Global 3D AOI & SPI Systems Market for PCB Assembly

- An Outline of the Global 3D AOI & SPI Systems Market for PCB Assembly

- Market Definition and Segmentation

- Study Assumptions and Abbreviations

- Research Methodology & Approach

- Primary Research

- Secondary Research

- Data Triangulation

- SPSS Methodology

- Executive Summary

- Growth Drivers

- Major Roadblocks

- Opportunities

- Prevalent Trends

- Government Regulation

- Growth Outlook

- Competitive White Space Analysis – Identifying Untapped Market Gaps

- Risk Overview

- SWOT

- Technological Advancement

- Technology Maturity Matrix for Global 3D AOI & SPI Systems Market for PCB Assembly Recent News

- Regional Demand

- Global 3D AOI & SPI Systems Market for PCB Assembly by Geography – Strategic Comparative Analysis

- Strategic Segment Analysis: 3D AOI & SPI Systems Market for PCB Assembly Demand Landscape

- 3D AOI & SPI Systems Market for PCB Assembly Demand Trends Driven by increasing complexity of PCB designs, growing adoption of smart manufacturing and automation technologies (2026-2036)

- Root Cause Analysis (RCA) for discovering problems of the 3D AOI & SPI Systems Market for PCB Assembly

- Porter Five Forces

- PESTLE

- Comparative Positioning

- Global 3D AOI & SPI Systems Market for PCB Assembly – Key Player Analysis (2036)

- Competitive Landscape: Key Suppliers/Players

- Competitive Model: A Detailed Inside View for Investors

- Company Market Share, 2036 (%)

- Camtek Ltd. (Israel)

- GÖPEL electronic GmbH (Germany)

- KLA Corporation (U.S.)

- Koh Young Technology, Inc. (South Korea)

- MIRTEC CO., LTD (South Korea)

- Nordson Corporation (U.S.)

- Omron Corporation (Japan)

- PARMI (Taiwan)

- SAKI CORPORATION (Japan)

- Test Research, Inc. (U.S.)

- Viscom SE (Germany)

- ViTrox Corporation (Malaysia)

- Yamaha Motor Co., Ltd. (Japan)

- Global 3D AOI & SPI Systems Market for PCB Assembly Outlook

- Market Overview

- Market Revenue by Value (USD Million), and Compound Annual Growth Rate (CAGR)

- 3D AOI & SPI Systems Market for PCB Assembly Segmentation Analysis (2026-2036)

- By System

- 3D AOI System, Market Value (USD Million), and CAGR, 2026-2036F

- SPI System, Market Value (USD Million), and CAGR, 2026-2036F

- By Inspection Stage

- SPI–Post Solder Printing (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Placement (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Method

- Inline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- Offline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- By End user

- Consumer Electronics, Market Value (USD Million), and CAGR, 2026-2036F

- Telecommunications, Market Value (USD Million), and CAGR, 2026-2036F

- Automotive, Market Value (USD Million), and CAGR, 2026-2036F

- Medical Devices, Market Value (USD Million), and CAGR, 2026-2036F

- Aerospace & Défense, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Regional Synopsis, Value (USD Million), 2026-2036

- North America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Asia Pacific Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Middle East and Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By System

- Market Overview

- North America Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

- By System

- 3D AOI System, Market Value (USD Million), and CAGR, 2026-2036F

- SPI System, Market Value (USD Million), and CAGR, 2026-2036F

- By Inspection Stage

- SPI–Post Solder Printing (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Placement (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Method

- Inline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- Offline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- By End user

- Consumer Electronics, Market Value (USD Million), and CAGR, 2026-2036F

- Telecommunications, Market Value (USD Million), and CAGR, 2026-2036F

- Automotive, Market Value (USD Million), and CAGR, 2026-2036F

- Medical Devices, Market Value (USD Million), and CAGR, 2026-2036F

- Aerospace & Défense, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- U.S. Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Canada Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By System

- Overview

- Europe Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

- By System

- 3D AOI System, Market Value (USD Million), and CAGR, 2026-2036F

- SPI System, Market Value (USD Million), and CAGR, 2026-2036F

- By Inspection Stage

- SPI–Post Solder Printing (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Placement (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Method

- Inline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- Offline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- By End user

- Consumer Electronics, Market Value (USD Million), and CAGR, 2026-2036F

- Telecommunications, Market Value (USD Million), and CAGR, 2026-2036F

- Automotive, Market Value (USD Million), and CAGR, 2026-2036F

- Medical Devices, Market Value (USD Million), and CAGR, 2026-2036F

- Aerospace & Défense, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- UK Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Germany Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- France Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Italy Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Spain Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Netherlands Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Russia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Switzerland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Poland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Belgium Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By System

- Overview

- Asia Pacific Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

- By System

- 3D AOI System, Market Value (USD Million), and CAGR, 2026-2036F

- SPI System, Market Value (USD Million), and CAGR, 2026-2036F

- By Inspection Stage

- SPI–Post Solder Printing (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Placement (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Method

- Inline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- Offline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- By End user

- Consumer Electronics, Market Value (USD Million), and CAGR, 2026-2036F

- Telecommunications, Market Value (USD Million), and CAGR, 2026-2036F

- Automotive, Market Value (USD Million), and CAGR, 2026-2036F

- Medical Devices, Market Value (USD Million), and CAGR, 2026-2036F

- Aerospace & Défense, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- China Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- India Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Korea Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Australia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Indonesia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Malaysia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Vietnam Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Thailand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Singapore Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- New Zealand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Asia Pacific Excluding Japan Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By System

- Overview

- Latin America Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Million), 2026-2036,

- By System

- 3D AOI System, Market Value (USD Million), and CAGR, 2026-2036F

- SPI System, Market Value (USD Million), and CAGR, 2026-2036F

- By Inspection Stage

- SPI–Post Solder Printing (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Placement (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Method

- Inline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- Offline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- By End user

- Consumer Electronics, Market Value (USD Million), and CAGR, 2026-2036F

- Telecommunications, Market Value (USD Million), and CAGR, 2026-2036F

- Automotive, Market Value (USD Million), and CAGR, 2026-2036F

- Medical Devices, Market Value (USD Million), and CAGR, 2026-2036F

- Aerospace & Défense, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- Brazil Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Argentina Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Mexico Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By System

- Overview

- Middle East & Africa Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Million), 2026-2036,

- By System

- 3D AOI System, Market Value (USD Million), and CAGR, 2026-2036F

- SPI System, Market Value (USD Million), and CAGR, 2026-2036F

- By Inspection Stage

- SPI–Post Solder Printing (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Placement (Pre-Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- AOI – Post Reflow), Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Method

- Inline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- Offline Inspection Systems, Market Value (USD Million), and CAGR, 2026-2036F

- By End user

- Consumer Electronics, Market Value (USD Million), and CAGR, 2026-2036F

- Telecommunications, Market Value (USD Million), and CAGR, 2026-2036F

- Automotive, Market Value (USD Million), and CAGR, 2026-2036F

- Medical Devices, Market Value (USD Million), and CAGR, 2026-2036F

- Aerospace & Défense, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- Saudi Arabia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- UAE Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Israel Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Qatar Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Kuwait Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Oman Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Middle East & Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By System

- Overview

- Global Economic Scenario

- World Economic Outlook

- About Research Nester

- Our Global Clientele

- We Serve Clients Across World

3D AOI & SPI Systems Market for PCB Assembly Outlook:

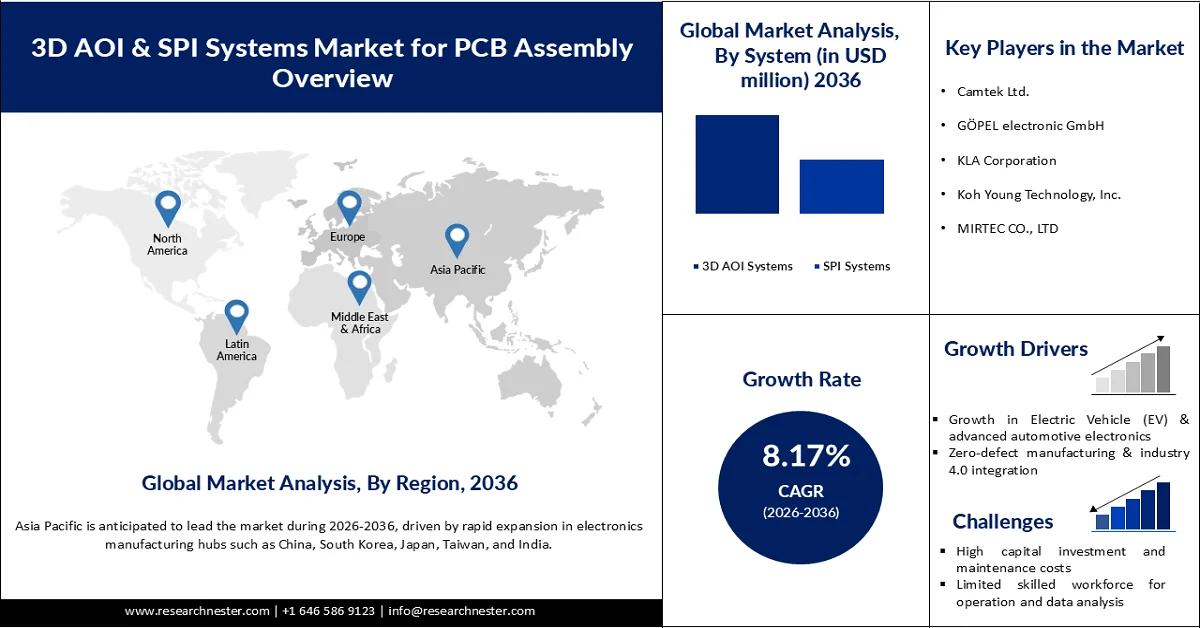

3D AOI & SPI Systems Market for PCB Assembly is valued at USD 2.01 billion in 2025 and is projected to reach USD 4.77 billion by 2036, growing at a CAGR of 8.17% during the forecast period, i.e., 2026-2036. In 2026, the industry size of 3D AOI & SPI systems market for PCB assembly is estimated at USD 2.17 billion.

The primary growth driver of the global 3D AOI & SPI systems market for PCB assembly is the increasing need for high-quality, defect-free electronics amid rising product complexity and miniaturization. As modern PCBs incorporate ultra-fine components and high-density designs, the margin for manufacturing error has significantly reduced, making advanced 3D inspection essential for yield improvement and reliability. About 60–90% of PCB assembly failures are caused by solder paste–related defects, which are often invisible to traditional 2D inspection methods. The push toward zero-defect manufacturing in sectors such as automotive and medical electronics, combined with increasing automation and adoption of Industry 4.0, further accelerates demand. The rapid growth of electronics production, particularly in consumer devices and electric vehicles (EVs), has significantly increased the demand for real-time inspection systems to minimize defects, reduce rework, and control cost losses. In the U.S. alone, by 2025, the electronics manufacturing industry supported approximately 5.2 million jobs. It generated about USD 1.8 trillion in total economic output, highlighting the sheer scale and economic importance of electronics production. This large-scale manufacturing environment, combined with the increasing complexity of EV and consumer electronics assemblies, underscores the critical role of advanced inspection technologies such as 3D AOI and SPI systems in ensuring high-quality assembly and preventing costly defects. Overall, the convergence of miniaturization, quality standards, and precision manufacturing is the core driver fueling market expansion.

Key 3D AOI & SPI Systems Market for PCB Assembly Market Insights Summary:

Regional Highlights:

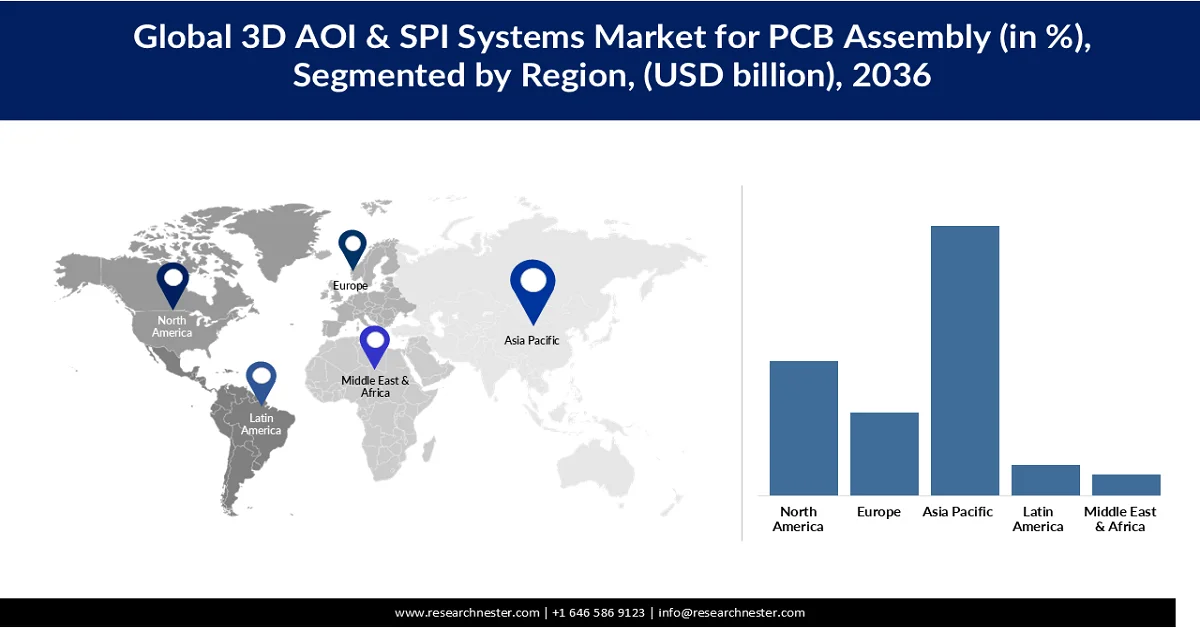

- By 2036, Asia Pacific is anticipated to capture 52% share in the 3d aoi & spi systems market for pcb assembly, propelled by rapid expansion in electronics manufacturing hubs across key countries.

- North America is forecast to secure around 26% share by 2036, supported by increasing investments in automation, smart factories, and quality inspection systems.

Segment Insights:

- By 2036, the 3d aoi systems segment in the 3d aoi & spi systems market for pcb assembly is projected to account for 64.37% share, attributed to superior inspection accuracy and the ability to detect complex defects that 2d systems often miss.

- The inline inspection systems segment is expected to reach 68.50% share by 2036, impelled by the shift toward continuous, real-time quality control within automated pcb assembly lines.

Key Growth Trends:

- Growth in Electric Vehicle (EV) & advanced automotive electronics

- Zero‑defect manufacturing & industry 4.0 integration

Major Challenges:

- High capital investment and maintenance costs

- Limited skilled workforce for operation and data analysis

Key Players: Camtek Ltd. (Israel), GÖPEL electronic GmbH (Germany), KLA Corporation (U.S.), Koh Young Technology, Inc. (South Korea), MIRTEC CO., LTD (South Korea), Nordson Corporation (U.S.), Omron Corporation (Japan), PARMI (Taiwan), SAKI CORPORATION (Japan), Test Research, Inc. (U.S.), Viscom SE (Germany), ViTrox Corporation (Malaysia), Yamaha Motor Co., Ltd. (Japan).

Global 3D AOI & SPI Systems Market for PCB Assembly Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.01 billion

- 2026 Market Size: USD 2.17 billion

- Projected Market Size: USD 4.77 billion by 2036

- Growth Forecasts: 8.17% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: Asia Pacific (52% Share by 2036)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Taiwan, Vietnam, Mexico, Poland

Last updated on : 8 April, 2026

3D AOI & SPI Systems Market for PCB Assembly - Growth Drivers and Challenges

Growth Drivers

- Growth in Electric Vehicle (EV) & advanced automotive electronics: The shift to electrification and autonomous features is rapidly increasing the volume and complexity of automotive electronics, which rely heavily on PCBs and require defect‑free assembly. In the U.S., electric and hybrid vehicles made up about 22 % of new light‑duty vehicle sales in 2025, reflecting accelerated adoption of EVs with sophisticated electronic systems (battery management, power electronics, ADAS). These systems employ densely populated PCBs where even microscopic manufacturing defects can lead to field failures or safety issues. Real‑time inspection tools such as 3D SPI and AOI are critical for ensuring high first‑pass yields and reducing costly rework or recalls. This trend is mirrored globally, where EV production and sales continue to rise year over year, increasing demand for advanced inspection in automotive PCB assembly.

- Zero‑defect manufacturing & industry 4.0 integration: Manufacturers across sectors are pursuing zero‑defect manufacturing (ZDM) models to reduce waste, enhance reliability, and meet stringent quality standards. Industry 4.0 technologies such as IoT, AI, and big data analytics enable real‑time process monitoring and predictive quality control, which are essential for ZDM. The U.S. National Institute of Standards and Technology (NIST) and other agencies emphasize digital quality infrastructure as central to advanced manufacturing competitiveness, reflected in a USD 2.3 trillion manufacturing value‑added sector (10.2 % of GDP) that increasingly relies on data‑driven quality systems. As factories deploy more sensors and networked inspection systems, 3D AOI and SPI become integral to IoT‑enabled smart lines, delivering not just detection but actionable feedback into manufacturing execution systems (MES). This reduces defect escape rates and cumulative rework costs, particularly in high‑precision industries like aerospace and medical electronics.

- Adoption of AI & machine learning for enhanced defect detection: The integration of artificial intelligence (AI) and machine learning (ML) into inspection systems is rapidly transforming how manufacturers detect and classify defects in PCB assembly. The integration of artificial intelligence (AI) and machine learning (ML) into inspection systems is rapidly transforming PCB assembly, enabling defect detection accuracies of around 95–98% with a defect rate as low as below 0.1%, significantly outperforming traditional inspection systems and enhancing overall quality and reliability. AI‑enabled 3D AOI and SPI systems can learn from vast datasets of inspected boards, improving defect recognition accuracy, reducing false calls, and enabling predictive quality insights across production lines. This shift reduces dependency on rule‑based inspection and accelerates fault identification even in highly complex boards. The growing use of data‑driven approaches supports in‑process decision making and closed‑loop control, which in turn reduces rework and boosts overall production yield. As the electronics industry increasingly moves toward smart manufacturing, AI/ML capabilities are becoming key differentiators that drive adoption of advanced inspection technologies, especially in high‑mix and high‑volume environments.

Challenges

- High capital investment and maintenance costs: 3D AOI and SPI systems require substantial upfront investment, often running into hundreds of thousands of dollars per unit, making it challenging for small and mid-sized PCB manufacturers to adopt them. In addition to purchase costs, these systems demand regular maintenance, software updates, and calibration, increasing the total cost of ownership. The high capital intensity can slow adoption in regions with cost-sensitive electronics manufacturing, particularly for smaller-scale or low-margin production lines.

- Limited skilled workforce for operation and data analysis: Advanced inspection systems rely on trained operators and engineers capable of handling complex software, interpreting inspection results, and integrating feedback into production lines. A shortage of skilled personnel in electronics manufacturing and quality control limits optimal utilization of 3D AOI and SPI systems. Without proper training, manufacturers may underutilize these tools or misinterpret defect data, reducing the expected improvements in yield and defect reduction.

3D AOI & SPI Systems Market for PCB Assembly Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2036 |

|

CAGR |

8.17% |

|

Base Year Market Size (2025) |

USD 2.01 billion |

|

Forecast Year Market Size (2036) |

USD 4.77 billion |

|

Regional Scope |

|

3D AOI & SPI Systems Market for PCB Assembly Segmentation:

System Segment Analysis

The 3D AOI systems segment is expected to hold 64.37% of the market share, driven by superior inspection accuracy and the ability to detect complex defects that 2D systems often miss. As PCB designs become more compact and densely populated, manufacturers increasingly rely on 3D AOI to ensure quality and reduce costly rework. The technology enables precise measurement of solder joints, component placement, and volume, which is critical for advanced electronics such as automotive, aerospace, and consumer devices. Growing adoption of automation and smart manufacturing further accelerates demand for 3D AOI systems, as they integrate well with Industry 4.0 environments. Additionally, the rising need for zero-defect production and stringent quality standards pushes manufacturers to upgrade from traditional inspection methods. Continuous advancements in imaging, AI, and data analytics also enhance system capabilities, making them more efficient and scalable. As a result, the 3D AOI segment significantly contributes to overall market expansion by improving yield, reducing defects, and supporting high-volume production.

Deployment Method Segment Analysis

The inline inspection systems segment is expected to grow at a significant market share of 68.50% by 2036. The segment drives the growth of the deployment method category by enabling continuous, real-time quality control within automated PCB assembly lines. Unlike offline systems, inline solutions are directly integrated into production workflows, allowing immediate detection and correction of defects, which significantly reduces downtime and rework costs. As manufacturers increasingly adopt high-speed, high-volume production, the demand for seamless inspection systems that do not interrupt the manufacturing process continues to rise. Inline systems also support Industry 4.0 initiatives by offering advanced connectivity, data analytics, and traceability, helping manufacturers optimize process efficiency and maintain consistent quality. Their ability to enhance throughput while meeting stringent quality standards makes them the preferred deployment method across industries such as automotive, consumer electronics, and industrial manufacturing. Consequently, the widespread shift toward automation and smart factories strongly accelerates the adoption and growth of inline inspection systems within the market.

End user Segment Analysis

The automotive segment is expected to hold a 34.56% market share by 2036 due to its stringent quality and reliability requirements. Modern vehicles incorporate complex electronic systems such as ADAS, infotainment, and electric powertrains, all of which depend on highly reliable PCB assemblies. This increases the need for advanced inspection solutions like 3D AOI and SPI to detect even the smallest defects in solder joints and component placement. Additionally, the shift toward electric vehicles (EVs) and autonomous driving technologies has significantly expanded the volume and complexity of automotive electronics, further boosting demand for precise inspection systems. Automotive manufacturers also emphasize zero-defect production and compliance with strict safety standards, driving continuous investment in high-performance inspection technologies. As production scales up globally, especially for EVs, the automotive segment continues to fuel growth in the end-use category by demanding higher accuracy, efficiency, and reliability in PCB inspection processes.

Our in-depth analysis of the 3D AOI & SPI systems market for PCB assembly includes the following segments:

|

Segments |

Subsegments |

|

System |

|

|

Inspection Stage |

|

|

Deployment Method |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

3D AOI & SPI Systems Market for PCB Assembly - Regional Analysis

Asia Pacific Market Insights

The 3D AOI & SPI systems market for PCB assembly in the Asia Pacific is expected to grow with a market share of 52% by 2036, driven by rapid expansion in electronics manufacturing hubs such as China, South Korea, Japan, Taiwan, and India. Rising demand for high‑quality printed circuit boards in automotive electronics, consumer devices, and industrial automation is boosting the adoption of advanced inspection technologies. Additionally, increasing investments in smart factories and Industry 4.0 initiatives are accelerating the deployment of AI‑enabled inspection systems to improve yield and reduce defects. Government incentives and favorable policies supporting the semiconductor and electronics sectors further strengthen market expansion. As manufacturing infrastructure continues to modernize, APAC is expected to remain the fastest‑growing regional market for 3D AOI & SPI solutions.

China has strengthened its position as a global manufacturing powerhouse, with its share of global manufacturing value added rising from 25.9 % in 2015 to 28.8 % in 2023, reflecting rapid expansion in electronics and high‑technology production. Official U.S. government analysis notes that China’s manufacturing share has continued to grow and now accounts for around 30 % of global manufacturing output, underscoring its dominant role in global production networks. China also accounts for over 50 % of global PCB production, making it a central hub for electronics assembly and quality inspection technology demand. This scale of electronics and PCB output means that advanced inspection systems such as 3D AOI are increasingly adopted to maintain quality and reduce defects in high‑volume manufacturing. Government‑backed policy initiatives and investment strategies under Made in China 2025 and similar industrial plans further catalyze the modernization and automation of manufacturing processes.

India’s electronics manufacturing ecosystem is expanding rapidly, with domestic electronics production increasing nearly six‑fold from USD 22.89 billion in 2014–15 to around USD 144.58 billion in 2024–25, reflecting strong industrial growth and value addition. Government projections indicate that India’s overall electronics production is expected to reach USD 300 billion by 2026, highlighting the sector’s strategic importance under national policy initiatives like Make in India and PLI schemes. Electronics exports have also surged, with mobile phone exports growing over 77‑fold from USD 188.7 million in 2014–15 to USD 14.46 billion in 2023–24, demonstrating increased global competitiveness. The sector’s domestic value addition has improved to 18–20 %, supported by targeted incentives and ecosystem development measures aimed at reducing import reliance and boosting local manufacturing. Policy support like the Electronics Components Manufacturing Scheme (ECMS) saw its budget raised to USD 4.82 billion in the Union Budget 2026–27, further accelerating capacity building for components and PCB manufacturing. This momentum in electronics production, exports, and component ecosystem expansion is increasingly driving demand for advanced inspection and automation technologies in India’s PCB assembly and quality‑control landscape.

North America Market Insights

North America leads the overall market revenue of 3D AOI & SPI systems market for PCB Assembly, with an expected share of around 26% by 2036, driven by increasing investments in automation, smart factories, and quality inspection systems. The region continues to focus on improving manufacturing efficiency and product reliability across sectors such as automotive, aerospace, and industrial electronics. Reshoring initiatives and the adoption of advanced PCB assembly technologies further support market expansion. Overall, the market shows consistent growth as manufacturers modernize operations and integrate advanced inspection solutions.

The U.S. manufacturing sector remains a substantive part of the economy, underscoring its broad industrial significance. Within this, the computer and electronic product manufacturing subsector continues to show sustained activity and productivity, reflecting ongoing production engagement in areas such as electronics and components. Recent trends highlight positive productivity growth in electronics‑related manufacturing output as the sector adapts to automation and technological integration. Government‑backed manufacturing support, including modernization initiatives, further reinforces demand for advanced assembly and inspection technologies. As a result, North America’s largest economy continues to drive incremental expansion in high‑precision manufacturing and quality inspection solutions.

Canada’s manufacturing sector, which includes electronics and related products, accounted for more than 10 % of the country’s GDP and roughly USD 174 billion in economic output in 2025, underlining its importance to national industrial growth. The computer and electronic product manufacturing subsector reported increased revenues of USD 18.6 billion in 2023, up 8.6 % from 2022, showing recent year‑on‑year expansion in output. Statistics Canada data also shows rebounds in computer and electronic product manufacturing output, reflecting periodic growth within broader goods‑producing industries. Government initiatives such as federal support for semiconductor and sensor fabrication signal long‑term investment in high‑tech manufacturing capacity. Overall, although the Canadian electronics manufacturing base is smaller than that of the U.S., it continues to strengthen through output growth and strategic industry support, supporting demand for advanced assembly and inspection tools.

Europe Market Insights

The 3D AOI & SPI systems market for PCB assembly in Europe is steadily growing as manufacturers increasingly adopt advanced inspection technologies to meet high-quality and reliability standards. European electronics companies are prioritizing 3D AOI and SPI systems to enhance defect detection, improve process efficiency, and ensure compliance with strict industrial standards. The integration of these systems into automated production lines supports complex PCB assembly across automotive, industrial, and consumer electronics sectors. Hybrid inspection platforms combining 3D AOI with SPI are also gaining traction to provide more comprehensive quality control. Overall, Europe’s focus on precision manufacturing, automation, and smart factory adoption continues to drive growth in this market.

In Germany, the PCB assembly and broader electronics manufacturing market is gradually expanding, supported by high demand from automotive electronics and industrial automation sectors. Local manufacturers are increasingly investing in automated production lines and precision inspection systems to meet stringent quality and reliability requirements amid evolving Industry 4.0 initiatives. Government incentives aligned with the European Chips Act and sector programs help strengthen local electronics and semiconductor capabilities, boosting domestic production infrastructure. EMS providers in Germany are diversifying into turnkey services and advanced prototyping to support complex electronic assemblies and reduce dependency on overseas suppliers. This focus on innovation and resilience continues to support sustained market development in high‑precision assembly and inspection segments.

France’s electronics and PCB manufacturing ecosystem is growing steadily, driven by niche sectors such as automotive, defense, and renewable energy electronics that require advanced circuit boards and reliable quality inspection. Government support through programs like the France 2030 plan and EU‑wide initiatives aims to strengthen local production capacity and integrate modern manufacturing technologies. French companies are modernizing production with automation and quality control systems to improve yields and support emerging demand from IoT, edge computing, and specialized electronics applications. The market’s diversification into energy‑efficient products and stricter regulatory compliance further stimulates investment in high‑precision assembly and inspection tools. Overall, these strategic shifts position France to maintain and grow its role within the European electronics manufacturing landscape.

Key 3D AOI & SPI Systems Market for PCB Assembly Players:

- Camtek Ltd. (Israel)

- GÖPEL electronic GmbH (Germany)

- KLA Corporation (U.S.)

- Koh Young Technology, Inc. (South Korea)

- MIRTEC CO., LTD (South Korea)

- Nordson Corporation (U.S.)

- Omron Corporation (Japan)

- PARMI (Taiwan)

- SAKI CORPORATION (Japan)

- Test Research, Inc. (U.S.)

- Viscom SE (Germany)

- ViTrox Corporation (Malaysia)

- Yamaha Motor Co., Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Camtek is a recognized provider of advanced inspection and metrology systems for semiconductor and PCB manufacturing. Its 3D AOI solutions deliver high‑precision defect detection and measurement, supporting fine‑pitch and complex board inspection requirements. The company integrates automated inspection with process feedback to improve manufacturing yields and cycle times. Camtek’s global presence and strong focus on R&D help drive innovation in quality control technologies.

- KLA is a leading supplier of process control and inspection systems, known for its high‑end metrology and 3D inspection technologies. In the PCB assembly market, KLA’s solutions enhance defect detection accuracy while enabling deep analytics and process optimization. The company leverages its semiconductor inspection expertise to deliver robust AOI and SPI systems tailored to next‑generation electronics. Strong investment in AI and machine learning differentiates its systems for complex, high‑volume production.

- Koh Young is a pioneer in 3D inspection systems, particularly in 3D SPI and 3D AOI for surface mount technology (SMT) lines. Its solutions combine precise 3D measurement with software analytics to detect solder paste and assembly defects at early stages. The company’s technologies help manufacturers minimize waste, improve yield, and reduce rework costs. Koh Young’s focus on smart manufacturing interfaces supports Industry 4.0 integration across global production facilities.

- Omron provides a range of factory automation and vision inspection systems, including 3D AOI for PCB assembly applications. Its inspection platforms are known for high throughput, reliability, and seamless integration with automated production lines. Omron emphasizes system connectivity and data analytics to enhance process control and reduce defect rates. The company’s long history in automation contributes to its strong market positioning in quality inspection.

- ViTrox specializes in vision inspection systems covering 3D AOI, SPI, and intelligent factory solutions. Its product portfolio is designed for flexible and modular deployment across varied PCB assembly environments. ViTrox emphasizes real‑time quality data, analytics, and feedback loops to help manufacturers enhance yield and reduce cycle times. The company’s competitive pricing and strong regional support make it a preferred choice for mid-to-large-scale electronics producers.

Below is the list of the key players operating in the global 3D AOI & SPI systems market for PCB assembly:

Key players in the 3D AOI & SPI systems market are driving growth by continuously innovating inspection technologies to improve accuracy, speed, and integration with smart manufacturing systems. They invest heavily in R&D to develop advanced solutions that address complex PCB assembly challenges, such as miniaturization and high-density components. Collaborations and strategic partnerships enable them to expand global reach and tailor offerings to diverse industry needs. Their focus on automation and quality enhancement helps manufacturers reduce defects, improve yield, and meet rising industry standards, fueling overall market expansion.

Corporate Landscape of the Global 3D AOI & SPI Systems Market for PCB Assembly:

Recent Developments

- In 2026, Koh Young announced it will serve as Premier Sponsor of the IPC APEX EXPO 2026 (March 16–19, Anaheim), where it plans to showcase its latest AI‑powered inspection and software solutions designed to help electronics manufacturers improve stability and productivity amid rising quality demands and tighter tolerances. The company highlighted that multiple new machine platforms and major feature upgrades will debut live at the event to demonstrate next‑generation capabilities for inspection and process control.

- In August 2025, ViTrox unveiled its next‑generation Smart 3D AOI solutions, introducing three new systems, including the V510Ai DST Smart 3D AOI, tailored for back‑end assembly processes such as selective soldering and post‑THT wave soldering. These platforms are designed to meet modern electronics manufacturing needs and have been recognized with industry awards, underscoring their advanced inspection performance for complex PCB production.

- Report ID: 8507

- Published Date: Apr 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2036

Copyright @ 2026 Research Nester. All Rights Reserved.