Precision Irrigation Market Outlook:

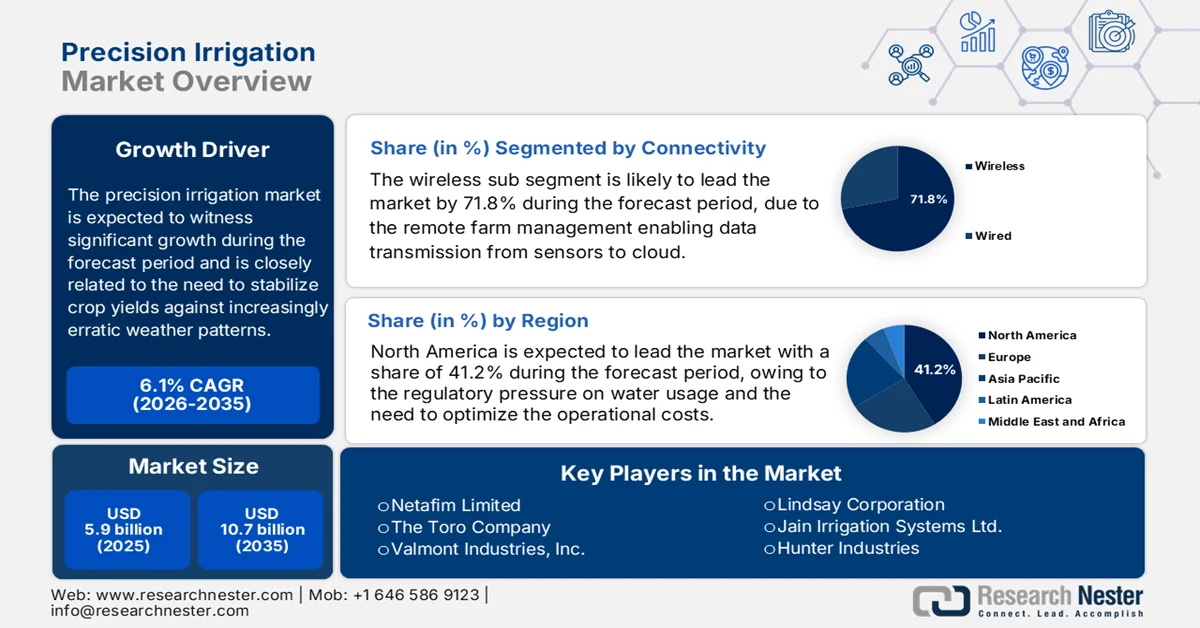

Precision Irrigation Market size was valued at USD 5.9 billion in 2025 and is projected to reach USD 10.7 billion by the end of 2035, rising at a CAGR of 6.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of precision irrigation is evaluated at USD 6.3 billion.

The global precision irrigation market is being shaped by the converging pressure of water resource depletion and the need to stabilize crop yields against increasingly erratic weather patterns. For industrial suppliers and agricultural equipment manufacturers, this translates to a growing demand from the commercial farming operations for systems that offer verifiable control over input application. According to the USDA January 2026 data, irrigation accounted for 47% of the total freshwater withdrawals, a volume that regulatory bodies are under pressure to reduce. On the other hand, the World Bank's August 2023 data depicts that the global freshwater extraction for agriculture has increased by 70%, which is unsustainable in the key aquifer-dependent growing regions. This impelled the agricultural enterprises to move beyond the traditional scheduling and invest in infrastructure that provides granular sensor-driven oversight of water distribution across vast acreages.

Moreover, the precision irrigation market is defined by the integration of remote monitoring capabilities into standard irrigation hardware, moving control from manual valve operation to centralized digital platforms. The automated irrigation systems, when paired with the soil moisture sensors, reduce water usage. According to the EPA, March 2026 data, the replacement of traditional systems with the WaterSense-labeled SMS has saved more than 390 billion gallons of water every year. This data is driving the procurement decisions among the cooperatives and large landholders, who view such infrastructure as capital investments with definable return timelines. Further, the farms utilizing precision technologies such as GPS-guided systems and variable rate irrigation accounted for a growing share of irrigated acreage, specifically in water-stressed western states where regulatory oversight is most acute. For upstream suppliers, this indicates a market increasingly defined by retrofitting existing large-scale pivot and drip systems with aftermarket control components, rather than solely relying on new system installations.

Key Precision Irrigation Market Insights Summary:

Regional Highlights:

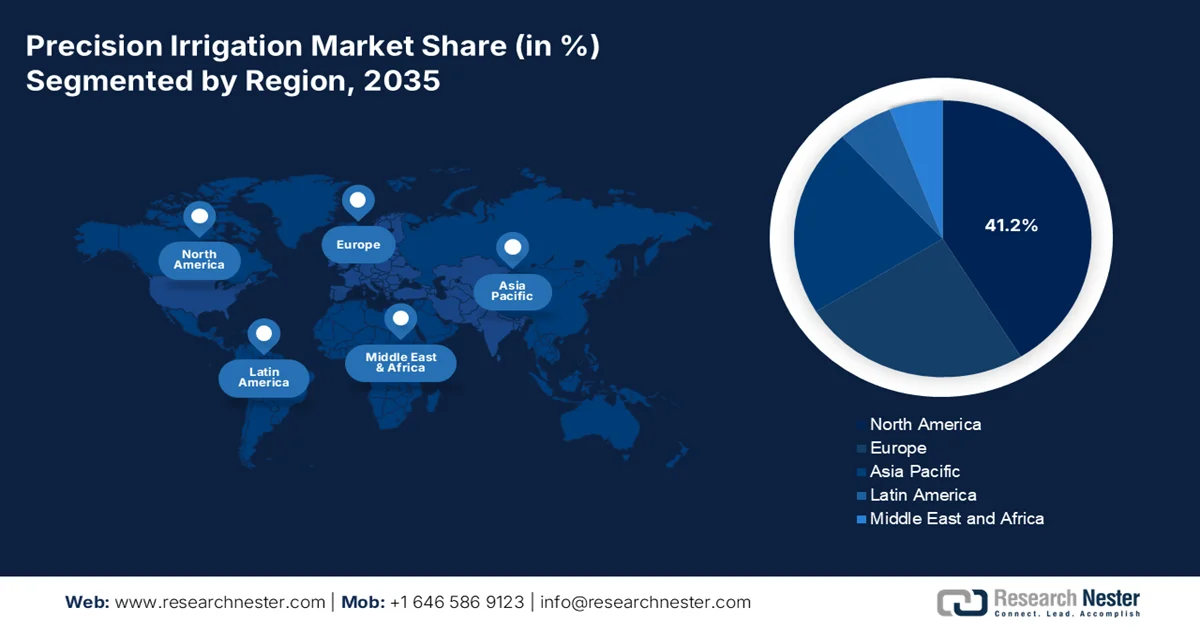

- In the precision irrigation market, North America is anticipated to command a 41.2% revenue share by 2035, attributed to stringent water-use regulations and increasing investments in cost-efficient irrigation technologies across large-scale farms

- Asia Pacific is projected to register the fastest growth during 2026–2035, gaining substantial share stimulated by strong government subsidy programs and rising adoption of digital precision irrigation solutions

Segment Insights:

- In the precision irrigation market, the wireless sub-segment under connectivity is projected to capture a dominant 71.8% share by 2035, fueled by the rapid expansion of advanced wireless communication protocols enabling real-time remote farm management

- Closed-loop systems within the system type segment are expected to maintain their leading position through 2035, accounting for a significant share impelled by the rising need for automated irrigation solutions to enhance water efficiency and resource optimization

Key Growth Trends:

- Rising agricultural water scarcity

- Global food security programs

Major Challenges:

- Connectivity and infrastructure deficit

- Fragmented customer base

Key Players: Netafim Limited, The Toro Company, Valmont Industries, Inc., Lindsay Corporation, Jain Irrigation Systems Ltd., Hunter Industries, Rain Bird Corporation, Rivulis Irrigation Ltd., Nelson Irrigation Corporation, EPC Industries Limited, Horizon Irrigation, Mahindra EPC Irrigation Ltd., T-L Irrigation Company, Mottech M. Technologies Ltd., Rubicon Water, Galcon, Bermad CS Ltd., Orbia Advance Corporation, Weenat, Husqvarna Group.

Global Precision Irrigation Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.9 billion

- 2026 Market Size: USD 6.3 billion

- Projected Market Size: USD 10.7 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (41.2% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, India, Germany, Brazil

- Emerging Countries: Australia, Japan, South Korea, Spain, Italy

Last updated on : 25 March, 2026

Precision Irrigation Market - Growth Drivers and Challenges

Growth Drivers

- Rising agricultural water scarcity: Water scarcity is reshaping the agricultural policy frameworks, directly influencing the demand for precision irrigation market technologies that enable precise water delivery at the farm level. According to the Geosciences Libre Texts December 2023 data, the irrigation withdrawals reached around 118 billion gallons per day, taking maximum total freshwater withdrawals in the U.S., making irrigation efficiency a key policy priority. Moreover, the governments are implementing stricter groundwater extraction rules and irrigation practices. Similar regulatory frameworks are expanding globally as water availability declines. These measures encourage the large-scale farms to transition from the traditional flood irrigation to digitally managed irrigation systems capable of monitoring soil moisture and optimizing water application.

Sources of Fresh and Salt Water on Earth, 2023

|

Water Source |

Freshwater Volume (cubic kilometers) |

Salt Water Volume (cubic kilometers) |

|

Oceans, Seas, and Bays |

0 |

1,338,000,000 |

|

Ice Sheets, Glaciers, and Permafrost |

24,364,000 |

0 |

|

Groundwater |

10,530,000 |

12,870,000 |

|

Surface Water |

122,210 |

85,400 |

|

Atmosphere |

12,900 |

0 |

|

Subtotals |

35,029,110 |

1,350,955,400 |

|

Grand Total (rounded) |

- |

1,386,000,000 |

Source: Geosciences Libre Texts December 2023

- Global food security programs: Government-led food security initiatives are surging the adoption of the precision irrigation market as countries seek to increase crop yields while managing limited water resources. According to the World Bank, October 2025 data, only 20% of the cultivated land worldwide is irrigated, but it contributes to 40% of the global food production. This highlights the productivity advantage of irrigation technologies. Governments are therefore directing funding toward irrigation modernization within national food security plans. Furthermore, the global population growth continues to pressure agricultural supply chains. Public programs targeting higher crop productivity per unit of water are expected to accelerate procurement of automated irrigation equipment, soil monitoring sensors, and data-driven irrigation scheduling technologies across commercial farming operations.

- Smart farming policy support: Government initiatives supporting digital agriculture are stimulating the adoption of sensor-based irrigation management systems. The technologies in the precision irrigation market often integrate with the broader digital agricultural frameworks that include remote sensing, field data analytics, and automated farm management platforms. Besides, digital agriculture technologies are increasingly supported via federal research funding and agricultural innovation programs. Federal agencies and research institutions continue to invest in smart farming systems that improve water use efficiency and farm productivity. Moreover, the public agricultural extension programs provide training and technical assistance to farmers adopting precision irrigation technologies. These initiatives lower the adoption challenges and increase the awareness of data-driven irrigation strategies.

Challenges

- Connectivity and infrastructure deficit: The precision irrigation market relies on the real-time data transmission from the field sensors to cloud platforms, which requires robust wireless connectivity. However, a vast majority of the agricultural land is located in rural areas with poor internet or cellular infrastructure. This connectivity issue is identified as a primary challenge for market implementation, as smart systems cannot function optimally without reliable data flow. Moreover, this limits the market penetration of an advanced closed-loop system that depends on constant communication.

- Fragmented customer base: The precision irrigation market is huge, and it ranges from the large commercial farms with many smallholders with limited technical knowledge. This fragmentation makes it costly and complex for suppliers to reach and educate end users effectively. Moreover, the agricultural water management in Africa has low access to extension services in regions such as Southern Africa, which severely hampers the adoption of new technologies. The farmers lack the training to use precision tools effectively, leading to poor ROI and stalled adoption.

Precision Irrigation Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 5.9 billion |

|

Forecast Year Market Size (2035) |

USD 10.7 billion |

|

Regional Scope |

|

Precision Irrigation Market Segmentation:

Connectivity Segment Analysis

Under the connectivity segment, the wireless sub-segment is leading and is poised to hold the share value of 71.8% by the end of 2035 in the precision irrigation market. The expansion of wireless communication protocols, such as LoRaWAN, cellular IoT, and satellite connectivity, has revolutionized remote farm management by enabling real-time data transmission from the in-field sensors to cloud-based platforms without the need for costly physical infrastructure. This shift allows farmers to monitor soil moisture, weather conditions, and equipment status from mobile devices, significantly reducing the labor costs and response times. According to the GAO January 2024 data, nearly 27% of the U.S. farms used internet-connected sensors for some aspect of crop production, highlighting the acceleration of the mainstream adoption of wireless technologies in modern agriculture.

System Type Segment Analysis

Within the system type segment, the closed-loop systems are leading in the precision irrigation market. These fully automated systems utilize a feedback mechanism where the sensors continuously monitor soil and crop conditions, automatically activating or deactivating the irrigation without human intervention. Moreover, this technology is critical for optimizing water use efficiency, reducing runoff, and ensuring crops receive precisely the right amount of water at the right time. The growing urgency of water scarcity and the need for precision in fertilizer application are driving the large-scale agricultural operations to replace manual scheduling with these intelligent systems. In addition, automated irrigation systems are used, demonstrating a significant increase in adoption as growers seek to conserve groundwater resources.

End user Segment Analysis

Commercial farms are the leading sub-segment in the precision irrigation market and are expected to hold the largest share by the end of 2035. Large-scale agricultural enterprises are the fastest adopters of precision irrigation technologies due to their substantial capital resource economies of scale and the imperative to maximize the yield on extensive acreages. These operations use advanced technologies such as variable rate irrigation and GPS-guided systems to manage field variability, optimize input costs, and ensure consistent crop quality. Moreover, the return on investment for the commercial farms is realized via significant water and energy savings, reduced dependency, and higher crop values. As per the report from the NITI June 2025 data, the remote sensing irrigation system has reduced 50% of the water use in commercial farms compared to the traditional methods, showing the economic and environmental incentives driving this segment.

Our in-depth analysis of the precision irrigation market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Component |

|

|

System Type |

|

|

Technology |

|

|

End user |

|

|

Application |

|

|

Connectivity |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Precision Irrigation Market - Regional Analysis

North America Market Insights

The North America is dominating and is expected to hold the regional revenue share of 41.2% by the end of 2035. The precision irrigation market in North America is driven by the regulatory pressure on water usage and the need to optimize the operational costs on large-scale commercial farms. In the U.S., funding is allocated for on-farm irrigation improvements, directly funding the hardware upgrades. Moreover, the Canada growth drivers center on the sustainability frameworks and provide direct incentives for adopting precision irrigation technologies that reduce nitrogen emissions and water use. With extensive existing center pivot and drip infrastructure, farmers are investing in after-market control components, soil sensors, and VRI packages rather than full system replacements. These trends are promoting the use of real-time data to schedule irrigation, moving farmers away from calendar-based methods toward actual crop water demand.

The expanding irrigation-intensive agriculture and federal support programs are shaping the precision irrigation market in the U.S. According to the USDA January 2026 data, the country reported 54.9 million acres of irrigated crop and pastureland, highlighting the scale of irrigation-dependent agricultural production. Moreover, the data also notes that farms using irrigation generate more than 50% of the total value of U.S. crop sales while accounting for less than 17% of harvested cropland, indicating significantly higher productivity on irrigated land. On the other hand, the GAO January 2024 data depicts that the USDA and the National Science Foundation allocated nearly USD 200 million for precision agriculture research and development, supporting technologies such as automated irrigation systems, variable rate applications, and sensor-based monitoring. Despite these initiatives, 27% of U.S. farms and ranches used precision agriculture practices as of 2023; therefore, there is an active growth in the market expansion.

The increasing adoption of advanced technologies to improve productivity, resource efficiency, and sustainability is shaping the precision irrigation market in Canada. According to the Government of Canada's May 2023 data, nearly 95,713 farms (50.4% of all farms in Canada) reported using at least one form of technology, reflecting a strong shift toward precision farming practices that support efficient water and input management. Additionally, 16.1% of farms reported using variable-rate input application technologies, which utilize sensor or GPS-based data to adjust the application of inputs such as fertilizer, chemicals, and water across fields, a capability closely aligned with precision irrigation systems. Technology adoption is particularly high among large farms, with 86.9% of farms in the USD 1 million to USD 1.99 million revenue category reporting the use of at least one technology, indicating that high-revenue agricultural operations are leading the transition toward data-driven farm management. These trends are supported by broader national efforts to improve sustainable agriculture.

APAC Market Insights

Asia Pacific is projected to emerge as the fastest-growing region and is poised to expand at the highest CAGR during the assessed period, 2026 to 2035. The precision irrigation market is driven by the intersection of acute water scarcity, government-led food security initiatives, and the fragmentation of landholdings that necessitates efficient input use. The primary drivers across the region are direct government subsidy programs that lower the capital barrier for small and marginal farmers. Besides India’s Per Drop More Crop scheme and China’s national water saving policies, which channel billions in public funding directly into drip and sprinkler adoption. Further, another trend is the rapid digitalization of agriculture with the mobile-enabled advisory services and low-cost precision irrigation controls via smartphone. The region's growth is defined by the large-scale commercial farms and advanced rate variable technology.

The precision irrigation market in India is expanding as increasing water demand and agricultural productivity targets drive the adoption of micro irrigation and precision farming technologies. According to the NWDA October 2023 data, India’s total utilizable water resources were about 1,123 billion cubic meters, of which 690 BCM comes from surface water and 433 BCM from groundwater, with irrigation accounting for around 80% of total water consumption. Moreover, the agricultural water demand is projected to increase to 910 BCM by 2025 and 1,072 BCM by 2050, highlighting the need for more efficient irrigation technologies. On the other hand, the CEEW September 2023 data depict that the Tamil Nadu Precision Farming Project reported yield improvements ranging from 30% to 200% for horticulture crops using irrigation-cum-fertigation systems. These data show a rising expansion of precision irrigation across commercial farms and horticulture production systems in India.

Impact of Precision Farming Technologies

|

Impact Area |

Technology / Practice |

Measured Benefit |

|

Crop Yield Improvement |

Micro-irrigation and fertigation under Tamil Nadu Precision Farming Project (TNPFP) |

Yield improvements ranged 30% 200% across horticulture crops compared with conventional irrigation |

|

Productivity Increase |

Micro-irrigation in orchard crops and vegetables |

Yield improvement 10%–60% compared with traditional irrigation methods |

|

Farm Productivity Growth |

Micro-irrigation adoption |

42.4% increase in fruit crop productivity and 52.7% in vegetables |

|

Water Efficiency |

Drip and sprinkler irrigation systems |

Water savings 30%–70% in orchards and 35%–60% in vegetables |

|

Fertilizer Efficiency |

Precision nutrient management and sensors |

Nitrogen fertilizer use reduced 10–20 kg per hectare |

|

Energy Savings |

Precision irrigation and laser land levelling |

Electricity savings around 755 kWh per hectare in rice–wheat systems |

|

Emission Reduction |

Precision farming technologies |

25–30% reduction in greenhouse gas emissions |

|

Input Reduction |

GIS-based patch spraying |

Herbicide reduction 50–75% |

Source: CEER September 2023

The efforts to improve agricultural water efficiency and modernize farming systems are driving the precision irrigation market in China. According to the People’s Republic of China's March 2025 data, China has developed over 1 billion mu of farmland and irrigation networks stretching to over 10 million kilometers, reflecting the scale of irrigation-dependent crop production. However, water scarcity remains a major policy concern, as China’s per capita water resources are about 2,100 cubic meters as per the Hudson Institute, March 2924, prompting the government to prioritize efficient irrigation technologies. Besides the increased spending on agriculture, forestry, and water affairs supports irrigation modernization and water conservation programs. As China seeks to secure food production while reducing water consumption in agriculture, precision irrigation technologies are expected to gain wider adoption across commercial farms, state agricultural projects, and modern agricultural demonstration zones.

Europe Market Insights

Europe market is growing significantly and is shaped by the convergence of the common agricultural policy, environmental architecture, and region-specific water stress patterns. The primary driver of the precision irrigation market in Europe is the CAP’s enhanced conditionality, which directs payments to environmental standards, including water management, pushing the commercial farms to invest in monitoring and precision application hardware. On the other hand, the increasing adoption of closed-loop systems in water-scarce southern Europe, where the competition for water resources between agriculture and tourism is increasing, is putting regulatory pressure on abstraction volumes. Moreover, the soil moisture sensors and flow meters are expanding across the continent as farms seek to modernize existing infrastructure without full system replacement. Funding flows through national CAP Strategic Plans, with member states allocating varying portions of their rural development budgets to irrigation modernization.

Strong agricultural production base and the growing adoption of smart farming technologies are driving the precision irrigation market in Germany. According to the GTAI 2025 data, Germany is Europe’s second-largest agricultural production nation with an output value of USD 80 billion, highlighting the scale of commercial farming operations that are increasingly integrating digital agricultural solutions. Moreover, about 16.6 million hectares, nearly half of Germany’s total land area, were used for agriculture, with arable farming accounting for more than 70% of agricultural land use, creating significant demand for technologies that optimize water and input application across large crop areas. These trends, combined with increasing pressure to improve resource efficiency and sustainability in farming, are expected to support the integration of precision irrigation technologies across Germany's commercial farms and agricultural enterprises.

The government backed agricultural innovation programs and the adoption of advanced farming technologies are propelling the precision irrigation market in the UK. According to the Government of the UK, April 2025 data, nearly USD 58 million is funded to support the agricultural R&D projects, including technologies that are designed to optimize water use and improve crop productivity. Moreover, this funding is distributed via multiple initiatives, including the Farming Innovation Programme and the Accelerating Development of Practices and Technologies competition, which allocated up to USD 26.2 million in 2025 to 2026 to help farmers test and implement new agricultural technologies on their farms. As UK agriculture continues to transition toward climate-resilient and resource-efficient production systems increased adoption of precision irrigation solutions across commercial farms and agricultural research projects.

Key Precision Irrigation Market Players:

- Netafim Limited (Israel)

- The Toro Company (U.S.)

- Valmont Industries, Inc. (U.S.)

- Lindsay Corporation (U.S.)

- Jain Irrigation Systems Ltd. (India)

- Hunter Industries (U.S.)

- Rain Bird Corporation (U.S.)

- Rivulis Irrigation Ltd. (Israel)

- Nelson Irrigation Corporation (U.S.)

- EPC Industries Limited (India)

- Horizon Irrigation (Australia)

- Mahindra EPC Irrigation Ltd. (India)

- T-L Irrigation Company (U.S.)

- Mottech (M. Technologies) Ltd. (Israel)

- Rubicon Water (Australia)

- Galcon (Israel)

- Bermad CS Ltd. (Israel)

- Orbia Advance Corporation (Mexico)

- Weenat (France)

- Husqvarna Group (Sweden)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Netafim Limited is a global pioneer in the precision irrigation market, having fundamentally transformed agricultural practices via its invention of the drip irrigation technology. The company has made significant advancements by integrating smart data analytics and IoT-enabled monitoring systems into its drip and micro irrigation solutions.

- The Toro Company is a key manufacturer in the precision irrigation market, leveraging its extensive expertise in turf management and agriculture to develop advanced water-saving technologies. The company has made significant advancements by integrating the precision irrigation data into its wireless and smart controller systems. In 2025, the company made a net sales of USD 4.51 billion.

- Valmont Industries Inc is a dominant player in the precision irrigation market, renowned globally for its Valley brand center pivot and the linear move irrigation systems. The company has made significant advancements by integrating the precision irrigation data into its proprietary control and monitoring platforms. In 2024, the company made a net sales of USD 4.1 billion.

- Lindsay Corporation stands as a technological leader in the precision irrigation market, best known for its Zimmatic center pivot systems and field management software. The company has made significant advancements by integrating the precision irrigation data into its innovative mobile and web-based platforms.

- Jain Irrigation Systems Ltd is a multinational and dominant player in the precision irrigation market, leveraging its deep agricultural expertise to address the water scarcity challenges. The company has made significant advances by integrating precision irrigation data into its comprehensive drip and sprinkler systems, combined with the mobile-based advisory services.

Here is a list of key players operating in the global precision irrigation market:

The global precision irrigation market is highly competitive and moderately consolidated, led by established multinational corporations alongside innovative regional players. The key strategic initiatives among top companies include the integration of IoT, AI, and cloud-based data analytics for remote monitoring and automated scheduling. Major players are aggressively pursuing geographic expansion via acquisition and partnerships to penetrate emerging markets in the Asia Pacific and Africa. For example, in August 2024, Rain Bird Corporation, a leading global irrigation company, acquired the Jordanian and Mexican assets of Adritec Group International. Further, there is a significant focus on developing water and energy-efficient solutions, such as drip and sprinkler systems, to address the global water scarcity concerns and stringent agricultural regulations. Companies are also shifting toward offering comprehensive farm management solutions rather than just hardware.

Corporate Landscape of the Precision Irrigation Market:

Recent Developments

- In February 2026, Orbia Advance Corporation, the global leader in precision agriculture solutions, announced two major water stewardship initiatives with Amazon India that will save approximately 175 million liters of water annually across Bengaluru’s western agricultural belt and 150 million liters across the northern Hyderabad agricultural belt, a combined total of approximately 325 million liters annually.

- In December 2024, Weenat, the European leader in soil moisture monitoring, announces its acquisition of CoRHIZE, a specialist in irrigation management solutions. This strategic step further advances efforts to help the agricultural sector optimize water management across France and Europe.

- In August 2024, Husqvarna Group signed an agreement to acquire the Brazilian company InCeres, a digital platform in the Professional light agriculture segment. InCeres is an expert in soil analysis that facilitates decision-making and improves productivity for farmers

- Report ID: 8472

- Published Date: Mar 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.