Thermally Conductive Filler Dispersants Market Outlook:

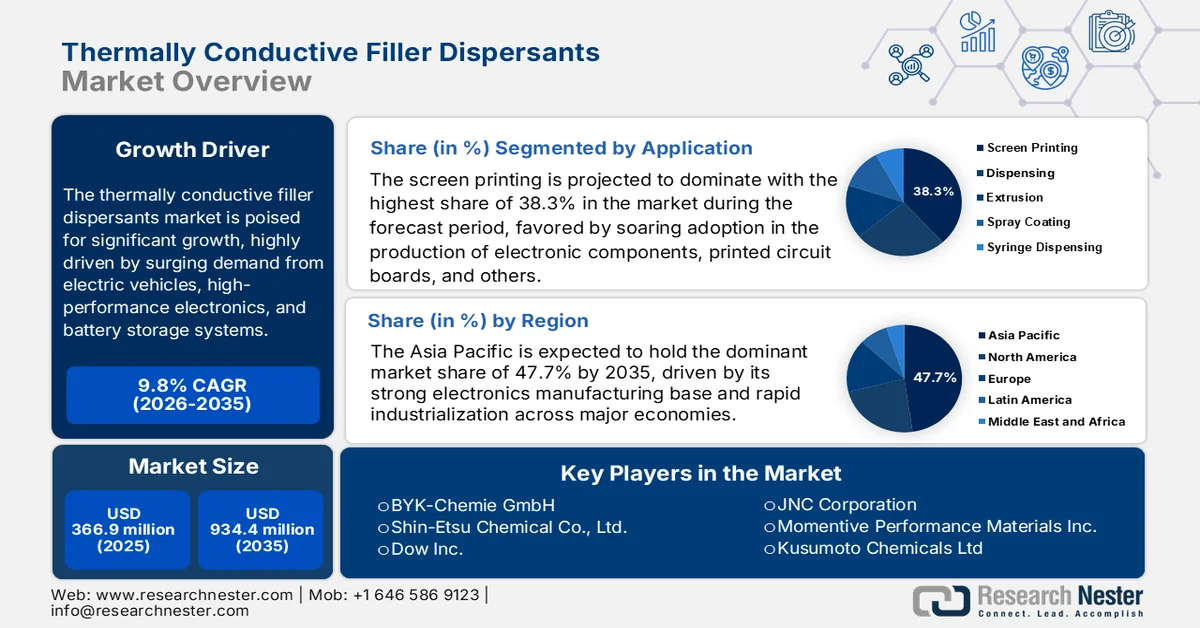

Thermally Conductive Filler Dispersants Market size was valued at USD 366.9 million in 2025 and is anticipated to exceed USD 934.4 million by the end of 2035, registering over 9.8% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of thermally conductive filler dispersants is evaluated at USD 402.8 million.

The global thermally conductive filler dispersants market is poised for solid growth in the next decade as it focuses on materials and additives used to improve the dispersion of thermally conductive fillers such as alumina, boron nitride, aluminum nitride, and silica within polymers, adhesives, and composites. These dispersants help achieve uniform particle distribution, reduce agglomeration, and enhance heat transfer efficiency in end use materials. For instance, the January 2025 article published by the U.S. Geological Survey revealed that in 2024, U.S. boron production was carried out by three companies in southern California, with most boron products being consumed domestically, and production levels increased when compared to 2023. The leading producer mined borate ores such as kernite, tincal, and ulexite through open-pit methods and supplied downstream processing plants producing boric acid, sodium borate, and specialty glass and ceramic raw materials. Meanwhile, another company used solution mining, and a third began similar operations in January 2024, thus positively contributing to the market’s expansion.

Boron Shipment Statistics in the U.S. 2022-2024: Imports, Exports, Prices, and Employment Trends

|

Statistic |

2022 |

2023 |

2024 |

|

Imports - Refined borax |

168 |

156 |

160 |

|

Imports - Boric acid |

48 |

38 |

42 |

|

Imports - Colemanite (calcium borates) |

1 |

2 |

1 |

|

Imports - Ulexite (sodium borates) |

38 |

20 |

37 |

|

Exports - Boric acid |

239 |

253 |

240 |

|

Exports - Refined borax |

651 |

604 |

590 |

|

Consumption (apparent) |

W |

W |

W |

|

Average import price (USD/ton, CIF) |

485 |

606 |

560 |

|

Employment (number) |

1,400 |

1,430 |

1,500 |

Source: USGS

Key Thermally Conductive Filler Dispersants Market Insights Summary:

Regional Highlights:

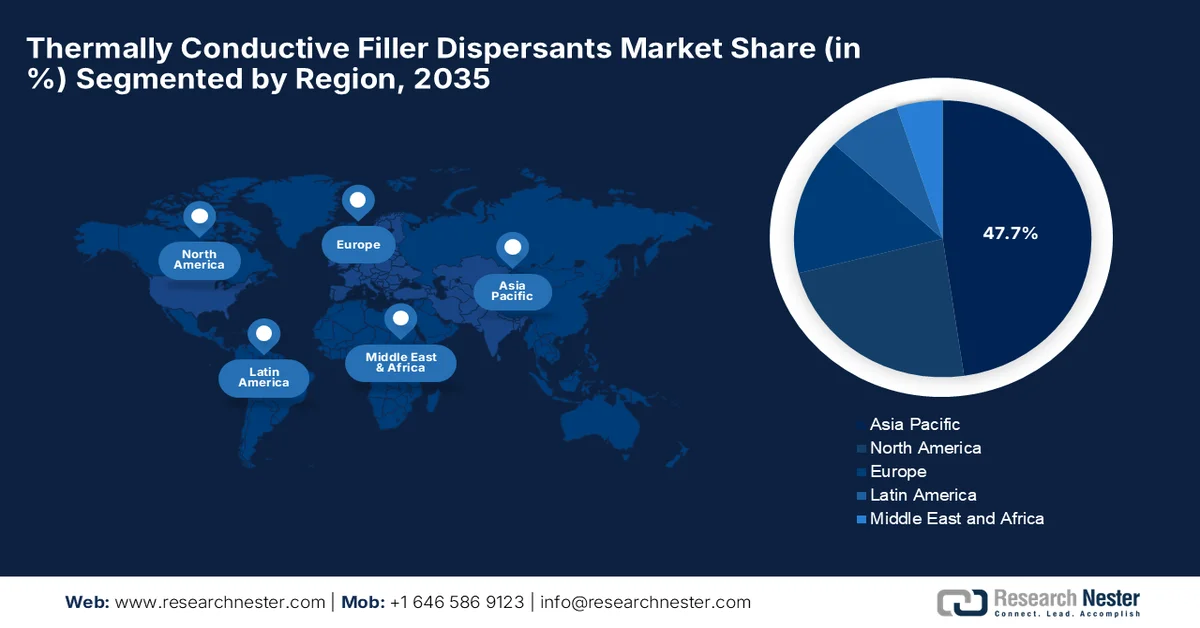

- Asia Pacific is projected to secure a 47.7% share by 2035 in the thermally conductive filler dispersants market, underpinned by rapid expansion of electronics manufacturing and rising demand for compact high-power electronic devices requiring efficient heat dissipation

- North America is anticipated to witness the fastest growth in the forecast period, accelerated by expanding semiconductor manufacturing, advanced electronics development, and increasing deployment of specialized thermal material formulations

Segment Insights:

- The screen printing segment is expected to command a 38.3% share by 2035 in the thermally conductive filler dispersants market, fueled by growing utilization across electronic components, printed circuit boards, thermal interface materials, and advanced electronic device manufacturing

- Metal-based fillers are forecast to capture a considerable revenue share by 2035, reinforced by superior thermal conductivity and increasing integration into advanced thermal interface materials, conductive pastes, adhesives, and encapsulation compounds

Key Growth Trends:

- Growth of electric vehicles and hybrid systems

- Expansion of 5G infrastructure and high-performance computing

Major Challenges:

- High cost of raw materials and formulation development

- Technical challenges in achieving high filler loadings

Key Players: BYK-Chemie GmbH (Germany),Shin-Etsu Chemical Co., Ltd. (Japan),Dow Inc. (U.S.),JNC Corporation (Japan),Momentive Performance Materials Inc. (U.S.),Kusumoto Chemicals Ltd. (Japan),Evonik Industries AG (Germany),Croda International Plc (United Kingdom),Lubrizol Corporation (U.S.),Wacker Chemie AG (Germany),Henkel AG & Co. KGaA (Germany),DuPont de Nemours, Inc. (U.S.),3M Company (U.S.),Saint-Gobain (France),Carbice (U.S.) ,Noctua (Austria),Indium Corporation (U.S.),LyondellBasell Industries N.V. (Netherlands),Dexerials Corporation (Japan),Denka Company Limited (Japan),H.B. Fuller Company (U.S.),Elkem ASA (Norway).

Global Thermally Conductive Filler Dispersants Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 366.9 million

- 2026 Market Size: USD 402.8 million

- Projected Market Size: USD 934.4 million by 2035

- Growth Forecasts: 9.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (47.7% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Singapore, Vietnam, Canada, United Arab Emirates

Last updated on : 10 June, 2026

Thermally Conductive Filler Dispersants Market - Growth Drivers and Challenges

Growth Drivers

- Growth of electric vehicles and hybrid systems: This is the primary growth catalyst for the thermally conductive filler dispersants market. The EV batteries, power electronics, and charging systems generate substantial heat that needs to be managed effectively. These dispersants readily enhance thermal interface materials, which improve battery performance, energy efficiency, and overall lifespan of automotive electrical systems. As per the article published by the International Energy Agency, global electric car sales surged past 20 million in 2025, which makes up 25% of all new cars sold worldwide and displaces 1.2 million barrels of oil per day. The report also underscored that China led with over 13 million EVs sold, which is nearly 55% of its new car market, whereas Europe rebounded strongly with 4.2 million sales driven by stricter CO₂ standards. The U.S. remained steady at just under 10%, whereas the emerging markets such as Türkiye and Nepal witnessed consistent growth, reflecting the global momentum toward electrification.

- Expansion of 5G infrastructure and high-performance computing: The modern consumer electronics, which include smartphones, laptops, gaming consoles, and 5G infrastructure equipment, are becoming more compact and are processing significantly more data. Therefore, this intense miniaturization leaves little physical room for heat dissipation, which in turn leads to high-temperature localized hotspots. As per an article published by the Organization for Economic Co-operation and Development (OECD) in October 2025, the rollout of 5G across OECD countries has transformed mobile connectivity, delivering faster speeds and lower latency. By 2024, 5G made up 37% of all mobile broadband subscriptions, wherein Denmark, Hungary, and Korea lead the adoption at 78.5%, 57%, and 55%. Mobile broadband penetration also soared, with Japan and the U.S. exceeding 200 subscriptions per 100 inhabitants, far above the OECD average of 140, thus heightening the demand in the thermally conductive filler dispersants market.

- Growth of data centers and cloud computing: The spur in digitalization and cloud computing is catalyzing the growth of data centers. These facilities consist of high-density servers that produce considerable amounts of thermal loads. Thermally conductive filler dispersants are considered to be essential components in thermal interface materials since they help to maintain optimal operating temperatures. For instance, the article published by the UN Trade & Development in January 2026 reported that Data centers captured over one‑fifth of global greenfield investment in 2025, with announced FDI exceeding USD 270 billion, owing to the heightened demand for AI infrastructure and digital networks. This surge lifted overall global FDI by 14% to USD 1.6 trillion. For the first time, telecommunications investment, powered by data centers, surpassed renewable energy in value, thus denoting an encouraging opportunity for thermally conductive filler dispersants market.

Global Data Centre FDI Investment Leaders 2025

|

Country |

Investment (USD billions) |

|

France |

69 |

|

U.S. |

29 |

|

Republic of Korea |

21 |

Source: UNCTAD

Challenges

- High cost of raw materials and formulation development: One of the extremely challenging factors hampering growth in the thermally conductive filler dispersants market is the high cost associated with the raw materials and formulation development. Effective thermal management systems require premium fillers such as boron nitride, graphene, aluminum nitride, and specialized ceramic materials, which readily increase the production costs. In addition, dispersants need to be properly orchestrated to gain compatibility with specific fillers as well as polymer matrices, thereby maintaining thermal performance and processing efficiency. Apart from this extensive research, testing, and validation are essential to optimize formulations for applications in electronics, electric vehicles, and semiconductors. Therefore, these development costs can be high for smaller manufacturers with limited resources.

- Technical challenges in achieving high filler loadings: Achieving high filler loadings and maintaining acceptable processing characteristics is a major challenge for manufacturers who are involved in the thermally conductive filler dispersants market. These materials sometimes necessitate very high concentrations of conductive fillers to reach target thermal conductivity levels. Therefore, increasing filler content can dramatically raise viscosity, making mixing, dispensing, molding, and coating processes more difficult. On the other hand, poor dispersion can lead to particle agglomeration, inconsistent thermal performance, and reduced mechanical properties. In this context, manufacturers need to balance thermal conductivity, flow behavior, stability, and end use performance, making product development extremely challenging as thermal management requirements continue to become more demanding.

Thermally Conductive Filler Dispersants Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.8% |

|

Base Year Market Size (2025) |

USD 366.9 million |

|

Forecast Year Market Size (2035) |

USD 934.4 million |

|

Regional Scope |

|

Thermally Conductive Filler Dispersants Market Segmentation:

Application Segment Analysis

The screen printing, which is under the application segment, is projected to dominate with the highest share of 38.3% in the thermally conductive filler dispersants market during the forecast period. The segment’s dominance is majorly favored by soaring adoption in the production of electronic components, printed circuit boards, thermal interface materials, and advanced electronic devices. Screen printing offers a very precise and uniform deposition of thermally conductive materials and supports high production efficiency. For instance, in January 2023, Celanese Micromax™ Conductive Inks announced nine new product grades at IPC APEX EXPO. This new PE800 series targets consumer applications such as touch sensors and EMI shielding, whereas the HT series addresses high-temperature needs, thus denoting a wider segment scope.

Type Segment Analysis

By the conclusion of the forecast period, metal-based fillers are anticipated to hold a considerable revenue share in the thermally conductive filler dispersants market. The growth of the segment is largely attributable to the superior thermal conductivity that is provided by metal-based fillers such as silver, copper, aluminum, and nickel, which enable efficient heat dissipation in different categories. In addition, their ability to provide enhanced thermal management while maintaining electrical and mechanical performance has increased their adoption in advanced thermal interface materials, conductive pastes, adhesives, and encapsulation compounds. In August 2024, Sumitomo Bakelite Co., Ltd. began sample shipments of its new silver sintering paste with a high thermal conductivity of 150 W/m·K, which is designed for next-generation power semiconductors. Besides, this innovation replaces lead solder, reduces environmental impact, and enhances SiC semiconductor performance by improving heat dissipation.

End use Segment Analysis

In the end use segment, electronics & electrical is expected to show lucrative growth opportunities in the thermally conductive filler dispersants market during the discussed timeframe. The segment’s growth is fueled by rising investments in semiconductor fabrication facilities, expansion of AI and cloud computing infrastructure, and rising deployment of 5G communication networks. These developments are driving higher consumption of electronic materials, including thermal interface materials, encapsulants, and conductive formulations. In January 2024, the National Institute for Materials Science, Sumitomo Metal Mining, N.E. CHEMCAT, and Priways announced the joint development of a thick-film conductive ink that is suitable for large-area, large-current printed electronics. It uses copper particles and metal complex inks, and the innovation enables controllable thickness, low-temperature sintering, and improved oxidation resistance.

Our in-depth analysis of the thermally conductive filler dispersants market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Type |

|

|

End use |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Thermally Conductive Filler Dispersants Market - Regional Analysis

APAC Market Insights

The thermally conductive filler dispersants market in the Asia Pacific is forecasted to attain the highest share of 47.7% during the forecast period. The region’s progress in this field is characterized by a massive electronics manufacturing ecosystem and industrialization in key nations such as China, Japan, South Korea, and India. Escalating consumer demand for increasingly compact, high-power electronics such as smartphones, smart home devices, and high-performance computing platforms heightens the adoption of these dispersants to optimize heat dissipation. For instance, in July 2023, JX Metals Corporation, in collaboration with AIST, achieved world-leading fine copper wiring formation of 6 μm using screen offset printing. These breakthrough advancements in terms of printed electronics enable further miniaturization of smartphones and wearables while reducing energy and material consumption, thus suitable for bolstering the market’s growth.

The nation’s largest and unparalleled industrial production capabilities have positioned China thermally conductive filler dispersants market at the forefront of growth in the regional market. The country’s market is heavily dependent on chemical wetting and dispersing additives to integrate heavy loads of thermally conductive materials and advanced carbon nanomaterials into matrix systems for heat-sink compounds and thermal interface materials. Most notably, China's world-leading production of electric vehicles, lithium-ion batteries, and automated energy storage systems acts as the primary catalyst for specialized dispersants. As per an article published by CSIS Organization in July 2025, the country’s exponential rise in terms of EV exports is deliberately reshaping mobility in emerging economies, which offers affordable models and accelerating adoption where demand was once limited. In addition, this surge is driving industrial policy experimentation, wherein the governments are leveraging the energy transition to boost domestic industries and reduce reliance on internal combustion vehicles, thus denoting an encouraging opportunity for the thermally conductive filler dispersants market to grow.

The manufacturing initiatives, such as Make in India and a massive push toward domestic electronics hardware production, are allowing the transformative growth of the thermally conductive filler dispersants market in India. Growth in the country’s market is heavily propelled by the surging consumer electronics sector, accelerating localization of smartphone and appliance assembly, and the extensive upgrade of telecommunications networks and data center facilities. As per an article published by Press Information Bureau (PIB) in March 2026, India has emerged as the world’s second-largest mobile manufacturing country, making a huge transformation from a net importer to a net exporter of smartphones under the Make in India and Atmanirbhar Bharat vision. The report also states that mobile phone production rose to USD 66 billion in 2024-25, which is a 28-fold increase, whereas the exports of mobile phones surged to USD 24 billion, which is a 127-fold jump. Government initiatives such as PLI schemes, electronics manufacturing clusters, and component manufacturing programs have driven exponential growth in production and exports, contributing to wider thermally conductive filler dispersants market expansion.

North America Market Insights

The North America thermally conductive filler dispersants market is poised to grow at the fastest rate over the forecasted years. The region’s expansion in this field is mainly propelled by the strong presence of semiconductor manufacturers, advanced electronics producers, aerospace companies, and electric vehicle technology developers. The innovations in chip design, advanced packaging technologies, and high-performance computing systems are increasing the use of specialized material formulations that require effective filler dispersion. For instance, in April 2024, Micron Technology announced a major CHIPS and Science Act funding agreement of USD 6.1 billion from the U.S. Department of Commerce with a main goal to support the construction of advanced memory semiconductor fabs in Idaho and New York. This particular investment is aimed at significantly expanding domestic semiconductor manufacturing capacity to meet rising demand from different applications. This expansion deliberately strengthens the U.S. electronics and electrical ecosystem, thereby driving increased demand for electronic materials used in semiconductor packaging and production processes.

The expansion in semiconductor manufacturing, advanced packaging technologies, and high-performance electronics production is responsible for reshaping the growth dynamics of the U.S. thermally conductive filler dispersants market. Also, the rising complexity of miniaturized electronic components and performance requirements in aerospace, defense, and telecommunications sectors are enhancing the demand for advanced material formulations across the country. The U.S. Department of Commerce in November 2024 reported that the Biden-Harris Administration has awarded TSMC Arizona almost USD 6.6 billion in direct funding under the CHIPS Incentives Program to support its USD 65 billion investment in three advanced semiconductor fabs in Phoenix. This marks the largest foreign direct investment in a U.S. greenfield project, expected to produce A16 technology chips, thus contributing to wider market expansion.

The escalating demand for high-performance heat dissipation in consumer electronics and advanced telecommunications infrastructure is the main factor driving the growth of Canada thermally conductive filler dispersants market. Domestic manufacturers have an increased priority towards the development of non-silicone and innovative silicone-based formulations to improve overall filler loading capacity, lower viscosity, and enhance processing stability. Based on the government data published in March 2023, it generously invested USD 36 million through the Strategic Innovation Fund in Ranovus Inc. in order to support a USD 100 million project advancing domestic semiconductor manufacturing. In addition, this initiative will expand Ranovus’s workforce to 200 employees, provide opportunities to 150 co-op students, and generate around 40 new patents.

Europe Market Insights

The Europe thermally conductive filler dispersants market has acquired a prominent position in the global dynamics owing to the stringent thermal management needs in automotive electrification and telecommunications. Apart from this, the region's strict emphasis on industrial sustainability shifts manufacturing toward eco-friendly, bio-based, and low-VOC chemical formulations. Denoting the same in June 2024, Evonik has commissioned a new plant at Rheinfelden for its AEROSIL® Easy-to-Disperse silicas to enhance the global supply of high-quality fumed silica. The company also notes that this innovative technology simplifies paint and coating formulations by reducing dispersion to a single step, saving time, energy, and costs. Hence, such instances reflect that the region is advancing efficient and sustainable dispersant technologies that enhance filler dispersion and support high-performance thermal materials across different applications.

The prominent automotive engineering sector and its strong transition toward electric mobility are responsibly uplifting the thermally conductive filler dispersants market in Germany. The market is highly driven by strict compliance with regional environmental mandates, which is leading to a shift toward halogen-free, low-emission, and sustainable polymeric structures, providing encouraging opportunities for pioneers in this field. In May 2026, Henkel announced the expansion of its EV battery thermal management portfolio with two new materials, i.e., Bergquist TGF 2030APS, which is a silicone-free thermal gap filler with 1.7 W/m·K conductivity, and Loctite TLB 9270APS, a polyurethane-based adhesive offering 2 W/m·K conductivity. The company also notes that these solutions improve heat dissipation, bonding strength, and production efficiency, thereby supporting sustainability through low-energy curing and solvent-free formulations.

The UK thermally conductive filler dispersants market is developing at a steady pace, which is propelled by the domestic expansion of aerospace engineering, defense applications, and specialized electric vehicle manufacturing. Local product innovation is highly focused on high-purity, low-emission, and halogen-free polymeric dispersants to align with strict national environmental standards and material compatibility needs. For instance, in October 2023, the UK government, along with industry, announced a total of USD 108 million in funding for 20 groundbreaking net-zero tech projects, which include hydrogen-powered off-road vehicles, lithium scale-up plants, and advanced EV battery systems. The government data also revealed that out of this USD 55 million comes from government support, matched by USD 53 million from the automotive sector, hence denoting a lucrative growth opportunity.

Key Thermally Conductive Filler Dispersants Market Players:

- BYK-Chemie GmbH (Germany)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Dow Inc. (U.S.)

- JNC Corporation (Japan)

- Momentive Performance Materials Inc. (U.S.)

- Kusumoto Chemicals Ltd. (Japan)

- Evonik Industries AG (Germany)

- Croda International Plc (United Kingdom)

- Lubrizol Corporation (U.S.)

- Wacker Chemie AG (Germany)

- Henkel AG & Co. KGaA (Germany)

- DuPont de Nemours, Inc. (U.S.)

- 3M Company (U.S.)

- Saint-Gobain (France)

- Carbice (U.S.)

- Noctua (Austria)

- Indium Corporation (U.S.)

- LyondellBasell Industries N.V. (Netherlands)

- Dexerials Corporation (Japan)

- Denka Company Limited (Japan)

- H.B. Fuller Company (U.S.)

- Elkem ASA (Norway)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BYK-Chemie GmbH is a subsidiary of ALTANA AG, which is one of the most prominent suppliers of specialty additives and dispersing agents globally. The company has established a strong position in the thermally conductive filler dispersants market through its portfolio of wetting and dispersing additives, especially designed for highly filled systems containing aluminum oxide, boron nitride, graphite, and other conductive fillers.

- Shin-Etsu Chemical Co., Ltd. is a foundational player and a leading supplier of silicone materials, thermal interface materials, and specialty chemical products. Besides, the firm deliberately leverages its expertise in silicone chemistry to develop thermally conductive compounds and formulations that require efficient filler dispersion technologies.

- Dow Inc. is yet another major player that supplies a wide range of thermal management materials used in electronics, automotive, and industrial sectors. The company deeply emphasizes innovation in high-performance formulations that are well capable of accommodating elevated filler concentrations while maintaining processability and reliability.

- Evonik Industries AG is recognized for its specialty additives and dispersant technologies that enable efficient incorporation of thermally conductive fillers into polymer matrices. The company has strengthened its thermally conductive filler dispersants market position through the development of certain dispersing agents that are suitable for high-loading thermal interface materials used in electric vehicle batteries and power electronics.

- Momentive Performance Materials Inc. is a leading supplier of silicone-based specialty materials, which are suitable for electronics, automotive, aerospace, and industrial markets. The company is highly focused on continued innovation of products, customer-suitable solutions, and expansion into electric vehicles, renewable energy systems, and advanced electronics.

Below is the list of some prominent players operating in the global thermally conductive filler dispersants market:

The thermally conductive filler dispersants market is a moderately consolidated landscape that hosts global specialty chemical manufacturers, silicone material suppliers, and advanced thermal management solution providers who are competing in terms of innovation and application expertise. Apart from this, the leading companies in this field are highly focused on developing dispersants that enable higher filler loadings, improved thermal conductivity, and enhanced processing performance for electronics, electric vehicles, semiconductors, and industrial applications. Major players in the sector are opting for investments in research and development, expansion of thermal interface material portfolios, development of sustainable and low-VOC formulations, and collaborations with OEMs and electronics manufacturers. Furthermore, companies are also advancing boron nitride, aluminum oxide, and graphene-based thermal management technologies with the main goal to address increasing heat dissipation requirements in electronic and electrification applications.

Corporate Landscape of the Thermally Conductive Filler Dispersants Market:

Recent Developments

- In June 2026, Carbice and Noctua entered into a tactical partnership to bring Carbice’s advanced carbon nanotube thermal pads to the DIY PC cooling market, with Noctua handling exclusive retail distribution and future product collaboration.

- In May 2026, Henkel expanded its EV battery thermal management portfolio with two new thermal interface materials, which are the Bergquist TGF 2030APS gap filler and the Loctite TLB 9270APS adhesive. These solutions improve heat dissipation, support high‑volume production, and enhance sustainability.

- Report ID: 7357

- Published Date: Jun 10, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.