Solid-State Battery Electrolytes Market Outlook:

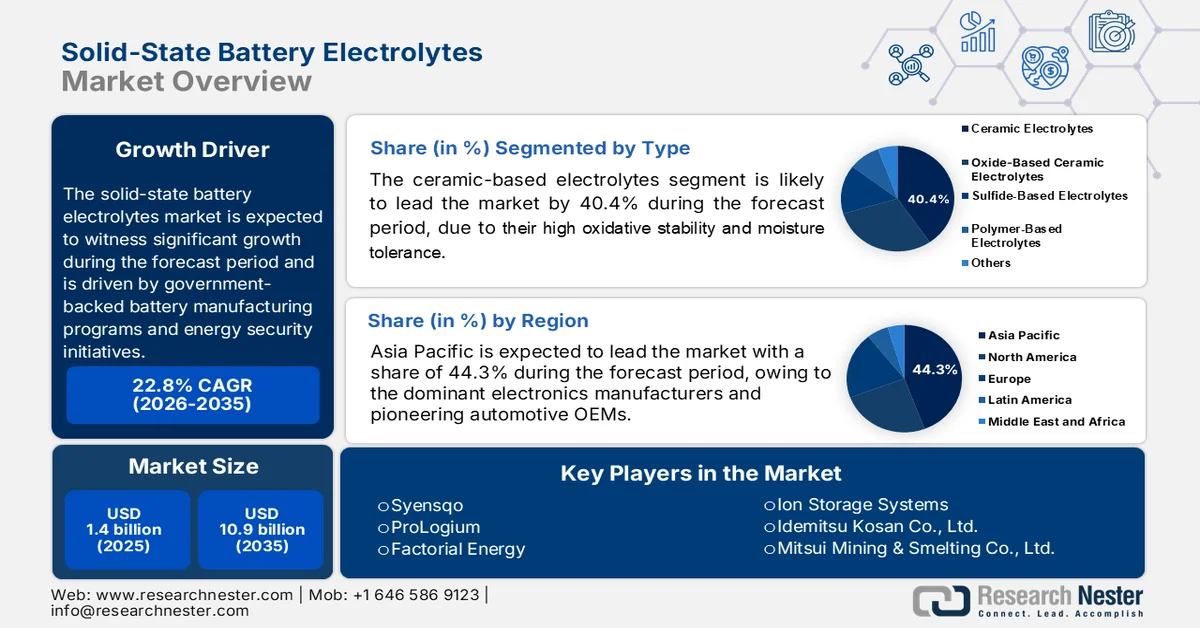

Solid-State Battery Electrolytes Market size was valued at USD 1.4 billion in 2025 and is poised to reach USD 10.9 billion by the end of 2035, expanding at around 22.8% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of solid-state battery electrolytes is assessed at USD 1.7 billion.

The solid-state battery electrolytes market is being shaped by government-backed battery manufacturing programs, electric vehicle (EV) deployment targets, and energy security initiatives that are increasing demand for advanced battery materials across automotive, defense, aerospace, and stationary storage applications. According to the International Energy Agency 2025 data, global electric car sales exceeded 17 million units, representing a significant expansion of the battery demand base and creating long-term requirements for next-generation electrolyte materials that can support higher energy density and improved operating performance.

In the U.S., the U.S. Department of Energy (DOE) February 2022 data depicts that the nation continues to direct substantial funding toward domestic battery innovation and supply chains through programs supported by the Bipartisan Infrastructure Law, including more than USD 7 billion allocated for battery supply-chain development. These investments are accelerating pilot-scale and commercial-scale research activities involving advanced electrolyte systems, while strengthening collaboration among material suppliers, battery manufacturers, national laboratories, and automotive OEMs. For B2B stakeholders, the market environment is increasingly influenced by localization requirements, supply-chain resilience objectives, and government-supported manufacturing capacity expansion.

Key Solid-State Battery Electrolytes Market Insights Summary:

Regional Highlights:

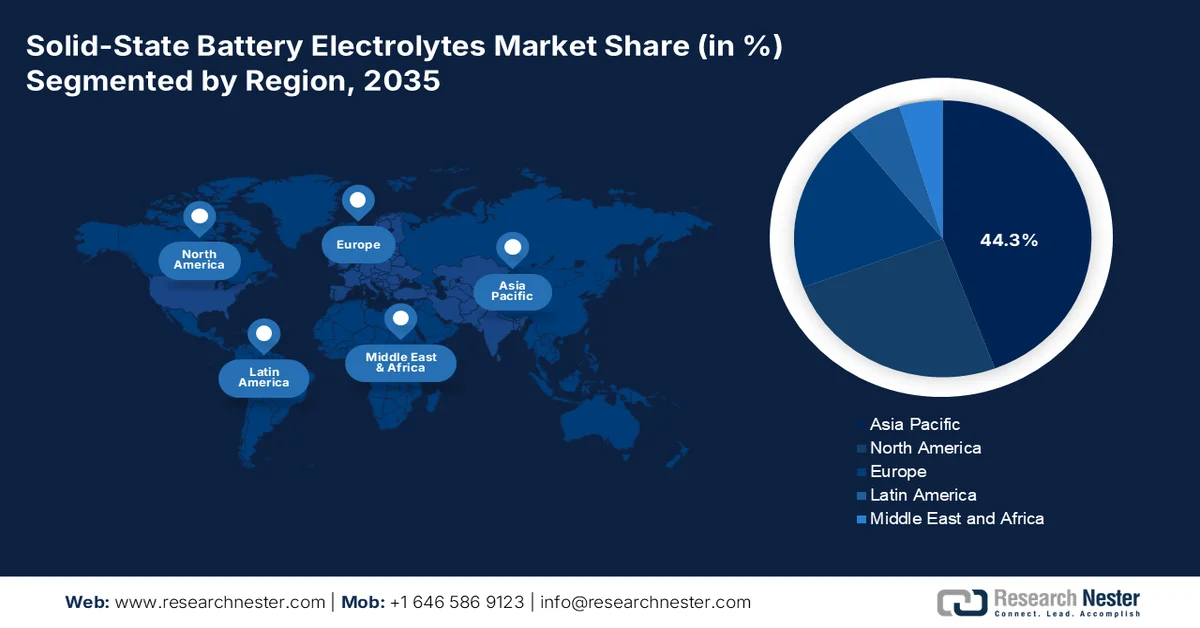

- Asia Pacific is anticipated to capture 44.3% of the solid-state battery electrolytes market by 2035, reinforced by dominant electronics manufacturers, pioneering automotive OEMs, and a mature lithium-ion ecosystem

- North America is expected to witness the fastest growth during 2026-2035, bolstered by innovative startups, established chemical companies, and robust government-backed research initiatives

Segment Insights:

- Ceramic-based Electrolytes are projected to account for 40.4% of the solid-state battery electrolytes market by 2035, propelled by high oxidative stability, superior moisture tolerance, and advances in doping technologies that enhance ionic conductivity

- Electric Vehicles are expected to remain the leading application throughout 2026-2035, supported by increasing demand for extended driving ranges, faster charging, and enhanced battery safety

Key Growth Trends:

- Government funding for domestic battery manufacturing

- Rising EV deployment supported by public funding

Major Challenges:

- High manufacturing complexity

- Interfacial instability

Key Players: Syensqo (Belgium),ProLogium (Taiwan),Factorial Energy (U.S.),Ion Storage Systems (U.S.),Idemitsu Kosan Co., Ltd. (Japan) ,Mitsui Mining & Smelting Co., Ltd. (Japan).

Global Solid-State Battery Electrolytes Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.4 billion

- 2026 Market Size: USD 1.7 billion

- Projected Market Size: USD 10.9 billion by 2035

- Growth Forecasts: 22.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (44.3% share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, Japan, South Korea, United States, Germany

- Emerging Countries: Canada, France, United Kingdom, India, Italy

Last updated on : 7 July, 2026

Solid-State Battery Electrolytes Market - Growth Drivers and Challenges

Growth Drivers

- Government funding for domestic battery manufacturing: Government investment in battery supply chains is one of the strongest demand drivers for solid-state battery electrolytes because electrolyte materials are critical inputs in next-generation battery production. In the United States, the Department of Energy (DOE) February 2022 data announced more than USD 3 billion for battery manufacturing and processing projects under the Bipartisan Infrastructure Law, supporting domestic battery-material ecosystems and advanced battery technologies. These programs encourage manufacturers to expand pilot and commercial production capabilities for advanced electrolytes. As battery gigafactory construction accelerates, demand for advanced electrolyte materials is expected to increase alongside manufacturing capacity expansion and localization requirements.

- Rising EV deployment supported by public funding: The rapid expansion of electric vehicle (EV) markets continues to strengthen long-term demand for advanced battery materials. According to IBEF February 2026 data, India has surged the EV sales to 30% of private cars. Governments across North America, Europe, China, Japan, and South Korea continue to provide incentives for EV adoption and charging infrastructure deployment. As automakers seek longer driving range, faster charging capability, and improved battery safety, investment in solid-state battery programs is increasing. Companies that establish partnerships with automotive OEMs participating in government-backed electrification programs are likely to gain a competitive advantage as commercialization timelines advance.

Challenges

- High manufacturing complexity: Producing solid-state electrolytes—particularly sulfides and halides—requires precise atmospheric control (dry rooms, inert gas) to prevent moisture degradation, significantly increasing CAPEX and operational complexity. Scaling from lab-scale (grams) to ton-level production while maintaining phase purity and consistent particle morphology remains a formidable engineering hurdle.

- Interfacial instability: Solid-solid interfaces between electrolytes and electrodes suffer from poor physical contact, leading to high charge-transfer resistance and dendrite penetration over cycling. This interfacial degradation reduces coulombic efficiency and cycle life, particularly with lithium-metal anodes.

Solid-State Battery Electrolytes Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

22.8% |

|

Base Year Market Size (2025) |

USD 1.4 billion |

|

Forecast Year Market Size (2035) |

USD 10.9 billion |

|

Regional Scope |

|

Solid-State Battery Electrolytes Market Segmentation:

Type Segment Analysis

Within the type segment, ceramic-based electrolytes are leading in the solid-state battery electrolytes market and is poised to hold the share value of 40.4% by the end of 2035. The segment is emerging as a game-changing due to their high oxidative stability and moisture tolerance. The Frontiers February 2025 study demonstrates that molybdenum doping achieves exceptional ionic conductivity of 0.30 S cm⁻¹, comparable to liquid electrolytes, effectively overcoming the primary conductivity barrier. Fluorine doping enhances lattice stability, while cerium improves structural integrity and reduces interfacial resistance, as validated by symmetrical half-cell evaluations. Crucially, the nano-engineering approach reduces energy consumption by 40% and hazardous waste by 75% compared to conventional methods.

Application Segment Analysis

The electric vehicles stand as the largest application driving the market, fueled by the global push for extended driving ranges, faster charging, and enhanced safety over conventional lithium-ion systems. According to the ACS Publications October 2023 data, the solid-state electrolytes enable automakers to deploy lithium-metal anodes, achieving energy densities that surpass 400 Wh/kg, a critical milestone for mass EV adoption. The National Renewable Energy Laboratory (NREL), in its 2024 transportation electrification brief, reported that solid-state battery adoption in light-duty EVs could reduce pack-level cost-per-mile compared to current NMC-liquid cells. This compelling economic and performance advantage ensures automotive applications of the electrolyte market revenue, making it the most influential end-use segment globally.

Battery Type Segment Analysis

Pouch cells are projected to lead the market, driven by their flexible, lightweight design and superior space efficiency – critical attributes for automotive and consumer electronics applications where volumetric energy density is paramount. Pouch packaging allows for thinner electrolyte layers and easier stacking of bi-polar electrodes, which is particularly advantageous for sulfide and polymer-based electrolyte systems. Top companies have optimized their solid-state cell architectures around pouch formats to maximize active material loading and simplify thermal management. This efficiency advantage positions pouch cells as the preferred form factor for next-generation EV battery packs.

Our in-depth analysis of the solid-state battery electrolytes includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Application |

|

|

Battery Type |

|

|

End user |

|

|

Manufacturing Process |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Solid-State Battery Electrolytes Market - Regional Analysis

APAC Market Insights

Asia Pacific is dominating the solid-state battery electrolytes market and is projected to hold the regional revenue share of 44.3% by the end of 2035. The region is driven by the dominant electronics manufacturers and pioneering automotive OEMs. The region benefits from a mature lithium-ion ecosystem, enabling faster scale-up of sulfide and oxide electrolyte production. Japan and South Korea lead in materials science, while China aggressively expands domestic solid-state capacity through state-backed industrial policies. Additionally, the region's robust raw material refining infrastructure and government incentives for next-generation batteries create a cost-competitive advantage. With a strong focus on automotive electrification and consumer electronics, Asia Pacific remains the undisputed leader in solid-state electrolyte development and manufacturing capacity.

The government-led battery manufacturing and electric mobility initiatives that are strengthening the domestic advanced battery ecosystem is shaping the market in India. The IISD April 2026 data reported that USD 2.2 billion is allocated for Advanced Chemistry Cell (ACC) Production Linked Incentive scheme to establish 50 GWh of domestic battery manufacturing capacity, creating opportunities for next-generation electrolyte suppliers. Additionally, the PIB March 2025 data reported that more than 4.4 million electric vehicles were registered in India, reflecting rapid growth in battery demand across passenger and commercial vehicle segments. These developments are encouraging investment in advanced battery materials, research, and localized supply chains.

The continued expansion of the country’s battery manufacturing base and electric vehicle industry is driving the solid-state battery electrolytes market in China. According to the People’s Daily Online February 2025 data, the country produced 13.17 million new energy vehicles (NEVs) in 2024, highlighting the scale of battery demand across transportation sectors. In addition, China’s Ministry of Industry and Information Technology (MIIT) reported that the nation’s power battery installed is reflecting substantial growth in battery deployment and manufacturing activity. These developments are encouraging battery producers to invest in next-generation technologies, including solid-state battery platforms, to improve performance and competitiveness. As China strengthens its leadership in advanced battery manufacturing, demand for high-performance electrolyte materials is expected to increase across automotive and energy-storage applications.

North America Market Insights

North America is projected to emerge rapidly during the assessed period, 2026 to 2035 in the market. The region is driven by the dynamic ecosystem of innovative startups, established chemical giants, and robust government-backed research initiatives. Sulfide and polymer electrolytes currently dominate development pipelines, driven by their compatibility with high-energy lithium-metal anodes. Strategic partnerships, such as those between OEMs and electrolyte developers, are accelerating pilot-line construction and technology de-risking. Additionally, a strong emphasis on domestic supply chain resilience and green manufacturing principles, including dry-electrode coating and solvent-free synthesis, is reshaping the market, positioning North America as a critical hub for next-generation solid-state battery innovation outside Asia.

The strong federal support for battery manufacturing and accelerating energy-storage deployment is shaping the solid-state battery electrolytes market in the U.S. In September 2024, the U.S. Department of Energy (DOE) announced more than USD 3 billion in funding for 25 battery manufacturing and processing projects across 14 states, strengthening domestic production of advanced battery materials and creating new opportunities for electrolyte suppliers. In parallel, the U.S. Energy Information Administration (EIA) March 2025 data reported that utility-scale battery storage capacity reached approximately 26 gigawatts, reflecting rapid expansion of energy-storage infrastructure. These investments are encouraging battery developers to scale next-generation technologies, increasing demand for high-performance solid-state electrolyte materials across automotive, grid-storage, and industrial applications.

The federal investments aimed at establishing a domestic battery value chain and supporting clean transportation initiatives is shaping the market in Canada. The Canada Energy Regulator June 2024 data reported that new zero-emission vehicle (ZEV) registrations reached approximately 185,000 units in 2023, representing continued growth in battery-powered transportation adoption. These developments are encouraging battery manufacturers and material suppliers to expand research, production, and sourcing activities, creating favorable conditions for solid-state electrolyte commercialization across automotive and energy-storage applications.

Europe Market Insights

The market in Europe is characterized by a strong regulatory push for sustainable and localized battery production, driven by the European Battery Alliance and stringent environmental mandates. The region emphasizes polymer and composite electrolytes, leveraging its chemical industry expertise to develop eco-friendly, solvent-free manufacturing processes. Europe also prioritizes raw material circularity, investing heavily in recycling and second-life applications for battery components. With a robust academic-industrial R&D network and ambitious electrification targets, Europe is steadily building a self-reliant, environmentally conscious solid-state electrolyte supply chain that complements its automotive manufacturing heritage.

The increasing investments in battery manufacturing and the country’s strong electrification strategy is driving the solid-state battery electrolytes market in Germany. According to European Commission January 2025 data, demonstrating sustained demand for advanced battery technologies despite broader automotive market fluctuations. In addition, the European Commission May 2025 that Germany would support battery research and industrial projects through the European battery value chain, with more than EUR 1 billion in federal funding committed to battery innovation and production initiatives. These developments are encouraging manufacturers to accelerate next-generation battery development, creating favorable conditions for solid-state electrolyte suppliers serving automotive, industrial, and energy-storage applications.

The government-backed battery innovation programs and rising electrification across the transport sector is driving the market in the UK. According to the ForeCourt Trader June 2025 data, there were 1.39 million licensed battery electric vehicles (BEVs) on UK roads, reflecting continued growth in demand for advanced battery technologies. Additionally, in 2025 the UK government announced billion through the Automotive Transformation Fund to strengthen domestic zero-emission vehicle and battery supply chains, including support for battery manufacturing and advanced materials development. These initiatives are fostering investment in next-generation battery technologies and encouraging collaboration between automakers, battery developers, and material suppliers. As domestic battery production capacity expands, demand for high-performance solid-state electrolyte materials is expected to increase across automotive and energy-storage applications.

Key Solid-State Battery Electrolytes Market Players:

- Syensqo (Belgium)

- ProLogium (Taiwan)

- Factorial Energy (U.S.)

- Ion Storage Systems (U.S.)

- Idemitsu Kosan Co., Ltd. (Japan)

- Mitsui Mining & Smelting Co., Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Syensqo, the Solvay spin-off, is a specialty materials leader in the market, focusing on high-performance polymer-based electrolytes and composite membranes. The company leverages its sulfonic-acid chemistry expertise to produce flexible, safe electrolyte solutions that enhance interfacial stability.

- ProLogium is a unique player in the market, developing complete solid-state cells with proprietary oxide-ceramic electrolytes and polymer binders. The company differentiates itself through its continuous-coating manufacturing process, which produces ultra-thin, mechanically robust electrolyte layers.

- Factorial Energy is a U.S.-based manufacturer advancing the market with its proprietary polymer-based FEST® electrolyte system. The company focuses on scalable, high-safety solutions for automotive end-users. Strategic partnerships with major automakers underscore its competitive positioning.

- Ion Storage Systems is a U.S.-based niche manufacturer in the market, specializing in ceramic-based electrolyte membranes for anode-free battery architectures. The company emphasizes intrinsic safety and room-temperature operation.

- Idemitsu Kosan Co., Ltd. is a Japanese leader in the market, manufacturing high-performance sulfide-based electrolytes for automotive end-users. Leveraging its petrochemical heritage, the company offers industrial-scale production capabilities and superior ionic conductivity.

Here is a list of key players operating in the global market:

The solid-state battery electrolytes market is highly consolidated, led by North America firms due to advanced R&D and high procedural volumes. Key players focus on strategic initiatives such as product innovation, geographic expansion into Asia-Pacific, and regulatory approvals. Mergers and acquisitions are common to enhance portfolio diversification and distribution networks. For example, in March 2024 Zylox-Tonbridge announced a new strategic partnership with Avinger. Europe and Japan companies compete through precision engineering and cost-effective solutions, while emerging players from India and South Korea target niche segments. Intense rivalry drives technological integration, including image-guided devices and disposable catheters for peripheral and coronary applications.

Corporate Landscape of the Market:

Recent Developments

- In January 2026, Syensqo and Axens announced the launch of Argylium, a new company dedicated to developing and scaling up commercial demonstration of advanced materials for solid-state batteries in Europe.

- In June 2025, ProLogium officially unveils its 4th-generation disruptive innovation, the Superfluidized Inorganic Solid-State Electrolyte, marking the beginning of a new era for solid-state lithium batteries, one defined by full functionality, wide applicability, and scalable mass production.

- Report ID: 8661

- Published Date: Jul 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.