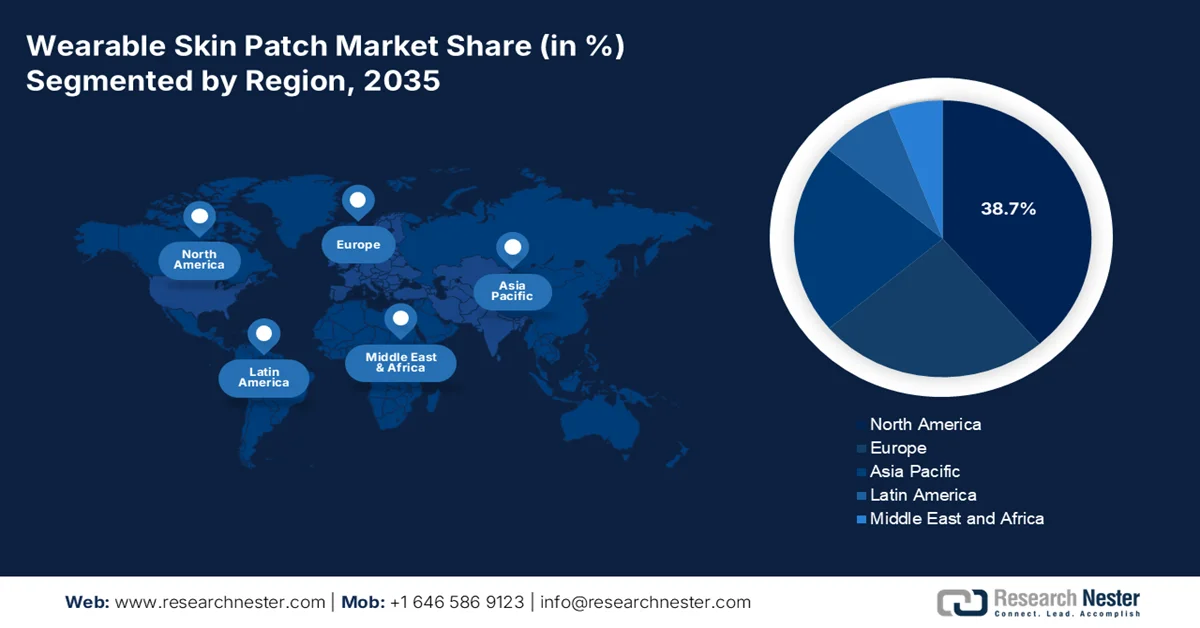

- By 2035, the North America region in the wearable skin patch market is anticipated to command a 38.7% share, owing to the accelerating adoption of digital health technologies, supportive reimbursement frameworks, and a high chronic disease burden.

- Over the forecast period 2026–2035, Asia Pacific is projected to emerge as the fastest-growing region, impelled by rising chronic disease prevalence, government-backed digital health initiatives, and expanding telemedicine integration.

Segment Insights:

- By 2035, the blood glucose patches sub-segment under type in the wearable skin patch market is projected to account for a 33.8% share, propelled by its critical role in diabetes management through continuous, needle-free, and real-time glucose monitoring.

- Over the forecast period 2026–2035, the chronic disease management segment within application is expected to secure the second-largest share, driven by the expanding adoption of wearable skin patches that enable proactive and daily monitoring of long-term conditions.

Key Growth Trends:

- Rise in the aging population

- Expansion in digitalized health facility

Major Challenges:

- Regulatory and compliance barriers

- Data privacy and cybersecurity risks

Key Players: Abbott Laboratories (U.S.), Dexcom Inc. (U.S.), Medtronic plc (Ireland), Koninklijke Philips N.V. (Netherlands), Johnson & Johnson (U.S.), Boston Scientific Corporation (U.S.), GE Healthcare (U.S.), Nitto Denko Corporation (Japan), L’Oréal Group (France), Smith & Nephew plc (UK), 3M Company (U.S.), Insulet Corporation (U.S.), Senseonics Holdings, Inc. (U.S.), VitalConnect, Inc. (U.S.), MC10 Inc. (U.S.), iRhythm Technologies, Inc. (U.S.), Biotricity Inc. (Canada), ResMed Inc. (Australia), Kakao Healthcare (South Korea), Cipla Ltd. (India)

Global Wearable Skin Patch Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 15.9 billion

- 2026 Market Size: USD 17.3 billion

- Projected Market Size: USD 34.2 billion by 2035

- Growth Forecasts: 8.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Canada, Australia

Last updated on : 18 February, 2026

Wearable Skin Patch Market - Growth Drivers and Challenges

Growth Drivers

- Rise in the aging population: The international demographic transition is increasing the need for continuous monitoring solutions, since the elderly population is facing increased chronic disease risks. According to official statistics published by the WHO in October 2025, 80% of older people are projected to reside across low- and middle-income nations by the end of 2050. In addition, the proportion of the world’s population more than 60 years old is poised to almost double from 12% to 22%. Besides, by the end of 2030, 1 in 6 people in the world is expected to be over 60 years of age, and the number of persons aged more than 80 years is anticipated to triple by the end of 2050 and reach 426 million, thereby denoting a huge growth and expansion opportunity for the wearable skin patch market globally.

- Expansion in digitalized health facility: The presence of national health programs has resulted in generous investment in digital health platforms and telemedicine, thus creating a suitable ground for the wearable skin patch market integration. As per an article published by OECD in November 2023, there is a huge opportunity for investments in digital strategy to effectively generate potential returns of USD 3 for USD 1 of investment. Moreover, significant estimates in the U.S. have demonstrated that fragmented care tends to increase the payer’s pricing by more than USD 4,000 per patient. Besides, patients usually spend less time in acute care when providers save time between viewing and requesting external records. Meanwhile, digital health significantly contributed to lower expenses by USD 1,187 per patient, while gaining better health results, thus proliferating the market’s growth.

- Increased innovation in biomarker: The aspect of innovations in biosensing technology is enabling patches to successfully detect a comprehensive range of biomarkers, further extending applications from glucose monitoring to infectious and oncology disease tracking. Based on government estimates published by the PIB Government in February 2026, the 2026-2027 Union Budget effectively proposed the Biopharma SHAKTI with an outlay of Rs. 10,000 crores for more than 5 years. This is aimed at strengthening India’s ecosystem for the production of biosimilars and biologics. In addition, the initiative aligns with the intention of transforming the country into a notable international biopharma industry and grabbing 5% of the worldwide biopharmaceutical market share, thus boosting the wearable skin patch market.

Challenges

- Regulatory and compliance barriers: The wearable skin patch market faces significant regulatory hurdles, particularly in securing approvals from agencies such as the FDA in the U.S., EMA in Europe, and regional health authorities. These patches often combine medical device functionality with digital health applications, requiring dual compliance with medical device regulations and data privacy laws. The complexity of clinical trials, safety validation, and cybersecurity standards delays product launches and increases costs. Moreover, evolving regulations around AI-enabled diagnostics and data interoperability add uncertainty for manufacturers. Companies must invest heavily in compliance infrastructure, which can slow innovation and limit smaller players' entry into the wearable skin patch market.

- Data privacy and cybersecurity risks: The wearable skin patch market is continuously collecting sensitive health data, including glucose levels, heart rate, and blood pressure. This raises concerns about data privacy, cybersecurity, and patient consent. Breaches or misuse of health data can erode consumer trust and trigger legal liabilities under frameworks, such as HIPAA in the U.S. and GDPR in Europe. As patches integrate with telehealth platforms and cloud-based analytics, the risk of cyberattacks increases. Healthcare providers and insurers demand robust encryption, secure interoperability, and compliance with international data protection standards. Addressing these challenges requires significant investment in cybersecurity infrastructure, raising costs and slowing adoption. Therefore, failure to mitigate risks could lead to regulatory penalties and reputational damage, undermining wearable skin patch market growth.

Wearable Skin Patch Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.9% |

|

Base Year Market Size (2025) |

USD 15.9 billion |

|

Forecast Year Market Size (2035) |

USD 34.2 billion |

|

Regional Scope |

|

Wearable Skin Patch Market Segmentation:

Type Segment Analysis

The blood glucose patches sub-segment, which is part of the type segment, is anticipated to hold the largest share of 33.8% in the wearable skin patch market by the end of 2035. The sub-segment’s upliftment is primarily attributed to its importance for diabetes management by offering 24/7, needle-free, and real-time monitoring of sugar levels. According to official statistics published by NLM in April 2025, Abbott’s FreeStyle Libre series comprises a 14-day sensor duration, along with factory calibration that diminishes fingerstick testing. Additionally, with an average absolute relative difference of 9.2% to 9.7%, these waterproof and compact systems readily ensure accuracy for different patient populations. Besides, there is the availability of various continuous glucose monitoring sensors with different features, thereby fueling the sub-segment’s expansion globally.

Continuous Glucose Monitoring (CGM) Sensor Feature Comparative Analysis (2025)

|

CGM Sensor |

Size in cm |

Duration (day) |

Glucose Range (mg/dL) |

Warm-Up Time (Minutes) |

Memory Storage |

Calibration Required |

MARD % |

|

Abbott FreeStyle Libre 3 |

2.1 (diameter*0.28) |

14 |

40 to 500 |

60 |

14 days |

No |

7.9 to 9.4 |

|

Dexcom G7 |

2.7*2.4*0.46 |

10 (12-hour grace period) |

40 to 400 |

30 |

24 hour |

No (optional) |

8.2 to 9.1 |

|

Medtronic Guardian 4 |

6.6*5.1*3.8 |

7 |

40 to 400 |

120 |

- |

No |

10.1 to 11.2 |

|

Caresens Air (i-SENS)/Barozen Fit (Handok) |

3.5*1.9*0.5 |

15 |

40 to 500 |

120 |

12 hours |

Yes (every 24 hours) |

9.4 to 10.42 |

Source: NLM

Application Segment Analysis

By the end of the forecast period, the chronic disease management segment under application is projected to garner the second-largest share in the wearable skin patch market. The segment’s growth is highly fueled by the adoption and development of wearable skin patches, since these devices transform the ailment of slow-progressing and long-lasting conditions from hospital-based and reactive care to daily and proactive monitoring. As per an article published by NLM in July 2024, the urban primary healthcare center in Poland accounts for an estimated 4,000 patients, with 21,700 visits as of 2022. In comparison to this, the rural primary healthcare facility selectively serves a small-scale village in South Poland with nearly 1,200 residents and receives approximately 11,000 patient visits in the same year, thereby denoting an optimistic outlook for the segment’s exposure.

Technology Segment Analysis

The flexible electronics sub-segment is expected to account for the third-largest share in the wearable skin patch market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by enabling patches to conform seamlessly to the human body while maintaining durability and accuracy. Unlike rigid sensors, flexible substrates allow for continuous monitoring of physiological signals such as glucose levels, heart rate, and hydration without causing discomfort. This adaptability is critical for long-term wear, particularly in chronic disease management, where patients require uninterrupted monitoring. Besides, advancements in organic semiconductors, stretchable circuits, and nanomaterials have accelerated the commercialization of flexible patches, thus boosting the segment’s growth.

Our in-depth analysis of the wearable skin patch market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Application |

|

|

Technology |

|

|

Function |

|

|

End use |

|

|

Product Innovation |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Wearable Skin Patch Market - Regional Analysis

North America Market Insights

The North America wearable skin patch market is anticipated to garner the highest share of 38.7% by the end of 2035. The market’s upliftment in the region is highly driven by an increase in the adoption of digitalized health technologies, government reimbursement policies, and robust healthcare technologies. According to official statistics published by the CDC Government in March 2025, chronic diseases, such as diabetes, heart diseases, and cancer, are notable death causes in the U.S., and are also considered leading drivers of the country’s USD 4.9 trillion in yearly healthcare expenses. Besides, among adults aged more than 65 years, over 90% have almost 1 chronic condition. In addition, among midlife adults aged between 35 and 64 years, over 75% have at least 1 condition, thereby enhancing the market’s demand in the overall region.

The wearable skin patch market in the U.S. is growing significantly, owing to the presence of reimbursement policies, federal healthcare expenditure, the increase in monitoring technologies, and focus on chronic disease management. Based on government estimates published by the CMS Government in January 2026, the national health expenditure (NHE) in the country increased by 7.2% to USD 5.3 trillion as of 2024 or USD 15,474 per person, and further accounted for 18.0% of gross domestic product (GDP). Additionally, the Medicare spending also grew by 7.8% to USD 1,118.0 billion in the same year, or 21% of the overall NHE. Meanwhile, the Medicaid spending also surged by 6.6% to USD 931.7 billion in 2024, or 18% of overall NHE. Besides, an increase in other healthcare services and solutions is also suitable for bolstering the market’s demand in the overall country.

Healthcare Solutions Expenditure Growth Analysis in the U.S. (2024)

|

Components |

Growth % |

Expenditure Amount |

NHE % |

|

Private Health Insurance |

8.8 |

USD 1,644.6 billion |

31 |

|

Out of Pocket |

5.9 |

USD 556.6 billion |

11 |

|

Other Third Party Payers and Programs and Public Health Activity |

7.0 |

USD 590.5 |

11 |

|

Hospital Expenditure |

8.9 |

USD 1,634.7 billion |

10.6 |

|

Physician and Clinical Services |

8.1 |

USD 1,109.7 billion |

7.4 |

|

Prescription Drugs |

7.9 |

USD 467.0 billion |

10.8 |

Source: CMS Government

The provision of provincial and federal healthcare investments, an increase in the telehealth integration, industrial associations, and support offering through research and development are readily driving the wearable skin patch market in Canada. Based on government estimates published by the Government of Canada in August 2025, the Parliament Secretary to the Minister of Health notified more than USD 10 million in funding for supporting approaches that tend to empower the population to adopt health behaviors. This includes being active, consuming nutritious foods, and combating smoking, eventually resulting in a long-lasting and optimized life quality. This funding opportunity is extremely crucial for addressing severe chronic conditions, thereby proliferating the market’s demand in the overall country.

APAC Market Insights

The Asia Pacific wearable skin patch market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by a rise in chronic disease prevalence, government-funded strategies, and rapid healthcare digitalization, along with the presence of preventive care programs and telemedicine services. According to official statistics published by Intelligent Hospital in October 2025, there has been an increase in the telemedicine output in China by more than 1.9 times as of 2022. Besides, Singapore has one of the greatest international digital readiness indexes, accounting for more than 2.37 among regional nations. Moreover, the telemedicine service utilization is massively influenced by the region’s diversified demographics, including digital literacy, education, income, and age distribution, along with its more than 4.7 billion population, thus boosting the market’s growth.

The wearable skin patch market in China is gaining increased traction, owing to the aspects of government healthcare digitalization, the presence of a massive patient base, and a domestic manufacturing push. As per an article published by NLM in July 2024, there has been an upsurge in diabetes in the country from less than 1% to 11.2%. Besides, as of 2022, the overall prevalence of the disease among adults, aged between 18 and 79 years, in Beijing eventually increased from 9.6% to 13.9%, along with an annual percentage rate change (APC) of 2.1%. In addition, undiagnosed diabetes surged from 3.5% to 7.2%, along with an APC of 4.1%. However, there has also been a decrease in diabetes treatment and awareness ratios of 1.4%, thereby ensuring a huge growing opportunity for the wearable skin patch market in the overall nation.

The thorough growth in government expenditure, expansion in telemedicine, a rise in chronic disease burden, and the existence of private and public partnerships are readily boosting the wearable skin patch market in India. As stated in an article published by NLM in January 2022, the healthcare system in the country is considered one of the largest health systems internationally, catering to more than 1.3 billion population. Besides, the country comprises more than 5 lakh trained doctors working under the present health system, as well as a massive force of grassroots-level workers, including more than 7 lakh Anganwadi workers, ASHAs, FMPHWs, and ANMs. Additionally, the domestic health infrastructure consists of 1.6 lakh sub-centers, 22,975 PHCs, and 2,935 CHCs, thereby denoting an optimistic outlook for the overall market’s development in the country.

Europe Market Insights

Europe wearable skin patch market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly propelled by a rise in rare disorder prevalence, government-funded healthcare digitalization, the presence of robust regulatory frameworks, and the emphasis on quality standards for wearable and transdermal patches. According to official statistics published by Rare in 2024, rare disorders readily affect a restricted number of people per disease, jointly affecting 1 person in every 17 people within the region. Additionally, an estimated 30 million people in the overall region suffer from a rare disease. However, to combat this condition, the Europe Agency for the Evaluation of Medicinal Products has accepted over 150 orphan drugs, thereby effectively bolstering the market’s demand in the overall region.

The wearable skin patch market in Germany is gaining increased exposure, owing to the presence of reimbursement policies, the integration into chronic disease management programs, and the optimization of preventive care services. As per an article published by NLM in July 2023, the existence of therapies such as acute transcatheter treatment of coronary occlusion in acute myocardial infarction, the advent of notable pharmacological treatments for heart risks, and the implantation of defibrillators in patients with malignant arrhythmias risk led to a decline in cardiovascular mortality by almost 70% for more than past 40 years. Despite this decline, the cardiovascular disease prevalence has significantly upsurged by over 1.5 million cases, thereby denoting a huge growth opportunity for the wearable skin patch market in the country.

The aspects of healthcare modernization, increased support by government budget allocations, and a rise in the demand for non-invasive monitoring solutions, especially for cardiovascular and diabetes conditions, are responsible for boosting the wearable skin patch market in France. As per an article published by the ITA in August 2024, the medical devices industry in the country has been amounted to an estimated turnover of €37.4 billion as of 2023. The industrial turnover for medical devices exported from the country is roughly at €9.5 billion, which is 25% of the overall industry. In addition, the industry is also projected to witness a yearly growth of almost 2% for the upcoming several years. Meanwhile, there exist more than 1,300 medical device organizations in the country, based on which the market in the country is continuously expanding.

Overall Industry Size Analysis for Medical Devices in France (2020-2023)

|

Components |

2020 |

2021 |

2022 |

2023 |

|

Total industry size |

- |

- |

36,742 |

37,476 |

|

Total local production |

- |

- |

33,077 |

33,738 |

|

Total exports |

- |

- |

9,375 |

9,562 |

|

Total Imports |

- |

- |

13,040 |

13,300 |

|

Imports from the U.S. |

- |

- |

4,384 |

4,384 |

|

Exchange rate 1 EUR |

USD 1.14 |

USD 1.18 |

USD 1.09 |

USD 1.08 |

Source: ITA

Key Wearable Skin Patch Market Players:

- Abbott Laboratories (U.S.)

- Dexcom Inc. (U.S.)

- Medtronic plc (Ireland)

- Koninklijke Philips N.V. (Netherlands)

- Johnson & Johnson (U.S.)

- Boston Scientific Corporation (U.S.)

- GE Healthcare (U.S.)

- Nitto Denko Corporation (Japan)

- L’Oréal Group (France)

- Smith & Nephew plc (UK)

- 3M Company (U.S.)

- Insulet Corporation (U.S.)

- Senseonics Holdings, Inc. (U.S.)

- VitalConnect, Inc. (U.S.)

- MC10 Inc. (U.S.)

- iRhythm Technologies, Inc. (U.S.)

- Biotricity Inc. (Canada)

- ResMed Inc. (Australia)

- Kakao Healthcare (South Korea)

- Cipla Ltd. (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Abbott Laboratories is a global leader in continuous glucose monitoring (CGM) through its FreeStyle Libre system, which has set benchmarks in non-invasive wearable skin patch technology for diabetes management. Its strong R&D and FDA approvals position Abbott as a dominant player in chronic disease monitoring.

- Dexcom Inc. specializes in real-time glucose monitoring patches, widely adopted for diabetes care. Its Dexcom G6 and G7 sensors are among the most advanced CGM devices, offering seamless integration with mobile apps and telehealth platforms.

- Medtronic plc is a major medical device company with strong investments in wearable monitoring solutions. Its focus includes diabetes management patches and integration with insulin delivery systems, enhancing patient outcomes through connected care.

- Koninklijke Philips N.V. leverages its expertise in healthcare technology to develop wearable biosensors and patches for patient monitoring. Its solutions are widely used in hospitals and telehealth, supporting remote patient monitoring and chronic disease management.

- Johnson & Johnson invests in wearable medical technologies through its medical devices division, focusing on patches for drug delivery and health monitoring. Its innovation pipeline emphasizes non-invasive solutions aligned with preventive healthcare trends.

Here is a list of key players operating in the global wearable skin patch market:

The international wearable skin patch market is highly competitive, dominated by U.S. players such as Abbott, Dexcom, and Medtronic, alongside strong Europe-based firms, such as Philips and Smith & Nephew. Additionally, Asia-specific companies, including Nitto Denko in Japan and Kakao Healthcare in South Korea, are expanding rapidly, while ResMed in Australia and Cipla in India strengthen regional presence. Strategic initiatives include research and development investments in AI-enabled patches, mergers and acquisitions, and partnerships with telehealth providers. Besides, in December 2025, Intelligent Bio Solutions Inc. notified that it has successfully entered into a non-exclusive tactical alliance and collaboration deal with Vlepis Pty Ltd. This has readily positioned the organization to enter the consumer health monitoring industry, thus bolstering the wearable patch industry globally.

Corporate Landscape of the Wearable Skin Patch Market:

Recent Developments

- In October 2025, Samsung Electronics has leveraged its wearable technology to elevate health management by addressing some of the most severe risks in the present modern healthcare, by ensuring collaboration and innovation.

- In April 2025, Biolinq Incorporated notified a USD 100 million Series C financing that has been led by Alpha Wave Ventures, along with participation from existing investors, including Features Capital, Taisho Pharmaceutical, Aphelion Capital, Hikma Ventures, M Ventures, LifeSci Venture Partners, AXA IM Alts, and RiverVest Venture Partners.

- In February 2025, Epicore Biosystems proclaimed that its significantly raised USD 26 million in Series B funding, led by the Steele Foundation for Hope for driving the international adoption of its cloud analytics and personalized hydration and make expansion into biomarker targets.

- Report ID: 8399

- Published Date: Feb 18, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.