UV Disinfection Equipment Market Outlook:

UV Disinfection Equipment Market size was valued at USD 5.1 billion in 2025 and is projected to account for USD 14.3 billion by 2035, rising at a CAGR of 10.9% during the forecast period 2026 to 2035. In 2026, the industry size of UV disinfection equipment is estimated at USD 5.6 billion.

The UV disinfection equipment market is supported by tightening public health requirements across municipal water treatment, healthcare infrastructure, and industrial sanitation systems. The U.S. Environmental Protection Agency (EPA) continues to enforce microbial control standards under the Safe Drinking Water Act and the Long Term 2 Enhanced Surface Water Treatment Rule, which increased adoption of ultraviolet treatment systems for Cryptosporidium control in municipal utilities. According to the NLM March 2023 study, nearly 1.7 million healthcare-associated infections occur globally every year, contributing to the significant pressure on hospitals and long-term care facilities to strengthen the environmental disinfection protocols. UV room disinfection systems are increasingly being evaluated as supplemental infection control tools in healthcare environments where multidrug-resistant organisms remain a concern.

Besides, in wastewater treatment, the Policy Circle April 2022 reported that nearly 32 billion gallons of wastewater are treated daily in the U.S., creating sustained procurement requirements for tertiary disinfection systems capable of reducing microbial contamination without chemical residues. Industrial demand is also increasing in food processing and pharmaceutical manufacturing, where regulatory agencies require validated sanitation procedures and lower bioburden levels across production environments. Within industrial sectors, semiconductor manufacturing, life sciences, and beverage production facilities are increasing investments in high-purity water systems where ultraviolet treatment is routinely deployed for microbial control and process stability. Public infrastructure modernization, water reuse programs, and hospital infection reduction initiatives are therefore expected to remain core demand drivers for UV disinfection equipment suppliers across municipal and institutional procurement channels.

Key UV Disinfection Equipment Market Insights Summary:

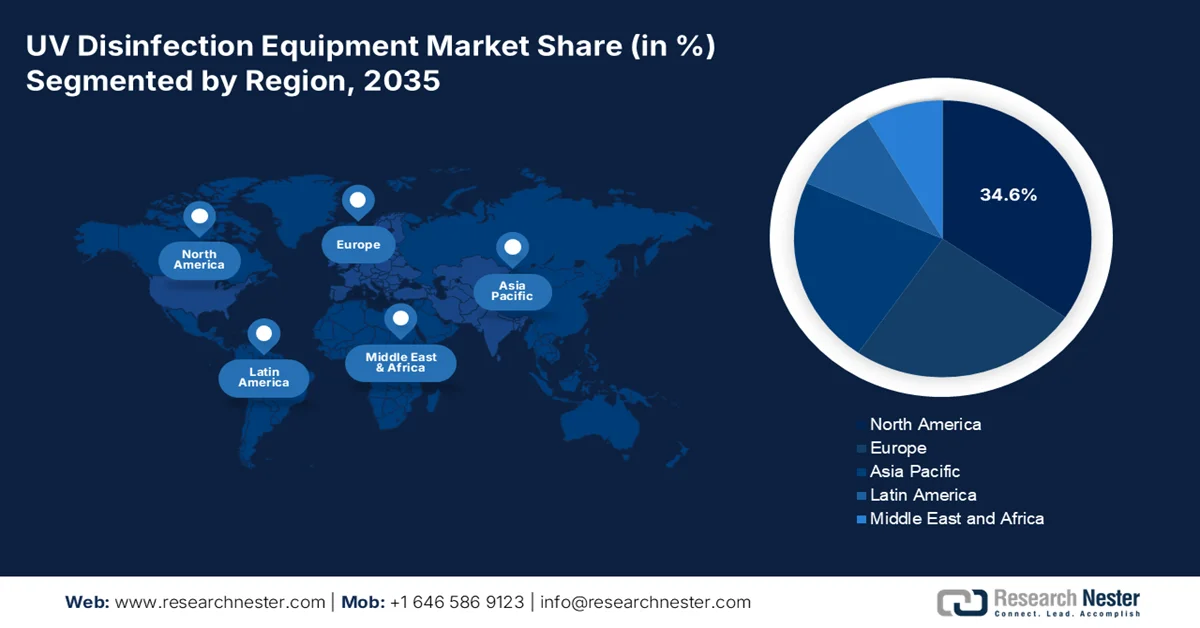

Regional Highlights:

- The North America UV disinfection equipment market is anticipated to command a 34.6% revenue share by 2035, fostered by stringent drinking water regulations and aging water infrastructure requiring upgrades

- Asia Pacific is projected to witness rapid expansion in the market throughout 2026-2035, stimulated by rapid urbanization, industrial growth, and tightening environmental regulations across various nations

Segment Insights:

- Within the UV disinfection equipment market, the UV lamps sub-segment is projected to capture a 39.6% share by 2035, propelled by operational efficiency through continuous monitoring and automated safety controls

- The water and wastewater treatment sub-segment is expected to maintain its dominance in the market during 2026-2035, reinforced by the growing need to inactivate pathogens without harmful chemical usage

Key Growth Trends:

- Expansion of government water infrastructure programs

- Rising healthcare-associated infection (HAI) control spending

Major Challenges:

- Performance uncertainty

- Technical limitations in UV-C LED efficiency

Key Players: Xylem Inc., Aquafine Corporation, Calgon Carbon Corporation, Halma plc, SUEZ Water Technologies & Solutions, ProMinent GmbH, Heraeus Holding GmbH, Kuraray Co., Ltd., Toshiba Corporation, Philips Lighting (Signify N.V.), Aquionics, Atlantic Ultraviolet Corporation, Xenex Disinfection Services, Seoul Viosys Co., Ltd., Clancy Environmental, Evoqua Water Technologies, UV Light Technology, De Nora, Nuvonic, Tekna.

Global UV Disinfection Equipment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.1 billion

- 2026 Market Size: USD 5.6 billion

- Projected Market Size: USD 14.3 billion by 2035

- Growth Forecasts: 10.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (34.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, Canada

- Emerging Countries: India, Indonesia, Malaysia, Singapore, South Korea

Last updated on : 29 May, 2026

UV Disinfection Equipment Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of government water infrastructure programs: Public investment in drinking water and wastewater infrastructure is a primary demand driver for the UV disinfection equipment across the municipal utilities. In the U.S., the Bipartisan Infrastructure Law allocated more than USD 50 billion for the Environmental Protection Agency water infrastructure programs, including the upgrades for drinking water treatment and wastewater reuse systems, as per the EPA April 2026 data. UV systems are increasingly specified in the tertiary treatment stages because utilities are under pressure to reduce microbial contamination while limiting chemical disinfectant byproducts. Europe and Asia are following similar modernization pathways via national sanitation and recycled water programs. The demand for UV disinfection equipment is expected to strengthen further as governments prioritize climate-resilient water treatment assets and stricter public health compliance standards in urban infrastructure projects.

- Rising healthcare-associated infection (HAI) control spending: Healthcare systems are increasing their investments in automated disinfection systems to reduce healthcare-associated infections and antimicrobial-resistant pathogens. According to the U.S. CDC, January 2026 data, about 1 in 31 hospital patients in the U.S. has at least one healthcare-associated infection on any given day. Hospitals are therefore integrating UV-C room disinfection systems into infection prevention protocols, particularly in intensive care units and surgical environments. The World Health Organization estimates that globally, hundreds of millions of patients are affected annually by healthcare-associated infections, increasing pressure on healthcare procurement agencies to deploy supplemental environmental disinfection technologies. Procurement is increasingly linked to measurable reductions in hospital-acquired infection rates and operating efficiency targets.

Challenges

- Performance uncertainty: The UV disinfection equipment industry suffers from inconsistent performance metrics across manufacturers, particularly for UV-C LED products. Different producers quote varying lifetimes, and there is no universal testing protocol for validating the log reduction claims. This lack of standardization creates customer confusion and slows purchasing decisions. New entrants must invest heavily in internal testing, third-party validation, and customer education to overcome skepticism about the product claims, especially when competing against established mercury technologies with decades of operational data.

- Technical limitations in UV-C LED efficiency: UV-C LED technology, while advancing rapidly, still faces technical challenges, including lower wall plug efficiency compared to the mature mercury lamps and significant heat dissipation requirements. High operating temperatures reduce the LED lifespan and output, necessitating complex thermal management systems that increase design complexity and cost. New entrants without specialized expertise in epitaxial growth chip architecture or thermal engineering struggle to develop competitive products, as efficiency directly impacts the Total Cost of Ownership (TCO) that end users evaluate when comparing UV technologies.

Ultraviolet Disinfection Equipment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

10.9% |

|

Base Year Market Size (2025) |

USD 5.1 billion |

|

Forecast Year Market Size (2035) |

USD 14.3 billion |

|

Regional Scope |

|

UV Disinfection Equipment Market Segmentation:

Component Segment Analysis

Within the component segment, the UV lamps sub-segment leads the UV disinfection equipment market and is poised to hold a 39.6% share by the end of 2035. The segment is driven by operational efficiency, triggering automatic cleaning mechanisms or alarm notifications when UV output falls below disinfection thresholds. According to the NIST May 2024 data, 254 nm lamps are highly effective at breaking DNA but require careful positioning to avoid skin and eye damage, often within ventilation shafts. The newer 222 nm Far UVC is safer for occupied spaces but produces ozone, a potential health risk. UV sensors and controllers address both challenges by continuously monitoring wavelength output, detecting ozone levels, and automatically adjusting lamp intensity or activating ventilation. Without these smart controls, facilities cannot safely deploy 222 nm systems in classrooms or elevators. Thus, while lamps provide the energy, sensors and controllers enable safe real-world operation, driving their leading revenue share.

Application Segment Analysis

The water and wastewater treatment stands as the leading sub-segment, driven by the fundamental need to inactivate pathogenic organisms such as Cryptosporidium, Giardia, and viruses without using harmful chemicals. UV radiation penetrates the genetic material of microorganisms, preventing their reproduction and protecting downstream users and the environment. Unlike chlorination, UV disinfection produces no toxic byproducts and requires no chemical storage or handling. Municipal drinking water plants, wastewater reuse facilities, and industrial process water systems rely heavily on UV technology. The effectiveness depends on wastewater clarity, UV intensity, exposure time, and reactor configuration. As water scarcity and stringent effluent regulations grow, water and wastewater treatment globally remains the dominant application for UV disinfection equipment.

Technology Segment Analysis

The UV-C LED is leading the technology segment in the market. As per the NLM April 202 study, the UV-C LEDs use semiconductor junctions doped with aluminum gallium nitride to emit narrow-spectrum UVC (200–280 nm) peaking at 265 nm near the optimal antimicrobial wavelength. Unlike the traditional low-pressure mercury lamps that peak only at 254 nm, LEDs offer the full UVC range. Critically, the Minamata Convention on Mercury, now signed by nearly 140 countries, is phasing out mercury vapor lamps, directly accelerating LED adoption. UV-C LEDs are more robust, flexible, durable, and eco-friendly with instant on/off capability and no hazardous waste. While traditional sources achieve disinfection and sterilization levels, UV-C LEDs are rapidly closing the performance gap, driving their market dominance by 2035.

Our in-depth analysis of the UV disinfection equipment includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Application |

|

|

End user |

|

|

Component |

|

|

Flow Rate |

|

|

Sales Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

UV Disinfection Equipment Market - Regional Analysis

North America Market Insights

North America is dominating the UV disinfection equipment market and is expected to hold the regional revenue share of 34.6% by the end of 2035. The region is driven by the stringent drinking water regulations and aging water infrastructure requiring upgrades. Municipal utilities across the U.S. and Canada adopt UV systems as a chemical-free barrier against chlorine-resistant pathogens. Wastewater treatment plants increasingly specify UV to meet discharge permits without forming harmful disinfection byproducts. Industrial sectors, including pharmaceuticals, food and beverage, and electronics manufacturing, require UV for process water purity. The shift away from mercury-containing lamps toward UV-C LED technology is accelerating, driven by environmental compliance and lower lifetime operating costs. Decentralized UV systems are gaining traction in small communities and remote locations. Real-time monitoring and automated controls have become standard expectations in procurement specifications.

The rising federal investment in water infrastructure modernization and stricter infection prevention initiatives across healthcare and industrial sectors is shaping the market in the U.S. In 2025, the U.S. Environmental Protection Agency (EPA) announced more than USD 2.366 billion via the Drinking Water and Clean Water State Revolving Funds to upgrade municipal water systems, including advanced treatment technologies that support pathogen reduction and water reuse objectives. Additionally, the American Medical Association's April 2025 data reported in 2024 that U.S. national health expenditures reached approximately USD 4.9 trillion, reflecting sustained spending growth across hospitals and healthcare facilities adopting supplemental disinfection systems. Increasing infrastructure replacement activity and hospital sanitation investments continue supporting procurement demand for UV-based disinfection technologies nationwide.

Municipal wastewater modernization projects aimed at improving regulatory compliance, energy efficiency, and long-term treatment reliability are driving the UV disinfection equipment market in Canada. As per the Saint John 2026 data, the City of Saint John’s planned upgrade of the Ultraviolet (UV) Disinfection System at the Millidgeville Wastewater Treatment Facility in New Brunswick is scheduled for 2026. The project is intended to extend facility service life, improve energy efficiency, and maintain compliance with Environment and Climate Change Canada (ECCC) wastewater discharge requirements. Such investments reflect broader infrastructure renewal trends across Canadian municipalities. Moreover, Statistics Canada reported that capital expenditures for water, sewage, and other environmental protection infrastructure reached billions annually, supporting procurement demand for advanced UV treatment systems in municipal and industrial applications nationwide.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035. The region is driven by rapid urbanization, industrial growth, and tightening environmental regulations across various nations. Municipal water and wastewater utilities are adopting UV technology to meet stricter discharge standards and address water scarcity through reuse schemes. Industrial sectors, including electronics, pharmaceuticals, food and beverage, and aquaculture, require UV for process water and effluent treatment. Japan and South Korea lead in UV-C LED innovation, while India and Indonesia focus on cost-effective decentralized systems for rural drinking water. Ballast water treatment regulations boost demand at major ports in Singapore, Malaysia, and China. Emerging concerns over emerging contaminants and chlorine-resistant pathogens are accelerating UV adoption.

Increased government investment in wastewater treatment capacity, industrial water reuse, and public health infrastructure is shaping the market in China. According to the UC Berkley California China Climate Institute, January 2026 data, the national urban sewage treatment rate exceeded 97%, reflecting continued upgrades in municipal treatment systems where ultraviolet disinfection technologies are increasingly deployed for tertiary treatment compliance. Additionally, the large-scale spending on pollution control and water infrastructure projects. Rising industrial production, stricter wastewater discharge standards, and expanding recycled water programs across major provinces continue supporting long-term procurement demand for advanced UV disinfection systems in China.

Key China Economic and Environmental Indicators, 2024

|

Indicator |

2024 Data |

|

Total Water Consumption |

592.5 billion cubic meters |

|

Environmental & Ecological Water Use Growth |

Up 7.8% YoY |

|

Surface Water Quality Compliance |

90.4% of monitored sections achieved Grade I–III quality |

|

Infrastructure Investment Growth |

Up 4.4% YoY |

|

High-Technology Industry Investment |

Up 8.0% YoY |

|

Computer & Electronics Manufacturing Growth |

Up 11.8% YoY |

|

Clean Energy Power Generation |

3,712.6 billion kWh, up 16.4% YoY |

|

Carbon Emissions per GDP |

Down 3.4% YoY |

|

Urbanization Rate |

67.0% |

|

Fixed Asset Investment |

52,091.6 billion yuan, up 3.1% YoY |

Source: The People’s Republic of China February 2025

The Japan UV disinfection equipment market is projected to increase from USD 242.3 million in 2025 to USD 437.4 million by the end of 2035 at a CAGR of 8.9%. In 2026, the market is projected to reach USD 260.5 million. The nation is driven by the strict national water safety regulations and high public sanitation standards. Under Japan’s Water Supply Act, authorities continuously monitor drinking water quality across microbiological indicators, pesticides, organic pollutants, and metal contaminants, driving sustained investment in advanced disinfection infrastructure. According to the OEC 2024 data, Japan has exported nearly USD 186 million worth of UV lamps globally, reflecting as one of the major exporters of the infrared and UV lamp components. Government-led safety initiatives are also supporting the adoption of UV disinfection systems in hospitals, schools, and other public facilities, where operators must comply with stringent hygiene and pathogen-control regulations nationwide.

Europe Market Insights

The Europe UV disinfection equipment market is shaped by the stringent drinking water and wastewater directives, industrial water reuse mandates, and the phase-out of mercury-containing equipment. Municipal utilities across Germany, France, Italy, Spain, and the UK are adopting the UV systems to comply with the revised EU Drinking Water Directive and Urban Wastewater Treatment Directive. Industrial sectors, including the pharmaceuticals, beverage production, and microelectronics, require UV for process water and the disinfection byproduct control. The Nordic countries lead in UV adoption for the municipal drinking water, while Southern Europe focuses on wastewater reuse for agriculture. Russia and Eastern European markets are modernizing aging Soviet era treatment plants with the UV technology.

Rising investment in wastewater treatment, modernization, industrial water reuse, and healthcare sanitation infrastructure is driving the UV disinfection equipment market in Germany. In 2024, Germany’s Federal Statistical Office (Destatis) reported that public expenditure on environmental protection measures continued to increase, supported by municipal investments in water and wastewater management systems. Additionally, the Bundesumweltministerium's February 2026 data stated that over 97% of the population in Germany is connected to public wastewater treatment facilities, creating sustained demand for advanced disinfection technologies capable of meeting strict EU water quality regulations. Growth in pharmaceutical manufacturing, food processing, and public healthcare infrastructure is also supporting procurement of UV treatment systems as operators focus on energy-efficient and low-chemical sanitation solutions across industrial and municipal applications.

The increased investment in water quality improvement, wastewater treatment, modernization, and healthcare infection control infrastructure is driving the market in the UK. The Government of the UK's February 2026 data indicated that the nation has announced more than GBP 104 billion in planned investment by water companies for environmental infrastructure upgrades, including wastewater treatment improvements and pollution reduction projects. Additionally, the OEC 2024 data indicated that the UK has imported nearly USD 45 million of UV components, supporting demand for supplemental disinfection components in hospitals and public institutions. Rising regulatory pressure on sewage discharge management and growing emphasis on sustainable low-chemical treatment processes are driving wider adoption of UV disinfection systems across municipal and industrial sectors.

Imports Data on UV Lamps, 2024

|

Country |

Value (USD million) |

|

Germany |

12.4 |

|

China |

11.9 |

|

Poland |

3.92 |

|

Norway |

2.2 |

|

India |

1.46 |

|

U.S. |

1.61 |

Source: OEC 2024

Key UV Disinfection Equipment Market Players:

- Xylem Inc. (U.S.)

- Aquafine Corporation (U.S.)

- Calgon Carbon Corporation (U.S.)

- Halma plc (UK)

- SUEZ Water Technologies & Solutions (France)

- ProMinent GmbH (Germany)

- Heraeus Holding GmbH (Germany)

- Kuraray Co., Ltd. (Japan)

- Toshiba Corporation (Japan)

- Philips Lighting (Signify N.V.) (Netherlands)

- Aquionics (U.S.)

- Atlantic Ultraviolet Corporation (U.S.)

- Xenex Disinfection Services (U.S.)

- Seoul Viosys Co., Ltd. (South Korea)

- Clancy Environmental (Australia)

- Evoqua Water Technologies (U.S.)

- UV Light Technology (UK)

- De Nora (Italy)

- Nuvonic (Ireland)

- Tekna (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Xylem Inc. is a global leader in the UV disinfection equipment market, offering advanced solutions through its Wedeco brand for municipal wastewater, drinking water, and industrial applications. The company has integrated real-time monitoring and automated control systems into its UV reactors, enabling predictive maintenance and energy optimization. In 2024, the company made a total revenue of USD 8,562 million.

- Aquafine Corporation specializes in high-flow, high-purity UV disinfection systems widely used in pharmaceutical, food and beverage, and semiconductor industries. Within the market, Aquafine differentiates itself through engineered-to-order solutions featuring advanced lamp-out detection, variable intensity control, and validated dose monitoring.

- Calgon Carbon Corporation, a subsidiary of Kuraray, provides UV disinfection equipment primarily for ballast water treatment, drinking water disinfection, and advanced oxidation processes. The company has embedded UV sensor data and flow-paced dosing algorithms into its systems, allowing adaptive treatment based on real-time water quality parameters.

- Halma plc, through its subsidiaries including Aquionics and Berson, is a major player in the UV disinfection equipment market for municipal and industrial applications. The company has pioneered the integration of UV intensity sensors, temperature compensation, and remote telemetry into closed chamber reactors. In 2024, the company made a revenue of USD 2.86 billion.

- SUEZ Water Technologies & Solutions offers comprehensive UV disinfection solutions for drinking water, wastewater reuse, and marine applications. Within the UV disinfection equipment market, SUEZ incorporates real-time UV transmittance and flow rate data into its control platforms, enabling closed-loop dose pacing and remote alarm management.

Here is a list of key players operating in the global UV disinfection equipment market:

The global UV disinfection equipment market is highly competitive, driven by increasing demand for water, air, and surface sanitation across healthcare, municipal, and industrial sectors. Key players are aggressively pursuing strategic initiatives such as mergers and acquisitions, technological innovations in UV-C LED, advanced reactor designs, and geographic expansion into emerging economies. For example, in April 2024, UV Light Technology announced that the company had been acquired by Daro Group Limited. Partnerships with the municipal water authorities and integration of IoT for real-time monitoring are common differentiators. Companies are also focusing on the energy-efficient mercury-free UV systems to comply with environmental regulations. Intense rivalry exists between North America, Europe, and Asia-Pacific manufacturers, each leveraging cost leadership or product differentiation.

Corporate Landscape of the Market:

Recent Developments

- In January 2026, De Nora has introduced the Sentinel® UV systems to deliver advanced, chemical-free drinking water disinfection with validated performance, energy efficiency, compact design, and safe operation.

- In September 2025, Nuvonic has announced the launch of three innovative UV solutions, which is designed to enhance water treatment processes. These UV solutions offer water treatment companies an efficient and cost-effective approach to remote monitoring. They also control municipal wastewater treatment, UV systems, and performance validation of drinking water UV systems.

- In July 2025, Tekna has announced that it has developed AvaUV, which is a cutting-edge UV disinfection technology. We cut the development cycle in half to deliver that helps people to stay safe.

- Report ID: 8511

- Published Date: May 29, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.