Surgical Equipment Market Outlook:

Surgical Equipment Market size was over USD 20.4 billion in 2025 and is expected to reach USD 52.1 billion by the end of 2035, growing at around 9.8% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of surgical equipment is estimated at USD 22.4 billion.

The surgical equipment market is supported by sustained growth in surgical procedure volumes, expansion of hospital infrastructure, and increasing public investment in healthcare systems. According to the NLM September 2022 study, an estimated 313 million surgical procedures are performed globally each year, highlighting the scale of demand for operating room instruments, visualization systems, electrosurgical devices, and related equipment. Healthcare expenditure continues to rise across major economies, creating favorable procurement conditions for surgical equipment suppliers. Data from the Organization for Economic Co-operation and Development (OECD) November 2025 data show that health spending accounts for approximately 9% of GDP on average across OECD countries, with several markets exceeding this level.

Aging demographics are another important demand factor. NLM July 2023 projects that the global population aged 60 years and older will increase from 1 billion in 2020 to 1.4 billion by 2030, contributing to higher volumes of orthopedic, cardiovascular, ophthalmic, and general surgical procedures. Public-sector efforts to improve access to surgical care are also increasing equipment requirements. The WHO and partner organizations have repeatedly identified surgical services as a critical component of universal health coverage, encouraging investments in operating theaters, sterilization capacity, and perioperative infrastructure across both developed and emerging healthcare systems.

Key Surgical Equipment Market Insights Summary:

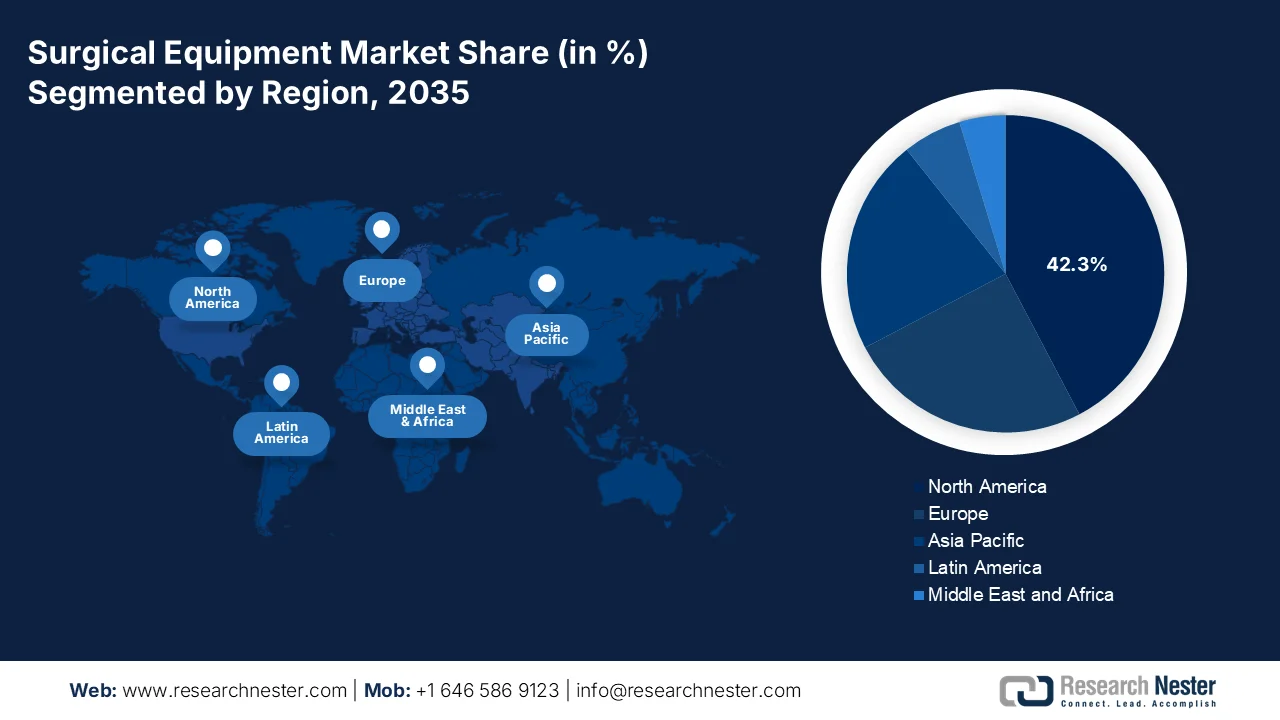

Regional Highlights:

- North America is anticipated to command 42.3% of the surgical equipment market revenue by 2035, underpinned by an advanced healthcare ecosystem, high procedural volumes, and early adoption of cutting-edge technologies

- Asia Pacific is set to witness accelerated expansion in the forecast period 2026-2035, stimulated by rapid healthcare infrastructure expansion, rising medical tourism, and increasing affordability of advanced surgical care

Segment Insights:

- The surgical sutures & staplers segment in the surgical equipment market is projected to capture 45.7% share by 2035, supported by the growing usage in wound closure process

- Cardiovascular surgery is expected to remain the leading application segment throughout 2026-2035, bolstered by the escalating global burden of coronary artery disease, valvular disorders, and heart failure

Key Growth Trends:

- Rising government healthcare expenditure

- Expansion of universal health coverage programs

Major Challenges:

- Stringent regulatory approvals

- Complex Supply Chain & Raw Material Sourcing

Key Players: Toray Industries (Japan), Teijin Limited (Japan), Mitsubishi Chemical Group (Japan), Solvay S.A. (Belgium), SGL Carbon SE (Germany), Johnson & Johnson (U.S.), Stryker (U.S.).

Global Surgical Equipment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 20.4 billion

- 2026 Market Size: USD 22.4 billion

- Projected Market Size: USD 52.1 billion by 2035

- Growth Forecasts: 9.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Australia, United Arab Emirates

Last updated on : 29 June, 2026

Surgical Equipment Market - Growth Drivers and Challenges

Growth Drivers

- Rising government healthcare expenditure: Government healthcare spending remains one of the strongest demand drivers for surgical equipment procurement. Higher public health budgets directly support operating room modernization, surgical instrument replacement, and expansion of hospital infrastructure. According to the AMA April 2025 data, U.S. national health expenditure reached USD 4.9 trillion in 2023, accounting for 17.5% of GDP, creating substantial purchasing capacity for advanced surgical systems and operating room technologies. The investments are increasing procurement of surgical equipment across public hospitals and ambulatory surgery centers. Additionally, many developing countries are directing healthcare budgets toward expanding surgical access and reducing procedure backlogs. For manufacturers, public-sector tenders and hospital modernization programs represent long-term revenue opportunities, particularly in countries implementing healthcare infrastructure upgrades and national surgical care expansion strategies.

- Expansion of universal health coverage programs: Governments worldwide are expanding universal health coverage (UHC) programs, increasing patient access to surgical care and boosting demand for surgical equipment. WHO December 2025 data estimates that approximately 4.6 billion people lack full access to essential health services, prompting national investments in healthcare accessibility. Increased reimbursement coverage encourages hospitals to expand operating room capacity and invest in modern surgical technologies. Public procurement programs associated with UHC implementation are creating significant opportunities for equipment manufacturers. The trend is particularly important in emerging economies where surgical infrastructure historically lagged demand, resulting in large unmet procedural needs.

Challenges

- Stringent regulatory approvals: Obtaining regulatory clearance is a protracted, expensive process requiring exhaustive clinical evidence and quality system compliance. New entrants lack in-house regulatory expertise, leading to submission rejections and delayed market access. The evolving EU Medical Device Regulation (MDR) imposes additional classification and post-market surveillance burdens, making Europe particularly challenging for smaller players without dedicated regulatory teams.

- Complex Supply Chain & Raw Material Sourcing: Medical-grade raw materials such as titanium, PEEK, and specialty polymers require rigorous traceability and certification. New manufacturers face supplier resistance due to low initial order volumes. Geopolitical disruptions, logistics bottlenecks, and single-source dependencies amplify risks, while maintaining buffer inventory strains working capital for companies with limited financial reserves.

Surgical Equipment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.8% |

|

Base Year Market Size (2025) |

USD 20.4 billion |

|

Forecast Year Market Size (2035) |

USD 52.1 billion |

|

Regional Scope |

|

Surgical Equipment Market Segmentation:

Product Type Segment Analysis

Under the product type segment, the surgical sutures & staplers are dominating and is poised to hold the share value of 45.7% by the end of 2035. The segment is driven due to the growing usage in wound closure process. According to the NLM September 2024 study, posterior spine surgery registry reveals that sutures are used nearly three times more frequently than staples (72.7% vs. 27.3%, p<0.01), reflecting surgeon preference for wound closure in complex spinal procedures. However, the choice of closure device significantly impacts infection outcomes—univariate analysis showed higher SSI rates with sutures (53.6%) compared to staples (40.5%, p=0.04) in propensity-matched cohorts. Notably, fusion procedures were more common in the staples group (44% vs. 27.2%, p<0.01), suggesting case-selection bias. Readmission and reoperation rates remained comparable across both groups at 30-day, 90-day, and 1-year intervals, reinforcing that both sutures and staples remain viable options when appropriately indicated.

Application Segment Analysis

In the surgical equipment market's application segment, cardiovascular surgery emerges as the leading sub-segment, driven by the escalating global burden of coronary artery disease, valvular disorders, and heart failure. Advanced robotic-assisted bypass systems, hybrid operating rooms, and transcatheter aortic valve replacement (TAVR) devices are fueling equipment demand. According to the CDC's May 2023 data, heart disease remains the leading cause of death in the United States, accounting for 699,659 deaths in 2022, sustaining urgent surgical interventions. Additionally, the NIH reports that cardiac catheterizations are performed annually, each requiring specialized guidewires, closure devices, and imaging-compatible surgical tables. The growing adoption of minimally invasive cardiac procedures, coupled with favorable CMS reimbursement policies for robotic-assisted cardiovascular surgeries, with hospitals prioritizing capital investments in advanced cardiac surgical suites.

End user Segment Analysis

Within the surgical equipment market's end user segment, hospitals maintain the largest revenue share, driven by their high-volume surgical volumes, multi-specialty capabilities, and substantial capital budgets for robotic systems, navigation platforms, and energy devices. Hospitals leverage group purchasing organizations (GPOs) to procure bundled equipment packages, ensuring cost efficiency while maintaining cutting-edge technology. According to the NLM November 2023 data, U.S. hospitals performed approximately 40 to 50 million inpatient surgical procedures, underscoring the immense consumption of both reusable capital equipment and single-use consumables. Furthermore, the CMS (2025) reports that Medicare-reimbursed surgical procedures, reinforcing their dominant position. Teaching hospitals additionally invest in simulation-based surgical trainers and smart ORs with IoT-enabled tracking.

Our in-depth analysis of the surgical equipment market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Application |

|

|

End user |

|

|

Technology |

|

|

Usability |

|

|

Material |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Surgical Equipment Market - Regional Analysis

North America Market Insights

North America is dominating the surgical equipment market and is projected to hold the regional revenue share of 42.3% by the end of 2035. The region is driven by the advanced healthcare ecosystem, high procedural volumes, and early adoption of cutting-edge technologies. The region benefits from robust hospital infrastructure, significant public and private healthcare spending, and a strong presence of leading medtech manufacturers. Key trends include the accelerating shift toward outpatient surgical settings, increasing preference for single-use sterile instruments to minimize cross-contamination, and growing integration of artificial intelligence and robotic assistance in operating rooms. However, manufacturers face persistent pricing pressures from group purchasing organizations and government-funded healthcare programs, compelling continuous innovation and cost optimization to maintain market competitiveness while meeting stringent regulatory standards.

The rising procedure demand supported by a growing patient base and increasing disease burden is shaping the market in the U.S. A major demand contributor is the expansion of the Medicare population, with the Common Wealth Fund October 2025 reporting that more than 68 million Americans were enrolled in Medicare, increasing utilization of surgical services related to cardiovascular disease, orthopedics, ophthalmology, and oncology. In addition, the NLM study in October 2025 shows that nearly 818 985 surgical procedures were performed, reinforcing demand for surgical instruments, electrosurgical systems, stapling devices, and operating-room equipment used across cancer care pathways. The combination of an aging beneficiary population and rising incidence of conditions requiring surgical intervention is expected to sustain procurement activity across both public and private healthcare facilities.

The increasing healthcare investment and rising surgical service utilization across provincial healthcare systems is shaping the market in Canada. According to the Insurance Portal December 2024 data, total health spending in Canada reached CAD 372 billion in 2024, equivalent to approximately CAD 9,054 per person, reflecting continued investment in hospital infrastructure, operating rooms, and medical technologies that support surgical care. Additionally, data from Government of Canada September 2024 data indicate that the population aged 65 years and older surpassed 7.8 million, accounting for nearly one-fifth of the national population and contributing to higher demand for surgical procedures related to orthopedic disorders, cardiovascular disease, cataracts, and cancer treatment. These demographic and healthcare expenditure trends continue to create a favorable procurement environment for surgical equipment suppliers serving Canada's hospital and specialty care sectors.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the surgical equipment market. The region is driven by rapid healthcare infrastructure expansion, rising medical tourism, and increasing affordability of advanced surgical care. Countries like China, India, and Japan are witnessing substantial modernization of public hospitals and the proliferation of private specialty surgical centers. Key trends include growing adoption of robotic-assisted and minimally invasive procedures, localization of manufacturing to reduce import dependence, and government-led initiatives to improve surgical access in rural and semi-urban areas. However, manufacturers encounter pricing sensitivity, fragmented regulatory landscapes, and intense competition from low-cost domestic producers, necessitating region-specific product portfolios, strategic partnerships, and tiered pricing strategies to effectively penetrate diverse Asian healthcare markets.

The growing role as a medical device manufacturing and export hub is shaping the market in India. According to the OEC 2024 data under HS4 Code 9018, India exported USD 1.5 billion worth of medical instruments in 2024, ranking 47th globally, with the United States accounting for USD 302 million of exports. This export performance reflects increasing production capacity and international demand for Indian-made medical and surgical devices. Alongside government initiatives such as the Production Linked Incentive (PLI) Scheme for medical devices and ongoing healthcare infrastructure expansion, rising exports are strengthening domestic manufacturing capabilities and improving the availability of surgical equipment across hospitals and specialty care facilities in India.

The strong manufacturing and export capabilities in medical devices is driving the market in China. According to OEC 2024 data under HS4 Code 9018, China exported approximately USD 13.5 billion worth of medical instruments in 2024, making it one of the world's leading exporters in this category. The robust export performance reflects China's extensive production infrastructure, established supply chains, and growing technological capabilities in medical device manufacturing. Combined with continued healthcare infrastructure expansion and increasing demand from domestic hospitals, the strong export base supports economies of scale and innovation across the surgical equipment sector. As healthcare modernization efforts continue, China's position as both a major consumer and global supplier of surgical equipment is expected to strengthen further.

Europe Market Insights

Europe represents a mature and highly regulated surgical equipment market, characterized by universal healthcare coverage, stringent quality standards, and strong emphasis on patient safety. The region's market is shaped by the Medical Device Regulation (MDR), which imposes rigorous clinical evaluation and post-market surveillance requirements, driving consolidation among manufacturers. Key trends include rising adoption of minimally invasive and robotic-assisted surgeries, growing demand for single-use devices to curb hospital-acquired infections, and increasing focus on sustainable, recyclable surgical materials. However, manufacturers face reimbursement constraints, fragmented procurement across national health systems, and pricing pressures from centralized purchasing bodies. Innovation partnerships between academic institutions and medtech firms remain strong across Germany, France, and the UK.

The strong healthcare investment and high patient utilization across its hospital system is driving the market in the UK. According to World Bank December 2025 data, healthcare expenditure accounted for approximately 12.27% of Germany's GDP in 2024, highlighting the country's commitment to funding healthcare services and medical technology. Additionally, German hospitals treated around 16.8 million inpatient cases, reflecting substantial demand for surgical interventions and associated equipment such as electrosurgical devices, sutures, staplers, and handheld instruments, as per the Deutsche Krankenhausgesellschaft. The combination of significant healthcare spending and a large inpatient population continues to support procurement of advanced surgical technologies, operating room upgrades, and replacement of existing equipment across Germany's healthcare sector.

Key Surgical Equipment Market Players:

- Toray Industries (Japan)

- Teijin Limited (Japan)

- Mitsubishi Chemical Group (Japan)

- Solvay S.A. (Belgium)

- SGL Carbon SE (Germany)

- Johnson & Johnson (U.S.)

- Stryker (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Toray is dominating player in the market supplies carbon-fiber-reinforced plastics (CFRP) for lightweight, high-strength surgical tool handles, robotic arm end-effectors, and patient positioning frames. Its Torayca® carbon fiber enables X-ray-translucent surgical tables and C-arm components, improving image clarity during orthopedic and neurosurgeries.

- Teijin penetrates the market via its Tenax® carbon fibers and Panlite® polycarbonate resins, used in sterilizable surgical power tools, drill housings, and endoscopic light guide sheaths. Its biocompatible polyethylene naphthalate (PEN) films serve as flexible circuits in laparoscopic cameras.

- Mitsubishi Chemical addresses the market through its high-heat-resistant polycarbonate (Iupilon®) for autoclaveable surgical trays and its carbon-fiber prepregs for robotic surgical boom arms. Its Diafoil® polyester films are critical for flexible printed circuits in electrosurgical pencils and ultrasonic scalpels.

- Solvay is a leader in the market in high-performance thermoplastics (KetaSpire® PEEK, Veradel® PESU) for implantable surgical instruments—such as pedicle screw drivers, bone saw guides, and suture anchors—that are MRI-safe and radiolucent.

- SGL Carbon specializes in the market through its SIGRAFIL® continuous carbon fibers and prepregs, engineered for load-bearing surgical tables, C-arm extension plates, and robotic end-effector arms that require high stiffness and radiation transparency. Its isotropic graphite grades are used as heating elements in surgical sterilizers and as electrodes in electrosurgical generators.

Here is a list of key players operating in the global surgical equipment market:

The automotive carbon fiber composites market is moderately consolidated, with leading players leveraging vertical integration, R&D in rapid-curing resins, and partnerships with OEMs to reduce costs and boost production throughput. Toray, Teijin, and Mitsubishi Chemical dominate via high-volume supply agreements with European and Japanese automakers, while U.S. firms like Hexcel and Solvay focus on aerospace-grade derivatives for ultra-luxury EVs. Chinese and South Korean players are scaling up affordable PAN-based fibers, intensifying price competition. Strategic initiatives include recycling programs, automated layup processes, and joint ventures for battery enclosures. Mergers and acquisitions target lightweighting for range extension, with increasing capacity expansions in North America and Southeast Asia to secure regional supply chains.

Corporate Landscape of the Market:

Recent Developments

- In November 2025, Teijin Limited and BioVaram announced that they have signed a agreement to explore opportunities for expanding usage of implantable medical devices and regenerative medicine products in India.

- In June 2025, Johnson & Johnson MedTech announced the launch of the ETHICON™ 4000 Stapler, which is an advanced surgical stapler designed to manage tissue complexities and deliver exceptional staple line integrity to minimize risk factors for surgical leaks and bleeding complications across specialties.

- In September 2024, Stryker announced the launch of 1788, which is a next-generation advanced surgical camera in India, elevating surgical visualization across specialties. The equipment is designed to use across multiple specialties and provides surgeons with enhanced imaging capabilities for improved patient outcomes.

- Report ID: 8643

- Published Date: Jun 29, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Surgical Equipment Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.