Smart Grid Sensors Market Outlook:

Smart Grid Sensors Market size was valued at USD 612.7 million in 2025 and is projected to account for USD 3.34 billion by 2035, rising at a CAGR of 18.5% during the forecast period 2026 to 2035. In 2026, the industry size of smart grid sensors is evaluated at USD 726.1 million.

The smart grid sensors market is being supported by sustained investment in grid modernization, transmission expansion, and reliability improvement programs led by utilities and public-sector agencies. According to the International Energy Agency March 2025 data, global electricity demand grew by about 4.3% in 2024 and is expected to continue rising through 2027, driven by industrial activity, cooling demand, data centers, and transport electrification. This growth is placing greater emphasis on real-time visibility across transmission and distribution networks, supporting demand for grid-connected sensing equipment used for asset monitoring, fault detection, load management, and network optimization. In the United States, the U.S. Department of Energy June 2026 data reported that more than USD 13 billion in federal funding has been directed toward grid modernization and resilience initiatives through programs associated with the Bipartisan Infrastructure Law and related investments.

Globally, smart grid sensor demand is being strengthened by renewable energy integration and the need for greater operational visibility across distributed energy resources. The International Energy Agency (IEA) 2024 data estimates that global investment in grids reached approximately USD 400 billion in 2024, reflecting increasing spending on transmission and distribution networks required to support clean-energy deployment. The IEA also indicates that electricity consumption growth is accelerating due to industrial electrification, electric vehicles, and digital infrastructure, requiring utilities to monitor increasingly complex power flows. In parallel, the U.S. EIA reports that renewable generation continues to expand across utility-scale and distributed installations, increasing the requirement for real-time sensing, fault detection, and power-quality monitoring equipment.

Key Smart Grid Sensors Market Insights Summary:

Regional Highlights:

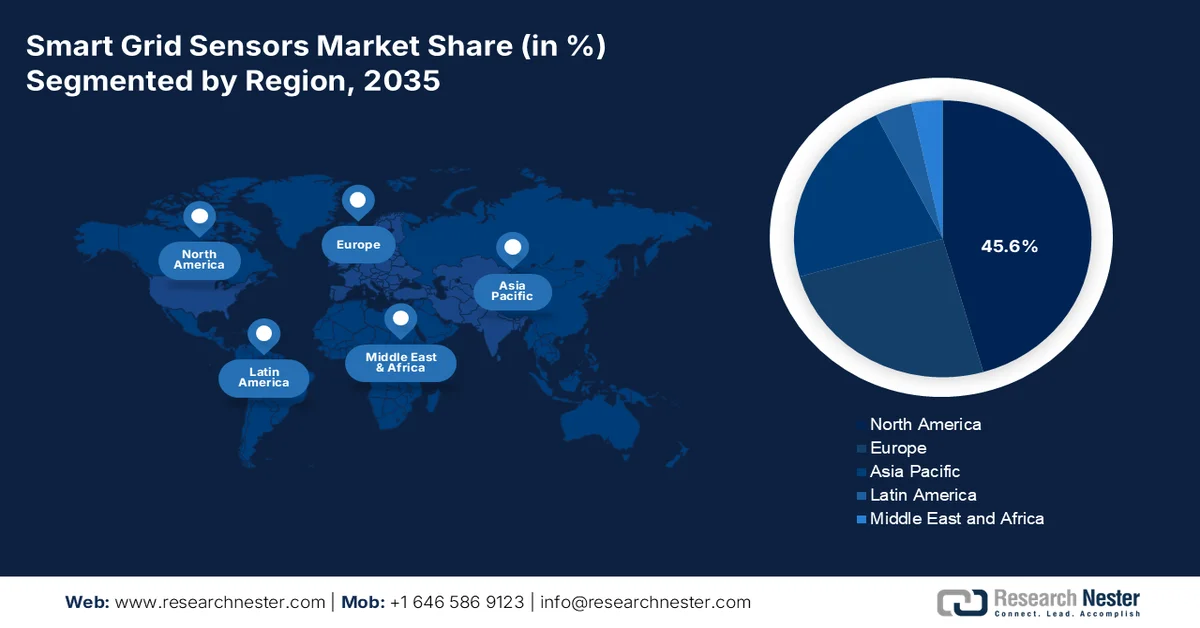

- North America is anticipated to capture 45.6% share by 2035 in the smart grid sensors market, supported by mature utility infrastructure, regulatory-led modernization initiatives, and escalating climate resilience requirements

- Asia Pacific is expected to witness the fastest expansion across 2026-2035, propelled by rapid urbanization, increasing electricity consumption, and government-backed grid modernization initiatives

Segment Insights:

- In the smart grid sensors market, Electric utility companies are projected to account for 55.3% share by 2035, stimulated by regulatory mandates for grid reliability and renewable integration

- Line sensors are anticipated to strengthen their position throughout 2026-2035 within the sensor type segment, fueled by growing requirements for real-time grid visibility, fault localization, and distributed energy resource integration

Key Growth Trends:

- Grid modernization investments

- Electrification of transportation and rising electricity demand

Major Challenges:

- Long utility procurement cycles

- High certification and compliance costs

Key Players: ABB (Switzerland),Siemens AG (Germany),Schneider Electric (France).

Global Smart Grid Sensors Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 612.7 million

- 2026 Market Size: USD 726.1 million

- Projected Market Size: USD 3.34 billion by 2035

- Growth Forecasts: 18.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, Canada

- Emerging Countries: India, South Korea, Australia, Indonesia, Vietnam

Last updated on : 15 June, 2026

Smart Grid Sensors Market - Growth Drivers and Challenges

Growth Drivers

- Grid modernization investments: Government-led grid modernization programs are a primary demand driver for smart grid sensors because utilities require real-time visibility across transmission and distribution assets to justify and manage infrastructure investments. In the U.S., the Department of Energy 2026 data announced up to USD 10.5 billion through the Grid Resilience and Innovation Partnerships Program to strengthen grid reliability, improve transmission capacity, and support advanced monitoring systems. Smart grid sensors are increasingly deployed for line monitoring, transformer health assessment, fault location, and power quality management across these projects. As utilities expand grid networks to support economic growth and electrification, sensor deployment is becoming a prerequisite for operational oversight.

- Electrification of transportation and rising electricity demand: Transportation electrification is increasing pressure on power networks and creating new requirements for grid monitoring. According to the International Energy Agency 2025 data, global electric vehicle sales exceeded 17 million units, significantly increasing electricity demand and distribution network complexity. Governments worldwide are supporting EV adoption through subsidies, charging infrastructure programs, and transportation decarbonization policies. As charging loads become more concentrated, utilities require advanced sensors to monitor feeder performance, transformer loading, and voltage fluctuations. Smart grid sensors provide real-time information that helps utilities manage demand spikes and optimize asset utilization.

Challenges

- Long utility procurement cycles: Utilities typically take months from pilot to full deployment, creating cash flow challenges for new entrants. Many require vendor pre-qualification, site visits, and multi-stage RFPs. Top companies have successfully completed a 12-month pilot with Hydro-Québec but waited additional months for a master supply agreement. During this period, the company required bridge financing. The global smart grid sensors market is expected to grow, despite utilities extending approval cycles due to workforce shortages and risk-averse procurement policies.

- High certification and compliance costs: Entering the Smart Grid Sensors market requires compliance with multiple regional standards, costing manufacturers million per product family. Smaller suppliers struggle with these upfront expenses before generating revenue. UK-based Sentinel Power Systems spent months and million obtaining IEC 61850 certification for its line sensor, delaying market entry. The government pricing constraints and certification backlogs at testing laboratories are the main challenge in smart grid sensors market.

Smart Grid Sensors Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

18.5% |

|

Base Year Market Size (2025) |

USD 612.7 million |

|

Forecast Year Market Size (2035) |

USD 3.34 billion |

|

Regional Scope |

|

Smart Grid Sensors Market Segmentation:

End user Segment Analysis

Electric utility companies is the dominant sub segment in the end user segment in the smart grid sensors market and in poised to hold the share value of 55.3% by the end of 2035. The segment driven by regulatory mandates for grid reliability and renewable integration. Utilities must expand capacity from ~270 GW to over 2,100–2,500 GW of wind, solar, and battery storage, alongside 900–1,100 GW of firm dispatchable generation such as nuclear, geothermal, or hydrogen turbines, as per the DOE April 2024 data. This massive scaling requires dense smart sensor deployment to manage bidirectional power flows, maintain voltage stability, and integrate diverse generation sources. Sensors enable utilities to monitor distributed energy resources in real time, prevent outages, and optimize dispatchable assets. Without advanced sensing infrastructure, grid operators cannot safely coordinate this heterogeneous clean energy mix, making utility companies the central driving force behind sensor market growth.

Sensor Type Segment Analysis

Line sensors represent a critical sub-segment within the sensor type category of the smart grid sensors market. These devices are mounted directly on overhead power lines or installed along underground cables to monitor real-time electrical and physical parameters. Typical measurements include current, voltage, conductor temperature, line sag, and fault-induced transients. By providing granular visibility at multiple points along a feeder, line sensors enable utilities to detect momentary interruptions, locate permanent faults precisely, and predict thermal overloads before equipment damage occurs. They are particularly valuable for integrating distributed energy resources such as rooftop solar, where bidirectional power flows complicate traditional protection schemes. Wireless communication capabilities allow line sensors to relay data to grid operators without requiring dedicated cabling. Their relatively low installation cost and high impact on reliability make them a foundational tool for grid modernization.

Technology Segment Analysis

Wireless sensor subsegment in the smart grid sensors market continues to evolve with specialized applications such as vibration monitoring for critical grid assets. In November 2023, Worldsensing, has launched a new wireless Vibration Meter featuring a tri-axial MEMS accelerometer. This device offers longer battery life, wider communication range, and a more competitive price point than existing technologies, while complying with key regulatory standards. For electric utilities, continuous vibration monitoring of transformers, switchgear, and transmission towers enables predictive maintenance by detecting anomalies such as loose windings or structural fatigue before failures occur. The extended battery life and robust wireless range make it ideal for long-term deployment in remote or hard-to-access substations. Such innovations drive wider adoption of wireless sensors across grid modernization programs, reducing downtime and maintenance costs.

Our in-depth analysis of the smart grid sensors market includes the following segments:

|

Segment |

Subsegments |

|

Sensor Type |

|

|

Component |

|

|

Technology |

|

|

Voltage Level |

|

|

Application |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Smart Grid Sensors Market - Regional Analysis

North America Market Insights

North America is dominating the smart grid sensors market and is projected to hold the regional revenue share of 45.6% by the end of 2035. The region is characterized by mature utility infrastructure, regulatory-driven modernization mandates, and increasing threats from extreme weather events. The U.S. leads with federal funding programs that support sensor deployment for grid hardening and wildfire prevention. Canada follows closely, focusing on remote community electrification and integration of distributed renewable resources. Utilities across the region are prioritizing wireless line sensors for fault detection, transformer monitors for predictive maintenance, and phasor measurement units for wide-area situational awareness.

The accelerating investments in grid reliability, renewable integration, and transmission modernization is driving the smart grid sensors market in the U.S. A key demand driver is the rapid expansion of utility-scale electricity infrastructure supported by federal funding programs. According to the U.S. Department of Energy 2026 data, the Grid Deployment Office announced USD 3.46 billion in grants to strengthen grid resilience and reliability. These projects include transmission upgrades, grid monitoring systems, and advanced operational technologies that require extensive deployment of sensors for real-time asset visibility and fault detection. As utilities modernize aging infrastructure and manage increasing electricity demand from electrification and data centers, procurement of line, transformer, and substation sensors is expected to expand steadily across the U.S. market.

The expansion of remote and off-grid renewable energy projects that require advanced monitoring and control infrastructure is driving the smart grid sensors market in Canada. According to the Government of Canada August 2025 data, the Fort Chipewyan Solar Project in Alberta, supported by approximately USD 4.5 million in federal funding. According to Natural Resources Canada, the project is the largest off-grid solar installation in Canada and supplies about 25% of the community’s electricity demand, reducing diesel consumption by approximately 650,000 litres annually. Projects of this nature depend on smart sensors for real-time monitoring of solar generation, energy storage systems, voltage conditions, and network performance. As Canada continues investing in community-scale clean energy and microgrid projects, demand for grid sensing technologies is expected to increase across remote and distributed power networks.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the smart grid sensors market. The region is driven by rapid urbanization, rising electricity demand, and government-backed grid modernization initiatives. China leads with nationwide distribution automation programs, while India focuses on reducing aggregate technical and commercial losses through feeder and transformer sensor deployment. Japan and South Korea prioritize sensor integration with advanced distribution management systems to support high renewable penetration. Australia addresses voltage violations from rooftop solar over-generation using bidirectional line sensors. Emerging economies such as Indonesia, Malaysia, and Vietnam are beginning pilot projects with multilateral funding support. International sensor suppliers increasingly establish local assembly partnerships to meet domestic content requirements and reduce landed costs.

The government's ongoing smart grid modernization initiatives under the National Smart Grid Mission (NSGM) and the Revamped Distribution Sector Scheme (RDSS) is shaping the smart grid sensors market in India. According to information published by Grid Controller of India Limited (GRID-INDIA) and government-supported smart grid programs, the Unified Real Time Dynamic State Measurement (URTDSM) Project is deploying 1,740 Phasor Measurement Units (PMUs) across networks above 400 kV, covering 356 substations and 34 control centers. By early 2025, 1,241 PMUs had already been installed on 400 kV and 765 kV transmission lines, while approximately 25 million smart meters had been deployed nationwide, as per the ORF December 2025 data. These investments are increasing demand for grid sensors that support real-time monitoring, dynamic state estimation, asset management, and grid reliability across India's expanding power infrastructure.

China’s expanding smart city initiatives are creating a supportive environment for the adoption of smart grid sensors by accelerating investments in IoT, AI, cloud computing, and large-scale sensor networks. According to the analysis, China cities are deploying advanced technologies such as digital twins, real-time monitoring systems, and extensive sensor infrastructure to support urban management and critical services. These capabilities are increasingly relevant to electricity networks, where utilities require continuous monitoring of grid assets and power flows. The ORF December 2025 data report also notes that Huawei participated in 28 of 34 China smart city projects in the Middle East, highlighting the scale of sensor-enabled infrastructure deployment. As China expands digital urbanization and smart infrastructure programs, demand for grid-monitoring sensors and related technologies is expected to strengthen alongside broader intelligent infrastructure investments.

Europe Market Insights

The Europe smart grid sensors market is shaped by cross-border renewable integration, aging transmission infrastructure, and harmonized technical standards under EU mandates. Germany, France, and the United Kingdom lead deployments, focusing on phasor measurement units for grid stability and line sensors for thermal rating optimization. Nordic countries prioritize vibration sensors for transformer condition monitoring in remote substations. Eastern European nations are accelerating sensor adoption through EU-funded cohesion programs that support grid digitization. Key drivers include the EU Network Code requirements for real-time monitoring of renewable generation connections. European utilities favor vendor-neutral, open-protocol sensors to avoid lock-in and facilitate cross-border data exchange agreements.

The accelerated energy transition and large-scale integration of renewable energy sources is shaping the smart grid sensors market in Germany. According to the Federal Ministry for Economic Affairs and Climate Action August 2022 data, Germany aims to achieve an 80% renewable share of electricity demand by 2030, supported by targets of 115 GW of onshore wind, 30 GW of offshore wind, and 215 GW of solar photovoltaic capacity. The growing complexity of managing decentralized power generation is increasing demand for grid-monitoring technologies. Germany already had more than 1.7 million decentralized renewable energy generation plants, with over 90% connected to distribution networks, creating substantial requirements for sensors that support real-time visibility, voltage control, fault detection, and grid stability across increasingly dynamic electricity systems.

The transition toward a more decentralized and digitally managed electricity system is driving the smart grid sensors market in the UK. According to UK Power Networks June 2024 data, the company delivered £91 million in customer benefits through flexibility services during 2023/24, awarded more than 1 GW of flexibility contracts, and dispatched over 7 GWh of flexible energy resources. In addition, UK Power Networks reported connecting nearly 8.3 GW of large-scale distributed generation to its network, with a further 10 GW in the connection pipeline. The increasing penetration of renewable energy, battery storage, electric vehicles, and flexible demand resources is creating strong demand for line sensors, transformer monitoring systems, and real-time grid visibility solutions to support network reliability, operational efficiency, and renewable integration.

Key Smart Grid Sensors Market Players:

- ABB (Switzerland)

- Siemens AG (Germany)

- Schneider Electric (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ABB is a dominant force in the smart grid sensors market, leveraging its extensive portfolio of grid automation and sensing technologies. The company has advanced the market through its wireless sensors and diagnostic devices, such as the Ability™ Smart Sensor, which monitors grid assets like transformers and circuit breakers in real time.

- Siemens AG plays a pivotal role in the smart grid sensors market by combining its deep expertise in power systems with advanced sensor technologies for real-time grid monitoring. The company offers a range of sensors for overhead lines, substations, and underground cables, focusing on high-precision fault detection and power quality analysis. In 2024, the company has made a net income of €10,387 million.

- Schneider Electric is a key innovator in the smart grid sensors market, emphasizing eco-efficient and interoperable sensing solutions for distribution networks. Its EcoStruxure™ Grid platform integrates smart sensors for monitoring transformer health, line temperature, and partial discharges. In 2024, the company has made a revenue of €40.2 billion.

Here is a list of key players operating in the global smart grid sensors market:

The global smart grid sensors market is highly competitive, characterized by a mix of established power automation giants and innovative sensor specialists. Key players focus on strategic initiatives such as partnerships with utility providers, expansion of IoT-enabled sensor portfolios, and investments in AI-driven analytics for predictive maintenance. Mergers and acquisitions are common to integrate advanced communication technologies, while regional players emphasize cost-effective solutions to capture local market share. For example, in February 2026, DNV announced the acquisition of Smarter Power Solutions Pty Ltd (SPS). Companies are increasingly prioritizing cybersecurity and interoperability to address grid modernization demands, with a notable push toward wireless and self-powered sensor systems for enhanced reliability.

Corporate Landscape of the Smart Grid Sensors Market:

Recent Developments

- In May 2026, G&W Electric, a global leader in innovative power grid solutions, announced the acquisition of Safegrid, a leading provider of intelligent grid monitoring solutions based in Finland with locations in Espoo and Turku.

- In April 2025, Gridspertise confirms its apex position in the smart meter revolution. This article explores its features and its production. The company was designed for one-way power flows from centralized fossil fuel plants to end users.

- In March 2025, Landis+Gyr, a global leader in energy management solutions, announced the commercial availability of the Revelo Cellular grid sensor, a versatile and powerful option for utilities seeking to add grid edge computing and sensing capabilities in an advanced meter.

- Report ID: 8343

- Published Date: Jun 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.