Ultra-thin Glass Market Outlook:

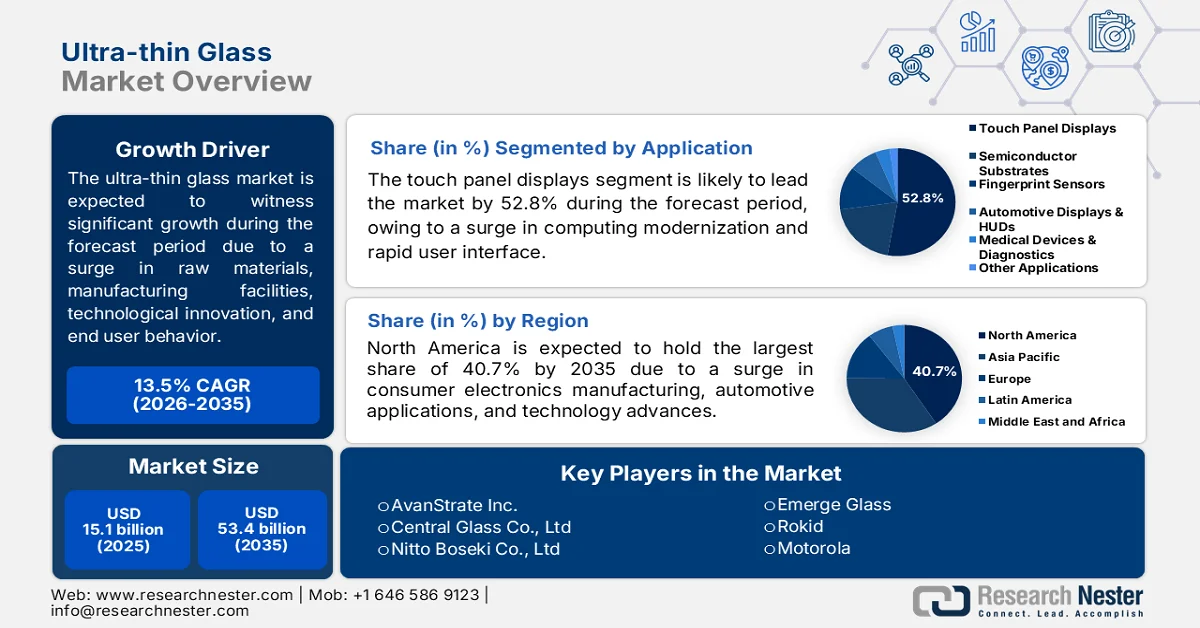

Ultra-thin Glass Market size was valued at USD 15.1 billion in 2025 and is expected to reach USD 53.4 billion by the end of 2035, gradually mounting at a 13.5% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of ultra-thin glass is assessed at USD 17.1 billion.

The global ultra-thin glass market is effectively shaped by a complex interplay of immediate growth factors, including regulatory landscapes, raw material ecosystems, technological advancements, industrial policies, manufacturing infrastructure, and end user behavior. According to official statistics published by the International Finance Corporation (IFC) in 2023, different nations consumed over 194 million tons of glass, and this particular demand is projected to surge to 256 million tons by the end of 2027, demonstrating a compounded 3.5% yearly growth rate. This particular growth is equivalent to 20,000 km of window glass, which is over half the size of Belgium. This also caters to 45% of container glass and 33% of specialty glass, both of which readily account for the largest glass production share. Besides, the continuous glass and glassware supply dynamics are also responsible for positively impacting the market’s enhancement.

Glass and Glassware Global Export/Import Analysis, 2024

|

Countries/Components |

Export (USD) |

Import (USD) |

|

China |

23.4 billion |

5.1 billion |

|

Germany |

7.3 billion |

6.0 billion |

|

U.S. |

6.2 billion |

9.8 billion |

|

Global Trade Valuation |

85.4 billion |

|

|

Global Trade Share |

0.3% |

|

|

Product Complexity |

0.5 |

|

Source: OEC

Furthermore, the biometric authentication integration into glass surfaces, the presence of circular economy mandates for display waste, thermal management glass for over-the-air vehicle updates, and edge sealing for flexible OLED encapsulation are a few trends that are responsible for driving the ultra-thin glass market globally. As stated in an article published by CAPEXIL in 2026, in terms of glass exports to different countries, the U.S. accounts for USD 321 million, which is followed by USD 67.5 million in Spain, USD 51.2 million in France, USD 42.4 million in Nepal, and USD 35.7 million in Brazil. In addition, Germany also caters to USD 34.6 million in glass exports, along with USD 26.2 million in Turkey, USD 24.7 million in Belgium, and USD 24.2 million in Mexico. Therefore, with this continuous increase in export facilities, the ultra-thin glass market is readily expanding worldwide.

Key Ultra-thin Glass Market Insights Summary:

Regional Highlights:

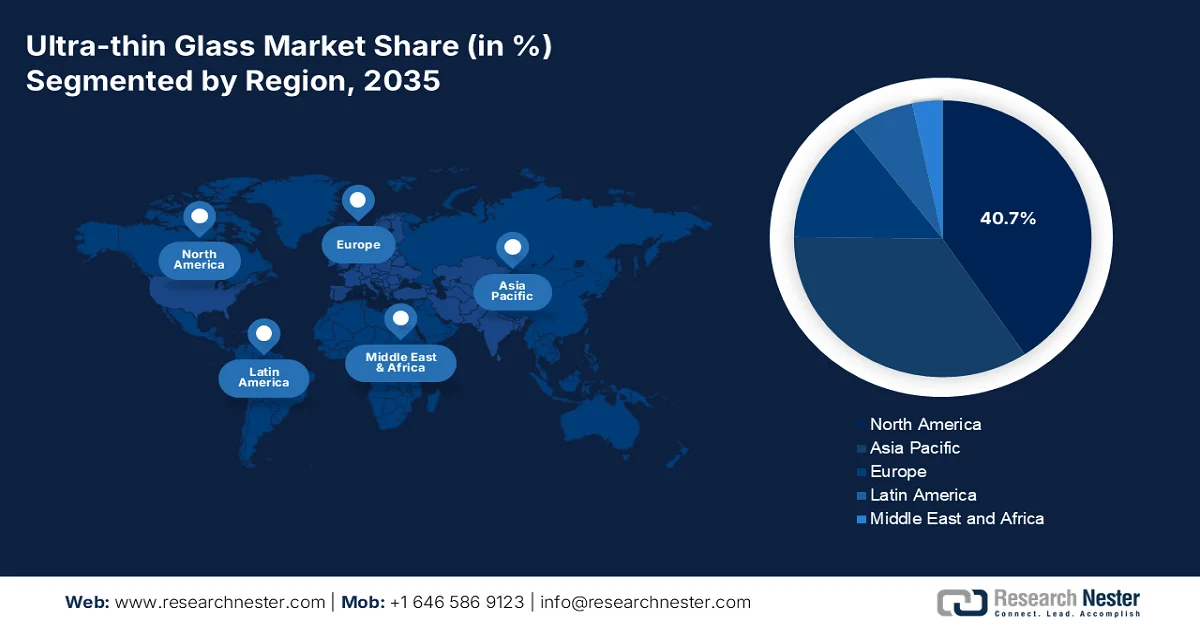

- North America ultra-thin glass market is projected to capture 40.7% share by 2035, bolstered by rising demand for consumer electronics, expanding automotive glazing applications, and the growing adoption of foldable smartphones and wearable devices

- Europe is anticipated to witness the fastest growth in the market throughout 2026–2035, accelerated by technological advancements, stringent sustainability regulations, and increasing adoption of lightweight materials to curb carbon emissions

Segment Insights:

- The touch panel displays sub-segment is expected to account for 52.8% of the ultra-thin glass market by 2035, stimulated by the growing requirement for space-saving, fast, and intuitive user interfaces across multiple industries

- The fusion draw process segment is poised to secure the second-largest share in the market during the forecast period, reinforced by its critical role in producing ultra-thin, defect-free, and high-quality flat glass for advanced display technologies

Key Growth Trends:

- Emissions trading system integration for glass manufacturing

- Secondary display industrial formalization

Major Challenges:

- Manufacturing yield inconsistencies across scale

- Chemical durability degradation in humid environments

Key Players: Corning (U.S.), AGC Inc. (Japan), Schott AG (Germany), Nippon Electric Glass Co., Ltd (Japan), NSG Group (Japan), CSG Holding Co., Ltd (China), Luoyang Glass Co., Ltd (China), Triumph Science and Technology Co., Ltd (China), CNBM (Bengbu) Photoelectric Materials (China), Taiwan Glass Ind. Corp. (Taiwan), Dowoo Insys (South Korea), Samsung Corning Advanced Glass (South Korea), LG Chem Ltd. (South Korea), BOE Technology Group Co., Ltd (China), TCL Technology Group Corporation (China), AvanStrate Inc. (Japan), Central Glass Co., Ltd (Japan), Nitto Boseki Co., Ltd (Japan), Xinyi Glass Holdings Limited (Hong Kong/China), Emerge Glass (India), Rokid (U.S.), Motorola (U.S.), Lenovo (China).

Global Ultra-thin Glass Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 15.1 billion

- 2026 Market Size: USD 17.1 billion

- Projected Market Size: USD 53.4 billion by 2035

- Growth Forecasts: 13.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.7% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Japan, South Korea, Germany

- Emerging Countries: India, Vietnam, Brazil, Mexico, United Arab Emirates

Last updated on : 13 May, 2026

Ultra-thin Glass Market - Growth Drivers and Challenges

Growth Drivers

- Emissions trading system integration for glass manufacturing: The extension of carbon emissions trading systems to focus on glass manufacturing has escalated the ultra-thin glass market adoption. According to official statistics published by the Environmental Engineering Research Organization in 2025, the global glass production constitutes 130 million tons per year. In addition, this production comprises 48% of container glass, 42% of flat glass, and 5% of tableware and other glass products. Besides, an estimated 40 million tons of glass products are estimated to be produced and manufactured in Europe, and meanwhile, the yearly production from the U.S. is found to be 12.3 million tons. Therefore, with these ongoing production facilities, the ultra-thin glass market is rapidly gaining increased exposure.

- Secondary display industrial formalization: The formalization of secondary and tertiary display industries has developed unprecedented volume demand for ultra-thin glass. This has been possible with the smartphone replacement cycle expansion that requires display cover glass for devices. As per a data report published by Columbia University in May 2022, India is a country with a massive potential pool of 550 million feature phone users, which further has the potential to ensure transition to smartphones. Besides, an estimated 97% of the internet users in the country have access through mobile phones. Of this, 40% users are based in rural locations, indicating no restriction of internet access, which in turn, is enhancing the ultra-thin glass market demand for smartphone production.

- Print-on-demand decorative glass platforms: This is a transformative driver for the ultra-thin glass market, readily emerging from the home décor and commercial interiors sector, with the rise of print-on-demand platforms specializing in tempered ultra-thin glass panels. Besides, companies currently operate fulfillment centers where customer-uploaded artwork is digitally printed directly onto 0.5mm to 0.7mm glass sheets using UV-curable ceramic inks, then tempered and shipped within forty-eight hours. This particular model has expanded ultra-thin glass consumption beyond traditional electronics channels into furniture, kitchen backsplashes, office whiteboards, and hotel room wall art. Unlike consumer electronics which requires rigorous quality control for touch sensitivity and optical uniformity, decorative applications accept minor surface variations, allowing manufacturers to repurpose second-grade glass that would otherwise be discarded.

Challenges

- Manufacturing yield inconsistencies across scale: The aspect of transitioning from pilot-line production to mass manufacturing remains the industry's operational nightmare. The fusion draw process, widely regarded as the gold standard for optical-quality glass, becomes exquisitely sensitive to environmental variables when targeting sub-0.1mm thickness. Besides, minute fluctuations in molten glass viscosity, draw speed uniformity, or localized temperature gradients across the isopipe create thickness variations exceeding acceptable tolerances across the same master sheet. Furthermore, edge bead formation, a phenomenon where surface tension pulls glass thicker at sheet boundaries, requires aggressive trimming that wastes significant material, directly eroding profitability in the ultra-thin glass market.

- Chemical durability degradation in humid environments: The ultra-thin glass market faces an accelerated aging crisis when deployed in high-moisture or chemically aggressive environments, a particular concern for automotive interiors and wearable devices worn during exercise. The very property enabling flexibility and reduced thickness simultaneously amplifies glass vulnerability to surface corrosion over time. Ambient water vapor slowly hydrolyzes the glass network, breaking siloxane bonds and leaching network modifiers from near-surface layers, creating a leached layer that weakens mechanical strength. While thicker glass offers enough bulk that surface corrosion remains negligible over product lifetimes, sub-0.1mm glass has no such reserve, and meanwhile, corrosion penetrates a meaningful percentage of total thickness within months rather than years.

Ultra-thin Glass Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

13.5% |

|

Base Year Market Size (2025) |

USD 15.1 billion |

|

Forecast Year Market Size (2035) |

USD 53.4 billion |

|

Regional Scope |

|

Ultra-thin Glass Market Segmentation:

Application Segment Analysis

Based on the application segment, the touch panel displays sub-segment is anticipated to grab the largest share of 52.8% in the ultra-thin glass market by the end of 2035. The sub-segment’s upliftment is primarily driven by its importance for modernizing computing and providing space-saving, fast, and intuitive user interfaces across different sectors. According to official statistics published by NLM in October 2025, there has been an increase in the utilization of touchscreen displays, especially among children aged 8 years, and spending an average of 2.5 hours each day. Based on this, the World Health Organization (WHO) has recommended that parents ensure suitable monitoring of screen time for older children, restricting it to not more than 2 hours per day. Besides, 35% parents are focused on touch display utilization for enhancing young children’s cognitive development and language skills, thus driving the ultra-thin glass market demand globally.

Manufacturing Process Segment Analysis

The fusion draw process segment, part of the manufacturing process, is projected to garner the second-largest share in the ultra-thin glass market during the forecast period. The segment’s growth is highly fueled by its necessity for manufacturing ultra-thin, perfect, and high-quality flat glass, particularly for display technologies. As stated in an article published by the Journal of Cleaner Production in July 2024, the worldwide glass manufacturing process initially utilizes 144 million tons of virgin raw materials, along with 28 million tons of cullet, which is crushed waste glass. This eventually leads to the production of 96 million tons of flat and 97 million tons of container glass products, as well as constitutes the generation of 22 million tons of process emissions, majorly anthropogenic carbon emissions, including carbon dioxides, thus proliferating the segment’s expansion.

Thickness Segment Analysis

By the end of the stipulated timeline, the 0.1 mm-0.5 mm sub-segment, which is part of the thickness segment, is expected to account for the third-largest share in the ultra-thin glass market. The sub-segment’s development is highly propelled by representing the commercial heart of the ultra-thin glass market because it successfully bridges two competing performance requirements: enough structural robustness to survive manufacturing and assembly, yet sufficient thinness to enable the sleek, lightweight device architectures that modern consumers demand. Besides, glass within this band exhibits markedly different handling characteristics in comparison to thinner variants. Additionally, it resists spontaneous warping during transport, maintains flatness necessary for uniform optical coating deposition, and tolerates standard vacuum gripper pick-and-place equipment without microfracture induction.

Our in-depth analysis of the ultra-thin glass market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Manufacturing Process |

|

|

Thickness |

|

|

End use Industry |

|

|

Glass Type |

|

|

Wafer Substrate Innovation |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Ultra-thin Glass Market - Regional Analysis

North America Market Insights

North America in the ultra-thin glass market is anticipated to grab the highest share of 40.7% by the end of 2035. The market’s upliftment in the region is effectively fueled by the sustained demand from consumer electronics manufacturers, an increase in automotive glazing applications, the proliferation of foldable smartphones, wearable devices, and tablets, and the existence of worldwide manufacturing and technology facilities. According to official statistics published by the Pew Research Center in November 2025, 98% of the population in the region effectively owns a different kind of cellphone. In addition, nearly 9 in 10, which is 91%, own smartphones, demonstrating an increase from 35% since the past years. Besides, 99% of the population aged between 18 and 29 years, along with those aged between 30 and 49 years, own a cellphone. Therefore, with this increased utilization of cellphones and smartphones, there is a huge demand for the ultra-thin glass market in the region.

Cellphone and Smartphone Ownership in the U.S., 2005-2025

|

Year |

Cellphone |

Smartphone |

|

2005 |

67% |

- |

|

2006 |

73% |

- |

|

2007 |

75% |

- |

|

2008 |

84% |

- |

|

2009 |

83% |

- |

|

2010 |

82% |

- |

|

2011 |

87% |

35% |

|

2012 |

89% |

45% |

|

2013 |

92% |

58% |

|

2014 |

89% |

59% |

|

2015 |

91% |

69% |

|

2016 |

95% |

77% |

|

2017 |

- |

- |

|

2018 |

95% |

77% |

|

2019 |

96% |

81% |

|

2020 |

- |

- |

|

2021 |

97% |

85% |

|

2022 |

- |

- |

|

2023 |

97% |

90% |

|

2024 |

98% |

91% |

|

2025 |

98% |

91% |

Source: Pew Research Organization

The ultra-thin glass market in the U.S. is growing significantly, owing to the increased demand for durable and lightweight materials for electronic and consumer electronics vehicles, the existence of manufacturing and technology facilities, the rise in electric vehicles, and strong federal funding. As stated in an article published by the Global Electronics Association in November 2025, the electronics manufacturing industry is a powerful economic growth and resilience, effectively supporting 5.2 million regional employment opportunities, significantly contributing USD 853 billion to the gross domestic product (GDP), and also generating USD 1.8 trillion in overall economic output. Based on this growth, the industry is focused on fueling advancement, sustaining high-wage employment, and expanding the supply chain dynamic that underpins national security and worldwide competitiveness, thus proliferating the ultra-thin glass market upliftment.

The strong energy efficiency coupled with cold climate targets, the increased adoption in commercial and residential building windows, organizational collaboration, and strict energy standards are certain factors that are driving the ultra-thin glass market in Canada. As per a data report published by Natural Resources Canada in November 2025, the country’s total energy supply accounts for 81% of fossil fuels, which comprises 30% oil, 28% coal, and 23% natural gas, along with 14% of renewables, and 5% of nuclear. Based on this, direct energy caters to 8.1% of GDP or USD 232 billion, comprising 6% of petroleum, 1.8% of electricity, and 0.3% of others. Meanwhile, the energy indirect accounts for 1.7% of the GDP, which amounts to USD 50 billion, which is positively fueling the market’s exposure in the overall country.

Energy’s Nominal GDP Contribution by Territory/Province, 2024

|

Territory/Province |

GDP (USD Million) |

|

Alberta |

129,551 |

|

British Columbia |

22,778 |

|

Saskatchewan |

20,618 |

|

Ontario |

27,120 |

|

Quebec |

16,201 |

|

Newfoundland and Labrador |

7,178 |

|

New Brunswick |

1,990 |

|

Nova Scotia |

958 |

|

Northwest Territories |

211 |

|

Prince Edward Island |

116 |

|

Yukon Territory |

73 |

|

Nunavut |

70 |

Source: Natural Resources Canada

Europe Market Insights

Europe in the ultra-thin glass market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by technological advancement, strict sustainability regulations, strong demand for key end use industries, increased focus on eco-friendly manufacturing practices, a surge in lightweight materials to reduce carbon emissions, and advanced manufacturing capabilities. According to official statistics published by the Europe Digital Strategy in July 2025, the region invested USD 210.7 million in breakthrough digitalized technologies. This was made possible by the newest approaches of the Horizon Europe Program that bolstered collaborative research and development across the overall region. Besides, the objective of this investment was to develop cutting-edge technologies, thus denoting a huge growth opportunity for the market in the region.

The ultra-thin glass market in Germany is gaining increased traction, owing to the advanced manufacturing capabilities for down-draw and fusion draw processes, a strong automotive industry, with increased focus on electric vehicle manufacturing, government support through the Federal Ministry for Economic Affairs and Climate Action (BMWK), and an increase in flat panel displays. As stated in an article published by the ITA in November 2024, the automotive industry is the country’s largest sector that supports nearly 780,000 employment opportunities. In this regard, the industry generated more than USD 611 billion in overall sales, indicating an over 11% rise from 2022. This growth includes USD 496.3 million for motor vehicles. USD 15.7 million for trailers, and USD 99.8 million for parts and accessories, thus denoting continuous development for the ultra-thin glass market in the country.

The post-Brexit industrial policy for supporting innovative manufacturing industries, the Green Industrial Revolution and Net Zero Strategy, along with a suitable supply chain for specialty glass exports, are a few trends that are proliferating the ultra-thin glass market in the UK. As per an article published by the UK Government in January 2026, the manufacturing industry in the country offers more than 760,000 employment opportunities, along with USD 111.1 billion in yearly gross value added (GVA). In addition, the domestic 10-year approach is projected to almost double business investment in advanced manufacturing to USD 52.8 billion by the end of 2035, which is further backed by USD 5.8 billion in public funding and a worldwide competitive business environment. Therefore, with such development in the upcoming future, there is a huge growth opportunity for the market in the country.

APAC Market Insights

The Asia Pacific in the ultra-thin glass market is projected to experience suitable growth by the end of the stipulated duration. The market’s growth in the region is highly driven by an expansion in smartphone production, commitment to next-generation display technologies, panel display fabrication facilities, sustained industrial demand, and the deployment of 5G and 6G infrastructure. According to official statistics published by the CKGSB Knowledge in January 2026, 6G is expected to emerge as the biggest game changer in the region, and constitutes the potential to generate more than USD 50 billion in the next 5 years of rollout. Besides, in terms of 5G network, China is dependent on ZTE and Huawei for achieving comprehensive deployment at home and effectively boosting globally, thus denoting an optimistic outlook for the market’s growth and expansion.

The ultra-thin glass market in China is gaining increased exposure, owing to the strong manufacturing facility, the largest electronics producer of smartphones, tablets, televisions, and laptops, as well as policies to support semiconductor manufacturing, growth in the automotive industry, and a rise in government investments. As stated in an article published by the ITIF Organization in September 2024, the country’s enterprises’ worldwide liquid crystal display (LCD) production share has successfully reached 72%. Likewise, the share of organic light-emitting diode (OLED) production surpassed 50%. Besides, the domestic share of capital expenditure investments for display technologies accounted for 85%, with domestic organizations predicted to account for more than 90% of capital expenditure, thus enhancing the market’s exposure.

The aspects of the ongoing demand from consumer and industrial electronics, integrated display devices, and computing devices, along with the trade ecosystem, increased reliance on imports, the presence of cost-competitive base glass and specialty raw materials, are certain drivers fueling the ultra-thin market growth in Japan. Besides, the domestic ultra-thin glass industrial size was valued at USD 579 million as of 2025, which is further projected to be worth USD 638.1 million by the end of 2026. In addition, the industry in the nation is also anticipated to reach USD 1,530 million, with a 10.2% growth rate by the end of 2035. This growth is readily supported by localized manufacturing, the spread of digitalization, and increased efforts towards decarbonization, as well as government strategies. Therefore, all these factors are highly supporting market expansion in the overall nation.

Key Ultra-thin Glass Market Players:

- Corning (U.S.)

- AGC Inc. (Japan)

- Schott AG (Germany)

- Nippon Electric Glass Co., Ltd (Japan)

- NSG Group (Japan)

- CSG Holding Co., Ltd (China)

- Luoyang Glass Co., Ltd (China)

- Triumph Science and Technology Co., Ltd (China)

- CNBM (Bengbu) Photoelectric Materials (China)

- Taiwan Glass Ind. Corp. (Taiwan)

- Dowoo Insys (South Korea)

- Samsung Corning Advanced Glass (South Korea)

- LG Chem Ltd. (South Korea)

- BOE Technology Group Co., Ltd (China)

- TCL Technology Group Corporation (China)

- AvanStrate Inc. (Japan)

- Central Glass Co., Ltd (Japan)

- Nitto Boseki Co., Ltd (Japan)

- Xinyi Glass Holdings Limited (Hong Kong/China)

- Emerge Glass (India)

- Rokid (U.S.)

- Motorola (U.S.)

- Lenovo (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Corning leverages its proprietary fusion draw manufacturing process to produce ultra-thin glass substrates with pristine surface quality, making it the preferred supplier for premium consumer electronics brands requiring high durability. The company continuously advances its glass chemistry formulations to improve drop performance and scratch resistance while reducing thickness for next-generation foldable and rollable device architectures.

- AGC Inc. capitalizes on its deep heritage in architectural and automotive glass to offer ultra-thin glass solutions tailored for curved display applications and interior vehicle touch interfaces. The company focuses on developing environmentally sustainable manufacturing methods and halogen-free compositions to meet tightening global regulatory standards for electronic materials.

- Schott AG specializes in ultra-thin glass with extremely low surface roughness and high thermal stability, targeting specialized applications such as semiconductor wafer packaging and biomedical microfluidic devices. The company emphasizes precision down-draw technology that enables tight thickness tolerances critical for optical waveguide and sensor protection layers in high-reliability environments.

- Nippon Electric Glass Co., Ltd directs its ultra-thin glass portfolio toward display cover applications and thin-film transistor backplanes for portable electronics requiring excellent light transmission characteristics. The company invests heavily in automated inspection systems capable of detecting sub-micron defects on glass surfaces moving at high production speeds.

- NSG Group utilizes its global footprint and float glass expertise to produce ultra-thin glass for building-integrated photovoltaic modules and energy-efficient smart window systems. The company integrates surface coating technologies directly into its manufacturing line to deliver functional glass ready for lamination without secondary processing steps.

Here is a list of key players operating in the global ultra-thin glass market:

The ultra-thin glass market remains highly concentrated, with the top five manufacturers collectively commanding the majority of global production capacity. Companies, such as Corning in the U.S., AGC in Japan, and Schott in Germany, maintain technological leadership through proprietary fusion draw and down-draw processes that enable sub-0.1mm thickness with pristine surface quality. Key strategic initiatives include Corning's investment in Gorilla Glass Ceramic nano-crystal technology, Schott's achievement of 30-micron glass with one million-plus fold endurance, and Chinese manufacturers like Triumph Science and CNBM aggressively scaling domestic UTG production to reduce import dependency. Besides, in February 2026, Samsung Electronics notified the expansion of its commercial display offerings, which is led by the introduction of Samsung Spatial Signage. This expansion comprises AI-based content capabilities through Samsung VXT, with the latest additions to its supersized commercial display lineup, thus driving the ultra-thin glass industry globally.

Corporate Landscape of the Market:

Recent Developments

- In January 2026, Rokid unveiled Rokid AI Glasses Style, which is a voice-centric and display-free AI glass, developed for all-day wear by combining an open AI ecosystem, dual-chip, and prescription-first design, along with a robust commitment to global accessibility.

- In November 2025, Motorola introduced the Motorola Edge 70, along with the latest Moto G57 Power, Moto G57, and the Moto Buds Bass that are readily packed in power, style, and durability at different price points.

- In September 2024, Lenovo introduced IdeaPad and New Yoga Devices, effectively designed for empowering consumers with AI technology to enhance creativity and user productivity.

- Report ID: 8566

- Published Date: May 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Ultra-thin Glass Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.