Industrial Emission Control Systems Market Outlook:

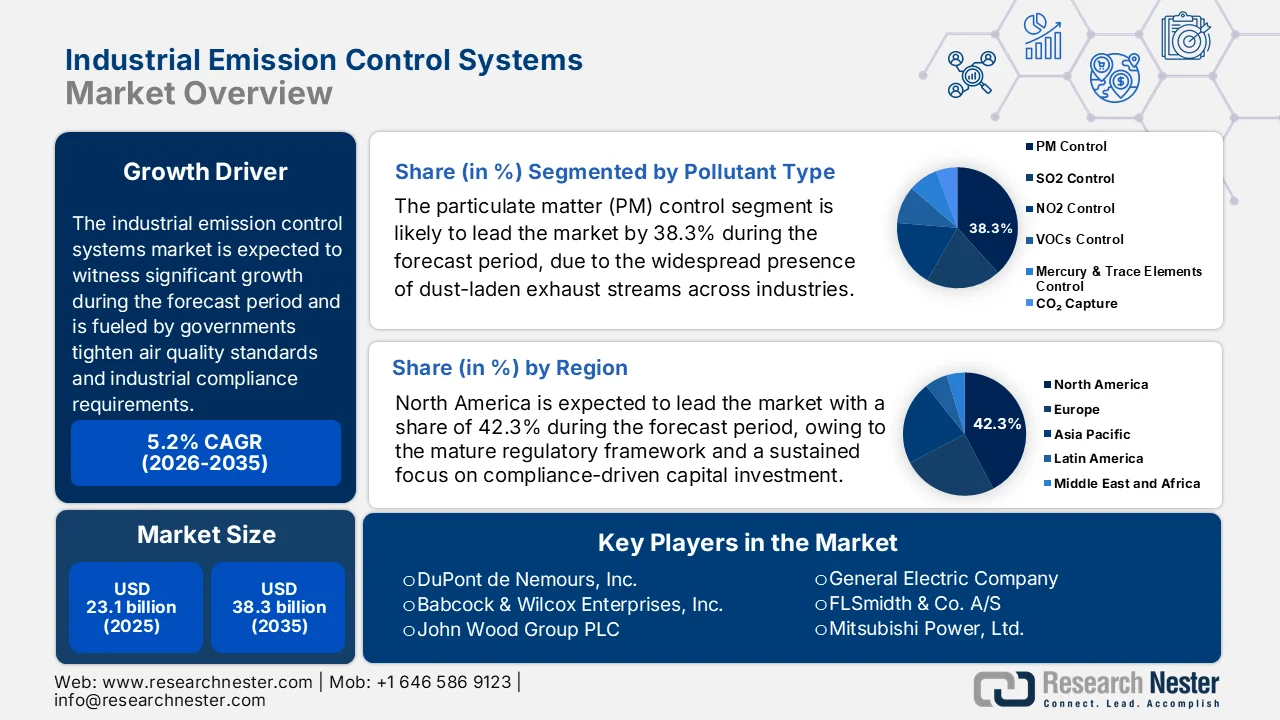

Industrial Emission Control Systems Market size was valued at USD 23.1 billion in 2025 and is projected to reach USD 38.3 billion by the end of 2035, rising at a CAGR of 5.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of industrial emission control systems is assessed at USD 24.3 billion.

The industrial emission control systems market is gaining sustained investment support as governments tighten air quality standards and industrial compliance requirements. According to the EPA's August 2024 data, the national emissions of key air pollutants have declined by 78% even as industrial output expanded significantly, reflecting the impact of mandated control technologies across power generation, chemicals, and manufacturing sectors. Programs such as the Clean Air Act enforcement and the National Emissions Standards for Hazardous Air Pollutants continue to require the installation of scrubbers, electrostatic precipitators, and catalytic reduction systems in high-emission facilities. These regulatory frameworks are directly influencing the capital expenditure cycles, mainly in sectors such as cement, steel, and refining, where compliance thresholds are becoming progressively stringent.

Besides, the international financing institutions and multilateral organizations have reinforced the emission control requirements as a condition for industrial infrastructure investment. According to the C.G. Environment Conservation Board September 2023 data, the Environmental Health and Safety Guidelines for Thermal Power and other industrial sectors stipulate performance standards that borrowing entities must meet, including particulate matter concentrations not exceeding 50 milligrams per normal cubic meter (mg/Nm3) for existing facilities and 30 mg/Nm3 for new facilities. National regulatory agencies have simultaneously tightened permissible limits. As per the NITI Aayog December 2024 data, the thermal power plants operating in critically polluted industrial clusters are required to achieve particulate emission limits of 30 mg/Nm3 and sulfur dioxide of 100 mg/Nm3, with compliance verification conducted via continuous monitoring systems linked to centralized servers. These binding thresholds create sustained procurement demand across both new plant construction and existing facility retrofits.

Regulatory Limits for Key Industrial Effluent Discharge Parameters (2023)

|

Parameter |

Limits |

|

pH |

5.5 – 9.0 |

|

Suspended Solids |

100 mg/L |

|

BOD |

30 mg/L |

|

COD |

250 mg/L |

|

Oil and Grease |

10 mg/L |

Source: C.G. Environment Conservation Board September 2023

Key Industrial Emission Control Systems Market Insights Summary:

Regional Highlights:

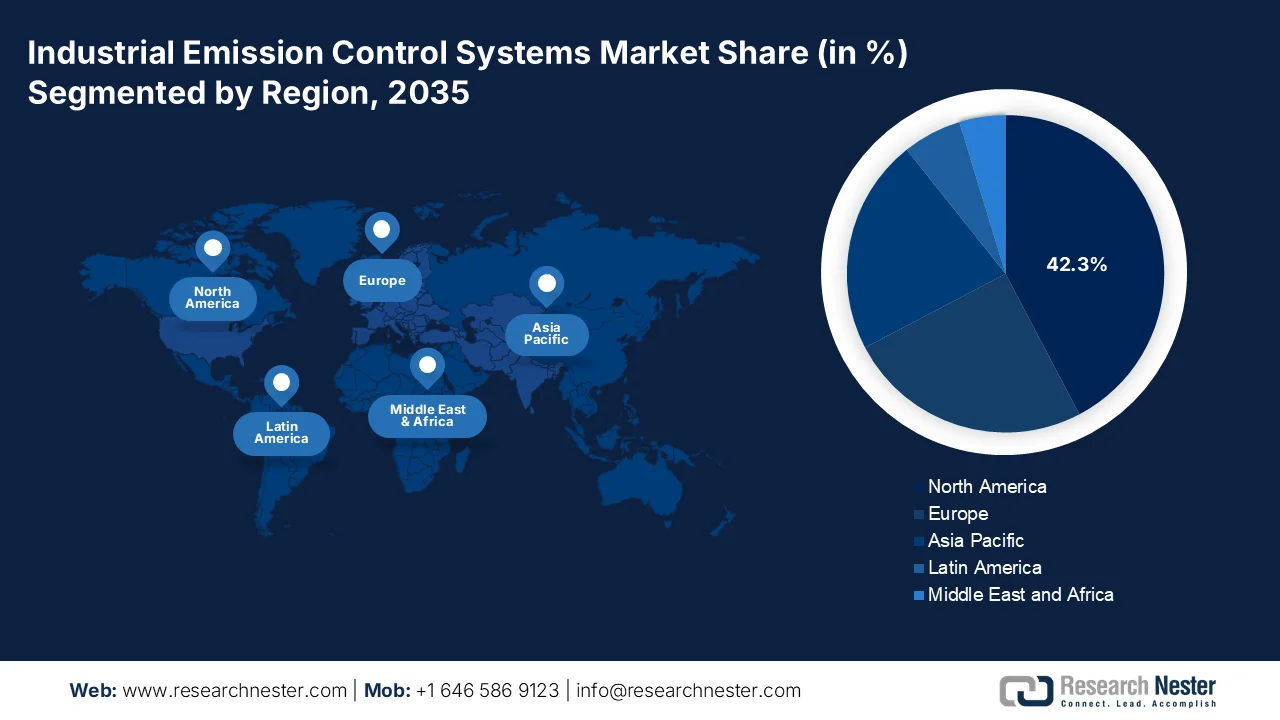

- North America in the industrial emission control systems market is anticipated to command a 42.3% share by 2035, attributed to strong compliance-driven capital investments across regulated industrial sectors

- Asia Pacific is forecast to witness a CAGR of 7.1% during 2026–2035, stimulated by rapid urbanization and stringent emission control mandates across emerging economies

Segment Insights:

- Within the pollutant type segment, particulate matter control in the industrial emission control systems market is projected to account for a 38.3% share by 2035, fueled by the widespread presence of dust-laden exhaust streams across industries

- Under the service type segment, aftermarket services are anticipated to secure a 45.3% share by 2035, propelled by increasing demand for operational optimization and equipment longevity amid stringent regulatory compliance requirements

Key Growth Trends:

- Expansion of air quality programs

- Industrial decarbonization funding

Major Challenges:

- Stringent and evolving regulatory compliance

- Operational reliability and system failure risks

Key Players: DuPont de Nemours, Inc., Babcock & Wilcox Enterprises, Inc., John Wood Group PLC, General Electric Company, FLSmidth & Co. A/S, Mitsubishi Power, Ltd., Hamon Group, AAF International, Donaldson Company, Inc., Schenck Process Holding GmbH, Thermax Limited, Sumitomo Heavy Industries, Ltd., KC Cottrell Co., Ltd., Yara Marine Technologies AS, Andritz AG, TPG Rise Climate, MIRATECH Corp, Knorr-Bremse, ABB, Födisch Group.

Global Industrial Emission Control Systems Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 23.1 billion

- 2026 Market Size: USD 24.3 billion

- Projected Market Size: USD 38.3 billion by 2035

- Growth Forecasts: 5.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: South Korea, Brazil, Indonesia, Vietnam, Mexico

Last updated on : 1 April, 2026

Industrial Emission Control Systems Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of air quality programs: Rising public expenditure on air pollution control is a primary demand driver for the industrial emission control systems market. Governments are allocating budgets to enforce the emission standards and upgrade industrial infrastructure. According to the EPA, February 2026 data, USD 3 billion is allocated under the Inflation Reduction Act to support air quality improvement, including industrial decarbonization and emissions monitoring initiatives. These funds are directed toward retrofitting facilities with advanced emission control technologies. On the other hand, EU continues to finance air pollution reduction under a program aligned with the Industrial Emission Directive, targeting large combustion plants and manufacturing units. This consistent funding pipeline is pushing industries to increase the capital investment in emission abatement systems. The availability of public funding reduces the compliance costs and supports technology adoption, mainly in energy-intensive sectors.

- Industrial decarbonization funding: Global climate commitments are translating into direct funding for industrial emission reduction technologies. The IEA 2023 data reports that the global energy-related CO2 emissions grew by 1.1% in 2023, prompting governments to allocate funding toward industrial decarbonization. Moreover, the World Resource Institute's March 2024 data depicts that the U.S. DOE has announced over USD 6 billion for industrial decarbonization projects under the federal programs supporting carbon capture and emission reduction in heavy industries. These initiatives directly require emission control systems such as carbon capture units and advanced filtration technologies. These investments are shifting demand from basic compliance systems toward integrated solutions that align with net-zero targets.

- Rising expansion of industry in emerging nations: Rapid industrialization is increasing the emission levels, prompting governments to enforce stricter controls. The industrial value-added growth in developing economies continues to expand, necessitating the parallel environmental regulations. Governments are introducing the emission standards alongside industrial policies, ensuring that new facilities are equipped with control systems from the outset. India and China have integrated the emission control requirements into industrial licensing processes. Public investment in industrial corridors and manufacturing zones often includes environmental compliance infrastructure, further supporting the demand in the industrial emission control systems market. Further, as the industrial output scales, compliance requirements are expected to tighten, reinforcing long-term demand across multiple sectors.

Challenges

- Stringent and evolving regulatory compliance: Navigating the complex, fragmented, and frequently tightening regulatory landscape across different jurisdictions poses a compliance burden for manufacturers in the industrial emission control systems market. Further, the regulations vary not only by country but also by region or state, requiring companies to develop flexible product lines that can meet the diverse emission standards for pollutants and particulate matter. Top companies address this by deploying technologies such as their low-pressure wet gas scrubbing system, which integrates with NOx and particulate control technologies to provide comprehensive compliance solutions for refineries facing increasingly strict emissions standards across North America.

- Operational reliability and system failure risks: Even after the installation, the risk of system failure due to inadequate maintenance, software errors, or operational oversight can lead to significant regulatory penalties and reputational damage, posing a challenge for new players who must prove long-term reliability. For example, a leading company had an incident where the control system software update compromised critical coke oven gas operations, resulting in a significant release of emissions. The NSW Environment Protection Authority issued a fine, noting that the company had failed to identify the control valve operations as a potential risk during the pre-work assessments.

Industrial Emission Control Systems Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.2% |

|

Base Year Market Size (2025) |

USD 23.1 billion |

|

Forecast Year Market Size (2035) |

USD 38.3 billion |

|

Regional Scope |

|

Industrial Emission Control Systems Market Segmentation:

Pollutant Type Segment Analysis

Within the pollutant type segment, the particulate matter control is leading in the industrial emission control systems market and is projected to hold the share value of 38.3% by the end of 2035. The segment is driven by the widespread presence of dust-laden exhaust streams across industries such as cement, mining, and power generation. Technologies such as fabric filters and electrostatic precipitators are essential for capturing fine inhalable particles to meet the stringent ambient air quality standards. Moreover, the number of industrial clusters identified as critically polluted based on particulate matter levels is driving the mandatory installation of high-efficiency dust collectors. These persistent non-attainment states compel the industries to invest significantly in the advanced PM control technologies to avoid operational shutdowns and comply with mandated emission reduction timelines.

Service Type Segment Analysis

Under the service type segment, the aftermarket services are dominating the segment and are poised to hold the share value of 45.3% by the end of 2035 in the industrial emission control systems market. As industrial facilities face a strong regulatory deadlines operator are prioritizing operational optimization and equipment longevity over new greenfield installations, leading to sustained revenue growth in retrofit and upgrade contracts. According to the FracTracker Alliance July 2025 data, Shell has submitted nearly 80 malfunction reports indicating 400 million of the air pollutant emissions. This data underscores the need for robust aftermarket service agreements. The manufacturers are expanding their service networks to offer predictive maintenance using data analytics, ensuring continuous compliance, minimizing downtime, and avoiding costly penalties.

Application Industry Segment Analysis

The power generation is the dominant sub-segment in the application industry segment and is driven by the global fleet of coal-fired power plants requiring flue gas desulfurization, denitrification, and particulate control retrofits to meet the modern emission standards. While the renewable penetration is increasing, the thermal power continues to be the backbone of electricity grids in many developing economies, necessitating continuous investment in pollution abatement. According to the People Daily Overseas Edition, May 2024 data, China reported that over 94% of its existing coal-fired power capacity had completed ultra-low emission retrofits, representing a cumulative investment over the past decade. This demonstrates the substantial capital allocated to the sector ensuing its continued dominance in the industrial emission control systems market via large-scale engineering procurement and construction contracts for emission control systems.

Our in-depth analysis of the industrial emission control systems market includes the following segments:

|

Segment |

Subsegments |

|

Equipment Type |

|

|

Pollutant Type |

|

|

Application Industry |

|

|

Technology Type |

|

|

Service Type |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Industrial Emission Control Systems Market - Regional Analysis

North America Market Insights

North America is dominating the industrial emission control systems market and is poised to hold the regional revenue share of 42.3% by the end of 2035. The region is defined by a mature regulatory framework and a sustained focus on compliance-driven capital investment across the power generation, oil and gas, chemical, and manufacturing sectors. The region’s market dynamics are shaped by the federal enforcement of stationary source emission standards, with industrial operators prioritizing equipment upgrades, retrofits, and aftermarket services over new greenfield installations due to the aging installed base of coal-fired and industrial boiler assets. Additionally, the market is witnessing increased integration of digital monitoring platforms that enable predictive maintenance and real-time compliance reporting as industrial end users seek to minimize downtime and avoid regulatory penalties

The manufacturing sector’s significant contribution to national greenhouse gas emissions and the projected rise in output from emissions intensive industries is shaping the industrial emission control systems market in U.S. According to the Congressional Budget Office February 2024 data, manufacturing accounted for 12% of total U.S. greenhouse gas emissions in 2021 with nearly 75% of these emissions arising from fuel combustion for process heat and the remainder from industrial processes. Besides, the chemical and refining industries alone contributed 59% of manufacturing emissions, indicating concentrated demand for emission control solutions in these verticals. Although manufacturing emissions declined by 17%, driven by improved emissions intensity and efficiency gains, future projections indicate a 17% increase in emissions due to expansion in high-output industries. These data show an optimistic industrial emission control systems market growth and expansion in the country.

CO2 Emissions Intensity in Manufacturing Industry (2024)

Source: Congressional Budget Office February 2024

Sustained reductions in key air pollutants and persistent emissions from high-impact industries such as oil and gas mining and utilities are shaping the industrial emission control systems market in Canada. According to the Government of Canada, June 2025 data emissions in 2023 declined significantly compared to 1990 levels, including SOx (80%), NOx (45%), VOCs (38%), CO (65%), and PM2.5 (15%), reflecting the long-term impact of regulatory enforcement and adoption of emission control technologies. However, sectoral data show that the oil and gas industry, ore and mineral processing, and electric utilities remain the largest contributors to SOx and NOx emissions, while VOC emissions are heavily linked to hydrocarbon extraction and solvent use. Alberta accounted for 42% of NOx and 35% of VOC emissions, indicating concentrated demand for advanced emission control systems in energy-intensive provinces. These data are fueling the market growth.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the industrial emission control systems market and is expected to expand at a CAGR of 7.1% during the assessed period, 2026 to 2035. The region is driven by the rapid urbanization and the enforcement of stringent emission standards across China, India, Japan, South Korea, and Southeast Asian nations. The key drivers include China’s ultra-low emission policy extension to industrial boilers and steel mills, and India’s Flue Gas Desulfurization mandate for thermal power plants. Trends shaping the industrial emission control systems market are the shift toward modular and prefabricated emission control systems suitable for space-constrained retrofit sites, and the integration of continuous emission monitoring systems with a centralized guarantee of emission reduction outcomes. Manufacturers are increasingly establishing regional manufacturing and service hubs to reduce costs and provide localized technical support.

The large-scale deployment of continuous monitoring infrastructure and the national air quality programs are fueling the industrial emission control systems market in India. As per the PIB December 2023 data, the government targets a 40% reduction in the PM10 levels across 131 non-attainment cities, thus creating sustained regulatory pressure on industrial emitters. This has directly surged the adoption of the Continuous Emission Monitoring Systems with over 30,000 units already installed across India industries based on the UPCCCE April 2024, focusing on the pollutants such as particulate matter, SO₂, and NOₓ. Moreover, the state-level enforcement is also strengthening demand with the Uttar Pradesh Pollution Control Board (UPPCB) conducting regular inspections to ensure compliance and data accuracy. Further, these data show a consistent demand for integrated emission control systems, particularly in power generation and heavy industrial sectors where compliance requirements are becoming increasingly stringent.

The continues expansion on ongoing air quality challenges and tightening environmental oversight are shaping the industrial emission control systems market in China. According to the ITA September 2025 data, China’s annual average PM2.5 concentration was 29.3 µg/m³ in 2024, significantly exceeding the WHO guideline of 5 µg/m³, with over 30% of cities failing to meet national air quality standards. Despite overall improvement trends, sharp YoY increases in PM2.5 levels were recorded in key urban centers such as Harbin (+72%), Yinchuan (+56%), and Beijing (+46%), underscoring persistent regional pollution spikes driven by the industrial emissions and adverse meteorological conditions. Moreover, the air pollution contributes to 2 million deaths annually, reinforcing the urgency for stricter emission controls and industrial compliance. These data show active investment opportunities in the nation.

Europe Market Insights

The industrial emission control systems market in Europe is driven by the Industrial Emissions Directive and the European Green Deal, which mandate continuous reduction in air pollutants from large combustion plants, waste incineration, and industrial manufacturing facilities. The member states are required to implement best available technology conclusions, triggering investment cycles for selective catalytic reduction systems, fabric filters, and flue gas desulfurization units across cement, steel, chemical, and power generation sectors. The key trends include the integration of carbon capture readiness into emission control retrofits, increased adoption of continuous monitoring systems for real-time compliance reporting adn the emergence of public-private co-financing mechanisms that reduce the capital barriers for industrial operators. The market is defined by a mature installed base with aftermarket services representing a growing share of revenue as facilities seek to extend equipment life and maintain operational reliability under tightening enforcement timelines.

The long-term emission reduction targets and strict carbon budgeting frameworks that require sustained industrial compliance are fueling the industrial emission control systems market in the UK. According to the Office for National Statistics, November 2025 data, UK territorial greenhouse gas emissions declined to 371 million tonnes of CO2 equivalent in 2024, representing a 54% reduction, while production-based emissions stood at 476 Mt CO2e, down 43% over the same period. Despite this progress, industrial activity remains a significant contributor, with the industry sector emitting approximately 48.3 Mt CO2e in 2024. The gap between declining territorial emissions and higher consumption-based emissions also highlights the need for deeper emission controls within domestic manufacturing and supply chains. These regulatory pressures are driving demand for across manufacturing energy supply and heavy industry sectors where emission reductions must accelerate to meet legally binding national targets.

Top Emitting Sector on Territorial Basis (2024)

|

Sector |

Emission (million tons of CO2e) |

|

Electricity Supply |

37.5 |

|

Fuel Supply |

28.4 |

|

Domestic Transport |

110.1 |

|

Buildings and Product Uses |

79.8 |

|

Industry |

48.3 |

|

Agriculture |

46.4 |

|

Waste |

19.5 |

|

Land use, Land use Change and Forestry |

1.4 |

Source: Office for National Statistics, November 2025

The strict national decarbonization targets sector-specific emission reductions, and the continued regulatory enforcement across the heavy industries is shaping the industrial emission control systems market in Germany. According to the Umweltbundesamt, March 2024 data, total greenhouse gas emissions declined to 673 million tons of CO2 equivalent, representing a significant reduction compared to the previous years, with the industrial sector contributing approximately 155 Mt CO2 equivalents. The Federal Ministry for Economic Affairs and Climate Action (BMWK) reports that Germany allocated over USD 110 billion under its Climate and Transformation Fund (KTF) to support industrial decarbonization, including carbon capture and efficiency upgrades. Further, these policy-backed investments and targets are sustaining the demand for filtration desulfurization and carbon capture solutions, particularly as industries align with tightening EU and national compliance frameworks.

Key Industrial Emission Control Systems Market Players:

- DuPont de Nemours, Inc. (U.S.)

- Babcock & Wilcox Enterprises, Inc. (U.S.)

- John Wood Group PLC (UK)

- General Electric Company (U.S.)

- FLSmidth & Co. A/S (Denmark)

- Mitsubishi Power, Ltd. (Japan)

- Hamon Group (Belgium/Europe)

- AAF International (American Air Filter) (U.S.)

- Donaldson Company, Inc. (U.S.)

- Schenck Process Holding GmbH (Germany)

- Thermax Limited (India)

- Sumitomo Heavy Industries, Ltd. (Japan)

- KC Cottrell Co., Ltd. (South Korea)

- Yara Marine Technologies AS (Norway)

- Andritz AG (Austria)

- TPG Rise Climate (U.S.)

- MIRATECH Corp (U.S.)

- Knorr-Bremse (Germany)

- ABB (Switzerland)

- Födisch Group (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- DuPont de Nemours, Inc is a leader in the industrial emission control systems market, using its advanced materials science to develop high-performance filtration media and membrane technologies. The company has made significant advancements by engineering durable chemical-resistant filter bags and wet electrostatic precipitators that capture sub-micron particulate matter.

- Babcock & Wilcox Enterprises Inc is a key innovator in the industrial emission control systems market, specializing in comprehensive boiler cleaning, electrostatic precipitators, and flue gas desulfurization technologies. The company has advanced the industrial emission control systems market by integrating digital optimization tools and aftermarket service solutions that predict system wear and maintain peak collection efficacy. In 2024, the company made a revenue of USD 717,333 thousand.

- John Wood Group PLC is a prominent engineering firm in the industrial emission control systems market, differentiating itself via integrated project management and digital asset optimization for emission control infrastructure. The company has made significant advancements by combining its consulting expertise with proprietary Wood digital twin technology to monitor selective catalytic reduction systems.

- General Electric Company is a dominant player in the industrial emission control systems market, utilizing its deep expertise in power generation and digital industrial applications to advance emission control technologies. The company has advanced the market by developing integrated gasification combined cycle systems and leveraging a software platform for real-time monitoring. In 2024, the company has invested USD 1 billion in R&D.

- FLSmidth & Co. A/S is a specialized leader in the industrial emission control systems market, focusing on air pollution control solutions customized specifically for the cement and mining industries. The company has made significant advancements by pioneering hot gas fabric filters and efficient baghouse technologies designed to handle the corrosive, high-temperature exhaust typical of clinker production and mineral processing.

Here is a list of key players operating in the global industrial emission control systems market:

The industrial emission control systems market is highly competitive and is defined by a mix of multinational players and specialized technology leaders. The key players are pursuing strategic initiatives focused on digitalization, IoT-enabled monitoring for predictive maintenance, and the development of next-gen filtration materials to meet the tightening global emissions standards. A significant trend is the expansion of service networks and the acquisition of regional players to strengthen the aftermarket revenue streams. For example, in September 2024, TPG Rise Climate announced the acquisition of MIRATECH Corp. Companies are also investing in carbon capture integration and modular system design to offer cost-effective, scalable solutions for diverse industries such as power generation, cement, and chemicals.

Corporate Landscape of the Industrial Emission Control Systems Market:

Recent Developments

- In February 2025, international technology group ANDRITZ has acquired LDX Solutions, a leading provider of emission reduction technologies and related services in the North American industrial emission control systems market, with annual revenues of about USD 100 million.

- In January 2025, Knorr-Bremse has completed the sale of its subsidiary GT Emissions Systems to Rcapital Partners, a private equity fund from the UK. GT Emissions Systems, based in Peterlee, Great Britain, is a leading supplier of emission control systems for diesel engines in on-highway commercial vehicles and off-highway vehicles.

- In August 2024, ABB announced that it has signed an agreement to acquire Födisch Group, a leading developer of advanced measurement and analytical solutions for the energy and industrial sectors.

- Report ID: 8491

- Published Date: Apr 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Industrial Emission Control Systems Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.