Silicon Carbide (SiC) Semiconductor Market Outlook:

Silicon Carbide (SiC) Semiconductor Market size was valued at USD 939.8 million in 2025 and is projected to exceed USD 4.40 billion by the end of 2035, expanding at over 16.7% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of silicon carbide semiconductor is estimated at USD 1.09 billion.

The growth dynamics of the silicon carbide semiconductor market are being reshaped by industries making a shift toward high-efficiency and high-temperature electronic solutions. Demand is being efficiently driven primarily by the rapid expansion of electric vehicles, renewable energy systems, and advanced industrial power electronics, where SiC devices offer superior performance when compared to traditional silicon-based semiconductors. As per an article published by the International Energy Agency, global electric car sales surged past 17 million in 2024, which accounted for more than 20% of new car sales worldwide, and China led this growth at 11 million units, which is nearly two-thirds of global EV sales. The global EV fleet reached 58 million cars, displacing more than 1 million barrels of oil per day, whereas China’s EV share hit 50% of new sales. In addition, Europe’s growth stagnated at 20% market share, though the UK rose to 30% and Norway neared full electrification at 88% BEV sales. In the U.S., sales climbed to 1.6 million, surpassing a total of 10% market share, thus contributing to wider market expansion.

Furthermore, the silicon carbide (SiC) semiconductor market benefits from automakers who are integrating SiC components into powertrains and charging infrastructure to improve energy efficiency and reduce system losses, whereas the renewable energy sector is adopting them in inverters for solar and wind applications. At the same time, advancements in terms of semiconductor manufacturing and increasing investments in wide bandgap technologies are enhancing production capabilities and accelerating commercialization. In October 2024, the U.S. Department of Commerce revealed that the Biden-Harris Administration announced preliminary terms with Wolfspeed for up to USD 750 million in CHIPS Act funding to build the world’s largest 200mm silicon carbide wafer ecosystem in North Carolina and expand its New York facility. Together, these projects catalyze at least USD 750 million in private investment and drive a five-fold increase in SiC device output, thus positively contributing to the market’s expansion.

Key Government and Industry Developments Accelerating Growth in the Silicon Carbide (SiC) Semiconductor Market: 2024 to 2026

|

Year |

Organization |

Initiative |

Investment/Funding |

SiC Semiconductor Market Opportunity |

|

2026 |

Semiconductor Industry Association (SIA) |

U.S. semiconductor expansion projects |

USD 645.3 billion+ |

Greater SiC manufacturing and supply chain capacity |

|

2026 |

Amtech Systems |

Wafer substrate & packaging expansion |

USD 60 million |

Enhanced SiC wafer processing and packaging ecosystem |

|

2024 |

U.S. & European Union |

Chips Act implementation |

Public funding programs |

Increased SiC R&D and fabrication investments |

Source: Official Press Releases

Key Silicon Carbide (SiC) Semiconductor Market Insights Summary:

Regional Highlights:

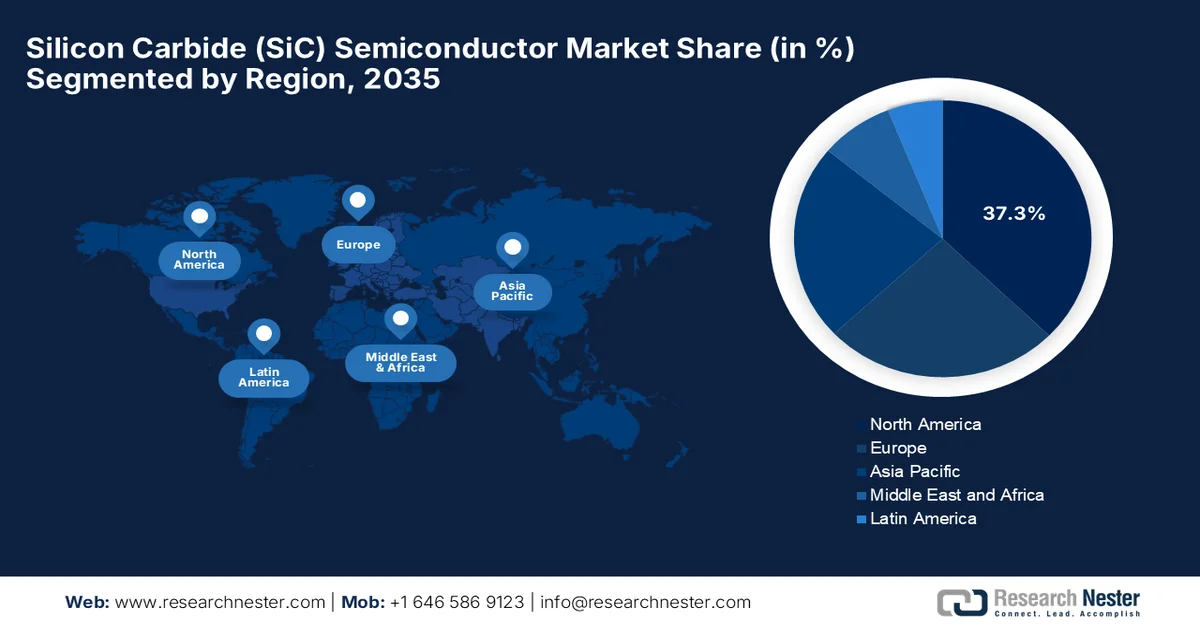

- North America is projected to command 37.3% revenue share by 2035, catalyzed by substantial investments in advanced power electronics for electric vehicles, renewable energy systems, and industrial automation

- Asia Pacific is anticipated to secure a commendable position in the silicon carbide (sic) semiconductor market throughout 2026-2035, stimulated by the rapid expansion of automotive manufacturing hubs and large-scale deployment of electric vehicles and ultra-fast charging networks

Segment Insights:

- The silicon carbide (sic) semiconductor market's SiC power modules segment is expected to capture 37.6% revenue share by 2035, accelerated by the growing transition toward system-level integration and the preference for pre-packaged power modules that simplify design complexity and speed up time-to-market

- By 2035, the 6-inch wafer segment is set to attain a noteworthy revenue share, reinforced by its manufacturing maturity, cost efficiency, and well-established supply chain for high-volume production

Key Growth Trends:

- Next-generation power grids & green energy

- Industrial & aerospace modernization

Major Challenges:

- Material defects and yield challenges in wafer production

- Competition from advanced silicon and alternative wide-bandgap materials

Key Players:Wolfspeed, Inc., Infineon Technologies AG, onsemi, STMicroelectronics N.V., ROHM Co., Ltd., Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., Toshiba Electronic Devices & Storage Corporation, Microchip Technology Incorporated, Renesas Electronics Corporation, Semikron Danfoss, GeneSiC Semiconductor Inc., Coherent Corp., SK Siltron Co., Ltd., Soitec SA, GlobalWafers Co., Ltd., Bosch GmbH, Navitas Semiconductor Corporation, Nexperia B.V., Hitachi Energy Ltd..

Global Silicon Carbide (SiC) Semiconductor Market Forecast and Regional Outlook:

-

Market Size & Growth Projections:

- 2025 Market Size: USD 939.8 million

- 2026 Market Size: USD 1.09 billion

- Projected Market Size: USD 4.40 billion by 2035

- Growth Forecasts: 16.7% CAGR (2026-2035)

-

Key Regional Dynamics:

- Largest Region: North America (37.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Taiwan, Singapore, Italy, Vietnam

Last updated on : 10 June, 2026

Silicon Carbide (SiC) Semiconductor Market - Growth Drivers and Challenges

Growth Drivers

- Next-generation power grids & green energy: Sic power modules efficiently minimize energy conversion losses in terms of massive solar inverters and wide turbine generators. Also, enhanced high-voltage handling improves the reliability of solid-state transformers used in modern electrical grids, prompting a profitable business environment for pioneers in the silicon carbide (SiC) semiconductor market. In this context, the article published in December 2025 by the World Resources Institute revealed that in 2024, clean energy accounted for more than 90% of new global electricity capacity. Global energy investment surpassed a significant value of USD 3.3 trillion in 2025, wherein almost USD 2.2 trillion was directed to clean energy, though emerging markets received only 15% of this spending despite vast renewable potential. Clean energy jobs rose to 35 million by 2023, thereby surpassing fossil fuel employment, and are projected to add 10 million more by 2030, driven by EVs, batteries, solar, and grids.

- Industrial & aerospace modernization: A wide bandgap allows SiC chips to operate flawlessly in high-temperature industrial motor drives. On the other hand, high power density drastically lowers the payload weight of power distribution units in aircraft, allowing increased uptake in the silicon carbide semiconductor market. These SiC semiconductors are being utilized in aerospace and defense systems as they can operate under extreme temperatures and pressure conditions. In November 2024, NASA Glenn Research Center demonstrated SiC JFET-R ASICs, which are capable of operating in extreme environments, including 500 °C air for over a year, Venus-like conditions at 460 °C and 9.3 MPa, and radiation exposure up to 7 Mrad TID. These circuits function across a -190 °C to +812 °C span, showing unmatched durability despite lower complexity than silicon ICs. Therefore, scaling and technology transfer enable mass production of SiC ASICs, and they readily lower barriers for deployment in aerospace and other harsh-environment applications.

Global Silicon Carbide (SiC) Exports by Country in 2024 - Trade Value & Shipment Volume

|

Reporter |

Trade Value (1000 USD) |

Quantity (Kg) |

|

China |

317,482.63 |

345,806,000 |

|

Brazil |

53,597.44 |

39,899,500 |

|

Germany |

51,636.88 |

25,897,300 |

|

Netherlands |

45,962.01 |

47,527,900 |

|

Japan |

42,652.05 |

— |

|

U.S. |

28,613.56 |

— |

|

European Union |

24,219.31 |

9,547,300 |

|

Other Asia, nes |

23,316.43 |

— |

|

Sweden |

20,170.17 |

9,025,060 |

|

Belgium |

17,625.33 |

12,799,200 |

|

Romania |

14,633.05 |

12,899,800 |

|

South Africa |

9,361.53 |

12,250,800 |

Source: WITS

Challenges

- Material defects and yield challenges in wafer production: The presence of crystal defects in SiC wafers, such as micropipes, dislocations, and stacking faults, is the major challenge for the silicon carbide semiconductor market. Therefore, these defects can remarkably impact device reliability, efficiency, and long-term performance, especially in the case of high voltage applications. The wafer quality has improved over the past few years, but still, achieving defect-free large-diameter wafers is considered to be difficult. As wafer sizes increase from 4-inch to 8-inch and beyond, maintaining uniform crystal integrity becomes even more complex. Apart from this, lower yields directly translate into higher production costs and reduced profitability for manufacturers, whereas continuous R&D is required to improve crystal growth techniques and enhance overall wafer quality.

- Competition from advanced silicon and alternative wide-bandgap materials: There are several proven advantages associated with SiC, but it still witnesses a very competition from advanced silicon technologies and other wide-bandgap materials such as gallium nitride. Silicon-based solutions offer better efficiency and cost-effectiveness for mid-power applications, which can limit SiC adoption in some of the segments. Meanwhile, GaN is gaining traction for high-frequency and fast-switching applications, thereby creating overlapping competition in the silicon carbide (SiC) semiconductor market. This, in turn, forces SiC manufacturers to justify their high costs through superior performance benefits. Therefore, the market positioning challenge becomes especially critical in consumer-driven sectors wherein this price sensitivity outweighs efficiency gains, thereby ultimately causing a slowdown to broader penetration of SiC solutions.

Silicon Carbide (SiC) Semiconductor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

16.7% |

|

Base Year Market Size (2025) |

USD 939.8 million |

|

Forecast Year Market Size (2035) |

USD 4.40 billion |

|

Regional Scope |

|

Silicon Carbide (SiC) Semiconductor Market Segmentation:

Type Segment Analysis

Under the type segment, the SiC power modules segment is anticipated to capture the highest revenue share of 37.6% in the silicon carbide (SiC) semiconductor market during the forecast period. The segment’s dominance is effectively propelled by a major shift toward system-level integration rather than discrete components, as OEMs prefer pre-packaged power modules to reduce design complexity and accelerate time-to-market. Demand is also being strengthened by the rapid electrification of commercial vehicles and high-power charging stations, where modular architectures improve scalability and thermal management. In September 2024, Wolfspeed introduced 2300V baseplate-less silicon carbide modules, which are built on 200mm wafer technology, designed for 1500V DC bus applications in renewable energy, storage, and fast-charging infrastructure. These modules were developed in partnership with EPC Power, and they will enhance utility-scale solar and storage systems with scalable, high-performance conversion.

Wafer Size Segment Analysis

In the wafer size segment, the 6-inch wafer is projected to gain a noteworthy revenue share in the silicon carbide semiconductor market by the end of 2035. Their established balance between manufacturing maturity, cost efficiency, and production yield is the main factor driving the sub-segment’s leadership in this sector. They are also supported by a more stable and qualified supply chain, making them the preferred choice for mass production in electric vehicles, industrial power systems, and renewable energy applications. In April 2024, ROHM Group company SiCrystal and STMicroelectronics expanded their long-term supply agreement for 150mm SiC substrate wafers, which was valued at a minimum of USD 230 million, and the production took place in Nuremberg, Germany. This particular deal strengthens ST’s supply chain and supports its ramp-up in SiC device manufacturing for automotive and industrial customers worldwide, thus denoting a wider segment scope.

Application Segment Analysis

By the conclusion of the forecast period, the automotive industry is predicted to grow at a considerable rate in the SiC semiconductor market. The segment’s growth is effectively fueled by rising utilization in traction inverters, onboard chargers, and DC-DC converters to improve driving range and energy efficiency. Automakers are also prioritizing high-voltage (800V+) architectures, which significantly benefit from SiC’s superior switching performance and thermal stability. For instance, in December 2025, Wolfspeed announced that its silicon carbide MOSFETs will power Toyota’s battery electric vehicle platforms, specifically onboard charger systems, in order to enhance efficiency, reliability, and charging performance. It significantly reduces energy loss and enables faster charging. The company’s SiC technology improves driving range and lowers lifetime costs, aligning with Toyota’s global electrification strategy.

Our in-depth analysis of the silicon carbide semiconductor market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Wafer Size |

|

|

Application |

|

|

Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Silicon Carbide (SiC) Semiconductor Market - Regional Analysis

North America Market Insights

North America silicon carbide semiconductor market is forecasted to attain the largest revenue share of 37.3% during the discussed timeframe. The region’s dominance is largely propelled by significant investments in advanced power electronics for electric vehicles, renewable energy systems, and industrial automation. In addition, rapid expansion of high-voltage EV infrastructure, increasing adoption of SiC-based power devices in data centers, and strong R&D activities supported by government initiatives are also solidifying regional growth. As per the article published by the Congress Government in April 2023, semiconductors are considered vital to both economic and national security, which are powering industries from AI and defense to automotive and communications. The U.S. based firms lead globally in terms of chip design 46%, manufacturing equipment 42%, and design software 72%, with about 11% of wafer fabrication and 5% of assembly, test, and packaging capacity being domestic.

Momentum in the U.S. silicon carbide semiconductor market is amplified by federal funding initiatives, which are aimed at onshore technology sovereignty, thereby forcing massive investment into expanding domestic wafer fabrication plants and establishing secure local supply chains for raw materials. The SiC semiconductor market benefits from a dense concentration of aerospace, defense, and high-voltage grid infrastructure players who are dependent on the material's superior thermal performance, along with hyperscale data center operators upgrading power distribution architectures to sustain intensive computation workloads. For instance, Coherent Corp. in April 2026 announced advancements in silicon carbide thick epitaxy on 150mm and 200mm platforms, which enable multi-kilovolt devices up to 10kV for AI datacenters and industrial power systems. The company also notes that these innovations support compact, energy-efficient conversion architectures for renewables, rail, fast-charging, and grid infrastructure, thereby meeting the reliability demands of large-scale deployments.

US Semiconductor Industry Investment Projects 2020-2026: Chip Manufacturing, Packaging & Materials Facilities

|

Company |

State |

Project Type |

Category |

Project Size |

|

Absolics |

GA |

New Facility |

Materials |

USD 343 million |

|

AGC Electronic America |

OR |

Expansion/Modernization |

Materials |

- |

|

Air Liquide |

AZ |

New Facility |

Materials |

USD 60 million |

|

Air Liquide |

ID |

New Facility |

Materials |

USD 250 million |

|

Air Liquide |

US |

New Facility |

Materials |

USD 50 million |

|

Akash Systems |

CA |

New Facility |

Semiconductors |

USD 121 million |

|

AMD |

NY |

New Facility |

Chip Design |

USD 3.3 million (across 2 locations) |

|

AMD |

NY |

New Facility |

Chip Design |

USD 3.3 million (across 2 locations) |

|

Amkor |

AZ |

New Facility |

Packaging |

USD 7 billion |

|

Amorphyx |

OR |

Expansion |

Semiconductors |

- |

Source: SIA

With a strengthened focus on advanced automotive integration, green energy deployment, and deep technical research, the silicon carbide semiconductor market in Canada is forecasted to witness surging growth in the next decade. The market is mainly propelled by the country's strategic transition toward zero-emission vehicle targets, which drives close integration between domestic automotive component manufacturers and international electric vehicle supply chains to develop powertrain and thermal management sub-assemblies. Based on government data in May 2026, it plans to spin off Canada’s Photonics Fabrication Centre (CPFC) into a commercial entity to expand domestic photonic semiconductor manufacturing and strengthen Canada’s technological sovereignty. It is anchored in Ottawa, the CPFC is North America’s only end-to-end pure play compound semiconductor facility, supporting industries from AI data centers and quantum technologies to defense and aerospace.

APAC Market Insights

The Asia Pacific SiC semiconductor market is forecasted to hold a commendable position in the global dynamics from 2026 to 2035. The region’s progress in this sector is majorly fueled by automotive manufacturing hubs, particularly in China, Japan, and South Korea, where the rapid mass-production of electric vehicles and ultra-fast charging networks drives an insatiable demand for SiC modules. This momentum is also sustained by massive government mandates for clean energy transition, which drives widespread adoption of SiC components in large-scale solar farms, wind power installations, and high-voltage direct current grid networks across the region. In June 2023, the Ministry of Economy, Trade and Industry (METI), Japan, announced financial support of USD 70.5 million to Sumitomo Electric Industries for the production of silicon carbide wafers. This intervention is classified as a national-level financial grant, and it aims to strengthen domestic semiconductor manufacturing capabilities and enhance supply chain resilience, thus suitable for surging market growth.

The country's massive electric vehicle ecosystem, which stands as the world's largest consumer and manufacturer of SiC-driven powertrains, inverters, and ultra-fast charging infrastructure, is responsibly uplifting the silicon carbide semiconductor market in China. This momentum is also being accelerated by massive state-directed capital investments, which are aimed at building a fully localized, end-to-end supply chain that spans raw substrate materials, advanced crystal growth epitaxy, and specialized fabrication plants, to eliminate reliance on foreign chip technologies. In May 2023, Infineon signed a long-term agreement with China-based SICC to secure high-quality 150mm silicon carbide wafers and boules, thereby covering a double-digit share of its future demand. This deal deliberately supports Infineon’s transition to 200mm wafer technology, and it strengthens supply chain resilience for growing automotive, solar, EV charging, and energy storage industries.

In India, the silicon carbide semiconductor market is growing at a rapid pace owing to the country’s extensive focus on localized electronics manufacturing and cleaner transport. Growth is heavily energized by the domestic electric vehicle revolution, particularly across the massive two-wheeler, three-wheeler, and public transit segments, which fuels a rising demand for high-efficiency SiC-based drivetrains, onboard chargers, and fast-charging networks. This momentum is further amplified by central government fiscal incentives, which proactively encourage global and domestic players to set up advanced packaging, testing, and wafer fabrication facilities in the country. As per an article published by Press Information Bureau (PIB) in August 2025, India’s Union Cabinet approved four new semiconductor projects under the India Semiconductor Mission with a combined generous investment of about USD 550 million, including the country’s first commercial silicon carbide compound semiconductor fab in Odisha. Besides, this SiCSem facility will manufacture SiC devices with applications in missiles, defense, EVs, railways, fast chargers, data centers, and solar inverters, whereas other projects in Punjab and Andhra Pradesh expand discrete and advanced packaging capabilities.

Europe Market Insights

Europe silicon carbide semiconductor market has acquired a prominent position as a vital center for high-performance engineering, automotive innovation, and industrial decarbonization. Growth in this region is fundamentally driven by certain stringent vehicle emission regulations and aggressive targets for electrification, which compel major automotive brands and tier-one suppliers to integrate SiC power modules into next-generation luxury electric vehicles and high-power charging networks. For instance, in March 2024, the European Commission approved a USD 2.2 billion Italy State aid measure with the main goal to support STMicroelectronics in building a new silicon carbide semiconductor manufacturing facility in Catania, Sicily. This project will advance 200mm SiC technology, strengthen the region’s semiconductor value chain, and ensure supply chain resilience under the Europe’s Chips Act, thus suitable for bolstering the region’s market growth.

The presence of premium domestic car manufacturers and tier-one automotive suppliers who are aggressively embedding SiC power modules into next-generation electric vehicle platforms is responsible for the expansion of Germany silicon carbide semiconductor market. This momentum is also carried forward by substantial industrial investments and government backing under regional microelectronics initiatives, which are funding the construction of massive, SiC fabrication plants and research facilities on the country’s soil to secure a domestic supply of wide-bandgap chips. In May 2026, the European Commission approved a total of USD 310 million in Germany State aid to strengthen the semiconductor supply chain with two first-of-a-kind facilities. In this context, Carl Zeiss will receive USD 239 million to build a plant in Oberkochen for next-generation EUV optical columns, which are important for advanced lithography machines. Zadient Materials Europe GmbH will get USD 71 million to establish a novel factory in Bitterfeld for ultra-pure silicon carbide source materials, thereby enhancing supply security and energy efficiency under the Europe’s Chips Act.

The UK silicon carbide semiconductor market is gaining momentum due to the country's increasing focus on semiconductor innovation, electrified transportation, and next-generation energy systems. Growth is also supported by strong collaboration between industry, research institutions, and government-led technology initiatives, which are aimed at strengthening domestic semiconductor capabilities. In May 2023, the country’s government announced the launch of its National Semiconductor Strategy, which identifies compound semiconductors as a strategic area of national strength and commits up to USD 250 million for 2023-2025, with plans to invest up to USD 1.25 billion in the next decade. This strategy has an increased priority on semiconductor R&D, chip design, intellectual property, and compound semiconductor technologies through targeted infrastructure development and innovation initiatives, thus denoting an optimistic market opportunity.

Key Silicon Carbide (SiC) Semiconductor Market Players:

- Wolfspeed, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- onsemi (U.S.)

- STMicroelectronics N.V. (Switzerland)

- ROHM Co., Ltd. (Japan)

- Mitsubishi Electric Corporation (Japan)

- Fuji Electric Co., Ltd. (Japan)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- Microchip Technology Incorporated (U.S.)

- Renesas Electronics Corporation (Japan)

- Semikron Danfoss (Germany)

- GeneSiC Semiconductor Inc. (U.S.)

- Coherent Corp. (U.S.)

- SK Siltron Co., Ltd. (South Korea)

- Soitec SA (France)

- GlobalWafers Co., Ltd. (Taiwan)

- Bosch GmbH (Germany)

- Navitas Semiconductor Corporation (U.S.)

- Nexperia B.V. (Netherlands)

- Hitachi Energy Ltd. (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Wolfspeed, Inc. has become a pioneer in the space of silicon carbide technology and maintains one of the industry's most extensive SiC intellectual property portfolios. The company operates a vertically integrated business model that is structured around crystal growth, wafer manufacturing, device fabrication, and advanced packaging.

- Infineon Technologies AG is yet another foundational player in this SiC semiconductor market and has registered itself as a leading supplier of SiC power semiconductors. The firm is highly focused on enhancing power efficiency and system integration through continuous product innovation as well as manufacturing expansion.

- onsemi has established itself as a major player in the SiC semiconductor market through its EliteSiC™ portfolio and strategic focus on electric mobility and energy infrastructure. The company has achieved several long-term supply agreements with automotive manufacturers, and it continues to expand its SiC production capabilities.

- STMicroelectronics N.V. is one of the strongest global leaders in silicon carbide power devices, which is supplying SiC MOSFETs, diodes, and power modules to automotive and industrial customers across the globe. The company has deliberately strengthened its market position through tactical partnerships with EV manufacturers and remarkable investments in SiC substrate sourcing and production capacity.

- ROHM Co., Ltd. is a prominent innovator in terms of silicon carbide power semiconductor technology, which offers a portfolio of SiC MOSFETs, Schottky barrier diodes, and power modules. In addition, the company proactively collaborates with automotive OEMs and power system manufacturers with the main goal of developing high-efficiency power solutions.

Here is a list of key players operating in the global SiC semiconductor market:

The global silicon carbide semiconductor market hosts semiconductor manufacturers, wafer suppliers, and power electronics specialists. Leading companies in this field are highly focused on expanding SiC wafer production capacity, advancing larger wafer technologies, and strengthening vertically integrated supply chains with the main goal of securing substrate availability and reducing costs. Strategic initiatives adopted by the SiC semiconductor market participants include investments in 200mm and next-generation 300mm SiC wafer manufacturing, long-term supply agreements with automotive OEMs, partnerships for EV and renewable energy applications, and the development of high-efficiency power devices for AI data centers and industrial systems. For instance, in November 2025, GE Aerospace introduced its Gen-4 SiC MOSFET chips, which deliver 1200V capability, ultra-low resistance, and a record 200°C temperature rating, enabling faster switching, higher efficiency, and greater durability for next-gen power systems.

Corporate Landscape of the Silicon Carbide (SiC) Semiconductor Market:

Recent Developments

- In June 2026, Infineon Technologies introduced the industry’s first-ever silicon carbide bidirectional switch based on its 750 V CoolSiC™ G2 technology, thereby integrating two power switches into a single top-side-cooled package to simplify system design while improving efficiency and reliability.

- In January 2026, Wolfspeed announced a major silicon carbide technology breakthrough with the successful production of a single-crystal 300mm, which is a 12-inch SiC wafer, and this is a significant step toward high-volume commercialization and enhanced manufacturing scalability.

- Report ID: 8610

- Published Date: Jun 10, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.