Automotive Semiconductor Market Outlook:

Automotive Semiconductor Market size was valued at USD 51.1 billion in 2025 and is expected to grow to USD 106.4 billion by 2035, at a CAGR of 8.5% over the forecast period, i.e., 2026-2035. In 2026, the industry size of automotive semiconductor is estimated at USD 55.4 billion.

The surging electric vehicle adoption, advanced driver-assistance systems, and increased vehicle connectivity are responsible factors driving the automotive semiconductor market. According to the article published by the World Resources Institute in December 2025, electric vehicle adoption is led by Norway, with almost 92% of passenger car sales in 2024, which is followed by Sweden, Denmark, Finland, the Netherlands, and China, with nearly half of all sales. Besides, China dominates in total volume, selling 11.3 million EVs in 2024, whereas the U.S. accounted for around 10% of sales. This expansion is an S‑curve pattern, where adoption surges once EVs become cost‑competitive, as seen in Norway’s rise from below 1% to more than 90% in a span of 14 years. In order to meet climate agendas, major economies such as China, Europe, and the U.S need to scale EV adoption as quickly as these leaders, denoting a huge opportunity for automotive semiconductors.

Furthermore, the automobiles are becoming software-defined, high-compute platforms in which the silicon content per vehicle is rising at a rapid pace, efficiently boosting demand for power electronics, sensors, and microcontrollers. The automotive semiconductor market is making a shift towards components such as Silicon Carbide (SiC) and Gallium Nitride (GaN), with the main goal of improving EV charging, along with power management efficiency. In May 2023, the article published by the U.S. Department of Energy stated that worldwide decarbonization has fueled growth in power electronics, wherein the automotive, consumer, industrial motors, and home appliances are identified as the largest demand sectors. In addition, silicon dominates with 96% market share in 2022, whereas SiC and GaN are gaining enhanced traction as wide‑bandgap alternatives are offering higher efficiency and performance. At the same time, SiC is expected to reach 17% market share by 2028, largely fueled by EV inverters and charging infrastructure, hence positively impacting the market’s exposure.

Key Automotive Semiconductor Market Insights Summary:

Regional Highlights:

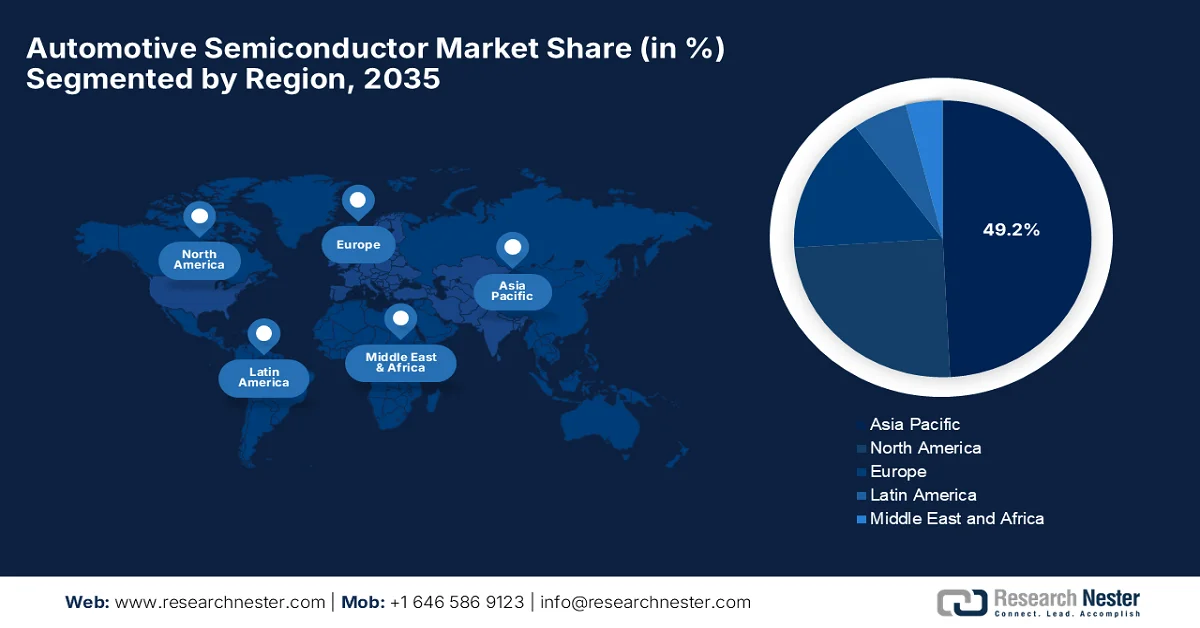

- Asia Pacific automotive semiconductor market is projected to secure a 49.2% revenue share by 2035, bolstered by large-scale vehicle manufacturing and accelerating EV adoption alongside semiconductor localization initiatives

- North America is poised to witness the fastest growth during 2026–2035, fueled by expanding automotive demand and intensified investments in semiconductor R&D and supply chain resilience

Segment Insights:

- Passenger vehicles segment in the automotive semiconductor market is anticipated to account for a 60.6% share by 2035, propelled by high production volumes and increasing integration of advanced infotainment, safety, and connectivity features

- Discrete power segment is expected to capture a considerable share by 2035, stimulated by rising demand for power semiconductors supporting vehicle electrification and efficient powertrain systems

Key Growth Trends:

- Advanced driver assistance systems

- Increased electronics content per vehicle

Major Challenges:

- Supply chain disruptions

- Dependency on foundries

Key Players: Infineon Technologies AG (Germany), NXP Semiconductors N.V. (Netherlands), STMicroelectronics N.V. (Switzerland), Texas Instruments Inc. (U.S.), Renesas Electronics Corporation (Japan), ON Semiconductor (U.S.), Continental AG (Germany), Robert Bosch GmbH (Germany), Qualcomm Technologies, Inc. (U.S.), Analog Devices, Inc. (U.S.), Micron Technology, Inc. (U.S.), Toshiba Corporation (Japan), ROHM Semiconductor (Japan), Nexperia (Netherlands), Diodes Incorporated (U.S.), GlobalFoundries (U.S.), Valens Semiconductor Ltd (Israel), Samsung Electronics Co., Ltd. (South Korea), Nvidia Corporation (U.S.), Intel Corporation (U.S.), Tata Electronics Ltd (India), Broadcom Inc. (U.S.).

Global Automotive Semiconductor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 51.1 billion

- 2026 Market Size: USD 55.4 billion

- Projected Market Size: USD 106.4 billion by 2035

- Growth Forecasts: 8.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (49.2% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Vietnam, Brazil, Mexico, Indonesia

Last updated on : 6 April, 2026

Automotive Semiconductor Market - Growth Drivers and Challenges

Growth Drivers

- Advanced driver assistance systems: There has been escalating adoption of features such as automatic emergency braking, adaptive cruise control, lane‑keeping assist, and progression toward higher autonomy levels. This factor boosts demand for sensors, radar, LiDAR, cameras, AI processors, and high‑performance SoCs, thereby benefiting the overall automotive semiconductor market. In this context, as per an article published by Press Information Bureau (PIB) in February 2026, the Ministry of Road Transport & Highways has set up a Centre of Excellence for Road Safety at IIT Madras to integrate global best practices and strengthen collaboration between academia, industry, and the government of India. The article also stated that advanced traffic management systems with AI-based monitoring, ANPR cameras, and ADAS rules for heavy vehicles are being introduced to enhance safety on national highways, hence positively impacting automotive semiconductor market growth.

- Increased electronics content per vehicle: Modern cars are essentially computers on wheels, wherein the electronics control safety, infotainment, navigation, connectivity, climate, and comfort systems. This massively increases microcontrollers, memory chips, and logic IC requirements per vehicle, prompting a profitable business environment for the automotive semiconductor market. Alliance for Automotive Innovation in August 2025 stated that, in terms of the automotive semiconductor supply chain, each car requires over 1,700 chips to power control, safety, and emerging technologies. It mentions that about 95% of these are foundational chips, designed for durability under harsh conditions. Besides, the U.S.-based automakers remain heavily reliant on foreign supply, whereas China is making aggressive investments in foundational chip production.

- Connected and software‑defined vehicles: Connected car technologies, i.e., OTA updates, telematics, and software‑defined vehicle systems, depend on advanced semiconductors for processing, data security, and network functionality. In this regard, the ARXIV Organization in July 2024 revealed that modern vehicles are evolving into software-defined vehicles by integrating sensors, actuators, and complex systems that may require up to 1 billion lines of code for full autonomy. Therefore, to manage this complexity, researchers propose deterministic SDVs built on four pillars: outcome-drivennetwork configurator, data layer configurator, hypervisor configurator, and vehicle abstraction layer, all coordinated by a software orchestrator. At the same time, this approach aims to simplify service development, improve reliability, and support adaptive vehicular applications, hence denoting an optimistic opportunity for the automotive semiconductor market.

Challenges

- Supply chain disruptions: The automotive semiconductor market is immensely susceptible to supply chain concerns that are disrupted by the globalized production network. Events such as geopolitical tensions and natural disasters can cause halts in production or delay shipments of highly essential components such as wafers and chips. At the same time, automotive chips sometimes rely on foundries that are situated in specific regions, in turn making the supply chain concentrated and fragile. Moreover, the aspect of long lead times for semiconductor fabrication, which can be several months, complicates the recovery from disruptions. In addition, automakers mostly operate on just-in-time inventory systems, leaving little buffer during shortages. Therefore, the mismatch between supply flexibility and demand volatility has led to production halts and loss of revenue across the industry.

- Dependency on foundries: Most of the automotive semiconductor companies are actually fabless, and they depend on third-party foundries for manufacturing. This dependency is a major bottleneck for the automotive semiconductor market, especially during peak demand scenarios when foundries prioritize higher margin sectors such as consumer electronics. Also, the automotive chips, often produced using older nodes, may receive lower priority. Therefore, the limited control over production schedules and capacity allocation can ultimately cause delays and shortages. In addition, the geopolitical factors affecting major foundry locations can disrupt supply. In this context, this reliance reduces flexibility and increases the overall vulnerability, leading some companies to explore vertical integration or long-term partnerships in order to secure supply.

Automotive Semiconductor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.5% |

|

Base Year Market Size (2025) |

USD 51.1 billion |

|

Forecast Year Market Size (2035) |

USD 106.4 billion |

|

Regional Scope |

|

Automotive Semiconductor Market Segmentation:

Vehicle Type Segment Analysis

Under the vehicle type segment, passenger vehicles are forecasted to gain the largest revenue share of 60.6% in the automotive semiconductor market during the discussed time frame. The segment’s dominance is largely ascribed to mass market volumes and the inclusion of advanced features such as infotainment, safety systems, and connectivity. In this context, the article published by Invest India reported that India’s automobile sector recorded a total turnover of USD 240 billion in FY 2024-25, wherein the exports surpassed 5.3 million units, including 770,000 passenger vehicles. The report underscored that leading companies such as Skoda Auto Volkswagen India export about 30% of their production, whereas Maruti Suzuki exports nearly 280,000 units on a yearly basis, which indicates insatiable demand for automotive semiconductors in the years ahead.

Component Segment Analysis

By the conclusion of the forecast period, the discrete power segment, which is a part of the component, is anticipated to grow with a considerable share in the automotive semiconductor market. The automotive industry is highly dependent on semiconductors across all component categories, as these chips support vehicle networking, electrification, and the expansion of shared mobility services. In this context, Infineon Technologies, in October 2023, signed a multi-year agreement with Hyundai Motor Company and Kia Corporation to supply silicon carbide (SiC) and silicon (Si) power semiconductors, securing manufacturing capacity through 2030. These power semiconductors are highly essential for vehicle electrification, enabling efficient inverters and powertrain systems in EVs. Hence, such tactical strategies adopted by the players underscore the growing demand for high-quality discrete power devices in the automotive sector.

Application Segment Analysis

In the automotive semiconductor market, the body electronics is predicted to grow at a significant rate over the forecast period. The growing need for semiconductor components in safety-related applications is mainly driven by the stringent regulatory requirements and industry standards. As per an article published by PIB in December 2025, India’s national highway network expanded at a noteworthy rate, and it reached 146,560 km, which is a 61% growth since 2014, with access-controlled high-speed corridors increasing from 93 km to 3,052 km. Besides, the Ministry of Road Transport & Highways improved the vehicle safety standards by mandating high-security registration plates and integrating advanced driver assistance systems in terms of new vehicles. Therefore, these measures reflect the emerging nation’s focus on modernizing infrastructure along with embedding advanced electronics and safety systems in vehicles.

Our in-depth analysis of the global automotive semiconductor market includes the following segments:

|

Segment |

Subsegments |

|

Vehicle Type |

|

|

Component |

|

|

Application |

|

|

Fuel Type |

|

|

Functionality |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Semiconductor Market - Regional Analysis

APAC Market Insights

The Asia Pacific automotive semiconductor market is anticipated to capture the largest revenue share of 49.2% by the end of 2035. The region’s dominance is efficiently propelled by mass vehicle production in China, India, and Japan, coupled with rising EV adoption and semiconductor localization. In October 2023, PIB stated that the Union Cabinet approved a Memorandum of Cooperation between India and Japan to strengthen semiconductor supply chain resilience. This particular MoC will be in force for five years, fostering both government-to-government and business-to-business collaboration. It aims to boost employment opportunities in IT by reaping the complementary strengths of both nations. Also, the collaborative effort benefits industries that rely heavily on advanced electronics, digital technologies, and semiconductor components, most notably IT, telecommunications, automotive, consumer electronics, and industrial manufacturing.

In China, the automotive semiconductor market is growing exponentially, which is influenced by factors such as a well-established automotive industry and increasing vehicle production. The country’s strong government support for the semiconductor sector deliberately accelerates market expansion. In June 2025, a CBBC Organization article revealed that the country’s semiconductor industry is growing at an extensive pace, which is driven by government investment and innovation, with strong demand from automotive, EVs, AI, and 5G sectors. At the same time, key players such as SMIC, YMTC, and Huawei’s HiSilicon are advancing in chip design and manufacturing, though U.S. export controls and reliance on ASML’s EUV machines need to be addressed. Besides, more than USD 192 billion has been invested in fabs since 2014, hence reflecting a lucrative opportunity as a global semiconductor powerhouse.

The strong government initiatives promoting electric vehicle adoption are the main factor driving growth in the automotive semiconductor market in India. This shift is increasing the demand for semiconductors used in motor control units, battery management systems, and power electronics. As per an article published by PIB in February 2024, India’s semiconductor mission advanced with Cabinet approval for three new units under the USD 91 billion programme. Tata Electronics, with Taiwan’s PSMC, will make an investment of USD 11 billion to build a fab in Gujarat, producing high-performance and automotive chips. The report highlighted that Tata Semiconductor Assembly and Test will set up a USD 3.3 billion packaging unit in Assam, whereas CG Power, with Renesas and Stars Microelectronics, will invest almost USD 915 million in Gujarat for specialized chips, thus suitable for bolstering the overall country’s market growth.

North America Market Insights

The North America automotive semiconductor market is expected to register the fastest growth rate from 2026 to 2035. The region’s prominence is largely attributable to the expansion of the automotive sector and increasing demand for vehicles across the region. In addition, the surging technological advancement and research and development are another key factor supporting market growth. As per an article published by the U.S. Department of Commerce in November 2024, the Biden-Harris Administration allocated GlobalFoundries up to USD 1.5 billion under the CHIPS Incentives Program to strengthen U.S. semiconductor supply chains. This funding is estimated to support GF’s USD 13 billion investment over the next decade in New York and Vermont facilities, producing chips vital for automotive, defense, aerospace, and communications.

The strong technological base and presence of leading industry players are responsible for driving the U.S. automotive semiconductor market. The rapid development of technologies such as advanced driver assistance systems and autonomous driving is fueling demand for high-performance semiconductors. In December 2023, the U.S. Department of Commerce announced a new industrial base survey to assess the country’s semiconductor supply chain, highly focused on legacy chips critical for industries such as automotive, telecom, and defense. The survey was launched in January 2024, and it aimed to identify sourcing practices. At the same time, safeguarding the legacy chip supply chain is a matter of national security, requiring industry collaboration, hence indicating a positive market outlook.

Canada automotive semiconductor market has gained enhanced exposure backed by a major shift towards autonomous driving technologies. The country’s market also benefits from government investments, aimed at securing supply chain resilience and fostering continued innovations in the years ahead. Based on the government data published in July 2024, Canada announced a total of USD 120 million investment through the Strategic Innovation Fund to support CMC Microsystems in a USD 220 million project expanding semiconductor manufacturing and commercialization. The initiative will establish the FABrIC network, thereby solidifying the country’s semiconductor and smart sensor industry. FABRIC is highly focused on industries such as automotive, telecom, and low-carbon technology, and it likely to boost domestic production and supply chain resilience.

Europe Market Insights

Europe automotive semiconductor market is expected to witness noteworthy growth in the upcoming years. The region’s prominence in this field is largely driven by well-established semiconductor manufacturing hubs in countries such as the Netherlands, Germany, and France. These countries provide extensive support for market expansion, and the region’s focus on green energy and sustainability is readily accelerating the adoption of electric vehicles, boosting demand. The European Chips Act, which came into force in September 2023, aims to strengthen the region’s semiconductor ecosystem, reduce external dependencies, and boost technological sovereignty. Besides, it has set a target of doubling Europe’s global market share in semiconductors to 20% by 2030, concentrating on research, innovation, manufacturing, skills, and supply chain resilience. In 2025, the Semicon Coalition of the region’s member states signed a declaration for a Chips Act 2.0, thereby solidifying Europe’s ambition to build a resilient and competitive semiconductor industry.

Electrification, advanced power management, and the shift toward autonomous driving are certain trends that are reshaping the growth dynamics of the automotive semiconductor market in Germany. Strong government support through policies and subsidies complements the domestic automotive manufacturing base, whereas initiatives such as Industry 4.0 are encouraging innovation in connected and autonomous vehicle technologies. In November 2024, the International Trade Administration reported that Germany’s automotive industry, which was valued at USD 611 billion in 2023, is the region’s largest sector with two-thirds of turnover generated abroad. The government targets 15 million EVs by 2030, whereas charging infrastructure is also readily expanding, with almost 116,000 public points installed by 2023. A total of USD 6.7 billion in investments in the Deutschlandnetz fast‑charging network denotes a huge opportunity for automotive semiconductors in the country.

The UK automotive semiconductor market maintains a strong position in the region owing to its expertise in chip design, intellectual property, and advanced compound semiconductors. The sector is currently undergoing a structural shift as manufacturers transition toward connected automated vehicles, which require a higher volume of chips when compared to internal combustion engines. In May 2023, the article published by the government of the UK states that the country’s national semiconductor strategy aims to secure world-leading strengths in future semiconductor technologies by leveraging R&D, chip design, IP, and compound semiconductors. It is mainly focused on three objectives, i.e., growing the domestic sector, enhancing supply chain resilience, and protecting national security. The strategy targets industries reliant on semiconductors, including automotive, AI, high-performance computing, defence, and healthcare, and includes up to USD 1.2 billion investment over the next decade to foster innovation.

Key Automotive Semiconductor Market Players:

- Infineon Technologies AG (Germany)

- NXP Semiconductors N.V. (Netherlands)

- STMicroelectronics N.V. (Switzerland)

- Texas Instruments Inc. (U.S.)

- Renesas Electronics Corporation (Japan)

- ON Semiconductor (U.S.)

- Continental AG (Germany)

- Robert Bosch GmbH (Germany)

- Qualcomm Technologies, Inc. (U.S.)

- Analog Devices, Inc. (U.S.)

- Micron Technology, Inc. (U.S.)

- Toshiba Corporation (Japan)

- ROHM Semiconductor (Japan)

- Nexperia (Netherlands)

- Diodes Incorporated (U.S.)

- GlobalFoundries (U.S.)

- Valens Semiconductor Ltd (Israel)

- Samsung Electronics Co., Ltd. (South Korea)

- Nvidia Corporation (U.S.)

- Intel Corporation (U.S.)

- Tata Electronics Ltd (India)

- Broadcom Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Infineon Technologies AG is a well-recognized global player in the marketplace of automotive semiconductors, especially in microcontrollers, power electronics, sensors, and functional safety‑critical chips for ADAS and electrification. The company has active partnerships and is expanding its portfolio of products, such as RISC‑V-based automotive MCUs and controllers for software‑defined vehicles.

- NXP Semiconductors N.V. is yet another prominent player whose product portfolio emphasizes secure, connected automotive systems, including radar solutions for ADAS, in‑vehicle networking, and battery management products. The firm’s automotive segment is a strategic focus with offerings that support connectivity, infotainment, and electrification.

- STMicroelectronics N.V. is based in Europe and is a central automotive chip supplier that maintains a very positions in MCUs, power devices, and MEMS sensors. The company’s strategic moves include acquiring part of NXP’s sensor business to bolster its sensor portfolio for automotive safety and control systems.

- Texas Instruments Inc. is a key provider of analog, power management, and embedded processor solutions, which are suitable for automotive applications such as radar, ADAS, and electrification. The firm is deliberately expanding semiconductor manufacturing capacity supported by CHIPS funding to strengthen automotive supply resilience.

- Renesas Electronics Corporation is a Japan-based supplier of automotive microcontrollers, SoCs, and power management ICs, which are highly essential attributes for the EV powertrains, BMS, and vehicle electronics. In 2024, the company began operations at a dedicated wafer fab with a prime goal to enhance capacity for automotive and industrial semiconductors.

Below is the list of some prominent players operating in the global automotive semiconductor market:

The automotive semiconductor market is an extremely competitive landscape that hosts established players as well as emerging new entrants. Industry leaders such as Infineon, NXP, STMicroelectronics, and Renesas leverage broad portfolios spanning power semiconductors, microcontrollers, and sensors, whereas pioneers based in the U.S., such as Texas Instruments, Qualcomm, and Analog Devices, are focused on analog, connectivity, and edge processing solutions. At the same time, continuous product innovations, tactical partnerships, and expansions in EV and autonomous platforms underscore competitive differentiation and future growth of the industry. In February 2026, STMicroelectronics completed the acquisition of NXP’s MEMS sensors business to strengthen its leadership in automotive safety and industrial sensor categories, thus denoting a positive market outlook.

Corporate Landscape of the Automotive Semiconductor Market:

Recent Developments

- In March 2026, NXP Semiconductors introduced its third-generation RFCMOS radar transceiver, which is the TEF8388, featuring 8 transmit and 8 receive channels to enable high-resolution imaging radar for Level 2+ to Level 4 autonomous driving.

- In June 2025, Continental’s Automotive group announced the launch of an advanced electronics & semiconductor solutions organization to design and verify automotive semiconductors, with GlobalFoundries as its exclusive manufacturing partner.

- Report ID: 4158

- Published Date: Apr 06, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Automotive Semiconductor Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.