Semiconductor Memory Market Outlook:

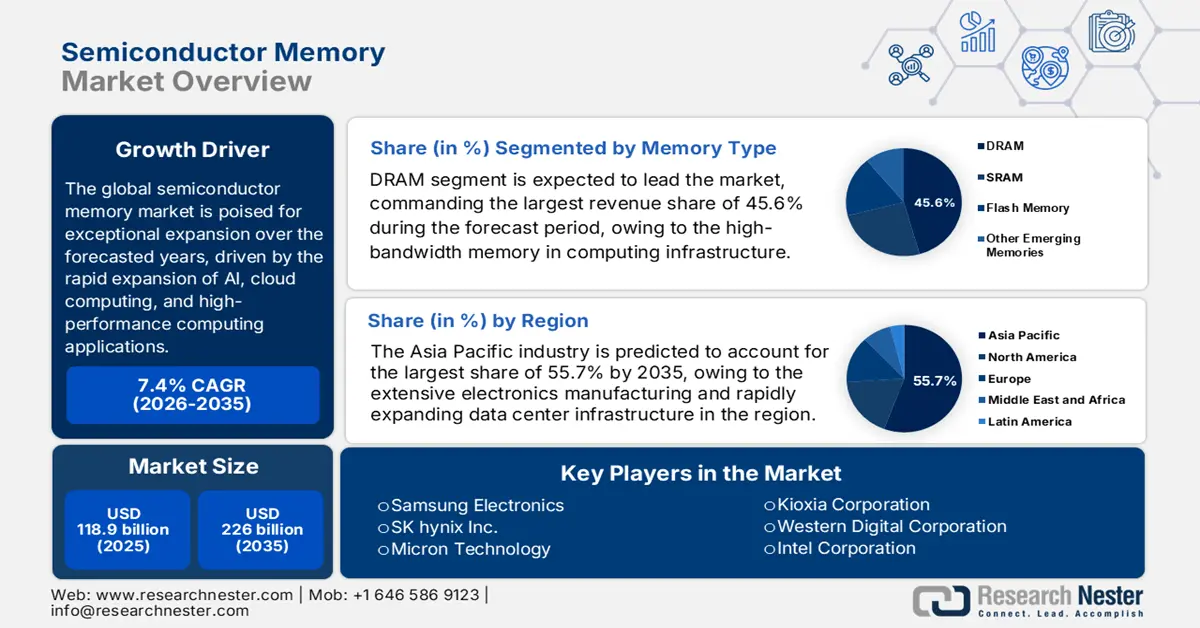

Semiconductor Memory Market size was valued at USD 118.9 billion in 2025 and is projected to reach USD 226 billion by the end of 2035, rising at a CAGR of 7.4% during the forecast period, i.e., 2026-2035. The industry size of the semiconductor memory market is estimated to reach USD 127.7 billion by the end of 2026.

The global semiconductor memory market is poised for exceptional expansion over the forecasted years, driven by the rapid emergence of AI, cloud computing, and high-performance computing applications. In the memory chip supply chains, they are highly specialized and geographically segmented, where the raw‑material sourcing, wafer fabrication, assembly, and testing often occur across different countries. The analysis by OECD in June 2025 found that critical inputs to semiconductor manufacturing, which include silicon, borates, rare gases, and other wafer‑fabrication materials, are concentrated among a limited number of exporting economies. It also stated that in 2022, global exports of raw materials associated with semiconductor inputs rebounded past USD 18 billion after prior declines, with the U.S., Germany, and China among the largest exporters of silicon-based inputs.

Global Semiconductor Memory Sales Statistics

|

Metric |

Value |

Notes |

|

Global Semiconductor Sales (2022) |

USD 602 billion |

Total market for all semiconductor types. |

|

Memory Chip Share of Total Sales (2021) |

28% (USD 154 billion) |

Memory is the second-largest segment after Logic (42%). |

|

Primary Memory Types |

DRAM & NAND Flash |

These two categories account for the majority of memory chip sales. |

Source: Congress.gov

Furthermore, on the pricing aspect, in July 2025, the U.S. Bureau of Labor Statistics reported that import prices for semiconductor manufacturing reduced by 1.4% from December 2021 to December 2024, which then rose by 2.4% in 2022, followed by a 3.8% drop in 2023 and stability in 2024. It also mentioned export prices, which decreased 3.6% over the same period, reflecting fluctuations in global demand and raw material costs. In addition, the producer price index for semiconductor manufacturing grew by 6.1% from 2021 to 2024, which reflects gradual cost increases in domestic production. Meanwhile, in 2024, the total U.S. semiconductor export value surpassed USD 70.1 billion, with Texas and Oregon accounting for around half of exports, highlighting key regional production hubs. Hence, the stable prices and rising producer prices indicate the presence of supply-chain resilience and controlled production costs, supporting consistent growth in the semiconductor memory market.

Key Semiconductor Memory Market Insights Summary:

Regional Highlights:

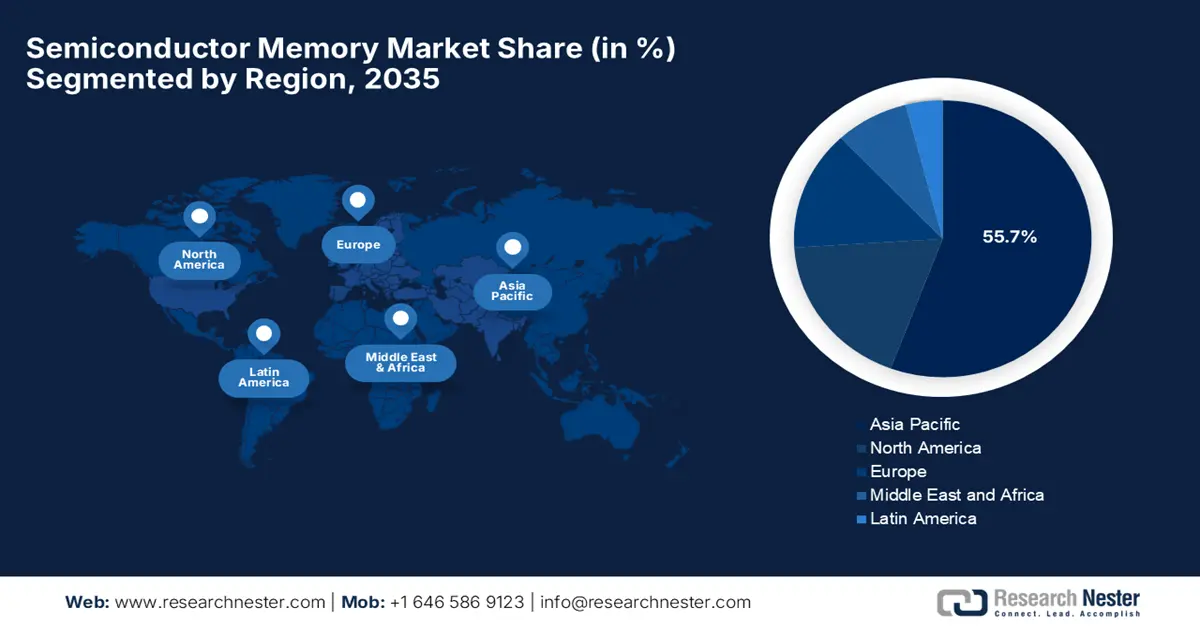

- The Asia Pacific region is anticipated to command 55.7% of the semiconductor memory market by 2035, propelled by extensive electronics manufacturing and the rapid expansion of data-center infrastructure.

- North America is set to strengthen its position in the semiconductor memory landscape by 2035, underpinned by a robust cloud ecosystem and accelerating adoption of AI and machine-learning applications.

Segment Insights:

- The DRAM segment is projected to capture a 45.6% share by 2035 in the semiconductor memory market, driven by the escalating requirement for high-speed, high-bandwidth memory in computing infrastructure.

- The data centers & servers segment is anticipated to secure a lucrative revenue share by 2035, owing to the rapid global expansion of hyperscale cloud facilities and the architectural transition toward AI-optimized servers.

Key Growth Trends:

- AI and high-performance computing

- Expansion of cloud and data centers

Major Challenges:

- Supply-demand cyclicality

- Escalating manufacturing complexity

Key Players:Samsung Electronics (South Korea), SK hynix Inc. (South Korea), Micron Technology (U.S.), Kioxia Corporation (Japan), Western Digital Corporation (U.S.), Intel Corporation (U.S.), Nanya Technology Corporation (Taiwan), Winbond Electronics Corporation (Taiwan), Powerchip Semiconductor Manufacturing Corp. (Taiwan), Infineon Technologies AG (Germany), Cypress Semiconductor (U.S./Germany), STMicroelectronics (Switzerland/France), Macronix International Co., Ltd. (Taiwan), SMIC - Memory Manufacturing Partnerships (China), FMC - Ferroelectric Memory Company (Germany).

Global Semiconductor Memory Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 118.9 billion

- 2026 Market Size: USD 127.7 billion

- Projected Market Size: USD 226 billion by 2035

- Growth Forecasts: 7.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (55.7% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, South Korea, Japan, Germany

- Emerging Countries: India, Vietnam, Taiwan, Singapore, Mexico

Last updated on : 10 December, 2025

Semiconductor Memory Market - Growth Drivers and Challenges

Growth Drivers

- AI and high-performance computing: The rapid rise of artificial intelligence, machine learning, and large-scale computing workloads is driving consistent demand in the semiconductor memory market. AI data centers and compute-intensive applications are necessitating faster and more energy-efficient memory to handle massive data transfers. In May 2024, Micron Technology announced it had become the first company to validate and ship 128GB DDR5 32Gb server DRAM, which is especially designed for memory-intensive AI, machine learning, and high-performance computing workloads. The company also underscored that the modules offer up to 45% higher bit density, 22% improved energy efficiency, and 16% lower latency, supporting major server platforms including AMD, Intel, HPE, and Supermicro, thereby enabling AI data centers to achieve higher bandwidth, reinforcing memory as a critical enabler of next-generation computing performance.

- Expansion of cloud and data centers: The worldwide growth in cloud services and data-center infrastructure is increasing the adoption of memory modules and storage solutions. Also, the existence of enterprises that are moving workloads to hyperscale and cloud environments relies heavily on DRAM and NAND to ensure system reliability, creating sustained demand in the semiconductor memory market across both established and emerging regions. In December 2025, Marvell Technology, Inc. announced that it had acquired Celestial AI for approximately USD 3.25 billion, with a prime focus on accelerating optical interconnect solutions for next-generation AI and cloud data centers. Hence, this acquisition is expected to generate significant revenue and position the firm as the predominant leader in scale-up connectivity for AI infrastructure, addressing growing demands for high-performance, energy-efficient memory and compute systems.

- Enterprise and edge storage demand: The increasing need for high-capacity storage in enterprise applications, edge computing devices, and industrial systems is driving stronger adoption of NAND flash and DRAM. Organizations deploying AI, IoT, and edge analytics require memory solutions that support rapid data access, boosting growth in the semiconductor memory market. In January 2025, SK hynix at CES 2025 showcased its vision as a full-stack AI memory provider by introducing its advanced AI memory technologies, which include 16-layer HBM3E, high-capacity SSDs such as the 122TB D5-P5336, and on-device AI products for edge computing. The company highlighted innovations in processing-in-memory and CXL Memory Modules, which are designed to enhance performance and energy efficiency for next-generation AI data centers, hence providing comprehensive memory solutions to enterprise, cloud, and edge computing customers.

Major Semiconductor Industry Developments and Market Opportunities in Memory Technologies

|

Company |

Key Focus |

Year |

Market Opportunity |

|

Merck |

Semiconductor materials, Thin Films |

2025 |

High demand for AI chips; thin films critical for next-gen memory & logic |

|

NXP & TSMC |

Automotive 16 nm FinFET Embedded MRAM |

2023 |

Automotive MRAM adoption: faster, high-endurance memory solutions |

Source: Company Official Press Releases

Challenges

- Supply-demand cyclicality: This is the major drawback negatively impacting the expansion of the semiconductor memory market. The fluctuations in supply and demand, periods of overcapacity lead to price drops, whereas the shortages cause rapid price spikes, creating instability for both manufacturers and customers. Besides, the existence of this volatility is complicating long-term planning, capital investments, and inventory management across the entire value chain. Therefore, manufacturers need to predict demand for servers, AI systems, mobile devices, PCs, and automotive electronics segments, which are fluctuating independently. Furthermore, high fixed costs and multi-year fabrication cycles amplify financial risk during downturns, making expansion extremely difficult.

- Escalating manufacturing complexity: The semiconductor memory market faces severe difficulties in terms of manufacturing complexity and costs. This is due to the manufacturer's push for high density, faster speed, and lower power consumption. Involvement of technologies such as EUV lithography, 3D-NAND stacking with hundreds of layers, and advanced HBM packaging necessitates substantial R&D investment and ultra-precise manufacturing environments, making it challenging for small and medium-scale manufacturers. As nodes shrink and stack heights increase, defect rates and yield challenges multiply, adding to burgeoning costs. Furthermore, these escalating technological requirements create massive entry barriers, forcing smaller players out and consolidating the market expansion in the upcoming years.

Semiconductor Memory Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.4% |

|

Base Year Market Size (2025) |

USD 118.9 billion |

|

Forecast Year Market Size (2035) |

USD 226 billion |

|

Regional Scope |

|

Semiconductor Memory Market Segmentation:

Memory Type Segment Analysis

The DRAM segment is expected to lead the entire semiconductor memory market, commanding the largest revenue share of 45.6% during the forecast period. This sustained dominance of DRAM is primarily fueled by the insatiable demand for high-speed, high-bandwidth memory in computing infrastructure. In April 2025, Neumonda and Ferroelectric Memory Company announced that they had entered into a partnership to commercialize FMC’s non-volatile DRAM+, combining ferroelectric HfO₂ technology with traditional DRAM to create low-power, high-performance memory for AI, automotive, industrial, and consumer applications. In this partnership, Neumonda will support FMC with advanced memory design consulting and its Rhino, Octopus, and Raptor testing platforms to accelerate product development and ensure high-quality yields, hence reviving semiconductor DRAM design.

Application Segment Analysis

In the semiconductor memory market, data centers & servers’ subtype is anticipated to gain a lucrative revenue share by the end of 2035. This serves as the primary engine of memory demand, owing to the global expansion of hyperscale cloud facilities and the architectural shift towards AI-optimized servers. Simultaneously, the growth of data generation, cloud services, and generative AI requires servers with parallel processing capabilities, which in turn require huge quantities of DRAM and high-performance NAND flash for caching and storage. In October 2025, Qualcomm announced that it had launched the AI200 and AI250 solutions, delivering rack-scale AI inference performance with high memory capacity and energy efficiency for data centers. Furthermore, the AI250 possesses a near-memory computing architecture, providing over 10× higher effective memory bandwidth, whereas both support integration with leading AI frameworks.

End use Segment Analysis

By the conclusion of the discussed timeframe consumer electronics segment is likely to attain a significant revenue share in the semiconductor memory market. The growth in the segment is highly subject to the sheer volume of devices and their increasing memory content per unit. The core drivers are identified as the continuous performance escalation in smartphones, the single largest product category for advanced photography, gaming, and on-device AI features, along with the persistent need for memory in PCs, tablets, and wearables. In addition, the rise of smart home devices and IoT-enabled consumer products is further fueling demand for high-capacity, energy-efficient memory solutions. Advances in terms of AR/VR headsets and next-generation gaming consoles also contribute to higher memory requirements per device, hence contributing to overall market growth.

Our in-depth analysis of the semiconductor memory market includes the following segments:

|

Segment |

Subsegments |

|

Memory Type |

|

|

Application |

|

|

End user Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Semiconductor Memory Market - Regional Analysis

APAC Market Insights

The Asia Pacific is anticipated to lead the semiconductor memory market, capturing 55.7% of the total share by the end of 2035. This pace of progress in the region is highly propelled by extensive electronics manufacturing and rapidly expanding data center infrastructure. Countries in the region are increasingly integrating memory-intensive AI workloads, gaming devices, and industrial automation solutions. In September 2025, Kioxia Corporation and Sandisk Corporation together announced the commencement of operations at their new Fab2 semiconductor fabrication facility at the Kitakami Plant, Japan, which is designed to produce eighth-generation, 218-layer 3D flash memory using CBA technology. Besides, the facility incorporates AI-driven production efficiencies and earthquake-resistant architecture, with staged capacity ramp-up aligned to market demand, hence positively impacting market growth.

China is rapidly growing in the semiconductor memory market owing to the strong push toward self-reliance in semiconductor manufacturing and the presence of major state-backed initiatives to produce high-capacity DRAM and NAND on a domestic basis. Also, the booming smartphone, IoT, and AI-driven industries create substantial demand for memory with high density and performance. In addition, domestic firms are also exploring next-generation memory technologies such as 3D NAND and non-volatile DRAM to compete in the global landscape. Simultaneously, the country’s market also benefits from the government’s supportive policies, subsidies, and investment funds, which are accelerating R&D and production capabilities, fostering a robust ecosystem for semiconductor memory innovation. Therefore, the presence of this coordinated effort positions the country as a key contender in both consumer and enterprise memory sectors.

India is exponentially growing in the regional semiconductor memory market, efficiently backed by rapid digitization, government-led electronics manufacturing programs, and the expansion of cloud and AI-driven enterprises. Besides, collaborative efforts between educational institutions, startups, and multinational companies also help drive memory innovation in the country. In April 2025, the Ministry of Electronics & IT reported that the Government of India is proactively advancing its semiconductor memory ecosystem through the Semicon India Program, which offers fiscal support, incentives for chip design, and funding for fabrication and ATMP/OSAT facilities. It also mentioned that the strategic MoUs with the U.S., EU, Japan, and Singapore, along with talent development initiatives such as C2S and SMART Labs, aim to build a skilled workforce in VLSI and semiconductor design, hence contributing to market expansion.

North America Market Insights

North America is continuously growing in the international semiconductor memory market, positively impacted by a strong ecosystem of cloud computing providers, data centers, and technology startups. On the other hand, the increasing adoption of AI and machine learning applications across various industries is fueling the need for advanced DRAM and NAND solutions. In December 2025, Veeco announced that a leading global semiconductor memory manufacturer had selected its laser spike annealing system for advanced DRAM evaluation, which marks another milestone in the adoption of high-precision thermal processing technologies. The company also stated that its LSA platform will support next-generation DRAM nodes by enabling ultra-uniform annealing and improved device performance, hence strengthening the firm’s position in the memory manufacturing ecosystem as chipmakers accelerate development of higher-density DRAM technologies.

The U.S. is undergoing significant transformations in the regional semiconductor memory market, owing to the presence of government-led programs such as the Department of Energy’s exascale computing initiatives, and investments in AI infrastructure are creating heightened demand for high-performance memory. The presence of major chip manufacturers and design houses is efficiently strengthening domestic innovation and memory production capabilities. In June 2025, Micron announced a major expansion in the country plan totaling about USD 200 billion to boost domestic DRAM manufacturing and R&D, which includes a second leading-edge fab in Idaho, modernization of its Virginia facility, and new advanced HBM packaging capabilities. The company also stated that this is supported by CHIPS Act incentives; these investments aim to meet accelerating AI-driven memory demand while strengthening U.S. supply-chain resilience.

Canada has gained strong exposure in the semiconductor memory market, primarily shaped by its growing AI research hubs, technology incubators, and partnerships between universities and industry. The country’s market also benefits from sustainability initiatives, which push for energy-efficient memory solutions in both consumer and enterprise applications. In November 2025, the government of Canada announced a major investment of up to USD 210 million to expand semiconductor packaging and commercialization capabilities in partnership with IBM Canada and C2MI, strengthening domestic chip production. Besides, the initiative aims to enhance advanced packaging, bolster supply-chain resilience, and accelerate the commercialization of next-generation semiconductor technologies, hence propelling continued growth in the country’s market.

Europe Market Insights

Europe has acquired the most prominent position in the semiconductor memory market, supported by strong industrial and automotive sectors, with an emphasis on energy-efficient and high-reliability memory solutions. Governments across the region are funding initiatives to strengthen domestic semiconductor production and reduce dependence on imports. In November 2025, the European Commission announced that it had approved a €450 million (≈USD 490 million) Czech state-aid package to support Onsemi’s development of a first-of-its-kind silicon carbide (SiC) semiconductor manufacturing plant in Rožnov pod Radhoštěm. It also underscored that the €1.64 billion (≈USD 1.78 billion) facility will span the full production chain from SiC crystal growth to finished power devices and aims to strengthen Europe’s semiconductor autonomy under the EU Chips Act.

Germany has captured a dominant position in the regional semiconductor memory market, positively influenced by its automotive and industrial automation sectors, where high-performance, low-latency memory is critical. Simultaneously, the initiatives in the country aim to enhance chip design and fabrication capabilities by fostering a competitive memory ecosystem. In November 2025, The Ferroelectric Memory Company announced that it raised €100 million (≈USD 109 million) in a funding round, which was co-led by DeepTech & Climate Fonds and HV Capital, to advance its next-generation memory technology. In addition, FMC’s DRAM+ and 3D CACHE+ architectures leverage hafnium oxide to deliver faster, more energy-efficient memory for AI data centers and edge computing, addressing key performance and sustainability challenges in modern computing. Furthermore, this investment supports FMC’s mission to commercialize a regional, globally competitive memory solution and scale production.

The UK’s semiconductor memory market is primarily fueled by cloud services, AI startups, and growing smart infrastructure projects. The country’s market also benefits from investments in high-speed memory for data centers and enterprise computing are increasing to support AI, fintech, and healthcare applications. In May 2024, the country’s government announced that the UK Semiconductor Institute is an independent body that is designed to unify government, academia, and industry to advance the UK’s semiconductor sector, supported by a £1 billion (USD 1.32 billion) government strategy. It aims to provide infrastructure, foster R&D, develop skills, and attract international investment, focusing on UK strengths in compound semiconductors, design, and innovation. Hence, it drives market growth by fostering innovation, developing talent, and attracting investment to strengthen the country’s semiconductor ecosystem.

Key Semiconductor Memory Market Players:

- Samsung Electronics (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- SK hynix Inc. (South Korea)

- Micron Technology (U.S.)

- Kioxia Corporation (Japan)

- Western Digital Corporation (U.S.)

- Intel Corporation (U.S.)

- Nanya Technology Corporation (Taiwan)

- Winbond Electronics Corporation (Taiwan)

- Powerchip Semiconductor Manufacturing Corp. (Taiwan)

- Infineon Technologies AG (Germany)

- Cypress Semiconductor (U.S./Germany)

- STMicroelectronics (Switzerland/France)

- Macronix International Co., Ltd. (Taiwan)

- SMIC - Memory Manufacturing Partnerships (China)

- FMC - Ferroelectric Memory Company (Germany)

- Samsung Electronics is recognized as the global leader in the semiconductor memory sector, which is leveraging both DRAM and NAND flash segments. The dominance of the firm is highly propelled by the massive R&D investments, manufacturing expansion, and early commercialization of technologies such as V-NAND, LPDDR, and HBM. Furthermore, Samsung continues to build multi-billion-dollar fabs in Korea and the U.S. to secure long-term supply resilience.

- SK hynix Inc. has strengthened its position as the world’s most prominent memory producer, highly influenced by leadership in high-performance DRAM and advances in HBM technology. The company is also strongly leveraging extensive partnerships across cloud providers and AI chipmakers, due to which it is positioned as a major full-stack AI memory supplier. In addition, continued investment in advanced packaging, energy-efficient memory, and global manufacturing scale is readily fueling its competitive momentum.

- Micron Technology is the U.S.-based memory manufacturer, which is best known for innovations in DDR5, LPDDR5X, HBM, and 3D NAND. The company is efficiently expanding its manufacturing footprint, including advanced HBM packaging facilities in Singapore and major U.S. fab projects. Micron has a strong IP portfolio, long-term technology roadmap, and deep relationships with hyperscalers, which are making it a critical player in securing domestic supply resilience.

- Kioxia Corporation was formerly known as Toshiba Memory and is one of the world’s major NAND flash innovators. The company has sharpened its focus on high-density storage solutions for mobile, automotive, enterprise SSDs, and data-center applications. Kioxia is maintaining a strong technology roadmap and plays a vital role in the storage-memory segment, particularly as demand surges for hyperscale cloud storage and AI-heavy workloads, which are continuously necessitating large-capacity NAND.

- Western Digital Corporation is one of the central global producers of NAND flash memory and SSDs, operating one of the largest NAND joint ventures with Kioxia. The company is well known for high-quality enterprise and consumer storage solutions, and it supplies SSDs, embedded flash, and custom storage modules to major OEMs and hyperscalers. Furthermore, the company continues to invest in advanced 3D NAND, energy-efficient controllers, and edge-to-cloud storage architectures.

Below is the list of some prominent players operating in the global market:

The semiconductor memory market is considered to be highly competitive, which is dominated by the pioneers, primarily Samsung, SK hynix, and Micron. These key players are controlling most of the global DRAM and NAND output. The multibillion-dollar fabs, geographic expansion, supply-chain diversification, and joint ventures are a few strategies undertaken by these leading organizations to secure their market positions. For instance, in January 2025, Micron Technology announced that it had broken ground on a USD 7 billion HBM advanced packaging facility in Singapore to address growing AI data center demand. The company also mentions that this facility will expand advanced memory capacity and support NAND manufacturing. Furthermore, designed with sustainability and automation in mind, the investment positions the firm to provide high-performance, energy-efficient memory solutions.

Corporate Landscape of the Semiconductor Memory Market:

Recent Developments

- In November 2025, FMC announced that it had raised €100 million (~USD 108 million), which includes €77 million (~USD 83 million) in Series C equity and *€23 million (~USD 25 million) in public funding to accelerate the commercialization of its DRAM+ and 3D-CACHE+ memory chips. The company says its technology can deliver over 100% higher system efficiency and processing speed.

- In September 2025, SK hynix notified that it had completed development of the world’s first-ever HBM4 and prepared it for mass production, marking a major step in next-generation AI memory. The new chip delivers 2× the bandwidth and 40% better power efficiency than the previous generation, enabled by 2,048 I/O and operation speeds above 10 Gbps.

- Report ID: 8301

- Published Date: Dec 10, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.