Solar EPC Market Outlook:

Solar EPC Market size was valued at USD 107.2 billion in 2025 and is projected to reach USD 287.8 billion by the end of 2035, rising at a CAGR of 11.6% during the forecast period, i.e., 2026-2035. In 2026, the industry size of solar EPC is estimated at USD 119.6 billion.

The global solar Engineering, Procurement, and Construction (EPC) industry is poised for exceptional growth, based on factors such as global energy transition priorities and increasing adoption of renewable energy projects. Governments across major economies are introducing supportive policies, incentives, and regulatory frameworks that accelerate project approvals and the deployment of large-scale solar installations. Based on the government data from the U.S., which was published in April 2024, the Biden-Harris Administration, through the EPA, announced a total amount of USD 7 billion in solar grants to deliver residential solar to over 900,000 low-income and disadvantaged households across the nation. It was funded by the Inflation Reduction Act and President Biden’s Investing in America agenda, thereby increasing the growth potential of the solar EPC market.

Furthermore, the solar EPC market hosts a dynamic and evolving supply chain, which is an integration of technology providers, module manufacturers, and construction service firms to ensure proper project deliveries. Besides rising solar PV capacity, investment, and policy support, it directly boosts demand for EPC contractors to design, build, and install utility-scale and distributed solar projects. As of the February 2025 report from the IEA, the solar PV generation reached 1,600 TWh in 2023, which is up by 25%, and is continuing on track with 2030 net zero emissions scenarios. In addition, this capacity is expected to more than double between 2025 and 2030, highly attributable to low costs, faster permitting, strong policy support, and private sector adoption, especially in China, the U.S., Europe, and India. The global solar PV investment surpassed USD 480 billion in 2023, which was efficiently supported by technological innovation, distributed systems, and international collaboration.

Key Solar EPC Market Insights Summary:

Regional Highlights:

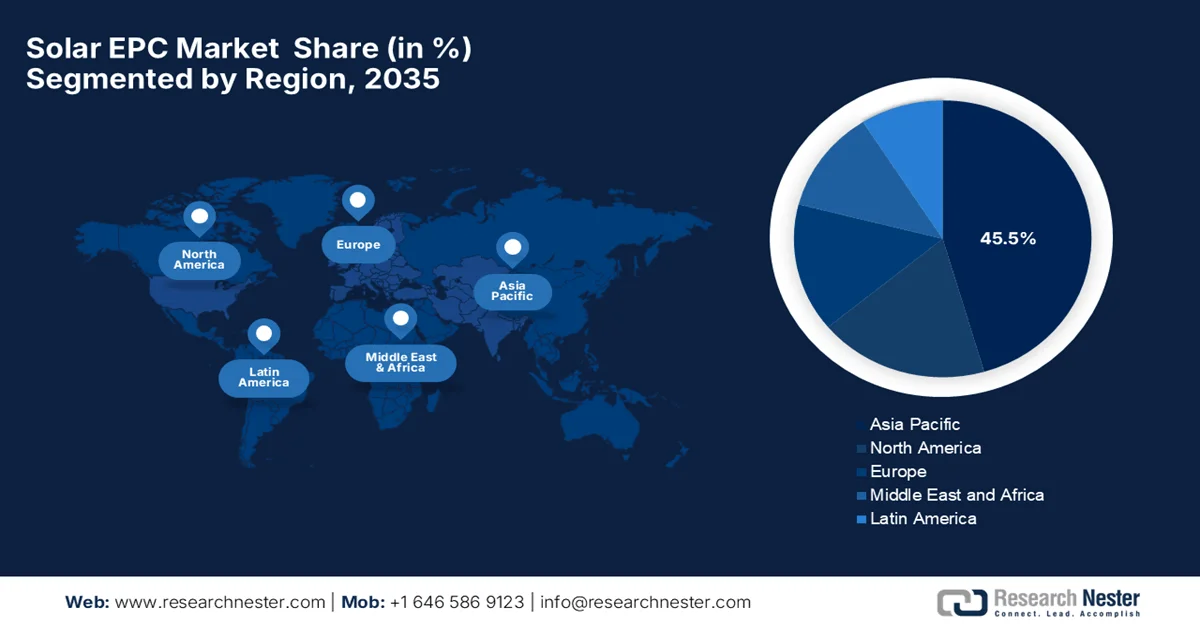

- Asia Pacific is anticipated to command a leading 45.5% revenue share by 2035 in the solar EPC market, impelled by rapid urban infrastructure development integrating solar installations across industrial parks, smart cities, and commercial projects

- North America is forecast to witness steady expansion through 2026–2035, supported by favorable project financing incentives and long-term power contracting mechanisms enabling large-scale bankable solar developments

Segment Insights:

- The rooftop segment is projected to account for a dominant 66.4% share of the solar EPC market by 2035, fueled by accelerating adoption across residential, commercial, and industrial end users.

- The photovoltaic solar segment is expected to expand at a considerable rate during 2026–2035, underpinned by cost competitiveness and rapid global deployments.

Key Growth Trends:

- Increase in affordability of solar technology

- Rising global demand for renewable energy

Major Challenges:

- Land acquisition challenges

- Grid integration and infrastructure constraints

Key Players: Quanta Services, Moss, SOLV Energy, Black & Veatch, Bechtel Corporation, Mortenson, Rosendin Electric, Canadian Sola, Sterling & Wilson Renewable Energy, Tata Power Solar Systems Limited, Vikram Solar, Jakson Group.

Global Solar EPC Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 107.2 billion

- 2026 Market Size: USD 119.6 billion

- Projected Market Size: USD 287.8 billion by 2035

- Growth Forecasts: 11.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, India, Japan, Germany

- Emerging Countries: Australia, South Korea, Saudi Arabia, Brazil, United Arab Emirates

Last updated on : 16 February, 2026

Solar EPC Market - Growth Drivers and Challenges

Growth Drivers

- Increase in affordability of solar technology: There has been a decline in costs of PV modules, inverters, and balance‑of‑system components owing to the economies of scale and improved manufacturing, making solar installations competitive along with traditional energy sources. This aspect of lower equipment expenses expands the solar EPC market demand across utility, commercial, and residential sectors. According to the article published by Our World in Data in June 2024, the solar PV prices have reduced by around 20% each time global installed capacity doubled, and is followed by Wright’s Law of consistent cost decline with increased production. The article also underscored that over the last decade, solar costs have dropped by about 90%, transforming it from one of the most expensive to one of the cheapest electricity sources globally, hence increasing the uptake in price-sensitive regions.

2024 Q1 Solar PV System Cost and LCOE Benchmarks by System Size

|

Type |

PV System Size |

MSP (USD/Wdc) |

MMP (USD/Wdc) |

O&M (USD/kWdc‑yr) |

LCOE (USD/MWh) |

|

UPV |

100 MWdc |

0.98 |

1.12 |

19 |

47 |

|

APV |

3 MWdc |

1.34 |

1.51 |

22 |

75 |

|

RPV |

8 kWdc |

2.74 |

3.15 |

30 |

142 |

Source: U.S. Department of Energy

2024 Q1 Solar PV + Energy Storage (ESS) System Cost and LCOE Benchmarks

|

Type |

PV System Size |

ESS Size |

MSP (USD/Wdc) |

MMP (USD/Wdc) |

O&M (USD/kWdc‑yr) |

LCOE (USD/MWh) |

|

UPV |

100 MWdc |

240 MWh |

1.73 |

1.99 |

48 |

94 |

|

APV |

3 MWdc |

6 MWh |

1.99 |

2.28 |

43 |

126 |

|

RPV |

8 kWdc |

13.5 kWh |

4.50 |

5.19 |

70 |

264 |

Source: U.S. Department of Energy

- Rising global demand for renewable energy: The concerns of energy security and fossil fuel volatility are the factors that are encouraging utilities, businesses, and governments to opt for solar power, boosting revenue in the solar EPC market. In April 2025, the Ministry of New and Renewable Energy disclosed that India’s renewable energy capacity reached 220.10 GW by March 2025, with a larger addition of 29.52 GW in FY 2024-25, mainly due to solar energy, adding 23.83 GW. The solar installations now total 105.65 GW, including ground-mounted, rooftop, hybrid, and off-grid systems. Wind power crossed the 50 GW and bioenergy and small hydro continue to support a diversified energy mix. The article also stated there are 169.40 GW of projects underway and 65.06 GW tendered, due to which India is steadily advancing toward its 500 GW renewable target for 2030, hence denoting an optimistic solar EPC market opportunity.

- Technological improvements & digitalization: Advancements in terms of solar technologies, i.e., high-efficiency PV panels, bifacial modules, energy storage integration, and digital project management tools, are improving project performance, efficiently driving the solar EPC market growth. For instance, in January 2026, Vikram Solar notified that it is making a complete transition to its advanced G12R module portfolio, which marks a structural shift toward high-efficiency, large-format solar technology. The modules are anchored in the HYPERSOL G12R series, and they deliver up to 640 Wp power output with efficiencies reaching 23.69%. Hence, with such consistent efforts from pioneers, the solar EPC market is set to bolster growth internationally by enhancing energy yield and reliability.

Challenges

- Land acquisition challenges: This is the major barrier causing obstacles to the upliftment of the solar EPC market across different nations. Contractors often come across issues such as land ownership disputes, fragmented plots, and community opposition, which can cause delays to the project timelines. Meanwhile, agricultural land usage restrictions and environmental regulations also complicate the process of site acquisition. In terms of the densely populated areas, gaining suitable plots for solar farms is found to be difficult. These delays in land clearance can cause procurement and construction delays, negatively impacting overall project schedules. In this context, companies need to conduct proper due diligence, local stakeholders early to acquire land legally and more efficiently.

- Grid integration and infrastructure constraints: Integrating these large-scale solar projects into existing electrical grids is identified as a considerable factor resulting in technical and logistical challenges for players operating in the solar EPC market. In most of the regions, grid capacity limitations, weak transmission infrastructure, and interconnection delays can prevent solar power evacuation. Therefore, EPC contractors need to design solutions that are compatible with local grid standards, which include inverter sizing, reactive power management, and curtailment mitigation. Any variability in solar generation requires advanced forecasting and storage integration, which increases both complexity and cost. On the other hand, weak grid infrastructure can lead to delays in commissioning and revenue realization for developers.

Solar EPC Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

11.6% |

|

Base Year Market Size (2025) |

USD 107.2 billion |

|

Forecast Year Market Size (2035) |

USD 287.8 billion |

|

Regional Scope |

|

Solar EPC Market Segmentation:

Mounting Type Segment Analysis

The rooftop is anticipated to garner the largest revenue share of 66.4% and lead the solar EPC market over the forecasted years. The dominance of the subtype is mainly propelled by accelerating adoption across residential, commercial, and industrial end users. These rooftop systems are identified as an attractive and decentralized power generation solution, which allows both consumers and businesses to reduce electricity costs and advance sustainability goals. In March 2025, Tata Power Solar Rooftop reported that it had surpassed 150,000 installations across India, by achieving a total rooftop capacity of around 3 GW and serving residential, commercial, and industrial customers. The company offers solutions through its Tata Power Solaroof program, with benefits such as reduced electricity bills. The suitable rooftop incentives coupled with such major milestones from pioneers denote that there is a strong opportunity for the segment to grow at the highest pace.

Technology Segment Analysis

The photovoltaic solar is expected to grow at a considerable rate in the solar EPC market, facilitated by its cost competitiveness and rapid global deployments. In this context Institute of Energy Economics and Financial Analysis in November 2024 reported that between FY2022 and FY2024, India’s solar PV exports surged more than 23 times, reaching nearly USD 2 billion in FY2024, wherein the U.S. accounted for over 97% of shipments. On the other hand, the major manufacturers such as Adani Solar, Waaree Energies, and Vikram Solar exported a significant portion of their annual production, capitalizing on higher margins abroad. Therefore, this rapid growth positions India as a strong alternative to Southeast Asia in the U.S, especially amid ongoing trade investigations and tariffs on China and SEA imports. Hence, such surging trade demand, coupled with cost-effectiveness, positions the sub-segment at the forefront of revenue generation in this field.

Installation Type Segment Analysis

The utility-scale solar is forecasted to emerge, grabbing a significant revenue share in the solar EPC market by 2035. Most large EPC contracts are associated with the utility-scale projects influenced by economies of scale and grid integration needs. In addition, utility-scale projects benefit from lower per-unit installation costs, thereby enabling EPC contractors to deliver competitively priced large-capacity plants. These installations are being paired with energy storage systems and hybrid configurations to ensure grid stability and proper power supply. Meanwhile, the aspect of long-term power purchase agreements with utilities and governments provides revenue certainty, attracting large-scale investments. Furthermore, expanding transmission infrastructure and grid modernization programs are deliberately facilitating the integration of solar plants, hence denoting a wider segment scope.

Our in-depth analysis of the solar EPC market includes the following segments:

|

Segment |

Subsegments |

|

Mounting Type |

|

|

Technology |

|

|

Installation Type |

|

|

Deployment Scale |

|

|

End use |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Solar EPC Market - Regional Analysis

APAC Market Insights

The Asia Pacific solar EPC market is expected to capture a total of 45.5% revenue share during the assessment period. The region’s prominence is highly driven by urban infrastructure development, where solar installations are embedded into industrial parks, smart cities, and new commercial developments. This integration creates large-scale EPC opportunities that are suitable for urban expansion, and the region is exploring alternatives to address land efficiencies. Based on the government data from Japan, which was published in August 2023, the country is emerging with two major solar technologies, such as space-based solar power and perovskite solar cells, with the main goal to overcome land and efficiency limitations of traditional PV. SBSP satellites are equipped with giant solar panels and will transmit microwaves to Earth, enabling a 90% utilization rate and power output comparable to nuclear plants. Kyoto University has led decades of microwave transmission experiments wherein the country’s basic plan on space policy targets a space-to-ground transmission test by FY2025, expanding solar deployment across urban environments.

The large-scale renewable base development in industrial regions, which is designed to supply power to distant demand centers are responsible for uplifting China solar EPC market. These mega-projects necessitate complex engineering, transmission coordination, and high-capacity EPC execution, providing encouraging opportunities for both foreign and domestic players. CPA in February 2024 revealed that the country controls more than 80% of the worldwide solar PV supply chain, spanning polysilicon, wafers, cells, and modules. There is a financial strain on the country’s players, whereas companies such as JinkoSolar, Trina Solar, and Canadian Solar sustain operations through substantial subsidies and investments from the country’s government, which allocated USD 130 billion into solar in 2023. This state-backed support propels solar EPC market growth by supporting project development, lowering financial risks for EPC contractors.

The constant government backing and the deployment of hybrid and renewable energy projects are the main fueling factors for the solar EPC market in India. Support also includes financial incentives, policy frameworks, and streamlined approval processes that make large-scale solar projects even more feasible. The country is also identified as a major trade hub, attracting more investments in this field. In this context, Energy & Environment in August 2025 stated that the country has emerged as the world’s third-largest solar energy producer, which has generated around 1,08,494 GWh in 2025. Besides, the country’s cumulative solar capacity reached 119.02 GW, which includes 90.99 GW from ground-mounted plants and 19.88 GW from rooftop systems. Government initiatives such as PM Surya Ghar Yojana, PM-KUSUM, and Solar Parks Scheme are driving adoption, whereas the domestic manufacturing of solar modules expanded from 38 GW to 74 GW in FY 2024-25, making it suitable for standard solar EPC market growth.

India Solar Energy Statistics 2025: Installed Capacity, Generation, and Government Initiatives

|

Metric |

Value (2025) |

Notes |

|

Solar Power Generation |

1,08,494 GWh |

Surpassed Japan’s 96,459 GWh |

|

Cumulative Solar Capacity |

119.02 GW |

90.99 GW ground-mounted, 19.88 GW rooftop, 3.06 GW hybrid, 5.09 GW off-grid |

|

Solar Module Manufacturing Capacity |

74 GW |

Up from 38 GW in FY 2024-25 |

|

Renewable Share of Total Installed Capacity |

50.07% |

Out of 484.82 GW total capacity |

|

Solar Parks Approved |

53 Parks |

Total capacity 39,323 MW; 18 fully developed |

Source: Energy & Environment

India’s Country-wise Imports of Solar PV Cells and Modules in 2021-22 and 2022-23 (USD Millions)

|

Country |

2021-22 Solar PV Cells (HS 85414011) |

2021-22 Solar PV Modules (HS 85414012) |

2022-23 Solar PV Cells (HS 85414200) |

2022-23 Solar PV Modules (HS 85414300) |

|

Australia |

0.01 |

- |

0.22 |

- |

|

Cambodia |

1.72 |

- |

52.72 |

- |

|

Canada |

1.32 |

- |

0.01 |

- |

|

Chile |

0.63 |

- |

- |

- |

|

Taiwan |

5.48 |

- |

0.13 |

1.92 |

|

China PRP |

1069.88 |

3075.32 |

581.45 |

874.89 |

|

France |

- |

- |

- |

- |

|

Germany |

0.19 |

- |

0.21 |

0.13 |

|

Hong Kong |

0.55 |

- |

229.12 |

3.04 |

|

Indonesia |

0.78 |

- |

1.56 |

- |

|

Italy |

- |

- |

0.01 |

- |

|

Japan |

- |

- |

0.61 |

- |

Source: Ministry of New and Renewable Energy

North America Market Insights

The solar EPC market in North America is primarily reshaped by suitable project financing incentives and long-term power contracting mechanisms, which readily enable large, bankable solar developments. The risk management, standardized EPC contracts, and strong institutional participation support constant project execution across the region’s vast geography. In January 2025, the U.S. Department of Energy reported that its loan programs office approved a total of USD 289.7 million loan guarantee to Sunwealth for Project Polo, which will deploy up to 1,000 solar PV and battery storage systems across 27 states. It has an aggregate capacity of 168 MW PV and 16.8 MW BESS, and it will function as a wide-scale virtual power plant by enhancing grid resilience and cutting 4.07 million metric tons of carbon emissions. Hence, from a strategic perspective, such government-backed financing is boosting investor confidence and accelerating large-scale solar-plus-storage projects in the region.

The expansion of community solar and shared solar ownership models creates EPC demand more than traditional utility and rooftop installations, driving business in the U.S. solar EPC market. These models broaden solar EPC market participation and diversify EPC project portfolios across different sectors. NREL in September 2024 revealed that between 2023 and 2024, community solar in the U.S. had expanded, with several states updating or enacting policies to enhance accessibility and benefits. Alaska established enabling legislation under Senate Bill 152, whereas Maryland made its 583 MW pilot program permanent. Colorado and Minnesota revised their programs to reserve 51% and 30% of new projects for income-qualified subscribers, and New Jersey converted its 243 MW pilot into a permanent program. These policy updates are creating new EPC opportunities across multiple states in the U.S., hence denoting a positive solar EPC market outlook.

Provincial-level clean electricity planning and public-sector procurement frameworks, which create structured and predictable project pipelines, are the main factors driving the growth of the solar EPC market in Canada. Long-term energy planning and utility-led initiatives deliberately support steady EPC demand in the country. In October 2024, the country’s government reported that under its greening government strategy, it has awarded more than USD 73 million in renewable energy certificate contracts to Hep Solar and South Head Switch Power to supply 100,600 RECs on a yearly basis from new solar facilities. This particular initiative supports 100% clean electricity for federal buildings, reduces up to 32,600 tons of eCO₂, and efficiently strengthens partnerships with Indigenous-owned businesses, thereby driving sustained solar EPC demand in the country.

Europe Market Insights

Europe solar EPC market has acquired a prominent position in the global landscape mainly due to cross-border energy integration and regional grid harmonization efforts, which support multi-country solar developments and interconnected renewable systems. EPC players in the region benefit from projects that are aligned with continental energy coordination. In April 2024, as stated by the European Commission, along with energy ministers from 23 Europe based countries, it launched the European Solar Charter to strengthen the region’s photovoltaic sector. This Charter promotes the region-specific solar panels, supports sustainable products, and encourages the use of non-price criteria in renewable energy auctions and public procurement. Furthermore, the initiative aims to help the region to reach at least 42.5% renewable energy by 2030, with solar PV as a key driver of the energy transition, hence denoting there is a huge opportunity for solar EPC in the upcoming years.

EU Solar Panel Trade 2024: Imports and Exports in USD

|

Trade Flow |

Value (€ billion) |

Largest Partners |

Share |

|

Imports |

11.1 (USD 12.1 billion) |

China |

98% of imports from China |

|

Exports |

0.7 (USD 0.76 billion) |

Switzerland, UK |

26% to Switzerland, 22% to the UK |

Source: Eurostat

The growth of citizen and cooperative solar ownership models, which are focused on decentralized generation and community participation, and increasing PV expansions, is rearranging the growth dynamics in the Germany solar EPC market. These projects generate constant EPC demand across distributed and mid-scale installations, encouraging more players to make investments in this field. In April 2024, the Federal Ministry of Economic Affairs & Energy reported that Germany’s Bundestag and Bundesrat adopted Solar Package I, which is designed to accelerate PV expansion toward 2030 climate targets. It was followed by a record 14 GW of new PV capacity in 2023, and the package simplifies deployment rules, reduces bureaucracy, and supports installations from balcony systems to large-scale ground-mounted projects. Furthermore, it also strengthens provisions for wind, bioenergy, and grid connections, forming a key part of the country’s solar strategy to ensure competitive prices in a climate-neutral electricity system.

The UK solar EPC market has gained enhanced traction, effectively driven by the rise of corporate-led renewable procurements in which businesses directly contract solar installations to meet long-term sustainability and energy sourcing objectives. Such trends support EPC activity across commercial and utility-scale projects in the country. For instance, in April 2024, RWE notified that it had signed its first UK solar power purchase agreement with Kerry Group, by committing a clean electricity supply from its Cotmoor and Copse Lodge solar projects for more than 10 years starting in 2025. It also mentioned that each project has a potential capacity of 49.9 MWac, wherein Cotmoor is already under construction, and Copse Lodge is set to follow in 2025. Hence, the presence of such corporate-led PPAs effectively drives consistent demand for EPC services in the country.

Key Solar EPC Market Players:

- Quanta Services (U.S.)

- Moss (U.S.)

- SOLV Energy (U.S.)

- Black & Veatch (U.S.)

- Bechtel Corporation (U.S.)

- Mortenson (U.S.)

- Rosendin Electric (U.S.)

- Canadian Solar (Canada)

- Sterling & Wilson Renewable Energy (India)

- Tata Power Solar Systems Limited (India)

- Vikram Solar (India)

- Jakson Group (India)

- Azure Power (India)

- ReNew Power (India)

- Enerparc AG (Germany)

- Greencells Group (Germany)

- Soventix GmbH (Germany)

- Prodiel S.L. (Spain)

- Sunseap Group (Singapore)

- SHIZEN ENERGY Inc. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Quanta Services is one of the leading EPC contractors that has a presence in utility-scale solar projects. The company benefits from its extensive engineering and construction capabilities to deliver turnkey solar solutions, which include transmission and substation integration. Quanta is focused on large-scale project execution and digital project management tools.

- Moss is yet another prominent player in this field, which specializes in engineering, procurement, and construction services for solar energy, with a prime focus on the rapid deployment of large-scale solar farms. The company has developed strong capabilities in terms of design, permitting, and execution, which are positioning it as a reliable EPC provider for both private developers and public utilities.

- SOLV Energy operates across the U.S. and is delivering turnkey solar EPC solutions for commercial, industrial, and utility-scale projects. In addition, the company integrates engineering, procurement, and construction services with performance monitoring, financing support, and O&M.

- Black & Veatch is identified as one of the most prominent global engineering and EPC firms that has a strong renewable energy portfolio, which includes solar, wind, and hybrid projects. International expansion, partnerships with utility-scale developers, and deployment of digital twin technologies for project optimization are the tactical strategies adopted by the firm to maintain its central position in this field.

- Bechtel Corporation has registered itself as one of the world’s largest engineering and construction companies that provides EPC services across energy sectors, including solar. In the solar EPC space, the company is focused on high-capacity utility projects by integrating advanced engineering, procurement, and construction methodologies.

Below is the list of some prominent players operating in the global solar EPC market:

The global solar EPC market is led by U.S.-based pioneers that are focused mainly on utility-scale installations and robust execution capabilities. Meanwhile, the India-specific players are leveraging cost-effective execution and rapid capacity deployment. Most of the international companies are opting for hybrid solutions by combining solar with energy storage and digital project delivery tools to enhance competitiveness in this field. Geographic expansion, vertical integration with manufacturing, and long-term O&M contracts are the main strategies opted for by the players to maintain their leading position in the solar EPC market. In January 2026, Tata Power Renewable Energy Limited reported that it had achieved a major milestone by commissioning 10 GW of EPC projects, which include 9.7 GW solar and 290 MW wind. In FY26’s first nine months, it added 1.88 GW capacity, which is a 33% rise over FY25, with Q3FY26 marking its highest-ever quarterly addition of 941 MW.

Corporate Landscape of the Solar EPC Market:

Recent Developments

- In January 2026, Hartek Power reported that it had secured a total of ₹353.77 crore (approximately USD 43 million) EPC contract in Karnataka for a 280 MW AC / 410 MWp DC solar PV project with an 80 MW / 320 MWh battery storage system at Challakere.

- In January 2026, Waaree Renewable Technologies Limited announced its board approval to acquire a 55% stake in Associated Power Structures Limited for ₹1,225 crore (approximately USD 150 million), making ASPL a subsidiary once completed.

- In November 2025, Sterling and Wilson Renewable Energy Limited stated that they secured a turnkey EPC contract for a 240 MW AC Solar PV project in South Africa, which is valued at approximately USD 147 million.

- Report ID: 5177

- Published Date: Feb 16, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.