Threat Detection Systems Market Outlook:

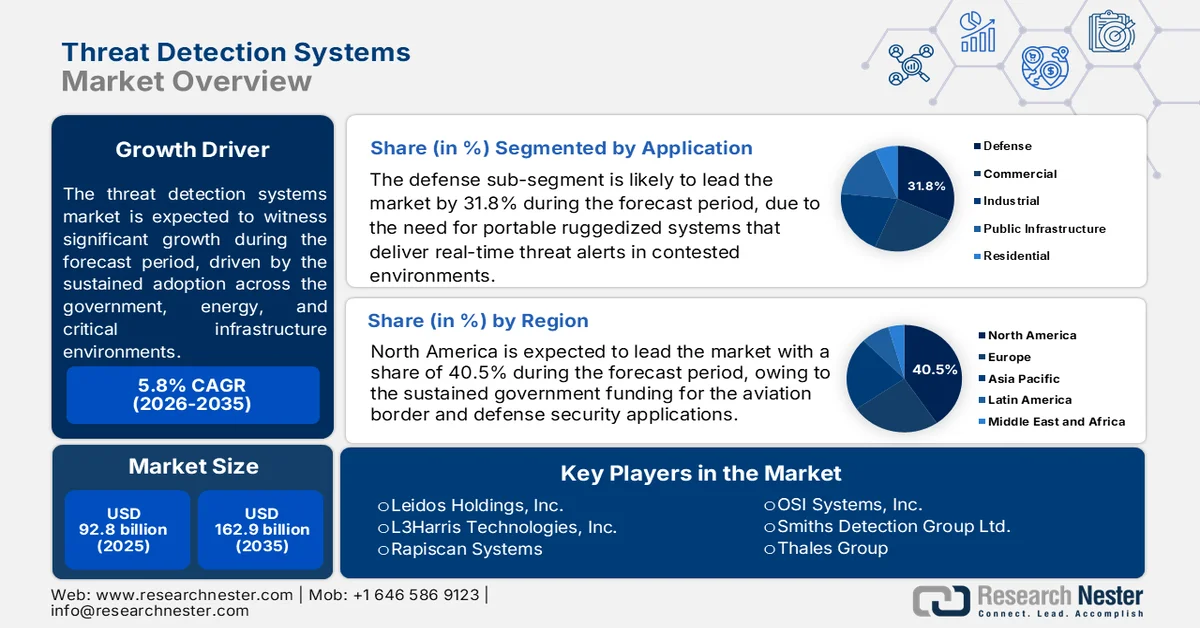

Threat Detection Systems Market size was valued at USD 92.8 billion in 2025 and is projected to reach USD 162.9 billion by the end of 2035, rising at a CAGR of 5.8% during the forecast period, 2026 to 2035. In 2026, the industry size of threat detection systems is assessed at USD 98.1 billion.

Threat detection systems are seeing sustained adoption across the government, defense, healthcare, financial services, energy, and critical infrastructure environments. The market is driven because organizations respond to the escalating cyber incident frequency and regulatory oversight. According to the FBI, April 2025 data, the cybercrime complaints registered in 2024 were over 859,532, reflecting continued financial exposure across enterprises and public sector institutions. The IC3 2023 data depicted that the ransomware complaints registered 880,418, with critical manufacturing, healthcare, government facilities, and transportation systems among the most affected sectors. In parallel, the operational directives for federal agencies under zero trust and continuous monitoring frameworks are increasing procurement demand for real-time network visibility, endpoint monitoring, and threat intelligence integration.

The National Institute of Standards and Technology has also intensified the adoption of the cybersecurity performance requirements via updates to the Cybersecurity Framework, prompting enterprises to strengthen the detection and incident response maturity. Demand is particularly strong among the organizations managing operational technology and hybrid cloud infrastructure, where continuous monitoring capabilities are tied to compliance obligations, cyber insurance requirements, and resilience planning. Public sector digital modernization initiatives across North America and Europe continue to support procurement cycles for the advanced detection and response infrastructure. Meanwhile, the International Telecommunication Union's November 2023 data noted that global internet penetration exceeded 67%, increasing enterprise exposure surfaces and driving broader deployment of cloud native monitoring and detection platforms. These data show a long-term growth and expansion in the market.

Key Threat Detection Systems Market Insights Summary:

Regional Highlights:

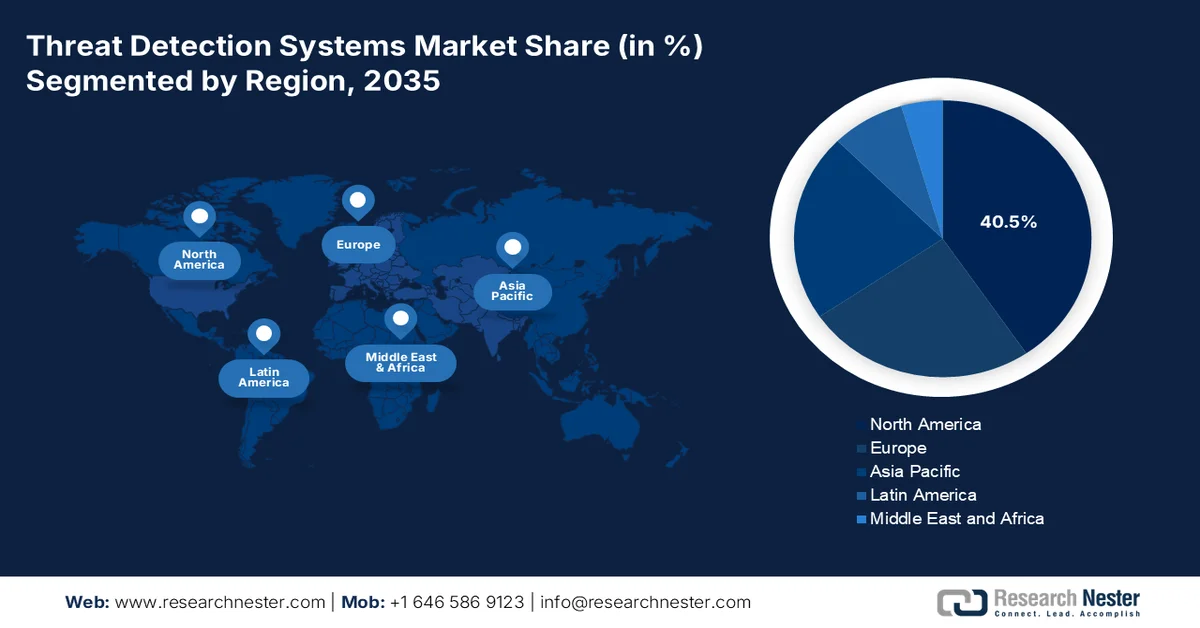

- North America is set to command 40.5% of the threat detection systems market by 2035, bolstered by sustained government funding for aviation, border, and defense security applications.

- Asia Pacific is anticipated to witness the fastest expansion during 2026-2035, stimulated by expanding aviation infrastructure, rising cross-border trade volumes, and national defense modernization programs.

Segment Insights:

- In the threat detection systems market, the defense application segment is projected to secure 31.8% share by 2035, supported by increasing demand for portable ruggedized systems that provide real-time threat alerts in contested environments.

- The cloud-based deployment mode segment is expected to retain its leading position through 2035, accelerated by the need for real-time data access, centralized storage, and AI-driven analytics across distributed environments.

Key Growth Trends:

- Expansion of federal cybersecurity

- Rising cybercrime losses

Major Challenges:

- Stringent regulatory compliance

- Supply chain and component sourcing vulnerabilities

Key Players: Leidos Holdings, Inc., L3Harris Technologies, Inc., Rapiscan Systems, OSI Systems, Inc., Smiths Detection Group Ltd., Thales Group, Safran S.A., Rheinmetall AG, Leonardo S.p.A., NEC Corporation, Fujitsu Limited, Hitachi, Ltd., EM Solutions Pty Ltd, Samsung Techwin (Hanwha Defense), LIG Nex1 Co., Ltd., Bharat Electronics Limited (BEL), CVC, Atos, Databricks, Vectra AI, Inc..

Global Threat Detection Systems Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 92.8 billion

- 2026 Market Size: USD 98.1 billion

- Projected Market Size: USD 162.9 billion by 2035

- Growth Forecasts: 5.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, United Kingdom, Germany, Japan

- Emerging Countries: India, South Korea, Indonesia, Malaysia, Vietnam

Last updated on : 2 June, 2026

Threat Detection Systems Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of federal cybersecurity: Government-led cybersecurity investment remains one of the strongest demand drivers for the threat detection systems market. In the U.S., the White House 2025 data reported that the federal cybersecurity budget request exceeded USD 13 billion for civilian agencies, with additional allocations supporting the Cybersecurity and Infrastructure Security Agency Zero Trust Architecture modernization and continuous diagnostics initiatives. The U.S. Department of Defense also continues large-scale spending under its cyber operations and network defense programs, increasing procurement of network monitoring, endpoint detection, and AI-supported analytics systems. Public agencies increasingly require integrated threat detection systems capable of real-time anomaly identification, cloud visibility, and automated incident escalation.

- Rising cybercrime losses: Rising cybercrime losses are surging the enterprise and government spending on the threat detection infrastructure. The FBI April 2024 data reported over USD 12.5 billion in cybercrime losses, with the ransomware attacks increasing. Critical sectors such as healthcare, manufacturing, transportation, and utilities remain primary targets. Governments are responding by strengthening the monitoring requirements and incident reporting mandates, which directly support demand for continuous threat detection systems. Healthcare institutions, public utilities, and financial entities are increasingly investing in threat intelligence integration and behavioral analytics to reduce operational disruptions and regulatory exposure. Organizations are also prioritizing the early warning systems capable of identifying lateral movement and insider threats.

Challenges

- Stringent regulatory compliance: Threat detection systems must comply with rigorous international and regional security regulations, including data privacy laws and industry-specific standards. New manufacturers often struggle to navigate this complex regulatory maze, delaying time to market. Top companies maintains its market leadership by embedding regulatory compliance into product design from the outset, particularly for their CBRNE detection systems used by government agencies.

- Supply chain and component sourcing vulnerabilities: Threat detection systems rely on specialized components such as high-quality sensors, X-ray tubes, and radiation detectors from a limited number of global suppliers. New entrants lack the purchasing power and supplier relationships to secure reliable, cost-effective components. Major manufacturers have vertically integrated their supply chain, manufacturing proprietary X-ray generators and detectors in-house. This strategy has allowed the company to maintain competitive pricing and reliable delivery schedules.

Threat Detection Systems Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

5.8% |

|

Base Year Market Size (2025) |

USD 92.8 billion |

|

Forecast Year Market Size (2035) |

USD 162.9 billion |

|

Regional Scope |

|

Threat Detection Systems Market Segmentation:

Application Segment Analysis

In the threat detection systems market, the defense sub-segment in the application is leading and is poised to hold the share value of 31.8% by the end of 2035. The segment is driven by the need for portable ruggedized systems that deliver real-time threat alerts in contested environments. Cyber Threat Analytics & Defensive Cyber Operations lead in investment and strategic importance. These systems integrate mission visibility data sets, providing cyber operators with real-time visualization tools and advanced analytic capabilities to detect intrusions, anomalies, and adversarial activities across military networks. Supporting this growth, the DHS 2025 data depicts that the U.S. Department of Defense budget allocated USD 394 million for the Joint Collaborative Environment, enabling a continued development of the Cyber Analytics and Data System. This scalable analytic environment ensures robust threat detection and rapid response for the national defense infrastructure.

Deployment Mode Segment Analysis

Under the deployment mode segment, the cloud-based is leading, enabling real-time data access, centralized storage, and AI-driven analytics across distributed environments. However, this shift introduces significant cybersecurity risks, including data breaches, shared infrastructure vulnerabilities, and complex regulatory compliance requirements such as GDPR and HIPAA. As noted in recent analyses of cloud-based diagnostic platforms, threats ranging from ransomware to misconfigured APIs demand multilayered countermeasures, including multi-factor authentication, role-based access control, encryption at rest, and continuous activity monitoring. According to a 2023 ENISA report, over 40% of healthcare cloud platforms experienced attempted data exfiltration incidents, underscoring the need for resilient deployment strategies.

Component Segment Analysis

The sensors are leading the component segment and is poised to hold the largest share value in the market. the segment is driven due to the requirement of primary data-capturing element in any detection system. Radiation & Nuclear Sensors used extensively for homeland security and defense applications to identify gamma neutron and other radioactive materials. According to the U.S. Nuclear Regulatory Commission many radiation portal monitors were deployed or upgraded at U.S. ports and border crossings. This deployment reflects the growing demand for high sensitivity solid state detectors and networked sensor arrays.

Our in-depth analysis of the threat detection systems includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Technology |

|

|

System Type |

|

|

Detection Method |

|

|

Deployment Mode |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Threat Detection Systems Market - Regional Analysis

North America Market Insights

North America is dominating the threat detection systems market and is expected to hold the regional revenue share of 40.5% by the end of 2035. The market is driven by the sustained government funding for the aviation border and defense security applications. The Transportation Security Administration continues deploying the advanced screening technologies across the airport checkpoints, while Customs and Border Protection operates non-intrusive inspection systems at land ports of entry. The Department of Defense maintains procurement programs for chemical, biological, radiological, nuclear, and explosive detection equipment. Network-connected systems are gaining adoption as agencies shift from standalone units to centralized data platforms. Data privacy requirements under the federal cloud security standards influence the procurement specifications, favoring vendors offering role-based access controls and encrypted data storage. Border modernization programs in both the U.S. and Canada sustain demand for portable and fixed detection platforms.

The rising financial and operational impact of ransomware attacks on critical infrastructure and public services is driving the threat detection systems market in the U.S. According to the GAO, January 2024 data, ransomware-related incidents in the country reached USD 886 million, representing a 68% increase compared to prompting organizations to strengthen real-time threat monitoring and incident response capabilities. In addition, the FBI reported that 870 critical infrastructure organizations were affected by ransomware in 2022 across 14 of the 16 critical infrastructure sectors, particularly manufacturing, energy, healthcare, and transportation. These escalating threats are increasing federal and enterprise investments in advanced threat detection systems, cybersecurity analytics, and continuous network monitoring technologies nationwide.

The rising ransomware incidents and expanding federal cybersecurity investments across critical infrastructure and public sector networks are driving the market in Canada. The Government of Canada's March 2023 data depicts that the government committed USD 875 million over five years, along with USD 238 million in ongoing annual funding, to strengthen national cybersecurity capabilities, improve cyber monitoring, and enhance threat response systems across government agencies and essential services. In parallel, the Canadian Centre for Cyber Security identified ransomware as one of the country’s most disruptive cyber threats affecting businesses, healthcare institutions, and infrastructure operators. Increasing cyber risks, combined with higher government funding for digital resilience and infrastructure protection, are accelerating demand for advanced threat detection and continuous monitoring solutions across Canada.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035, in the threat detection systems market. The market is driven by the expanding aviation infrastructure, rising cross-border trade volumes, and national defense modernization programs. Government agencies in Malaysia and Indonesia are deploying non-intrusive inspection equipment at seaports to counter smuggling activities. Regional manufacturers in China and South Korea compete alongside global suppliers for public sector contracts. Data sovereignty regulations across multiple countries require localized data storage for network-connected detection platforms. The shift from standalone to cloud-enabled systems is gradual, with many agencies prioritizing interoperability with the existing infrastructure. Border security modernization and critical infrastructure protection remain consistent demand drivers across the region.

Increasing cybersecurity regulation, industrial digitalization, and rising investments in critical infrastructure protection are shaping the threat detection systems market in China. The Cyberspace Administration of China and the Ministry of Industry and Information Technology have strengthened cybersecurity compliance requirements under the Data Security Law and Critical Information Infrastructure regulations, increasing deployment of network monitoring and threat detection platforms across finance, energy, and telecommunications sectors. According to the People’s Republic of China January 2024 data, the country’s software and information technology services industry generated over RMB 12 trillion in revenue in 2024, reflecting rapid enterprise digital expansion that requires advanced cyber monitoring capabilities. Additionally, China is significantly increasing network exposure and demand for real-time threat detection systems nationwide.

The Japan threat detection systems market is expected to grow from USD 3 billion in 2025 to USD 4.2 billion by the end of 2035 at a CAGR of 3.5%. In 2026, the industry size is expected to reach USD 3.1 billion. The market is driven by the expansion due to rising ransomware attacks, phishing activity, and stronger cybersecurity protection requirements across enterprises and critical infrastructure sectors. According to Japan Times, March 2026 data, the country recorded 226 ransomware-related damage cases in 2025, the second-highest annual total, with nearly 60% affecting small and medium-sized businesses. The NPA also reported that phishing incidents surged to a record 2,454,297 cases, approximately 1.4 times higher than the previous year, while unauthorized internet trading fraud caused losses of nearly ¥740.8 billion. Increasing cybercrime exposure is accelerating the adoption of advanced threat monitoring, endpoint detection, and real-time incident response systems across Japan’s financial, manufacturing, and commercial sectors.

Europe Market Insights

The market in Europe is shaped by the harmonized aviation security standards under the EU and national defense procurement programs. Member states implement the explosive detection requirements for airport baggage screening and air cargo inspection. Data privacy under the General Data Protection Regulation influences the procurement specifications, requiring vendors to offer localized data storage and cross-border transfer controls. Network-connected detection systems face additional compliance scrutiny regarding data sovereignty. Border security agencies deploy non-intrusive inspection systems at external EU borders and major seaports. Further, the Nordic countries prioritize radiation detection, while Eastern European nations focus on portable military detection units.

Rising cyber threats, increasing enterprise digitalization, and expanding national cybersecurity investments are driving the market in Germany. According to ITA's 2025 data, the country’s cyber threat landscape remained at a high risk level, with ransomware and malware attacks heavily targeting manufacturing, healthcare, and public infrastructure sectors. Germany’s cybersecurity spending also exceeded USD 10 billion in 2024 for the first time, reflecting accelerated investments in cyber resilience, industrial network protection, and threat monitoring technologies. Growing adoption of Industry 4.0 systems and cloud-connected industrial operations is further increasing demand for advanced threat detection platforms and continuous security monitoring solutions across Germany’s commercial and public sectors.

The threat detection systems market in the UK is expanding due to the rising frequency of cyberattacks targeting businesses, charities, and public sector organizations. According to the Government of the UK, April 2024 data, Cyber Security Breaches Survey, 50% of businesses and 32% of charities experienced a cybersecurity breach or attack within the last 12 months, while the figures increased to 70% for medium businesses and 74% for large enterprises. Phishing remained the most common attack vector, affecting 84% of businesses and 83% of charities that identified breaches. Increasing cyber risks across financial services, healthcare, and government infrastructure are accelerating investments in threat monitoring, endpoint detection, and real-time cybersecurity analytics solutions throughout the UK market.

Key Threat Detection Systems Market Players:

- Leidos Holdings, Inc. (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Rapiscan Systems (U.S.)

- OSI Systems, Inc. (U.S.)

- Smiths Detection Group Ltd. (UK)

- Thales Group (France)

- Safran S.A. (France)

- Rheinmetall AG (Germany)

- Leonardo S.p.A. (Italy)

- NEC Corporation (Japan)

- Fujitsu Limited (Japan)

- Hitachi, Ltd. (Japan)

- EM Solutions Pty Ltd (Australia)

- Samsung Techwin (Hanwha Defense) (South Korea)

- LIG Nex1 Co., Ltd. (South Korea)

- Bharat Electronics Limited (BEL) (India)

- CVC (UK)

- Atos (France)

- Databricks (U.S.)

- Vectra AI, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Leidos is a major player in the threat detection systems market, delivering advanced solutions for aviation, port, and border security. The company has integrated AI-driven analytics with its cargo and passenger screening systems to improve threat identification accuracy while reducing false alarms. In 2025, the company made a revenue of USD 17,174 million.

- L3Harris strengthens its position in the market via advanced radiation, explosive, and chemical agent detection technologies. The company has integrated its handheld and vehicle-mounted detectors with networked command-and-control systems, enabling real-time threat data sharing across military and homeland security operations. In 2025, the company made a revenue of USD 15,134 million.

- Rapiscan Systems is a leading innovator in the market, known for its X-ray baggage scanners, computed tomography hold baggage systems, and metal detectors. The company has advanced threat detection by integrating high-energy transmission technology with automatic explosives detection algorithms.

- OSI Systems holds a dominant share in the market, offering cargo and vehicle inspection systems, baggage scanners, and people screeners. The company has advanced the market by adopting backscatter and dual energy X-ray technologies for enhanced material discrimination.

- Smiths Detection is a global leader in the market, specializing in chemical, biological, radiological, nuclear, and explosive detection. The company has advanced mobile and fixed systems by adopting cloud-connected data analytics and real-time sensor networks for hazardous environments.

Here is a list of key players operating in the global market:

The global threat detection systems market is highly competitive, driven by rising security concerns and technological advancements. Key players from North America, Europe, and Asia-Pacific dominate, focusing on AI-integrated solutions, IoT-enabled sensors, and portable detection devices. Strategic initiatives include mergers and acquisitions to expand product portfolios, heavy R&D investments in chemical and radiological detection, and partnerships with government defense agencies. For example, in December 2025, CVC announced the acquisition of Smiths Detection for USD 2.54 billion. Companies are now prioritizing miniaturization and real-time data analytics to counter the evolving threats. Asia Pacific firms are rapidly gaining ground via cost-effective manufacturing and increased domestic defense spending, intensifying rivalry against established Western leaders.

Corporate Landscape of the Market:

Recent Developments

- In March 2026, Atos announced the launch of its Threat Research Center (TRC), which is a next-generation intelligence hub designed to deliver deeper, earlier, and more actionable insights into the world’s rapidly evolving cyberthreat landscape.

- In March 2026, Databricks announced Lakewatch, a new, agentic SIEM (Security Information and Event Management), which is designed to help organizations defend against advanced agent attackers.

- In May 2025, Vectra AI, Inc., partnered with Starhub and announced the launch of the Vectra AI Platform to enterprises across Singapore. This collaboration marks a significant expansion of StarHub’s cybersecurity capabilities, reinforcing its commitment to securing businesses in an increasingly complex threat landscape.

- Report ID: 8599

- Published Date: Jun 02, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.