Pumped Hydro Storage Market Outlook:

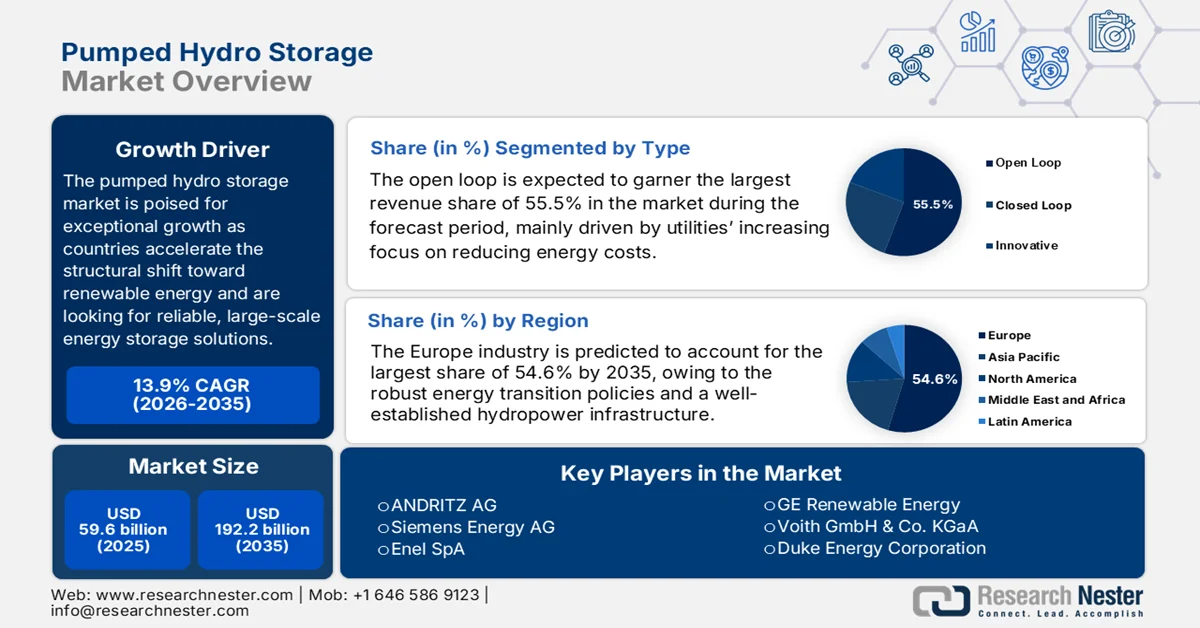

Pumped Hydro Storage Market size was valued at USD 59.6 billion in 2025 and is projected to reach USD 192.2 billion by the end of 2035, rising at a CAGR of 13.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of pumped hydro storage is assessed at USD 67.8 billion.

The pumped hydro storage market is poised for exceptional growth as countries accelerate the structural shift toward renewable energy and demand for reliable, large-scale energy storage solutions. Increasing integration of variable renewable sources such as wind and solar is efficiently driving demand for grid stabilization and long-duration storage, where pumped hydro is identified as a proven and efficient technology. In this context, the U.S. Department of Energy (DOE) stated that in 2023, hydropower accounted for about 27 % of U.S. utility-scale renewable electricity, playing a critical role in grid reliability. In addition, it is developed under Executive Order 14017, which recommends leveraging the federally owned fleet that is nearly 50% of domestic capacity. It also aims to create stable demand, strengthen domestic manufacturing visibility, and coordinate cross-industry material demand, hence creating an optimistic market opportunity.

Furthermore, the continuously upgrading government policies, modernization of aging grid infrastructure, and surging investments in clean energy projects are strengthening the pumped hydro storage market. Based on the government data from the U.S. DOE in October 2022, its Water Power Technologies Office issued a total of USD 10 million funding opportunity (DE-FOA-0002802) under the Infrastructure Investment and Jobs Act, with a prime focus to support development studies for new pumped storage hydropower facilities. This particular initiative is designed to facilitate licensing, site design, interconnection, and market analysis activities that improve projects toward construction and commissioning, particularly those enabling long-duration storage on tribal lands. The pumped storage accounted for 93% of U.S. utility-scale energy storage as of 2021, and this federal support efficiently strengthens the market’s growth potential. Also, there are many projects in the pipeline in pumped storage hydropower reflecting the constant efforts to expand energy storage infrastructure.

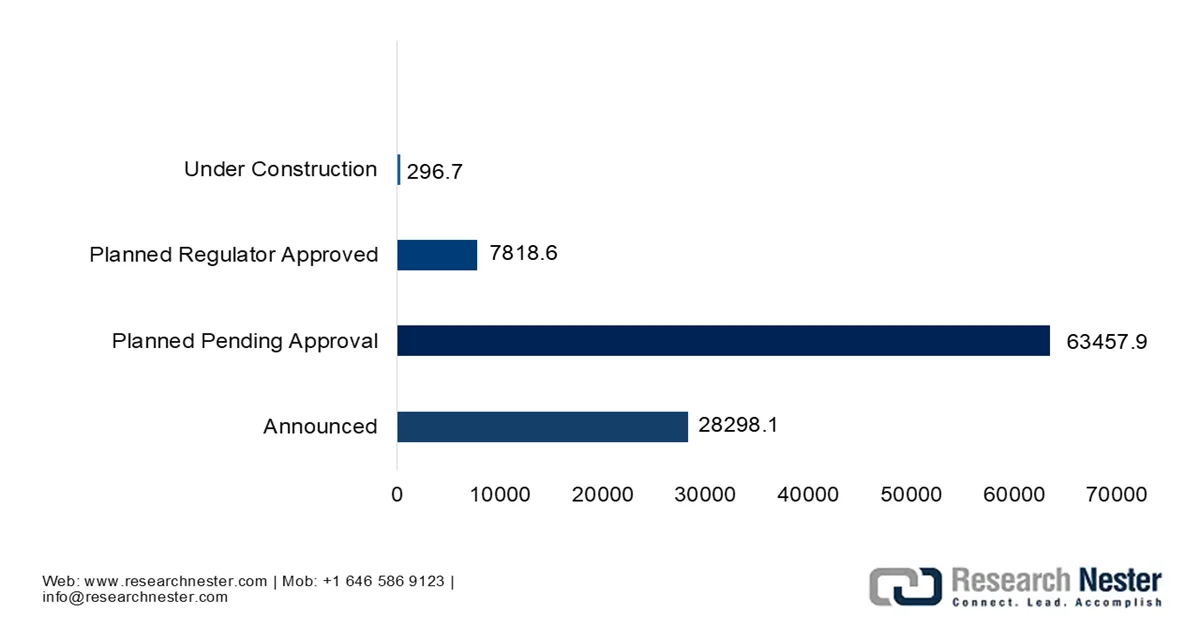

North and Central America Pumped Storage Hydropower Pipeline Capacity by Project Status (MW) 2024

Source: Hydropower.org

Key Pumped Hydro Storage Market Insights Summary:

Regional Highlights:

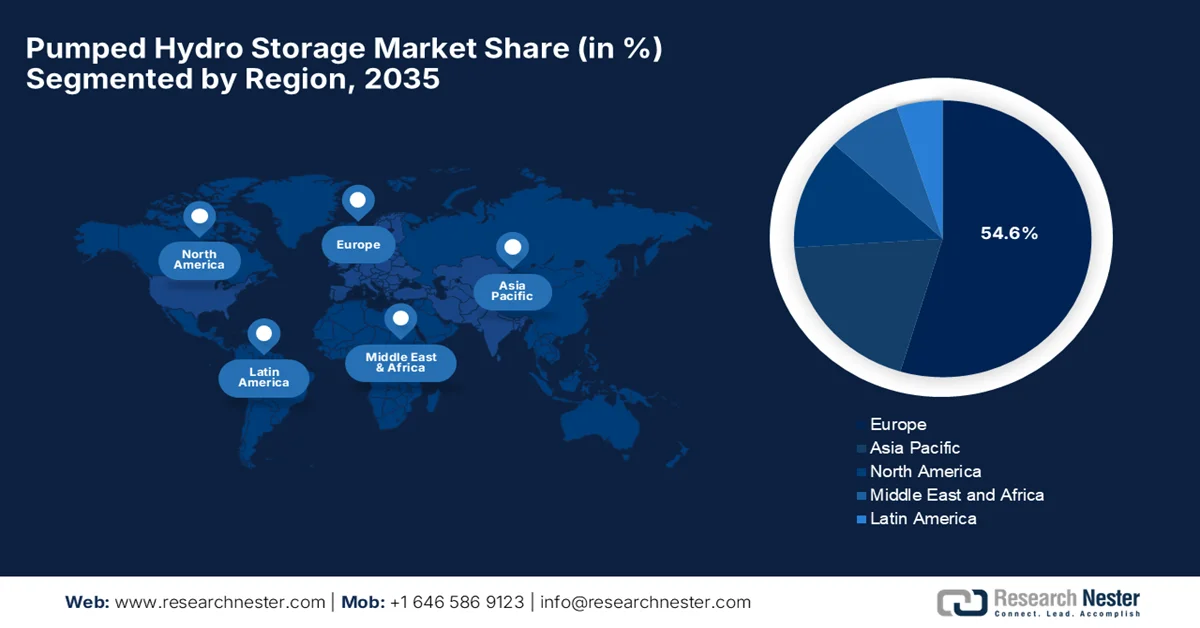

- In the pumped hydro storage market, Europe is projected to dominate with a 54.6% revenue share by 2035, attributed to robust energy transition policies, established hydropower infrastructure, and strategic initiatives by key market players.

- Asia Pacific is expected to witness the fastest growth during 2026–2035, propelled by escalating energy demand and ambitious renewable energy targets requiring long-duration storage solutions.

Segment Insights:

- In the pumped hydro storage market, the Open Loop segment is projected to secure a 55.5% revenue share by 2035, driven by utilities’ increasing focus on reducing energy costs and seamless integration with existing power infrastructure.

- The above 1,000 MW capacity segment is anticipated to capture a significant revenue share by 2035, bolstered by its suitability for national grid applications requiring large-scale energy storage and discharge capabilities.

Key Growth Trends:

- Technological advancements

- Increasing electricity demand

Major Challenges:

- Long development and construction time

- Limited suitable geographical sites

Key Players: ANDRITZ AG (Austria), Siemens Energy AG (Germany), Enel SpA (Italy), GE Vernova / GE Renewable Energy (U.S.), Voith GmbH & Co. KGaA (Germany), Duke Energy Corporation (U.S.), NextEra Energy, Inc. (U.S.), Torrent Power (India), Mitsubishi Heavy Industries (Japan), Toshiba Energy Systems & Solutions Corporation (Japan), Statkraft AS (Norway), China Three Gorges Corporation (China), Dongfang Electric Corporation (China), Harbin Electric Machinery Company (China), Edison SpA (Italy), Hydro-related groups (Europe), Snowy Hydro Limited (Australia), Bharat Heavy Electricals Limited (India)

Global Pumped Hydro Storage Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 59.6 billion

- 2026 Market Size: USD 67.8 billion

- Projected Market Size: USD 192.2 billion by 2035

- Growth Forecasts: 13.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Europe (54.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: China, United States, Japan, Germany, Australia

- Emerging Countries: India, Brazil, Vietnam, Indonesia, South Korea

Last updated on : 17 February, 2026

Pumped Hydro Storage Market - Growth Drivers and Challenges

Growth Drivers

- Technological advancements: The improvements in terms of turbine efficiency, variable-speed pump-turbines, digital controls, and monitoring systems are readily enhancing the performance of hydro storage. Also, the integration with smart grid technologies and hybrid configurations, such as co-located with solar or wind, improves operational flexibility, contributing to the pumped hydro storage market growth. In March 2024, the U.S. DOE’s Water Power Technologies Office, which is led by Argonne National Laboratory and NREL, identified that there are more than 1,800 potential sites in Alaska for closed-loop pumped storage hydropower to support clean energy integration. The study showed that PSH could provide long-duration storage, helping the Railbelt system and remote microgrid communities reduce reliance on diesel and integrate more wind and solar power. Hence, such instances denote the closed-loop systems as the foundational factor driving the pumped hydro storage market growth.

- Increasing electricity demand: The extensive population growth, economic development, and electrification of transport and industry are the main factors driving electricity demand, in turn fueling the need for proper storage solutions. In this context, the pumped storage helps to manage peak loads and maintain resilience against frequent outages. According to the official statistics published by the IEA Organization in January 2026, total net electricity generation in the OECD reached 883.8 TWh in October 2025, which is up 2.5% year-on-year. It also stated that renewable generation grew by 4.7% (+14.8 TWh), wherein solar and wind have become substantial. Therefore, from a strategic perspective, these data state that there is a huge demand for storage solutions, such as in the pumped hydro storage market, to balance intermittent renewable output and maintain grid reliability.

- Investment in storage programs: Public and private investment in modernizing energy systems and expanding storage capacities is booming, mainly influenced by the long-term value that pumped storage provides for grid flexibility and reliability. Based on the government data from the Ministry of Power, which was published in June 2025, India’s pumped storage program has made notable progress. It stated that ten projects with that have a combined 6.2 GW are already commissioned, and eight more totaling 8.5 GW are under construction. In addition, five projects of 5.8 GW have received concurrence, and 46 projects with a massive 64.8 GW capacity are under survey and investigation, reflecting strong government support and clear momentum in expanding the pumped hydro storage market capacity.

North and Central America Hydropower Projects: Capacities, Status, and Development Updates

|

Country/Region |

Project/Initiative |

Capacity (MW) |

Status |

Key Notes |

|

Canada (BC) |

Site C Project |

1,100 |

Full operation by Autumn 2025 |

Adds 8% to provincial capacity |

|

Canada (Québec & NL) |

Cooperative hydropower agreement |

- |

Announced 2024-25 |

Joint investment in future projects |

|

The U.S. (Colorado) |

Taylor River Hydro Project |

0.5 (500 kW) |

Commissioned 2025 |

Expected 3.8 GWh annually |

|

The U.S. (National) |

Bipartisan Infrastructure Law (BIL) funding |

- |

Ongoing since 2023 |

Supports refurbishment, small community projects, R&D |

|

Panama |

Changuinola II Project |

228 |

Completion by 2029 |

Part of the 2020-2034 national expansion plan |

|

Costa Rica |

La Garita Hydroelectric Plant modernization |

97 |

Completed early 2025 |

Upgraded facility now in full operation |

|

Dominican Republic |

Multiple hydropower projects |

- |

Ongoing |

Target: 25% renewable generation by 2025 |

|

The U.S. (Licensing) |

Non-federal hydropower fleet relicensing |

15,700 |

Expiring 2020-2035 |

Represents 40% of fleet capacity |

Source: Hydro Power.Org

Challenges

- Long development and construction time: The entire process of planning, approvals, and construction takes years for a PHS project to finish. The aspects of lengthy feasibility studies, environmental impact assessments, land acquisition processes, and designs delay execution, causing hindrance to the pumped hydro storage market expansion. Also, the construction itself is complex, which involves large-scale excavation, tunneling, and hydro-mechanical installation. Therefore, such extended timelines create uncertainty regarding future electricity market prices, regulatory frameworks, and technology competition. During the construction period, any changes in terms of policy or demand patterns can affect project viability. Furthermore, the battery storage systems can be deployed in months, which reduces pumped hydro’s competitiveness in fast-evolving renewable energy sectors.

- Limited suitable geographical sites: Pumped hydro storage requires specific topographical conditions, i.e., two reservoirs at different elevations, and should have a proper height difference and water availability. Such geographic requirements significantly limit viable project locations for the pumped hydro storage market. The flat terrains or water-scarce regions are unsuitable for traditional PHS systems. In addition, proximity to transmission infrastructure and demand centers is important to minimize the grid connection costs. As the best sites in many developed countries are already utilized, new projects face geographical constraints. Meanwhile, even when technically feasible sites are identified, social, environmental, or political barriers may restrict development, negatively impacting pumped hydro storage market growth.

Pumped Hydro Storage Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

13.9% |

|

Base Year Market Size (2025) |

USD 59.6 billion |

|

Forecast Year Market Size (2035) |

USD 192.2 billion |

|

Regional Scope |

|

Pumped Hydro Storage Market Segmentation:

Type Segment Analysis

The open loop in the type segment is expected to garner the largest revenue share of 55.5% in the pumped hydro storage market during the forecast period. The growth of the subtype is mainly driven by utilities’ increasing focus on reducing energy costs. Their strong market position is also supported by easy integration with existing power infrastructure and conventional power systems. In March 2025, HCC and Tata Projects Limited together reported that they achieved an approximately USD 300 million contract from Tata Power to construct the Bhivpuri off-stream open-loop pumped storage project (1,000 MW) in Karjat, Maharashtra. Therefore, such developments underscore that there is a continued adoption of open-loop pumped hydro systems to provide flexible, cost-effective energy storage and integrate with the existing power infrastructure.

Capacity Segment Analysis

The above 1,000 MW capacity is anticipated to lead the pumped hydro storage market in the storage capacity segment by capturing a significant revenue share by 2035. Systems of this scale are highly suitable for national grid applications due to their substantial energy storage and discharge capabilities. Meanwhile, in terms of densely populated or industrial regions, these large facilities help balance the electricity supply during peak and off-peak periods, ensuring that there is continuous power availability. Their size allows for long-term cost savings and operational efficiency, attracting more investments in this sector. In addition, countries that have advanced energy infrastructure have already deployed several of these high-capacity systems, which are crucial for integrating large-scale renewable energy and supporting energy-intensive industries.

Application Segment Analysis

The grid balancing, which is a part of the application segment, is likely to grow at a considerable rate in the pumped hydro storage market. The growth is mainly subject to global power systems integrating more intermittent renewables, which makes a reliable electric supply complex. Pumped hydro storage provides a very quick-response mechanism to absorb excess generation during periods of low demand and release stored energy during peak load, which helps to prevent any type of frequency fluctuations and voltage instability. In addition, by supporting short-term load balancing, these systems enhance overall grid resilience by providing spinning reserves and emergency backup power. Therefore, most of the governments and utilities are making investments in pumped hydro for grid balancing, identifying its efficient role in enabling a flexible and renewable-friendly power infrastructure.

Our in-depth analysis of the pumped hydro storage market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Capacity |

|

|

Application |

|

|

End user |

|

|

Technology Architecture |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Pumped Hydro Storage Market - Regional Analysis

Europe Market Insights

Europe pumped hydro storage market is anticipated to be the dominant region, capturing the largest share of 54.6% by 2035. The region’s leadership is mainly attributable to robust energy transition policies, key market players & their tactical strategies, and a well-established hydropower infrastructure. This particular region has spent years developing large-scale hydro projects, which also include pumped storage, resulting in substantial installed capacity. In February 2025, Fortum notified that it had launched a two-year feasibility study to assess the potential for new pumped hydro storage plants in three areas of Sweden by evaluating commercial, technological, environmental, and regulatory conditions. The study aims to determine whether new plants can meet economic and environmental criteria by efficiently supporting the Nordic energy transition, hence making it suitable for standard market growth.

The nation’s broader energy transition plan, which is providing flexibility and back-up capacity complementary to a growing share of wind and solar are certain driver boosting the pumped hydro storage market in Germany. Supportive governing bodies, coupled with investments in modernizing existing facilities, are also propelling the continued growth of the country’s market. In this regard, Bavaria’s Ministry of Economic Affairs and Energy in September 2025 reported an official planning approval for the Riedl pumped-storage power plant in Passau, which is developed by VERBUND AG, aiming for completion by 2031-32. It also underscores that pumped storage is as important as expanding photovoltaics and wind power, allowing surplus electricity to be stored and fed back into the grid during high demand. The project, which is being undertaken with an investment of more than 400 million euros (approximately USD 436 million), will provide 300 MW capacity, 3.5 million kWh storage, and strengthen the regional energy supply and economy.

Strategic energy planning that balances historical reliance on nuclear power with increasing deployment of renewables is the main driving factor for France pumped hydro storage market. This has encouraged investment in storage capacity that can provide longer-duration grid support and facilitate the integration of variable generation. In September 2025, as stated by the International Hydropower Association along with Eurelectric, it launched the Paris Pledge, by committing the regional hydropower sector to scale up pumped storage hydropower as a backbone for integrating variable renewables. More than 50 utilities and energy associations, such as EDF, have signed the pledge, encouraging the European Union and national policymakers to support long-duration storage through regulatory incentives and streamlined permitting, hence suitable for the standard pumped hydro storage market growth.

APAC Market Insights

The Asia Pacific pumped hydro storage market is expected to register the fastest growth from 2026 to 2035. The region’s prominence in this field is highly driven by the heightened energy demand and renewable energy targets. Countries across this region consider pumped storage as a highly essential element of long-duration energy storage, offering a way to manage intermittency associated with solar and wind generation. Based on the government data from Australia, which was published in February 2026, the Yarrabin (Phoenix) and Western Sydney Pumped Hydro projects in New South Wales, which is valued at USD 7 billion, have been declared critical state significant infrastructure by the NSW Government. It also stated that together, they could supply enough electricity to power over 1 million homes by providing long-duration storage to stabilize the grid and support peak demand as the state transitions from coal, hence denoting a positive pumped hydro storage market outlook.

The pumped hydro storage market in China is gaining traction as a result of strong emphasis on linking huge renewable energy generation with storage infrastructure. The country has an active pipeline of pumped storage projects that are efficiently supported by policy measures that integrate these systems into the central grid planning process. The country’s government in March 2025 stated that in Shanxi Province, a 1.4 million-kilowatt pumped-storage power station is set to begin construction in June 2025, with a total investment of about USD 1.53 billion. Moreover, this particular project will help integrate growing wind and solar generation by stabilizing the grid and reducing renewable energy curtailment. Therefore, with the continuous expansion of renewable energy capacity, pumped-storage projects have become highly essential to support the country’s dual carbon goals and long-term energy transition.

The strong government backing, renewable power integration, especially to address supply variability, is identified as the key enabler uplifting pumped hydro storage market in India. The country’s market is also carried forward by suitable policy initiatives and energy planning that emphasize the incorporation of storage assets that can support large solar and wind installations. Based on the government data in April 2025, the Central Electricity Authority (CEA) under the Ministry of Power, and the government have concurred on detailed project reports for six hydro pumped storage projects totaling 7.5 GW across Odisha, Karnataka, Maharashtra, Madhya Pradesh, and Andhra Pradesh. In addition, CEA also plans to concur at least 13 PSPs totaling 22 GW in 2025‑26, in which most are expected to be commissioned by 2030, reflecting the private sector participation and accelerating the country’s 200 GW pumped hydro potential.

Major Hydro Pumped Storage Projects in India (2024-25) by Capacity and State

|

Project Name |

Capacity (MW) |

State |

|

Upper Indravati |

600 |

Odisha |

|

Sharavathy |

2,000 |

Karnataka |

|

Bhivpuri |

1,000 |

Maharashtra |

|

Bhavali |

1,500 |

Maharashtra |

|

MP-30 |

1,920 |

Madhya Pradesh |

|

Chitravathi |

500 |

Andhra Pradesh |

Source: Ministry of Power

North America Market Insights

North America pumped hydro storage market is considered to be one of the strongest and most influential landscapes, highly driven by supportive regulatory frameworks and investment incentives for new PHS capacity and upgrades to existing facilities. The region also benefits from utility interest in long-duration storage, which continues to shape market development and modernization efforts. As of federal Energy Regulatory Commission (FERC) data in January 2026, it has issued an original license for the Goldendale Energy pumped storage hydroelectric project (1,200 MW) in Klickitat County, Washington, which is a closed-loop facility designed to store energy and support grid reliability. Therefore, such instances in the region will bolster the market growth by encouraging further investment in new pumped hydro projects, solidifying North America’s role as a leader in long-duration energy storage.

As developers and utilities explore opportunities to expand energy storage capacity, the U.S. pumped hydro storage market also continues to rise. Innovation in terms of modular and closed-loop designs is allowing projects to plan in areas with minimal environmental impact. On the other hand, public-private partnerships, coupled with federal incentives for clean energy infrastructure, are readily accelerating project approvals and financing. In March 2024, the U.S. DOE notified that its Water Power Technologies Office (WPTO) opened a technical assistance opportunity for hydropower developers, utilities, and stakeholders to support the development of hydropower hybrids and pumped storage hydropower projects. The program provides access to national laboratory expertise, modeling tools, and valuation support to help up to 18 projects improve planning, sizing, and operations over two to three years, hence denoting there is a huge opportunity for the pumped hydro storage market to grow in the upcoming years.

The extensive hydropower base, with growing interest in projects that support seasonal load balancing and renewable fluctuations are responsible factor for the upliftment of the pumped hydro storage market in Canada. The regulatory environment and physical geography are also the main assets propelling expansion, whereas the planned capacity reflects careful consideration of environmental and community impacts. According to the Ontario Government article published in January 2025, Ontario is moving ahead with pre-development work for the proposed pumped storage project in Meaford, which is in partnership with TC Energy and the Saugeen Ojibway Nation. It would deliver up to 1,000 MW of clean electricity storage, and the province is investing up to USD 285 million in feasibility studies and environmental assessments, hence positively impacting market growth.

Key Pumped Hydro Storage Market Players:

- ANDRITZ AG (Austria)

- Siemens Energy AG (Germany)

- Enel SpA (Italy)

- GE Vernova / GE Renewable Energy (U.S.)

- Voith GmbH & Co. KGaA (Germany)

- Duke Energy Corporation (U.S.)

- NextEra Energy, Inc. (U.S.)

- Torrent Power (India)

- Mitsubishi Heavy Industries (Japan)

- Toshiba Energy Systems & Solutions Corporation (Japan)

- Statkraft AS (Norway)

- China Three Gorges Corporation (China)

- Dongfang Electric Corporation (China)

- Harbin Electric Machinery Company (China)

- Edison SpA (Italy)

- Hydro‑related groups (Europe)

- Snowy Hydro Limited (Australia)

- Bharat Heavy Electricals Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ANDRITZ AG is one of the leading global suppliers of hydropower and pumped storage solutions, that is offering turnkey projects, turbine design, as well as digital control systems. The company has a strong presence across Europe, Asia Pacific, and North America, which is delivering both new installations and rehabilitation of existing plants.

- Siemens Energy AG is based in Germany, and the company offers complete hydropower solutions, which include turbines, generators, and automation systems for pumped storage plants around the world. Besides, the company is best known for its engineering knowledge, and it leverages digitalization and predictive maintenance technologies to improve efficiency and thereby reduce operational costs.

- Enel SpA is yet another leading pioneer in this field and is a vertically integrated energy company that develops, owns, and operates pumped hydro storage assets. The firm is mainly focused on renewable integration, long-duration energy storage, and sustainable grid management.

- GE Vernova has registered its position as a major supplier of hydropower and pumped storage solutions, offering water-to-wire systems that include turbines, generators, controls, and power electronics. In addition, the company has executed large projects in India, the U.S., and Europe, and is a pioneer in variable-speed pumped-storage technology, enabling faster response to load fluctuations.

- Voith GmbH & Co. KGaA is a prominent supplier of hydro and pumped storage equipment, which is specializing in turbines, pumps, and digital automation systems. The company is mainly focused on modernization and rehabilitation of existing plants along with new ones by integrating smart monitoring and predictive maintenance.

Below is the list of some prominent players operating in the global pumped hydro storage market:

The global pumped hydro storage market hosts well-established engineering firms, utilities, and regionally focused operators. Companies such as ANDRITZ, Siemens Energy, and GE Vernova dominate this sector through improved turbine technology and global project execution, whereas the players from emerging regions, such as Mitsubishi, Toshiba, and China Three Gorges, lead large-scale domestic deployments. Digitalization, hybrid energy systems, and regional partnerships are a few tactical strategies adopted by the pioneers to strengthen their market positions. In June 2025, ANDRITZ reported that it had secured a major order from Adani Green Energy Limited to supply pump turbines, motor generators, and electromechanical equipment for the 1,500 MW Tarali pumped storage project in Maharashtra, India. This is their second collaboration after the 500 MW Chitravathi project in 2023, hence making it suitable for standard market growth.

Corporate Landscape of the Pumped Hydro Storage Market:

Recent Developments

- In January 2026, Doosan Enerbility selected ANDRITZ to supply pump turbine units and related equipment for the 500 MW Yeongdong pumped storage plant in Chungcheong Province, South Korea, to support the country’s renewable energy expansion and grid stability.

- In June 2025, GE Vernova reported that it had commissioned the first of four 250 MW variable speed pumped storage units at THDC India Limited’s Tehri Pumped Storage Hydropower Plant, which will reach 2.4 GW and become India’s largest hydropower facility.

- Report ID: 4909

- Published Date: Feb 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Pumped Hydro Storage Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.