Portable Fuel Cell Market Outlook:

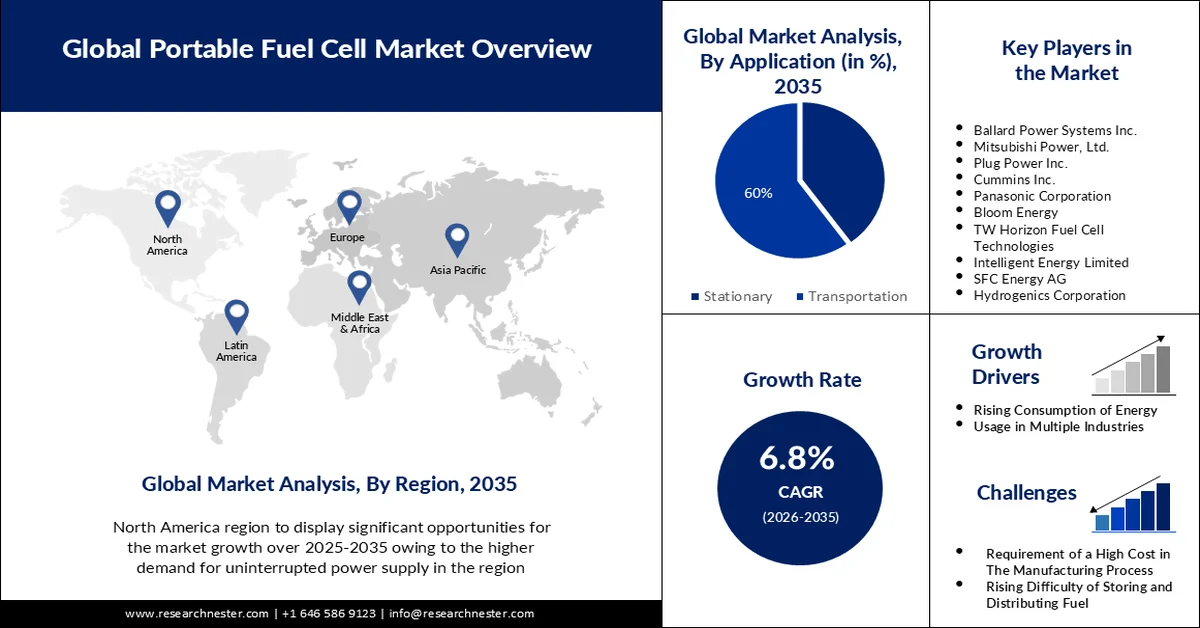

Portable Fuel Cell Market size was valued at USD 403.51 million in 2025 and is likely to cross USD 779.05 million by 2035, registering more than 6.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of portable fuel cell is estimated at USD 428.2 million.

The primary growth factor for the development of the global market during the forecast period is the rising demand for energy along with the need for an uninterrupted power supply to carry out various applications and services. As per recent statistics, it is forecasted that the global electricity demand is expected to considerably grow by the end of 2023. Furthermore, it is stated that an additional 2,500 terawatt hours (TWh) of electricity demand is anticipated to be added by 2025. Thus, this 9% growth would take the global electricity demand to almost 30,000 terawatt hours (TWh).

A portable fuel cell is a technologically advanced device that acts as a battery, and does not need recharging or does not run down, as long as fuel is supplied as an oxidant. Hence, these portable fuel cells are a high-demand product in numerous industries including automotive, electrical & electronics, and others. This is considered to be a major factor for market growth during the predicted period.

Key Portable Fuel Cell Market Insights Summary:

Regional Insights:

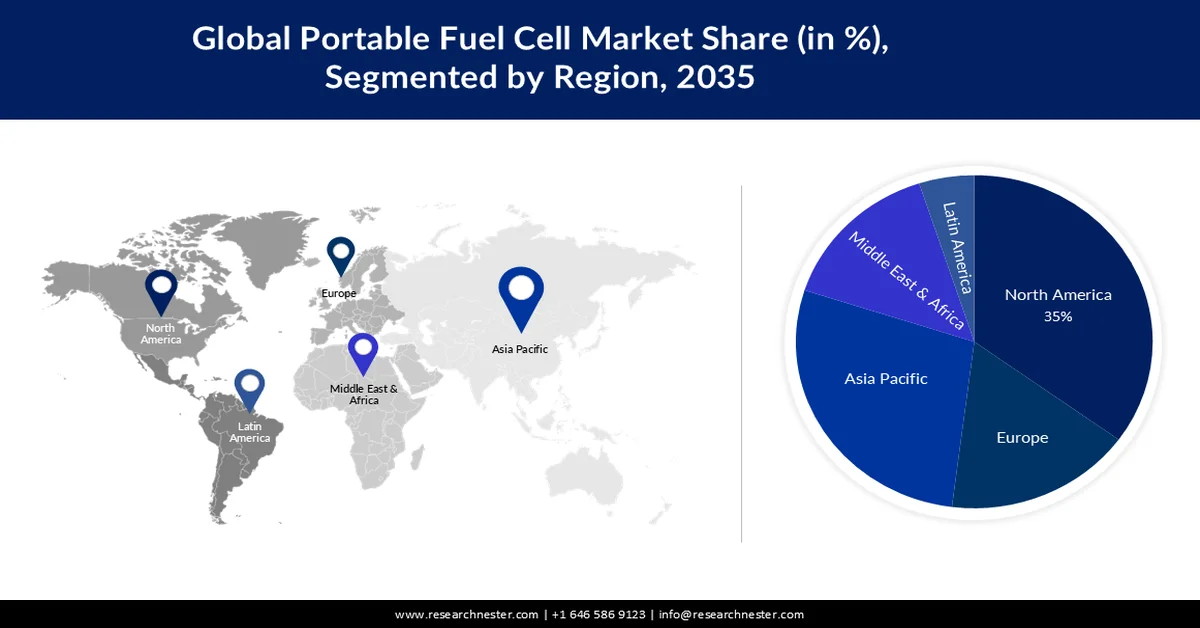

- North America is projected to command a 35% revenue share by 2035 in the portable fuel cell market, attributed to the expanding number of data centers and the increasing fleet of fuel cell vehicles across the region.

- Asia Pacific portable fuel cell market is anticipated to witness significant growth during 2026–2035, propelled by rising EV demand in Japan and South Korea alongside growing government investments in clean power generation.

Segment Insights:

- The hydrogen segment in the portable fuel cell market is expected to account for approximately 31% share by 2035, driven by the rising preference for hydrogen to reduce fossil fuel dependence and carbon emissions.

- The automotive segment is projected to secure a significant share by 2035, fueled by increasing automobile production and the high utilization of portable fuel cells for efficient vehicle electrical system operations.

Key Growth Trends:

- Rapid Growth of the Automotive Industry

- Escalation in the Electronics and Electrical Industry

Major Challenges:

- Requirement of High Cost in the Manufacturing Process

- Inadequate Infrastructure to Support Hydrogen Distribution

Key Players: Thermo Fisher Scientific Inc., Boehringer Ingelheim GmbH, Bayer AG, Novartis AG, Sanofi-aventis Groupe, Abbott Laboratories, Merck & Co., Inc., Validus Pharmaceuticals LLC, Teva Pharmaceutical Industries Ltd., Siemens Healthcare GmbH.

Global Portable Fuel Cell Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 403.51 million

- 2026 Market Size: USD 428.2 million

- Projected Market Size: USD 779.05 million by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, South Korea, United Kingdom

- Emerging Countries: Japan, South Korea, China, Germany, USA

Last updated on : 25 February, 2026

Portable Fuel Cell Market - Growth Drivers and Challenges

Growth Drivers

-

Rapid Growth of the Automotive Industry - A portable fuel cell is a very vital component in the automotive industry because automobiles such as buses, utility vehicles, cars, scooters, and bicycles require a secondary power source to recharge the batteries when needed. Thus, the rapid growth in the automotive industry is estimated to generate favorable opportunities for the utilization of portable fuel cells by vehicle manufacturers. As per recent records, it has been stated the global automotive sector generated a revenue of approximately USD 3 trillion in 2021. This figure is anticipated to constantly rise and reach almost USD 8 trillion by 2035.

-

Escalation in the Electronics and Electrical Industry - The demand for consumer electronic items such as laptops, mobiles, tablets, television, fridge, and others have been on a constant rise. As a result, the usage of portable fuel cells in electronics has also grown considerably, as fuel cells are capable of producing electrical power from the electrochemical process and further use the chemical substance/material as a source of fuel. Therefore, the expansion of the electronics and electrical industry is estimated to drive portable fuel cell market in the assessment period.

- Rising Carbon Footprint Across the World - With rapid urbanization and industrialization, the amount of carbon emission has also increased. This factor is estimated to surge the demand for portable cell fuels to curb energy combustion while lowering the release of carbon and saving the environment. As per the data released by the International Energy Agency (IEA), it has been stated that the global carbon dioxide (C02) emission from energy combustion and industrial processes rose 10 0.9% or 321 Mt in 2022 to a new all-time high of 36.8 Gt.

Challenges

-

Requirement of High Cost in the Manufacturing Process – During the initial stage, a high amount of investment is required to manufacture portable fuel cells using metals such as platinum and iridium that is frequently needed as catalysts in these devices. Furthermore, owing to higher costs of raw material also makes manufacturing portable fuel cells expensive.

-

Inadequate Infrastructure to Support Hydrogen Distribution

- Rising Difficulty in Storing and Distributing Fuel

Portable Fuel Cell Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 403.51 million |

|

Forecast Year Market Size (2035) |

USD 779.05 million |

|

Regional Scope |

|

Portable Fuel Cell Market Segmentation:

Fuel Type Segment Analysis

The hydrogen segment in the portable fuel cell market is estimated to gain the largest revenue share of about 31% in the year 2035, owing to the rising preference for hydrogen which lessens the reliance on fossil fuels and lowers the emission of carbon dioxide for protection of the environment. Further, the demand for hydrogen is estimated to increase as the result of several government regulations to save nature and the earth is anticipated to bolster segment growth in the estimated period. For instance, in 2021, the world's demand for hydrogen increased by 5% to 94 Mt, primarily owing to increased activity in the chemical and refining industries. Moreover, the consumption of hydrogen was 91 Mt in 2019.

End User Segment Analysis

Portable fuel cell market from the automotive segment is expected to garner a significant share in the year 2035. This can be impelled by the rising demand & production rate of automobiles and the high utilization rate of the portable fuel cell to ensure the proper functioning of the electrical system of the vehicle. The International Organization of Motor Vehicle Manufacturers (OICA), released global sales of vehicle statistics which revealed that it rose to 56 million in 2021 from 53 million in 2020. Whereas, the global production of vehicles was calculated to be 57 million in 2021.

Our in-depth analysis of the global market includes the following segments:

|

Fuel Type |

|

|

Application |

|

|

End User |

|

|

Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Portable Fuel Cell Market - Regional Analysis

North America Market Insights

North America industry is set to dominate majority revenue share of 35% by 2035. The major growth factor for the market expansion in the region can be attributed to the rise in the number of data centers and the growing count of fuel cell vehicles in the region which generates the need for a portable fuel cell for proper functioning in the longer run. According to reports, more than 2,600 data centers in the United States use more than 1.5% of the country's total energy. Moreover, there are now nearly 328 colocation data centers, around 24 network fabrics, and over 500 service providers in Canada. Besides this, as of February 2019, there were more than 6,500 fuel cell vehicles on American roads.

APAC Market Insights

The Asia Pacific portable fuel cell market is estimated to grow significantly during the time period between 2026-2035. The market in the Asia Pacific region is estimated to witness noteworthy growth over the forecast period on the back of rising demand for EVs in Japan and South Korea, along with increasing usage of fuel cells in vehicles in the region. Apart from this, the growing government investments in clean power generation are also expected to boost market growth in the region.

Portable Fuel Cell Market Players:

- Ballard Power Systems Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Plug Power Inc.

- Cummins Inc.

- BASF SE

- Medis TECHNOLOGIES

- Bloom Energy

- TW Horizon Fuel Cell Technologies

- Intelligent Energy Limited

- SFC Energy AG

- Hydrogenics Corporation

Recent Developments

- Mitsubishi Power, Ltd. Received an order pan-Europe for a solid oxide fuel cell (SOFC). The system will be put into operation by March 2022 and is developed to supply heat and electricity independently of the existing power grid.

- Plug Power Inc., a global leader in energy solutions announced the launch of its new product a 30-kilowatt (kW) hydrogen fuel cell engine.

- Report ID: 3701

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.